Abstract

This paper presents a highly granular database of nearly 500 capital flow management measures (CFMs) that cover 14 instruments and 49 countries at monthly frequency between 2008 and 2021. It sheds light on the incidence of CFMs along previously unexplored dimensions such as the nature of instruments used, and the asset class and direction of capital flows to which they were targeted. The paper also presents new indices of capital account policies to characterize the usage, stance and intensity of CFM policies. In comparison with existing indices of capital controls, we find that our data reveal significant intra-year changes in CFMs even when other indices exhibit stability over long periods. We find that a “stock-taking” version of our data generates similar assessments about episodic versus long-standing controls as some other indices, suggesting that existing indices may be capturing low-frequency characteristics of capital account policies. Mahir Binici is a senior economist in the European Department of the IMF. Previously, he worked in the Strategy, Policy, and Review Department, where he focused on external policy issues, including those related to India. Prior to joining the IMF, he held positions as an economist at the Central Bank of Turkey and the European Central Bank. Mitali Das is an Advisor in the Fiscal Affairs Department of the IMF. Previously, she was Co-Chair of the IMF flagship publication, External Sector Report, led the analytical work on unemployment dynamics and labor shares for the World Economic Outlook, served on the IMF missions to China, Japan, and Nauru, and in the Office of the Chief Economist. Prior to the IMF, Ms. Das held academic appointments at Columbia University, Harvard University, Dartmouth College, and the University of California Davis. Evgenia Pugacheva is a research officer in the Research Department of the IMF, where she works on the World Economic Outlook report. Her research focuses on the macroeconomic implications of climate change, international trade, and the COVID-19 pandemic. Prior to joining the IMF, she worked at the World Bank on the World Development Report.

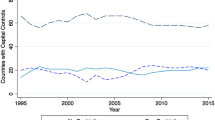

Source: Authors’ compilation from the Taxonomy

Source: Authors’ compilation from the Taxonomy

Source: International Financial Statistics and authors' calculations. Notes: Data for in-sample countries and 111 other countries in 2018. Weights for BOP are 6-quarter moving averages as of the fourth quarter of 2018. Weights for IIP are based on annual data

Source: Authors’ compilation from the Taxonomy.

Similar content being viewed by others

Notes

The entire database is available from any of the authors and can be requested by email. It will be posted on the internet at the time of the publication of the paper.

Throughout the paper, we use “capital inflows” to refer to liability flows and “capital outflows” to refer to asset flows. Following the residency-based principle of the Balance of Payments, liability flows pertain to capital flows from or to nonresidents while asset flows pertain to capital flows from or to residents. Throughout, “inflows” and “outflows” are in gross terms. Gross inflows consist of non-residents’ net purchases of domestic assets; gross outflows consist of residents’ net purchases of foreign assets.

In practice, the assessment for each measure is carried out through an iterative inter-departmental process involving the IMF’s Strategy, Policy and Review Department, Legal Department, and the Monetary and Capital Markets Department. IMF mission teams representing the country that is implementing the CFM provide all necessary inputs for this assessment, but are not otherwise involved in judging whether the measure is included in the Taxonomy. This process is designed to ensure a consistent approach in assessing whether a capital account policy measure qualifies as a CFM and it is applied equally across all member countries.

That information is available in IMF internal records pertaining to the Taxonomy and the authors of this paper have been able to access and use it.

We also make the database available at quarterly frequency to match the frequency at which most macroeconomic data are available.

We also assign +1 to measures whose enforcement was strengthened. There are 4 such measures. There is an additional CFM whose period of enforcement was extended, also assigned +1.

We write “inflow measures” (IM) as shorthand for CFMs on gross capital inflows, and analogously use “outflow measures” (OM) for capital flow management measures on gross capital outflows. The Taxonomy follows the BOP definition of gross inflows (non-residents’ net purchases of domestic assets) and gross outflows (residents’ net purchases of foreign assets).

There is a small minority of cases in which CFMs are neither price-based nor administrative or can be both.

The terminology in the literature is either “administrative” or “quantity-based” controls for CFMs such as quotas, approvals, outright prohibitions that are not market-based measures (see Ariyoshi et al. 2000 and Magud et al. 2018). We use the term “administrative” for these measures, which encompass both quantity based CFMs as well as the stricter enforcement of existing regulations.

