Abstract

The aim of this study is to investigate the effectiveness of research and development (R&D) tax incentives in generating additional business R&D expenditures in Turkey by applying propensity score matching (PSM) to correct any selection bias and to estimate the average treatment effect on the treated (ATT). Since the empirical literature lacks measurement of the effectiveness of these incentives in Turkey and partially touches upon global cases, this study contributes to fill this gap in the literature. For this purpose, the hypothesis that “R&D tax incentives increase business sector R&D intensity (the ratio of firm’s net R&D expenditures to total turnover)” is tested, and the effectiveness of R&D tax incentives is examined in the context of input additionality. The questions of whether R&D tax incentives are effective in increasing business sector R&D intensity and to what extent R&D tax incentives produce additional R&D intensity are answered. According to the results, R&D tax incentives have a positive effect on business sector R&D intensity. However, the additionality impact is limited since the R&D tax incentive multiplier is between 0 and 1.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Research and development (R&D) activities grew in importance especially after the Second World War, although it originally dates back to German R&D labs in the late 19th century. R&D started to be seen as a factor triggering growth, thus leading to enhanced competiveness an eventual rise in welfare (David, Hall, & Toole, 2000). The evolution of growth theory increased the prominence of technological change and innovation. Technological differences were considered the sources of productivity differences among nations, sectors, and industries (Acemoglu, 2012). Since technological change was seen as the source of productivity, it was regarded as the main driver of economic growth and over time technological change gained importance via endogenous growth models. The evolution in growth theories supposes technological changes as an engine of economic growth in various countries’ rising interest for R&D. Most countries are aimed at increasing R&D activities in order to achieve higher and sustainable growth rates. Their R&D expenditures to GDP ratio (R&D intensity) have increased rapidly over time. As business sector R&D activities are highly correlated with the R&D intensity and growth performance of a country (OECD, 2001), R&D expenditures by this sector assume greater importance.

As a result of several factors, such as market failures in the R&D field (Arrow, 1962; Nelson, 1959), which cause private investment to be lower than the socially desirable level, the financial constraints of small or newly established firms, and high costs of some technological development, business R&D investments preferably call for government support. For this purpose, governments offer generous R&D incentives through direct funding mechanisms such as procurement of R&D, grants, and subsidies and, as an indirect funding mechanism, R&D tax incentives. In the last decade, tax incentives have been widely used for promoting business sector R&D investment. In 2020, 33 of the 37 OECD countries implemented R&D tax incentives as a policy tool, while the number of countries was just 20 in 2000 (OECD, 2020).

In Turkey, the implementation of R&D tax incentives as an indirect funding mechanism was based on the promulgation of the Technology Development Zone Law in 2001; it was enhanced and made more supportive with the introduction of the R&D Activities Support Law in 2008. This legislation is still the basis of R&D tax incentives. It was later revised in 2016 and expanded to include design activities and introduced new regulations concerning the size of the firms in favor of SMEs. Due to the legal regulations governing R&D tax incentives, the share of R&D tax incentives in business enterprise expenditures on R&D (BERD) rose and reached 14.8% in 2018 from 6.94% in 2008 in Turkey. According to the OECD 2018 statistics, Turkey is the sixth highest among the OECD countries in terms of its share in BERD. The EU 27-total and OECD-total R&D tax incentives to BERD ratio are 7.19% and 5.97%, respectively, as of 2018. When R&D tax incentives are compared with direct funding, the increase in these incentives in the last decade has been more significant in Turkey. The direct funding share in BERD for the period 2008–2018 remained almost flat (9.54% in 2008 and 9.97 in 2018), while there was a remarkable increase in R&D tax incentives in the same period. R&D tax incentives have also increased as a percentage of Gross Domestic Product (GDP) in Turkey. They have risen more than fourfold since 2008 to 0.1% in 2018. The increase was not only as a percentage of GDP and BERD but also in the number of R&D tax incentive beneficiaries in the period 2010–2018.

The aim of the study is to evaluate the effectiveness of R&D tax incentives in Turkey in order to contribute to the empirical literature in the following ways. Firstly, despite the increasing weight of R&D tax incentives in Turkey, the literature lacks measurement of the effectiveness of these incentives. The study is aimed at filling the gap in the literature by testing the following hypothesis: “R&D tax incentives are effective in increasing business sector R&D intensity.” Secondly, the extent of the impact of R&D tax incentives on business sector R&D intensity is calculated for assessing the input additionality of this instrument with the help of the R&D tax incentive multiplier. Thirdly, in the study, propensity score matching (PSM) is applied to eliminate the problem of selection bias and compare R&D expenditures of R&D tax beneficiaries and nonbeneficiaries through estimating the average treatment effect on the treated (ATT). Finally, it improves the techniques used in the literature.

The next section explains the theoretical background of public support for private R&D activities by asking “Why should the government support private R&D activities?” After the reasons behind government support for R&D activities are clarified in the context of market failures in particular, trends in R&D government support mechanisms are examined especially for R&D tax incentives. Moreover, additionality which is a major concept for assessing the effectiveness of R&D policies is explained. The “Review of R&D Tax Incentives in Retrospect: An Empirical Discussion” section gives a brief summary of empirical literature that investigates the effectiveness of R&D tax incentives by surveying both cross-country and firm-level studies for different countries is provided. The “R&D Tax Incentives in Turkey” section provides information about the implications of R&D tax incentives in Turkey in the light of the evaluation of the policy over time. The “Methodology” section explains the methodology used in the study. In view of the datasets used in the study, PSM is considered the most suitable method for examining the effectiveness of R&D tax incentives. The “Description of Data and Empirical Results” section describes the data and discusses the empirical results. For investigating the effectiveness of R&D tax incentives, combined firm-level microdatasets constructed from TURKSTAT surveys and other statistics are used. The “Conclusion” section summarizes the results and discusses the conclusions about the effectiveness of R&D tax incentives in Turkey and provides policy recommendations as lessons learned for other develo** countries.

As an Indirect Funding Mechanism: R&D Tax Incentives and Effectiveness of These Policies in the Context of Additionality

As business sector R&D activities are highly correlated with the R&D intensity and growth performance of a country (OECD, 2001), R&D expenditures by this sector assume greater importance. Increasing business sector R&D expenditures are the one of the main focuses of countries for innovation and technological change and thereby higher growth rates. Although investment in R&D by the private sector is highly significant, it is unwise for several reasons to allow the business sector to act alone in the R&D field and leave R&D decisions to the market. Two competing and somehow dichotomous approaches to technological change, namely, neoclassical and evolutionary economics traditions, assume market failures versus systemic failures. Market failures, based on the neoclassical approach, and systemic failures, depending on the evolutionary approach, are the main justifications behind government intervention in R&D. While the market failures approach proposes the funding of business sector R&D activities directly with grants, subsidies, or procurements or indirectly with R&D tax incentives, the systemic failures approach suggests improvement of institutional frameworks and connections among actors in the innovation system. According to the market failures view of the neoclassical approach, R&D activities or the invention process suffer from indivisibilities, externalities in knowledge production, and uncertainties. As a result, the business sector tends to invest in R&D less than socially desirable levels and government support is aimed at boosting firms and compensating for the gap between the private and social returns of R&D investments (Akçomak, 2016; Arrow, 1962; Carvalho, 2011; Czarnitzki et al., 2011; Joseph & Johnston, 1985; Martin and Scott, 2000; Nelson, 1959). The systemic failures view of the evolutionary approach considers innovation as a complex evolutionary nonlinear process and emerges as a result of the interaction between economic actors. According to this approach, innovation system is governed by both market forces and nonmarket institutions and failures results mainly from diffusion of knowledge and differences in knowledge levels among the actors. Thus, this approach bases its arguments for government interventions on “systemic failures” innovation system. In this approach, government intervention is considered from a broader perspective beyond market failures and includes improvement of the innovation system through institutional frameworks and diffusion of knowledge (Akçomak, 2016; Bleda & Río, 2013).

Therefore, whatever the reason and whichever approach is advocated, government support for business sector R&D activities has increased and more resources are allocated from the budget for these activities. Total government allocation for R&D (at constant prices, PPP $) increased more than one and a half-fold in the last 20 years in the OECD. While it was $258,449.10 in 2000, it reached $398,300.41 in 2020. As of 2018, in most countries, direct funding and tax support for business sector R&D increased as a percentage of GDP compared to 2006. Figure 1 shows direct government funding and government tax support for business R&D (as a percentage of GDP) in 2018 and 2006.

Direct funding and tax support for business R&D (2006 & 2018). Source: OECD R&D tax incentive database (http://oe.cd/rdtax); March 2021

As with any other investment decisions, R&D investments require profit opportunities for private firms. The government attempts to solve the underinvestment problem of the business sector in R&D by implementing a policy mix that generally includes both funding mechanisms as complementary measures (Guceri, 2016). With the help of these support mechanisms, the government was aimed at reducing the relative cost and uncertainty of R&D investments. While the government has several support tools for the R&D field such as public–private R&D partnership, direct subsidies, and fiscal incentives, the decision on which one to use depends on national conditions such as firm and industrial structure, innovation performance, observed market failures in R&D, and the structure of the corporate tax system (Appelt et al., 2020; Carvalho, 2011; OECD, 2003). While direct funding mechanisms such as grants, subsidies, and public procurements allow governments to select R&D projects that have socially higher returns, thus increasing the control the government has over conducted R&D (OECD, 2003); on the other hand, selecting the most useful R&D project may have a high administrative cost and could be difficult in practice since there is asymmetric information between projects’ owners and the government. Moreover, the government could tend to reward lobbyists and bureaucrats instead of taking optimal decisions (Hall & Reenen , 2000). In addition, providing transparency in the support mechanism can also cause higher administrative costs. Another criticism regarding direct funding through selection of R&D projects by the government concerns picking winners and losers, thus reducing market competition. The financing of R&D projects by the government can also crowd out business sector R&D expenditures instead of increasing them (OECD, 2003). Despite all these disadvantages, direct funding provides a huge level of certainty to firms. It allows firms to know the amount financed by the government or the reduced cost before starting the project (Ravšelj & Aristovnik, 2020). Moreover, it can be more useful especially for small or newly established firms’ financial constraints through providing initial money for their R&D projects. On the other hand, the application process for direct support imposes a cost on firms and the opportunity cost may not be low, especially for SMEs (Busom et al., 2011). Despite the above-mentioned positive sides of direct subsidies, the challenges regarding this policy have gradually directed many governments to place more emphasis on tax incentives in the R&D field over the years (Czarnitzki et al., 2011). Tax incentives for R&D are widely used as public policy instruments for increasing private R&D investments. Since they reduce the relative cost of R&D investment, they increase the net present value of future R&D projects (OECD, 2003).

R&D tax incentives were implemented in Japan in 1966, in Canada in the 1960s, and in the USA (1981), France (1983), and Australia (1985) in the early 1980s (Hall & Reenen, 2000). Over the years, they have become a popular public policy tool for supporting business sector R&D activities due to their several advantages. They allow governments to help domestic firms to enhance their competitiveness since they are exempt from international trade agreements. Moreover, they are market based and they can be seen as more neutral compared to direct funding. If the policy design of tax incentives matches the policy goals, they can have lower administrative costs compared to direct funding despite their costs in budget expenditures (OECD, 2003; OECD, 2013). On the other hand, tax incentives allow markets to determine the allocation of R&D investments. Therefore, they reduce the power wielded by the government for allocating R&D resources among sectors, firms, and projects. Firms can also focus on lowering the tax burden instead of investing in R&D projects that have higher social returns. In addition, spillover effects can be lower in tax incentive cases compared to direct subsidies. Moreover, the benefits of tax incentives can be limited in some cases, such as firms with insufficient tax profits, and contrary to direct funding, the benefits of tax incentives can be calculated at the end of the fiscal year after the project starts, thus reducing the certainty of the R&D investment compared to direct funding. In addition, it can be considered windfall money by firms and may not change their R&D strategies (Guellec & Van Pottelsberghe De La Potterie, 2003; OECD, 2003; OECD, 2020; Ravšelj & Aristovnik, 2020).

While the policy design of R&D tax incentives is a function of the tax scheme of a country and depends on countries’ specific features and countries’ innovation ecosystem in terms of other public support, the impact of R&D tax incentives is affected by the magnitude of other nations’ R&D tax incentives since there is competition between nations for attracting more R&D-related foreign direct investment (OECD, 2008; Tassey, 2007). When the trend in public policies for supporting business R&D activities is examined for the last 20 years, the rise in the use of expenditure-based R&D tax incentives for supporting business R&D activity is noteworthy in OECD and partner economies. Figure 2 shows the increase in the number of countries that offer R&D tax support in the OECD and EU-27. As of 2020, 32Footnote 1 out of the 37 OECD countries and with Germany, which introduced R&D tax incentive for the first time in 2020, 21 EU-27 countries offer R&D tax support. These numbers indicate a 65% increase in OECD countries and an almost 100% increase in EU countries compared to 2000.

Number of countries offering R&D tax incentives(Central government level) (2000–2020). Source: OECD, The OECD Report on the R&D tax incentives database (2020) (http://oe.cd/rdtax)

Over the years, expenditure-based R&D tax incentives have risen not only in terms of the number of implementing countries but also as a share of total government R&D support. In 2018, the share of R&D tax incentives in total government support for business R&D in the OECD area was 56%, while it was 30% in 2000 (Appelt et al., 2020; OECD, 2020). The ratio of R&D tax incentives as a share of GDP has also increased over the years. While it was 0.04% in 2000 in the OECD area, it increased to 0.1% of GDP in 2018. In these years, the direct funding of business R&D expenditures was 0.1% of GDP and 0.08% of GDP, respectively. All these figures show that the use of tax incentives has increased compared to direct subsidies over the years and they expose the shift in the funding policy of governments clearly. Figure 3 shows the amounts of different funding mechanisms of business sector R&D activities as a percentage of GDP for the period 2000–2018 in the OECD. While there is an increasing trend in R&D tax incentives over the years, there is a decline in direct funding, especially after 2009. Figure 3 also shows clearly the shift in funding mechanism preferences in recent years. After 2015, the share of R&D tax incentives in GDP is higher than the share of direct funding.

Tax incentives vs. direct funding for business sector R&D activities (2000–2018). Source: OECD R&D tax incentives Database; March 2021

Greater use of R&D tax incentives among countries and the countries’ efforts for increasing the attractiveness of R&D tax incentives by providing more generous R&D tax incentives over the years indicate tax competition for attracting more R&D-related foreign direct investments (OECD, 2008). All these developments in the international environment make the measurement of R&D tax incentives’ generosity more important for cross-country comparisons.