We write “net inflow measures” to refer to those measures that are counted in NII, i.e., tightening measures on inflows and easing measures on outflows; we use “net outflow measures” for those measures counted in NOI, i.e., tightening measures on outflows and easing measures on inflows.

The weighted indices are constructed at quarterly rather than monthly frequency since that is the frequency at which BOP data are made available.

To illustrate, a change in the limit on portfolio debt purchases by non-residents receives a weight equal to the average share of portfolio debt flows in liability flows in the k most recent quarters.

For discussion on the incidence of CFMs in the Asia/Pacific Region, see Finger and Lopez Murphy (2019).

The exception was Iceland, which instituted a repatriation requirement along with a range of capital controls in November 2008 (when, compared to its level 12 months earlier, the kronur depreciated by 133 percent vis-à-vis the U.S. dollar and 71 percent in real effective terms) and removed it in March 2017.

This pattern broadly holds up when we exclude Greece and Ukraine, to which a significant number of actions on outflows can be traced.

Evidence that tightening of capital controls on inflows reflected investors’ abilities to circumvent existing controls is given in Simone and Sorsa (1999), De Gregório et al. (2000), Forbes (2007) and Cowan and De Gregorio (2007) for Chile in the 1990s; Cardoso and Goldfajn (1998) and Jeanne et al. (2012) for Brazil. Ostry et al. (2010) note “More relevant is the case of countries…which will need to design and implement new controls and likely strengthen them over time in the face of circumvention.”

In Fernandez et al. (2016) the original scale is 0 = low restrictions; 1 = high restrictions; and CFMs original direction is positive numbers = tightening, negative numbers = easing.

The correlations cannot be calculated in all pairs where the standard deviation in either country is zero.

See Quinn (1997), pages 541-544 for the details of the subjective assessments used in coding the data from the AREAER.

See Chinn and Ito (2006), pages 169-170 for the construction of their index, which is defined as the first principle component of the four AREAER binary variables discussed above. As noted by Chinn and Ito (P. 169-170) “by the nature of its construction, one may argue that the [index] measures the...existence of different types of restrictions” (emphasis is ours).

See Fernandez et al. (2016), pages 554-556 for details. As noted by the authors (P. 550), “…this extended and updated data set reports the presence or absence of capital controls, on an annual basis, for 100 countries over the period 1995–2013” (emphasis is ours).

The publicly available Quinn database currently goes through 2018.

For example, a country with vast capital account restrictions that happened to not tighten them in the time period of our database would appear more closed in the annual indices but not very restrictive by our index.

The published paper only covers through the period 2012:4. We thank Gurnain Pasricha for sharing with us the updated data that runs through 2015:4.

The Pasricha et al. (2018) database does not identify the measures or provide a reference to the AREAER or central bank announcement from where each measure is compiled. Therefore, we do not know what CFMs they include and cannot provide details on why those measures are not included in the Taxonomy.

In the case of Malaysia and Turkey, this is the case for both inflow CFMs as well as outflow easing CFMs (columns 1, 2 and 4); in the case of China, for both inflow CFMs (columns 1 and 2); in the case of Indonesia and Korea, for both outflow CFMs (columns 3 and 4), and for Argentina, for inflow easing CFMs (column 1).

For example, the Taxonomy records a (CFM/MPM) inflow tightening for Malaysia due to the minimum price for acquisition of property by foreigners introduced in 2009:2; another inflow tightening in 2010:1 when this restriction was tightened, and another inflow tightening when this measure was further tightened in 2014:1. However, Pasricha et al. (2018) do not record an inflow tightening CFM for Malaysia in 2009:2 (or in any other quarter of 2009); in 2010:1 (or any other quarter of 2010); or 2014:1 (or any other quarter of 2014).

References

Ahmed, S. and A. Zlate. 2014. Capital Flows to Emerging Market Economies: A Brave New world? Journal of International Money and Finance 48: 221–248.

Aizenman, J. and G. Pasricha. 2013. Why do Emerging Markets Liberalize Capital Outflow Controls? Fiscal Versus Net Capital Flow Concerns. Journal of International Money and Finance 39: 28–64.

Akinci, O. and J. Olmstead-Rumsey. 2018. How Effective are Macroprudential Policies? An Empirical Investigation. Journal of Financial Intermediation 33: 33–57.