The B-index, which was designed by Warda (1996), shows the generosity of R&D fiscal incentives and provides a measure for comparing different tax incentive systems. It is calculated as one dollar R&D expenditure’s after-tax cost (one minus the net present discounted value of fiscal incentives on R&D assets) value divided by one minus the corporate income tax rate. Therefore, a smaller B-index means a more generous tax incentive system (Appelt et al., 2019; Guellec & Pottelsberghe, 2003). The R&D tax generosity is also shown by using implied marginal R&D tax subsidy rates, which depend on the B-index and are calculated as “1 − B-index” (Appelt et al., 2019). It shows “the magnitude of marginal R&D tax credit rates applicable to an extra unit of R&D spend across a segment of the business population (e.g., SMEs or large enterprises).” (OECD, 2020, p. 14). Figure 4 demonstrates the implied marginal R&D tax subsidy rates in the period 2000–2020 in the OECD. When the implied marginal R&D tax subsidy rate is examined for the last 20 years, an increasing trend is easily recognized. After the stabilization period between 2013 and 2019, there was a rapid increase in 2020 with its first implementation in Germany in that year and greater R&D tax relief in a number of OECD countries due to the COVID-19 crisis (OECD, 2020).Footnote 2

OECD implied marginal R&D tax subsidy rates(Unweighted average) (2000–2020). Source: OECD R&D tax incentives database; May 2021 (http://oe.cd/rdtax)

Increasing the use of R&D tax incentives over the years has raised various questions about their effectiveness. In addition, financial consolidation measures in the aftermath of financial crises increased the necessity for balancing public expenditures. Therefore, the efficacy of R&D tax incentives gained importance. An effective R&D tax incentive policy might reduce the budget deficit through stimulating innovation and so economic growth. Another factor that has intensified interest in the effectiveness of R&D tax incentives has been the rising importance of innovation as a source of economic growth due to the decline in economic activity in the aftermath of the financial crises (European Commission, 2014). All these factors have led to questions about the effectiveness of R&D tax incentives and evaluation of this public policy, and measurement methods have grown in importance over the years. However, measurement of a policy’s effectiveness is not an easy matter. Additionality is a major concept for the evolution of R&D policies. The additionality concept was developed in the UK in the early 1980s for assessment of public support given to technology development companies. Later, it was used and developed in the evaluation of many programs in Europe. Today, additionality is a major concept for the evaluation of R&D programs (Georghiou L., 1999; Luukkonen, 2000).

Additionality enables assessment of the effects of R&D incentives or subsidies. It reveals the additional effects on the beneficiaries that accompany government intervention. R&D policy is expected to create “additional activity” to the activity that would occur in any situation. Additionality measures the difference that government funding programs have made to firms. The argument behind it is based on the market failure rationale. Firms tend to underinvest in R&D activities on their own because of their inability to take advantage of all the benefits arising from these activities (Georghiou L., 1999; Luukkonen, 1998).

Additionality is the value added and it has two features:

-

1.

Government funding must create “additional activity” to the activity that would have occurred in any situation.

-

2.

Government funding should have a “multiplier effect.” It is expected to create more R&D activity units than funding units. If the multiplier is higher than 1, it means that one unit of government funding produces activity more than one unit. If it is between 0 and 1, government funding is partly used to reduce firm’s own funds, and finally, if it is negative, it means that government funding is used to reduce firm’s own funds more than received government funds (Guy & Arnold, 1993; Sterlacchini & Venturini, 2019).

Measurement of the additionality of a specific policy/program involves some challenges. Firstly, it depends on the assumption that the benefits that are produced by the policy/program can be identified and can be attributed to the policy/program. Secondly, measurement time is an important factor. It should be appropriate according to the appearance of the program effects. Especially in R&D activities, there is a delay factor. The results can occur in a lag. On the other hand, as time goes on, the effects of other economic conditions could increase and careful isolation of them is required. Therefore, the time of the additionality measurement should be appropriate (Davenport et al., 1998). Additionality is grouped as input, output, and behavioral additionality, depending on where the impact of the policy is observed. While in input additionality the impact is expected to be observed in firm expenditures, in output additionality, it is expected to be observed in output indicators such as patents, sales of new products, and applications of processes and services. In behavioral additionality, the impact is expected to be seen as a change in the firm’s R&D behaviors or decisions. In this paper, we focus solely on the impacts of input additionality.

In sum, as an R&D public policy tool, the rising popularity of R&D tax incentives has increased questions about the effectiveness of this policy. While the additionality concept facilitates measurement of the effectiveness of this instrument, there are several attempts in the empirical literature to assess the effectiveness of the instrument as discussed in the next section.

Review of R&D Tax Incentives in Retrospect: An Empirical Discussion

The growing popularity of R&D tax incentives as a policy tool for supporting business R&D has led to questions about the effectiveness of this policy over time. Despite the widespread use of R&D tax incentives, the effectiveness of this policy is unclear in most cases. There have been several attempts to demonstrate the impact of R&D tax incentives for different countries/country groups and different R&D tax incentive programs but there is no consensus about the impact of these incentives. The results differ widely (Thomson, 2017). For literature from more than 20 years ago, Hall and Van Reenen (2000) provide a good summary of empirical evidence for the USA and other countries and conclude that a dollar tax credit induces a dollar additional R&D investment. When empirical literature is examined for mainly the last 20 years, the studies differ in data level. While some studies such as Bloom et al. (2002), Guellec and Pottelsberghe (2003), Falk (2006), Nam (2012), Thomson (2017), and Appelt et al. (2019) investigate the impact of R&D tax incentives from macro perspective by using cross-country data, firm-level studies such as Koga (2003), Hægeland and Møen (2007), Corchuelo and Martínez-Ros (2009), Czarnitzki et al. (2011), Lokshin and Mohnen (2012), Kobayashi (2014), Thomson and Skali (2016), Dechezleprêtre et al. (2016), Dumont (2017) usually focus on a single country and a country-specific tax incentive scheme. The studies in the literature differ not only in data level (such as firm-level or cross-country) or in results but also in the objective, which is affected by the R&D tax incentives, methodologies, and measures (Ientile & Mairesse, 2009). Cross-country analysis is generally done for OECD countries and investigate the impact of R&D tax incentives on business funded R&D expenditures by applying structural models. Bloom et al. (2002) investigate the impact of R&D tax incentives on the level of business-funded R&D investment for nine OECD countries for the period 1979-1997 from the user cost of R&D perspective. They apply a dynamic model and estimate both short- and long-run elasticities. They conclude that tax incentives are effective after examining country-specific fixed effects such as language, culture, supply of scientists, demand conditions, and macroeconomic conditions that affect the R&D investment independently of tax incentives such as common technology shocks. According to their study, a 10% decrease in the user cost of R&D increases the level of R&D investment by just over 1% in the short run, and this elasticity increases and approaches 10% in the long run.

Cross-country analyses are important since they provide an overall evaluation of R&D tax incentive schemes, which differ between countries. Since these incentives differ between countries in their design, implementation, and generosity, they could also provide more exogenous variation compared to micro-level studies (Appelt et al., 2019; Hall & Reenen, 2000; Thomson, 2017). On the other hand, firm-level studies, which usually focus on a single country, give more specific effectiveness measures for a country-specific tax incentive scheme. Therefore, for evaluating the efficiency of an R&D tax incentive program, firm-level studies could provide more detailed and reliable results (Ientile & Mairesse, 2009). They also mostly allow for sectoral analysis or specific analysis of firms’ characteristics, which could be important for policy design. While cross-country analysis is generally done for OECD countries and applying structural models, the countries or country groups, methodologies, and impact indicator vary in firm-level studies.

A matching method which is based on the comparison of treatment (being a beneficiary) and nontreatment (not being a beneficiary) cases is one of the widely used methods among firm level studies in the literature. Table 1 provides a summary of these studies in terms of country, research period, outcome, and matching techniques. As outcome variables, R&D expenditures over sales or turnover stand out. While the nearest neighbor and kernel matching come to the fore as a matching procedure, empirical studies generally prefer to include more than one matching method.

Although some of firm-level studies apply matching techniques, there are studies which apply structural model in line with cross-country studies. Koga (2003) investigates the effectiveness of R&D tax credits for Japanese firms in the manufacturing sector for the period 1989–1998 by using structural model and he calculates elasticities in line with most of the cross-country literature. He examines the impact of R&D tax credits on firm R&D investment. He estimates the tax price elasticity as −0.68 for all firms, and when it is estimated by taking into consideration firm size, it is calculated as −1.03 for large firms, and it is not significant for medium firms. This means that R&D tax credits are more effective in inducing R&D investments for large firms. He explains the higher effectiveness of R&D tax credits in large firms by their permanent base for R&D, related to having their own research centers and workforce for R&D.

While the literature on the effectiveness of R&D tax incentives is highly dominated by the developed countries, it is sparse for newly industrialized and/or develo** countries although these instruments have been used widely in these countries. Yang et al. (2012) investigate the effect of R&D tax incentives on R&D for Taiwan, which is newly industrialized and has shown a rapid increase in innovation and R&D. They examine the effectiveness of R&D tax incentives for manufacturing firms for the period 2000-2005 by applying PSM, IV, and GMM estimator methods. They analyze the effect of R&D tax incentives on the level of R&D expenditures and the growth of R&D expenditures. They also investigate the effectiveness in the sectoral dimension and examine the effectiveness of R&D tax incentives for electronics firms and nonelectronics firms. According to the PSM results, firms that benefit from tax incentives have a 53.8% higher R&D expenditure level. This effect rises to 71.8% for electronics firms when the analysis is done according to sector. On the other hand, they find no significant result for R&D growth. IV and GMM estimator results are in line with the PSM results. These results indicate that tax credits are more effective for electronic firms. Since budget deficits have become an important issue, a careful evaluation of tax credits is advised as well as differentiating tax incentives between sectors because of different effects of R&D tax incentives between sectors. Aralica and Botrić (2013) investigate the impact of R&D tax incentives on R&D expenditures and product and process innovation for Croatia as a small open country that is a moderate innovator for the period 2008–2009 by applying PSM. For matching, they apply frequently used matching methods such as kernel matching, nearest-neighbor matching, and caliper matching in the study. They find that while R&D tax incentives have a positive effect on R&D expenditures and product innovation, they have no significant effect on process innovation. Ravselj and Aristovnik (2020) take into consideration the effectiveness of both grants and tax incentives as public R&D policies at the same time, and they investigate the impact of both public R&D policies on business R&D expenditures for Slovenian companies, representing a small open economy for the period 2012-2016, by using panel data regression. Therefore, the study provides a comparable picture for R&D public policies in Slovenia. They find that tax incentives have a positive effect on R&D expenditures for Slovenian companies, while R&D subsidies have a negative effect. They emphasize the importance of the tax base for the effectiveness of tax incentives. They also analyze the interaction between R&D subsidies and tax incentives and find it significant and positive. Therefore, they suggest the simultaneous use of these instruments. They also emphasize that R&D subsidies are still important for small firms that do not have a sufficient tax base and R&D subsidies are effective in inducing business R&D expenditures when they are combined with R&D tax incentives. They also evaluate the policies based on company growth rates and find that both policies are effective regarding R&D expenditures for growing companies. For Turkey, although the literature has investigated the effectiveness of R&D grants (Gök, 2006; Gürbüz, 2018; Özçelik and Taymaz, 2008; Tandoğan, 2011; World Bank, 2019) widely, there is still a lack of knowledge about the effectiveness of R&D tax incentives. In conclusion, empirical efforts in the literature for tackling these challenges over the years have led to variation between studies yet both cross-country and firm-level studies in general find R&D tax incentives effective.

R&D Tax Incentives in Turkey

In Turkey, R&D activities have gained prominence in the 2000s. Science, technology, and innovation policies have become an important component of economic policy, especially after 2005 (Erdil et al., 2016). In line with other countries, R&D intensity in Turkey has increased over time. It doubled to 1.06% as of 2019 in comparison to 2001. The number of full-time equivalent (FTE) R&D personnel also increased sevenfold in the same period. To promote R&D activities in the last 20 years, the government has introduced several R&D incentives, and these have become an important part of the incentive system. Both direct and indirect incentives for supporting business sector R&D expenditures (BERD) have increased significantly during this period. The share of direct funding by the government in BERD more than doubled and reached 9.97% as of 2018, compared with 4.25% in 2000. As in many countries, grants and subsidies are the traditional government R&D funding mechanism in Turkey for promoting business sector R&D expenditures, but implementation of R&D tax incentives started with the Technology Development Zone Law No, which came into force in 2001 for supporting R&D activities in techno-parks and organized industrial zones. In 2004, a 40% tax allowance was provided to business sector R&D expenditures through updating the existing Corporate Tax Law and Income Tax Law. In 2006, Turkey set ambitious R&D targets within the ninth development plan for the period 2007–2013 such as increasing R&D expenditures to 2% of GDP, increasing private R&D expenditures to 60% of GDP, and raising the number of researchers to 80,000 (revised to 150,000 in 2008 since the target had been achieved) in 2013 (Tandoğan, 2011). Policies were also updated in line with the targets set for R&D indicators and in 2008 the R&D Activities Support Law, which is the basis of R&D tax incentives, came into force. In 2016, it was revised and design activities were also included and the name of the law was changed to “R&D and Design Activities.” Moreover, R&D tax incentives in Corporate Tax Law and Income Tax Law 193 were regulated in the R&D Activities Support Law from now on.

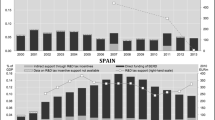

Figure 5 shows the trends of government funding mechanisms in Turkey in the last decade. While direct funding of business sector R&D expenditures (as a percentage of BERD) remained almost flat during 2008-2018 period, government tax relief for business sector R&D expenditures (as a percentage of BERD) increased significantly in the same period. R&D tax incentives have become widely used as a policy tool and R&D tax incentives as a percentage of GDP increased more than fourfold from 2008 to 2018 (Fig. 6).

Funding of business sector. Source: OECD database, May 2021

R&D tax incentives in Turkey. Source: OECD database, May 2021

Not only the amount but also the number of beneficiaries increased over time. The beneficiaries were numbered between 1000 and 8000 per year on average during the period 2010–2018, and the trend in the number of beneficiaries was significantly positive compared to other countries in the same range (Fig. 7).

Number of R&D tax relief beneficiaries (Countries with less than 8000 and more than 1000 beneficiaries per year on average) (2010–2018). Source: OECD, The OECD Report on the R&D tax incentives database (2020) (http://oe.cd/rdtax)

As of 2018, the number of R&D tax incentives beneficiaries is more than 5000. Regarding the other countries that have more than 5000 R&D tax relief beneficiaries in 2018, most of them are pioneers in R&D activities with high R&D expenditures as a percentage of GDP (Fig. 8).

Number of R&D tax relief beneficiaries(Countries with more than 5000 beneficiaries). Source: OECD, The OECD Report on the R&D tax incentives database (2020) (http://oe.cd/rdtax)

Methodology

Efforts for measuring the impact of a treatment or policy implication require the comparison of treatment outcomes and counterfactual outcomes. When the binary treatment is Ti and it is equal to 1 for beneficiaries and 0 otherwise. i = 1, ..., N and N indicates the number of total samples. Then, the potential outcomes for each member i of the sample (firm or participant) are YiT(i) and the impact of the treatment for i can measured by using the Roy-Rubin model as Eq. (1) (Caliendo & Kopeinig, 2008):

where 𝜏𝑖 denotes the treatment effect and potential outcome YiT(i) for i is the function of observable X and unobservable U(1) and U(0) as in Eqs. (2) and (3) (Heckman et al., 1997):

Therefore, measuring the impact of a treatment requires the counterfactual outcome Yi(0) that shows what if the beneficiary does not benefit from the treatment (program) but it is impossible to get this answer. Once a firm or an individual benefits from a treatment or a policy program, it is impossible to observe the outcome(s) without treatment for same person or firm.