Ariyoshi, Akira, Andrei A Kirilenko, Inci Ötker, Bernard J Laurens, Jorge I Canales Kriljenko, Karl F Habermeier, 2000. Capital Controls: Country Experiences with Their Use and Liberalization. IMF Occasional Papers 2000/009.

Baba, C. and Kokenyne, A. .2011. Effectiveness of Capital Controls in Selected Emerging Markets in the 2000's, IMF Working Papers 11/281, International Monetary Fund.

Bhattacharya, R., I. Patnaik, and A. Shah, 2011, Monetary policy transmission in an emerging market setting. IMF Working Paper no. WP/11/5.

Binici, M. and M. Das. 2021. Recalibration of Capital Controls: Evidence from the IMF Taxonomy. Journal of International Money and Finance 21: 1022–1052.

Cardoso, E. and I. Goldfajn. 1998. Capital Flows to Brazil: The Endogeneity of Capital Controls. Staff Papers 45: 161.

Chinn, M.D. and H. Ito. 2006. What Matters for Financial Development? Capital Controls, Institutions, and Interactions. Journal of Development Economics 81(1): 163–192.

Cowan, K. and De Gregorio, J. 2007. International Borrowing, Capital Controls, and the Exchange Rate: Lessons from Chile," NBER Chapters, in: Capital Controls and Capital Flows in Emerging Economies: Policies, Practices, and Consequences, 241-296, NBER.

Crowe, C. G. Dell’Ariccia, D. Igan and P. Rabanal. 2013. How to deal with real estate booms: Lessons from country experiences. Journal of Financial Stability, 9:3 300–319.

Das, M., S. Kalemli-Ozcan and G. Gopinath. 2021. Preemptive Policies and Risk-Off Shocks in Emerging Markets. NBER Working Paper 29615.

Edwards, S. and R. Rigobon. 2009. Capital controls on inflows, exchange rate volatility and external vulnerability. Journal of International Economics 78(2): 256–267.

Eichengreen, B. 2000. Taming Capital Flows. World Development 28(6): 1105–1116.

Eichengreen, B., P. Gupta and O. Masetti. 2018. Are Capital Flows Fickle? Increasingly? And Does the Answer Still Depend on Type? Asian Economic Papers 17(1): 22–41.

Fernandez, A., M. Klein, A. Rebucci, M. Schindler and M. Uribe. 2016. Capital Control Measures: A New Dataset. IMF Economic Review 64: 548–574.

Finger, H., and P. Lopez Murphy. 2019. Facing the Tides: Managing Capital Flows in Asia. International Monetary Fund, APD Departmental Paper No. 19/17.

Forbes, K. 2007. One Cost of the Chilean Capital Controls: Increased Financial Constraints for Smaller Traded Firms. Journal of International Economics, 71(2):294–323.

Forbes, K., M. Fratzscher and R. Straub. 2015. Capital-Flow Management Measures: What are They Good For? Journal of International Economics, 96:S76–S97.

Gallego, F., L. Hernández and K. Schmidt-Hebbel. 2002. Capital Controls in Chile: Were They Effective?, Central Banking, Analysis, and Economic Policies Book Series. In Banking, Financial Integration, and International Crises, edition 1, 3(12), ed. L. Hernández, K. Schmidt-Hebbel, and N. Loayza, 361–412. Central Bank of Chile.

De Gregorio, J., S. Edwards and R.O. Valdes. 2000. Controls on Capital Inflows: Do They Work? Journal of Development Economics 63(1): 59–83.

Henry, P.B. 2000. Stock Market Liberalization, Economic Reform, and Emerging Market Equity Prices. Journal of Finance 55: 529–564.

IEO. 2020. Capital Flow Measures and Housing-Related Issues in Advanced Economies, Independent Evaluation Office Report

IMF. 2011. Grappling with Crisis Legacies. Global Financial Stability Report, September.

IMF. 2012. The Liberalization and Management of Capital Flows: An Institutional View.

IMF. 2018. Taxonomy of Capital Flow Management Measures.

IMF. 2020. Toward an Integrated Policy Framework. IMF Policy Paper No. 2020/046.

Ilzetzki, E., C. Reinhart and K.S. Rogoff. 2019. Exchange Arrangements Entering the 21st Century: Which Anchor Will Hold? Quarterly Journal of Economics 134: 1–31.