Measurement efforts for impact of a treatment mostly focus on treated sample and calculate the average treatment effect on the treated (ATT) by using mean outcomes as in Eq. (4):

Counterfactual mean E[Y(0)| T = 1], which is the answer of the question of what if the treated group does not benefit from the treatment, is not observable. If E[Y(0)| T = 1] is replaced with the mean outcome of nonbeneficiaries E[Y(0)| T = 0],] then Eq. (4) will be revised as Eqs. (5) and (6):

However, in this method, unless E[Y(0)| T = 1] − E[Y(0)| T = 0] = 0, ATT cannot give the impact of the treatment because beneficiaries and nonbeneficiaries could differ even without treatment and this problem is called as selection bias E[Y(0)| T = 1] − E[Y(0)| T = 0] ≠ 0 case.

In this study, propensity score matching (PSM) method which eliminates the selection bias and bases on balancing scores is applied. It is a widely used method in the literature for investigating the impact of a treatment.

PSM depends on the calculation of probability of benefiting (participating) from a treatment for all sample (both beneficiaries and non-beneficiaries) by using observed characteristics of participants.

The validness of PSM depends on two assumptions:

-

1.

Conditional independence: potential outcomes Y are independent of treatment T in a given set of observed covariates X that are independent from treatment (Caliendo & Kopeinig, 2008).

This condition assumes that benefiting from a treatment and outcomes of a treatment base on solely observed characteristics. In other words, unobserved characteristics are not effective in both treatment participation decide and outcomes.

The validity of this assumption is reinforced by using a rich covariate X variable set in the application of propensity scores and the selection of covariate X depends on prior empirical studies and theory (Morris et al., 2013).

If all related X does not include in the model, the PSM results will be biased. However, using too many X in the model can cause over specification and higher standard errors for the estimated propensity scores (Khandker et al., 2010).

2. Overlap (sizable common support): an overlap area between beneficiary and nonbeneficiary samples with same characteristics X should be sizable (Khandker et al., 2010).

In other words, the control group should be sufficient for comparison with the treatment group. If the overlap area between two groups is too small, then matching estimator is not valid (Aerts & Czarnitzki, 2004).

For the validity of PSM, the selection of matching method is another important step. In the study, kernel matching, which is a frequently used matching method in the empirical literature, is applied since it allows us to use more information from the control group with smaller variance in ATT by using the weighted averages of propensity scores of control group membersFootnote 3. The risk of including bad matches from the control group is reduced by applying common support. Therefore, the treated firms that have propensity scores outside of the untreated firms’ propensity score range are discarded (Caliendo & Kopeinig, 2008; Sterlacchini & Venturini, 2019).

PSM method has several advantages. The method does not require a baseline or panel survey, and since it is semiparametric, it requires fewer constraints for the functional form of treatment model and assumptions for distribution of error term. However, the comparison success of the method depends on the correction of the selection bias in the analysis. In other words, benefiting from the treatment should depend on the observed differences between beneficiary and nonbeneficiary samples and unobserved characteristics should not be effective in both treatment participation decides and outcome; otherwise, the results could be suspicious (Czarnitzki et al., 2011; Khandker et al., 2010).

Description of Data and Empirical Results

Data

The effectiveness of tax incentives is investigated by using two combined datasets which are constructed from Innovation Survey (2018), Financial and Nonfinancial Corporations Research and Development Activities Survey (2018), Foreign Trade Statistics (2018), Company Accounts Statistics (2017-2018), and Annual Business Registers Framework (2018) Micro Datasets of TURKSTATFootnote 4. The Innovation Survey (2018), which is compiled about the innovation activities of firms and sources and the costs and strategies of these activities for the period 2016–2018, is the main source used in the study since it includes a question about whether firms are R&D tax incentive beneficiaries during the period 2016–2018. The survey (2018) covers 12,593 firms. The firms’ characteristics and R&D activity data are supported by using the Financial and Nonfinancial Corporations Research and Development Activities Survey (2018), which is compiled with annual surveys and administrative registration information. The survey covers 7251 firms for 2018. It is aimed at providing detailed information about the firms’ R&D activities in the context of R&D personnel structure, R&D expenditures, and the finance sources of R&D activities. For defining the firms’ characteristics such as firm age, turnover, foreign trade status, and financial conditions, the Foreign Trade Statistics (2018), Company Accounts Statistics (2017-2018), and Annual Business Registers Framework (2018) Micro Datasets are also used in the study.

After the combination of the above-mentioned surveys and statistics, the first dataset (d_total) covers 917 firms and all firms engaging in R&D activity in 2018. Table 2 summarizes main features of these 917 firms. 70% of firms are manufacturing firms, and 17.1% of firms are in the information and communication sector. Of the manufacturing firms, 65.3% are R&D tax beneficiaries. Moreover, of the total firms in the first dataset (917 firms), 62.2% are large firms and almost 70% of them are tax beneficiaries during the investigation period and most of the 917 firms are between 11 and 30 years old in the data for 2018 and in all age groups more than 50% are R&D tax beneficiaries. Although the number of young firms is relatively small, the proportion of beneficiaries is high among all the age groups. Another important feature of 917 firms is their integration into the international markets for R&D activities. While 85% of the total firms included in the study are integrated to international markets, 68% of these firms are R&D tax incentive beneficiaries.

Later, the Company Accounts Statistics (2017), which provide information about the financial statements of firms, are also added to the dataset to enrich the study. Since Company Account Statistics (2017) are not available for 917 firms, the second dataset (d_bs) covers 617 firms and it is a subsample of the first datasetFootnote 5. When the structure of datasets is considered, change in the definition and types of innovation in the Innovation Survey due to the updating of the Guidelines of the Oslo ManualFootnote 6, a time series comparison for research is not possible. In addition, R&D tax incentive beneficiary status of firms is questioned for the first time in the Innovation Survey (2018). Therefore, an important factor limiting the study is that the dataset is only a cross-section and this hinders long-term evaluations and makes examination of the causalities difficult. Moreover, applicability of the PSM method might also be questioned due to the validity of the potential control group. The question that why those companies do not benefit from R&D tax incentives during the period could raise. R&D tax incentives is available to all firms which are conducting eligible R&D expendituresFootnote 7. In the study, both datasets include the firms which are engaging R&D activities in 2018Footnote 8. However, avoiding from disclosing of R&D activities in formal documents due to trade secret concerns, higher bureaucracy, increasing probability of tax audit, not being sufficiently aware of the tax incentive benefits could affect the firms’ decision for benefiting from R&D tax incentives. If the control group were widely different from the treatment group, it could be difficult to find the R&D tax incentives nonbeneficiary firm which conducts R&D.

Variables

In this study, firms’ situation regarding their benefiting from R&D tax incentives is used as the treatment variable. It is investigated for the first time in the Innovation Survey (2018) and announced in December 2019. Since R&D tax incentives received by firms are a binary variable in the survey, they are used only as a dummy variable in the study. If firms benefit from R&D tax incentives during the period 2016–2018, it takes a value of “1,” otherwise “0”. A rich control variable set is determined for describing the observable characteristics of firms. In this model, only variables that are not influenced by R&D tax incentives (treatment) and affect firms’ decision about benefiting from R&D tax incentives and the outcome variable are included in the light of the empirical literature and economic theory. For this purpose, control variables that are fixed variables over time or have not been affected by the expectation about participation are chosen (Caliendo & Kopeinig, 2008). The control variables are used to the extent permitted by the data source. It is aimed at including a large set of control variables for determining counterfactuals with the most similar features since omitting important variables can increase the bias in the estimation (Aralica & Botrić, 2013; Caliendo & Kopeinig, 2008; Heckman et al., 1997). The selected control variables and the reasons behind their selection are as follows.

Sectoral differences are important in R&D engagement since it affects the R&D facilities of firms. Manufacturing and nonmanufacturing firms can differ in terms of R&D activities in many aspects. Protection of intellectual property can be more difficult in the service sector compared to the manufacturing sector (Czarnitzki & Fier, 2002). R&D intensity is another factor that can differ between manufacturing and nonmanufacturing firms. Manufacturing firms can be more R&D intensive and their R&D tax incentive claims can be higher compared to nonmanufacturing firms (Kobayashi, 2014). Innovation strategies in the service sector can be also different from those in the manufacturing sector (Freitas et al., 2017). Technological capability is another factor that differs among sectors and affects the R&D activities of firms. Although new services such as information and communication technologies have high technological capability, the manufacturing sector still dominates R&D activities. The service and manufacturing sectors also differ in terms of production technologies (Czarnitzki & Fier, 2002). According to the empirical literature, the R&D tax price elasticity of firms also can differ regarding their industries (Yang et al., 2012). In addition, for taking into consideration unobservable differences between firms such as fixed costs differences, sectoral differences should be included in the study (Carboni, 2017). For the reasons mentioned above, being a manufacturing firm (dum_manu) is a dummy variable in the study.

According to the literature, firm size can be an important factor for the effectiveness of R&D tax incentives and firms’ R&D decisions. Koga (2003) stated that R&D tax price elasticity may differ according to the firm size. He found that it is higher for large firms. Firm size could also affect the R&D decisions according to organizational structure, specialization, and easy access to financial markets (Carboni, 2017). It could be also important for the tax incentive awareness of the firm. The probability of receiving public support for R&D could be higher for larger firms if smaller ones are not supported explicitly (Dumont, 2017). For these reasons, firms are grouped as small (small), medium (medium), and large (large) based on the number of employees. Firms that have between 10 and 49 employees are defined as small, those that have between 50 and 249 are defined as medium, and those that have 250 or more are defined as large, and small (small) and medium (medium) variables are used as dummy variables in the studyFootnote 9. While firm age is another important factor in firms’ R&D activities, the effect of firm age on firms’ R&D activities and thus their R&D tax incentive claims is unclear (Dumont, 2017; Yang et al., 2012). On the one hand, innovative activities could increase with firm age if “learning by doing” (Arrow, 1962) occurs. On the other hand, young firms may tend to be more innovative compared the older ones, as is the case in Turkey (The World Bank, 2019). Hence, firm age (age) is also included in the study as a control variable. Integration into international markets can be another important factor in R&D activities since competition forces firms to be more innovative. Hence, it increases the application for incentives and subsidies (Carboni, 2017). Therefore, the export and import activity of firms (international_markets) is also included as a dummy variable in the study. Benefiting from other R&D subsidies can be an indicator about a firm’s awareness about public support (Corchuelo & Martínez-Ros, 2009). It can increase the probability of benefiting from R&D tax incentives. On the other hand, it is an important factor that can affect the R&D activities of the firm. Therefore, benefiting from other R&D subsidies (other_subsidies) during the period 2016–2018 is controlled for in the study by including other_subsidy as a dummy variable. Belonging to a group can affect the financial conditions of a firm. It can reduce the financial constraints of the firm (Carboni, 2017). It can also help the firm to benefit from prior experiences of R&D tax incentives within the group (Aralica & Botrić, 2013). Belonging to an enterprise group like a holding or group of companies (belongs_to_group) is added to the model as a dummy variable.

Moreover, engaging in R&D cooperation with other institutions or enterprises can also affect the R&D activities and R&D tax claims of firms. It can increase the diffusion of knowledge (Aralica & Botrić, 2013). Therefore, the R&D cooperation status of firms (cooperation) is also used as a dummy variable in the model. Being a part of a multinational company or foreign ownership is another important firm characteristic for R&D activities and decisions since it allows knowledge spillovers and affects financial conditions. Therefore, being a domestic firm (domestic_firm) is also included in the study as a dummy variable. Having qualified employees is another important factor for the innovation activities of firms. Inadequacy in human capital can hamper innovative activities (Corchuelo & Martínez-Ros, 2009; Freitas et al., 2017; Sterlacchini & Venturini, 2019). It can also affect the R&D tax incentive claims of firms since it influences innovation activities. Hence, the firm’s situation in terms of having qualified employees (qualified_employees) is used in the study as a dummy variable. It takes “1” for firms that the share of higher education graduate employees on total employees is higher than 50%, “0” otherwise.

In the Innovation Survey (2018), some of the firms list inadequacy of financial resources within the enterprise and/or loans and capital inadequacy as important factors that hinder the innovation activities of firms. Since financial constraints are important for both the R&D activities and R&D tax incentive claims of firms, the question of whether financial constraints hamper the firm’s innovation activities (financial_constraint) is included as a dummy variable in the study. It takes “1” for firms that indicate inadequacy of financial resources within the enterprise and/or loans and capital inadequacy as important factors which hamper innovation activities, “0” otherwise.

For the purpose of extending the study, the balance sheet information of firms is also added as control variables in the second model. The profitability of firms is an important factor for the propensity to apply for R&D tax incentives since firms that have higher profitability can spend more on R&D activities, and therefore, they more likely to claim R&D tax incentives (Yang et al., 2012). Profitability (profitability) is defined as net profit over total sales in line with the literature. For the conditional assumption to hold, one-year lagged value of profitability (2017) is used in the second model since profitability is only available for a small sample of firms for the beginning of the treatment period, 2016. Financial debt situation is another important factor for the R&D activities of firms, although the sign of the effect on a firm’s R&D activities is not clear. As access to finance becomes easier, the R&D activities of firms can increase since it is an additional financial source for their R&D activities. On the other hand, increasing indebtedness can hamper the R&D activities of firms (Ravšelj & Aristovnik, 2020). The financial liability situation of firms (financial_leverage) is described as total liabilities (short and long-term) divided by total assets in line with the literature and one-year lagged value of it is used in the study for the same reason as profitabilityFootnote 10. Since the effectiveness of R&D tax incentives is investigated in the context of input additionality, the impact of R&D tax incentives on R&D intensity is examined in the study in line with the literature. For the calculation of R&D intensity, net R&D expenditures of firms in 2018 are divided by total turnover in same year. All variables except for the dummy variables and firm age are used by transforming them to natural logarithmsFootnote 11

According to the Heckman, Ichimura, and Todd (1997, 1998), bias in PSM could be low and, thus, the estimation performance of the method could be better under the following conditions:

-

1.

Using the same data source for the treatment and control groups

-

2.

Including a broad set of control variables X

-

3.

Using treatment and control groups that operate in the same location and market and are exposed to the same economic incentives (Cintina & Love, 2019; Khandker et al., 2010)

In the study, all three conditions above are satisfied for both of the datasets. The same surveys and statistical databases are used for both the treatment and control groups and both groups are in the same geographic area. Further, a rich dataset is used for control variables by taking into consideration the empirical literature and/or economic theory. The Innovation Survey (2018) and Financial and Nonfinancial Corporations Research and Development Activities Survey (2018) provide detailed information about firms’ R&D activities. The Foreign Trade Statistics (2018), Company Accounts Statistics (2017), and Annual Business Registers Framework (2018) are also very informative about firms’ characteristics such as firm age, turnover, number of employees, foreign trade status, and balance sheets. They are all used as observable characteristics that affect benefiting from R&D tax incentives and the R&D expenditures of firms.

Empirical Results

In the study, firstly, the probit model is applied for predicting the probability of benefiting from R&D tax incentives with the set of observable characteristics X. The results of the probit model are given in Table 3.

In the probit model, the R&D cooperation status of firms and benefiting from other R&D subsidies, having qualified employees affects positively the probability of benefiting from R&D tax incentives, while being a manufacturing firm and a small firm affects negatively this probability. Then, the propensity scores for benefiting from R&D tax incentives are calculated by using the probit model aboveFootnote 12. The region of common support is where the distributions of propensity scores of benefiting and nonbenefiting groups overlap are defined and the balancing test is applied. Then the treatment group, which consists of R&D tax incentives beneficiaries, is matched with the control group, which consists of the nonbeneficiaries with the most similar characteristics to the treatment group on the basis of their propensity scores.