Ilzetzki, E., Reinhart, C., and Rogoff, K. S.. 2021. Rethinking Exchange Rate Regimes, Handbook of International Economics, 5, Gita Gopinath, Elhanan Helpman and Kenneth Rogoff, (eds.).

Jeanne, O. 2012. Capital flow Management. American Economic Review 102: 203–206.

Jeanne, O., A. Subramanian and J. Williamson. 2012. Who Needs to Open the Capital Account? Peterson Institute for International Economics.

Klein, M.W., 2012. Capital Controls: Gates Versus Walls (No. w18526). National Bureau of Economic Research.

Korinek, A., 2012. Capital Controls and Currency Wars. Manuscript, University of Maryland.

Lane, P.R. 2015. International Financial Flows in Low-Income Countries. Pacific Economic Review 20(1): 49–72.

Lane, P.R. and G.M. Milesi-Ferretti. 2018. The External Wealth of Nations Revisited: International Financial Integration in the Aftermath of the Global Financial Crisis. IMF Economic Review 66(1): 189–222.

Lee, N and Sami, A., 2019. Trends in Private Capital Flows to Low-Income Countries: Good and Not-So-Good News, CGD Policy Paper 151.

Ma, G, and R. McCauley, 2008. Efficacy of China’s Capital Controls: Evidence from Price and Flow Data. Pacific Economic Review, 13(1): 104–23.

Magud, N., C. Reinhart and K. Rogoff. 2018. Capital Controls: Myth and Reality–A Portfolio Balance Approach. Annals of Economics and Finance 19(1): 1–47.

OECD, 2020. OECD Code of Liberalisation of Capital Movements, http://www.oecd.org/investment/codes.htm

Ostry, J. D., Ghosh, A. R., Habermeier, K.F., Chamon, M., Qureshi, M. S., and Reinhardt, D., 2010. Capital Inflows: The Role of Controls. IMF Staff Position Notes 2010/004.

Pandey, R., G. K. Pasricha., I. Patnaik and A. Shah 2015. Motivations for Capital Controls and Their Effectiveness. Bank of Canada Working Paper No. 2015–5.

Pasricha, G.K., M. Falagiarda, M. Bijsterbosch and J. Aizenman. 2018. Domestic and Multilateral Effects of Capital Controls in Emerging Markets. Journal of International Economics 115: 48–58.

Quinn, D. 1997. The Correlates of Change in International Financial Regulation. American Political Science Review 91: 531–551.

Schindler, M. 2009. Measuring Financial Integration: A New Data Set. IMF Staff Papers 56(1): 222–238.

Simone, F. N. D. and Sorsa, P., 1999. “A Review of Capital Account Restrictions in Chile in the 1990s”, IMF Working Papers 1999/052, International Monetary Fund.

Williams, D. 2001. Policy Perspectives on the Use of Capital Controls in Emerging Market Nations: Lessons from the Asian Financial Crisis and a Look at the International Legal Regime. Fordham Law Review 1: 561–621.

Acknowledgement

Yunhui Lin, and Seungeun Lee and Mona Wang provided outstanding research assistance. We thank the editor, Andrei Levchenko, and two anonymous referees for very helpful suggestions that have improved both the structure and content of our work. We have benefited from the guidance of Gita Gopinath, Sebnem Kalemli-Ozcan and Martin Schindler, and many helpful comments from John Beirne, Marcos Chamon, Pornpinun Chantapacdepong, Gaston Gelos, Hans Gensberg, Annamaria Kokenyne Ivanics, Gurnain Pasricha, Damiano Sandri, participants at OECD-IMF Workshop on Capital Flows, the Monetary Authority of Singapore, Reserve Bank of Australia, the National Bank of Belgium and the National Bank of Poland. We thank Joshua Aizenman, Gurnain Pasricha and Kristin Forbes for sharing their data with us. The views expressed herein are those of the authors and should not be attributed to the IMF, its Executive Board, or its management.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

All errors are ours. On behalf of all authors, the corresponding author states that there is no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Binici, M., Das, M. & Pugacheva, E. The Incidence of Capital Flow Management Measures: Observations from a New Database. IMF Econ Rev 72, 441–486 (2024). https://doi.org/10.1057/s41308-023-00204-z

Published:

Issue Date:

DOI: https://doi.org/10.1057/s41308-023-00204-z