Table 4 shows the kernel matching results, which are obtained by using the propensity scores. Under the assumptions of conditional independence and sizable common support, the mean differences in outcomes over common support give the ATT, which shows the impact of the treatment.

The difference between the treated and control groups is smaller than that in ATT than the unmatched result. This means that the unmatched difference result is overestimated since it ignores selection bias. PSM allows us to correct selection bias. According to the ATT result, which is obtained by applying PSM, R&D tax incentives have a positive and statistically significant effect on firms’ R&D intensity. R&D tax incentive beneficiary firms have 7% higher R&D intensity than they would have had without R&D tax incentives.

After matching the treated and control groups, the mean values and t stats show that both groups are balanced regarding the control variables as shown in Table 5 and Fig. 9.

Matching results

Kernel density estimates of propensity score distributions are shown in Fig. 10 regarding the matching status. The figure shows that the distributions overlapped sufficiently after matching.

Kernel density estimates of propensity score distributions

As a robustness check, in line with the literature, the kernel matching results are checked by applying nearest neighbor matching. The result of this matching method is consistent with the results of kernel matching, and it is shown in Appendix 6.

Empirical Results of the Second Model (Including Financial Conditions)

In order to enrich the study, for the financial condition variables of firms, financial_leverage and profitability control variables are added to the study in the second model. All estimation steps and methods of the first model are preserved in the second model. The results of the probit model are given in Table 6. According to the results, the R&D cooperation status of firms, benefiting from other R&D subsidies and profitability, positively affect the probability of benefiting from R&D tax incentives. Only being a manufacturing firm negatively affects this probability.

The propensity scores for benefiting from R&D tax incentives are calculated from this probit model, and the region of common support where the distributions of propensity scores of the benefiting and nonbenefiting groups overlap is defined, and the balancing test and kernel matching are applied as in the first model. Table 7 shows the kernel matching results. According to the results, R&D tax incentives have a positive and statistically significant effect on firms’ R&D intensity when the financial conditions of firms are also controlled for. However, the effect of R&D tax incentives on firms’ R&D intensity is slightly lower when the financial conditions of firms are taken into consideration. The R&D tax incentive beneficiary firms have 6% higher R&D intensity than they would have had without R&D tax incentives.

Treated and control group mean values and t stats show that both groups are balanced regarding to control variables after matching as shown in Table 8 and Fig. 11.

Matching results (second model with financial conditions)

Figure 12 shows that the kernel density estimates of propensity score distributions overlapped sufficiently after matching.

Kernel density estimates of propensity score distributions (second model with financial conditions)

The kernel matching results are checked by applying nearest neighbor matching, as in the first model. The result of this matching method is consistent with the results of kernel matching also for the second model, and it is shown in Appendix 6.

Input Additionality of R&D Tax Incentives

PSM enables evaluation of the effect of R&D tax incentives through calculation of ATT. With the help of ATT estimation, it is apparent that R&D tax incentive beneficiary firms have higher R&D intensity than they would have had without R&D tax incentives. Although this result indicates a positive effect of R&D tax incentives on the R&D intensity of firms, it does not reflect directly the input additionality, which shows to what extent the R&D tax incentives are reflected in the increase in R&D intensity. Calculation of the input additionality ratio or BFTB, which is the measure of the additional increase in R&D intensity of a firm for every money unit of foregone tax revenue, is important for assessing the input additionality of R&D tax incentives.

The input additionality ratio or BFTB can be interpreted as an R&D tax credit multiplier. A value of the multiplier greater than 1 implies that one money unit of government support produces R&D intensity more than one money unit. If the value of the multiplier is between 0 and 1, it means that government funding is partly used for reducing the firm’s own funding. In other words, one unit of government support is translated to R&D intensity less than one unit by the beneficiary firm. It means that government funding partially crowds out business R&D. This case indicates that the firm uses some part of the government support in other activities. Finally, a negative multiplier indicates that government support crowds out business R&D, which means that government support is used to reduce the firm’s own funding more than the received R&D tax incentives. This implies that the beneficiary firm uses all R&D government support for other activities rather than R&D (Appelt et al., 2019; Sterlacchini & Venturini, 2019).

Since BFTB or the additionality ratio is a cost–benefit analysis, the amounts of foregone tax revenue for firms are necessary as a cost of government funding. R&D tax incentives data are only available as a binary variable that shows whether the firm benefits from R&D tax incentives during the period 2016–2018. This hampers the calculation of the multiplier using firm-level data. Sterlacchini and Venturini (2019) compute the R&D tax multiplier by using the ATT value as a percentage of the R&D intensity of treated firms and the average effective tax credit rate of the country in their study. They calculate the average effective tax credit rate by dividing the amount of tax credits by R&D expenditures claimed for tax credits at country level. Then, they state that the ratio of ATT/R&D intensity (%) to average effective tax credit rate (%) gives the R&D tax credit multiplier. Due to the data constraints, the method applied by Sterlacchini and Venturini (2019) is followed for calculation of the multiplier. Since the ATT value and R&D intensity of treated firms is calculated by applying PSM, the average effective R&D tax incentive rate is needed for Turkey.

TURKSTAT announces the amounts of R&D tax incentives for Turkey on annual basis. Table 9 shows the amounts of R&D tax incentives during the period 2008–2018. As of 2018, the amount of R&D tax incentives is 4599 million TL.

Although the R&D tax incentives amount is available, the amount of R&D expenditures claimed for R&D tax incentives is not announced. Therefore, it is requested from TURKSTAT. Table 10 shows the R&D expenditures claimed for R&D tax incentives and R&D tax incentive amount for 2018.

R&D expenditures claimed for R&D tax incentives could be provided only for 2979 million TL R&D tax incentives by TURKSTAT. Due to data privacy, tax bases for 1619 million TL R&D tax incentives (income tax withholding and VAT) could not be provided. Therefore, the average effective R&D tax incentive rate is calculated in the light of the shared data.

Table 11 shows the calculation of the average effective R&D tax incentive rate. According to the calculations, it is computed as 22.2% for Turkey in 2018.

Table 12 shows the calculation of the R&D tax incentive multiplier. ATT/R&D intensity (%) is divided by the average effective R&D tax incentive rate (%). It is calculated as 0.4 for the first model for Turkey in 2018. When the financial conditions of firms are taken into account, the multiplier decreases slightly to 0.3 for the same year.

Both of the multipliers are between 0 and 1. These results imply that although R&D tax incentives produce additional R&D intensity, these incentives are partly used to reduce firms’ own funding in Turkey in 2018 since the multiplier is positive but less than 1. In other words, although R&D tax incentives have a positive effect on business R&D, this effect is limited since R&D tax incentive beneficiary firms allocate government support partially for other activities. Despite this, R&D tax incentives contribute to increased business sector R&D performance since the multiplier is positive. Due to the lack in empirical literature about the effectiveness of this instrument in Turkey, the results of the study can only be compared with empirical studies which is done for other countries in the literature. Although R&D tax incentive schemes differ from country to country and measurement methods of additionality of R&D tax incentives also differ widely in the empirical literature, the justification behind this policy instrument in economic theory and the advantages and disadvantages of the instrument are similar. Therefore, many studies such as Hall and Reenen (2000), Guellec and Van Pottelsberghe De La Potterie (2003), and Appelt et al. (2019) try to form a framework for a general assessment about the effectiveness of this instrument through cross-country analysis. For this reason, when the results are compared to other studies, they are consistent with the empirical literature. Although the measurement techniques differ, the impact of this instrument on business R&D is found mostly positive but limited in both cross-country and firm-level empirical studies such as Hall and Reenen (2000), Koga, (2003), Falk (2006), Lokshin and Mohnen (2012), Thomson (2017), Appelt et al. (2019), Sterlacchini and Venturini (2019), and Ravšelj and Aristovnik (2020). Generally, the effect of R&D tax incentives on business R&D increases in the long run. Due to data restrictions, it is impossible to evaluate R&D tax incentives for the long run for Turkey in the study. Therefore, investigating the long-term impact can be useful for policy evaluation in further studies with improvement of the R&D tax incentive data for Turkey.

Conclusion

Technological change has started to be accepted as an engine of growth through the evolution in growth theories. This approach has increased the importance of R&D activities, in particular business sector R&D activities, over time. Most countries have set ambitious targets for R&D indicators, especially for R&D intensity. This has led to expectations of increased R&D intensity led by business sector R&D expenditures. Several factors in the R&D field oblige governments to support business sector R&D activities. In economics, these factors that make government interventions in the R&D field necessary are explained mainly by neoclassical and evolutionary approaches. While the justification for government interventions in this field is explained through market failures in the neoclassical approach, it is explained through systemic failures in the evolutionary approach. The logic (market failures or systemic failures) behind the interventions shapes the policy tools. While the market failures approach proposes the funding of business sector R&D activities directly with grants, subsidies, or procurements or indirectly with R&D tax incentives, the systemic failures approach suggests improvement of institutional frameworks and connections among actors in the innovation system. Funding of business sector R&D activities based on the market failure approach increased government support in this field over time. It also raised the importance of the effectiveness of these policy instruments. Since they are budget-related instruments, their effective implication could compensate for government spending in this field through innovation and economic growth. Therefore, the advantages and disadvantages of these funding mechanisms are investigated widely over time. Their combination in funding of the business sector has also changed as a result of these evaluations.

While direct funding has been a traditional funding mechanism for years, R&D tax incentives, as an indirect funding mechanism, have increased as both a percentage of GDP and the number of countries that implement this policy tool. As a result of this rising popularity of R&D tax incentives, the effectiveness of this instrument is investigated widely in the empirical literature. The rising awareness for R&D activities in Turkey has demonstrated a parallel trend with other countries over time; it accelerated in the new millennium. As a result of policies formulated in the light of ambitious targets in this field, R&D indicators such as R&D intensity and personnel have risen over time. The share of BERD in total R&D expenditures has increased as required. Government funding for business sector R&D expenditures has also risen as a result of these developments. While direct funding (as a percentage of GDP) has remained flat as a traditional policy tool in this field, R&D tax incentives (as a percentage of GDP) have increased. Tax incentives for R&D have increased not only as a percentage of GDP but also as the number of beneficiaries over time.

Despite the wide use of R&D tax incentives, there is a lack of studies in the empirical literature about the effectiveness of this instrument. The aim of the study is to investigate the effectiveness of R&D tax incentives in Turkey. For this purpose, firstly the hypothesis that “R&D tax incentives increase business sector R&D intensity” is tested by using two cross-sectional datasets, which are combined versions of the Innovation Survey (2018), Financial and Nonfinancial Corporations Research and Development Activities Survey (2018), Foreign Trade Statistics (2018), Company Accounts Statistics (2017-2018), and Annual Business Registers Framework (2018) Micro Datasets of TURKSTAT. Since the question of whether firms benefit from R&D tax incentives during the period 2016–2018 is included in the Innovation Survey (2018), this survey forms the backbone of the study. The data of the Innovation Survey are enriched by using the other above-mentioned surveys and statistics that include information about R&D activities and firm characteristics and balance sheets. The first dataset includes 917 firms and the following control variables: whether a manufacturing firm, firm size (small, medium, and large), firm age, belonging to a group, whether a domestic firm, R&D cooperation status of firm, benefiting from other subsidies, integration in international markets, having qualified employees, whether financial constraints hamper firm’s innovation activities. Since balance sheet indicators such as financial leverage and profitability are also important for benefiting from R&D tax incentives and R&D investments of firms, these variables are added as control variables in the second dataset in line with the literature. This is intended to enrich the study and check the robustness of the result. In the second dataset the number of firms decreases to 617 since balance sheet variables are not available for all 917 firms. For avoiding the problem of selection bias, PSM is applied for both of the datasets and ATT is calculated. The estimations for both datasets confirm the hypothesis that R&D tax incentives increase business sector R&D intensity in Turkey. Then, the extent of the impact for producing additional R&D intensity is calculated with the help of the R&D tax incentive multiplier. The multiplier is calculated between 0 and 1 for both of the datasets. It is slightly lower for the second dataset, which takes the financial conditions of firms into account. These results imply that although R&D tax incentives are effective in increasing business sector R&D since they have a positive effect on the R&D intensity of firms, their effectiveness is limited as the multipliers indicate partial crowd-out.

Several factors may have contributed to these results. Firms may focus on lowering their tax burden instead of investing in R&D, benefits of R&D tax incentives may be limited due to insufficient tax profits of some firms, or firms may consider these incentives as windfall money and they may not change their R&D policies. Since they do not provide an initial money for R&D expenditures, they may not ease financial conditions, especially for firms experiencing financial difficulties. This means that if firms have sufficient financial resources for R&D expenditures, they may benefit more from R&D tax incentives but the effect of those incentives for encouraging firms to spend more on R&D may be lower if they do not have sufficient financial resources for spending on R&D. However, the results of the study have to be treated with caution for several reasons. Firstly, the multiplier approach takes into account private benefits. Knowledge spillovers due to increased R&D intensity of firms with the help of the R&D tax incentives are not taken into consideration in this approach. The sum of private and social benefits may be higher than estimated (Appelt et al., 2019; Sterlacchini & Venturini, 2019). Secondly, as a treatment variable, benefiting from R&D tax incentives is available only as a binary variable. Since the amount of R&D tax incentives for firms is not available, the multiplier was calculated from the overall country R&D tax incentives amount and total R&D tax incentives claims. Calculation of the multiplier can be improved by using firm-level R&D tax incentive data in future studies through improvement in R&D tax incentive data. Thirdly, the effect is calculated for only short-run in the study. The available data for R&D tax incentives are only cross-sectional because of changes in the definition and types of innovation in the main source of innovation statistics, the Guidelines of the Oslo Manual, and the question of whether firms benefit from R&D tax incentives is asked for the first time in the 2018 Innovation Survey. Therefore, these factors hamper long-term investigation of the effectiveness of these incentives and they limit the econometric methods in terms of impact analyses. The effect can be higher in the long run since most of the studies in the literature show that the effect of these incentives increases in the long-run.

Despite all the above-mentioned shortcomings, the study contributes to the empirical literature in the following ways. Firstly, the main contribution of the study is filling the gap in the empirical literature concerning the impact analysis of R&D tax incentives in Turkey. Since measurement of public policies is an up-and-coming issue in Turkey and the resources allocated for these incentives have increased over time, the efforts for investigating the effectiveness of these incentives are important. Secondly, majority of the control variables in the literature could be included in estimations. Another contribution of the study is that the estimations provide some insights about this public policy. It shows that the improvement of policies for R&D tax incentives can be useful for decreasing the crowd-out effect.

The studies in this field show that it is useful to evaluate R&D policies as a whole. Therefore, the coherence of policies that affect the R&D field is important. In this sense, the policy set that improves the financial conditions and predictability of firms (not only direct subsidies but also other factors such as credit conditions and certainty in economic policies) and tax policy may increase the effectiveness of R&D tax incentives. However, the results of the study can be considered as inferences based on R&D tax incentives and the R&D intensity in the business sector for the period 2016-2018 rather than as an evaluation of R&D tax incentive policy. Evaluation of this policy may require a broader perspective instead of calculation of the impact only for the R&D intensity in the business sector. In this sense, examination of effectiveness in the context of output additionality in further studies may be useful. As a suggestion for further research, there is a need for studies on the impacts of other types of additionalities through R&D tax incentives, namely, output and behavioral additionality. However, such an attempt requires the use of qualitative and mixed methods.

Notes