Abstract

A multi-period stock trading model is developed in which there are two types of traders—a “rational” type and a “gambler’s fallacy” type—both observing a public signal about the fundamental value in each period. The rational type holds correct beliefs on the signals, whereas the gambler’s fallacy type mistakenly believes that the sequence of the signals exhibits systematic reversals. We explore the dynamic equilibrium in which the two types trade with each other to speculate future price changes based on their inferences about the fundamental value. It is shown that the presence of the gambler’s fallacy type can generate both short-term momentum and long-term reversal. Furthermore, the pattern is robust even in a market with a large proportion of rational traders as the price is closer to the gambler’s fallacy type’s valuation. We also show that the gambler’s fallacy type becomes more influential in determining the price as the market switches from momentum to reversal. Interestingly, to an outside observer, it would appear as though the rational traders act as if they have “hot-hand” fallacy in prices, and that a trend following strategy is optimal in this model.

Similar content being viewed by others

Notes

Discussions about momentum can be dated back to the 1700s. James Grant published the book The Great Metropolis in 1838, which considered David Ricardo, an English political economist who had amassed a considerable fortune by trading both bonds and stocks in London markets in the late 1700s and early 1800s. Ricardo’s main strategies include the ideas that you should ‘cut short your losses’ and ‘let your profits run on’—in other words, the momentum strategy.

Tversky and Kahneman [42] pointed out that the gambler’s fallacy is a cognitive bias produced by a psychological heuristic called the representativeness heuristic, which states that people evaluate the probability of a particular event by assessing how similar it is to events they have experienced before, and how similar the events surrounding those two processes are. Numerous early studies have confirmed this general pattern. See [29] for a review.

Rabin and Vayanos [37] discuss their model mainly in the context of the fund-flow puzzle. Investors with gambler’s fallacy try to infer the unobservable fund manager’s investing ability from the fund’s observable performance history. They also briefly discuss the potential implications—momentum and reversal in a market with a representative investor.

The beliefs of the rational type are the same as seen in Grossman [22], in which each individual observes a private signal \(y_t=V+\xi _t\) and believes that this is the actual signal-generating process.

In Rabin and Vayanos [37], the term \(\beta \underset{k=0}{\overset{t}{\varSigma }}\delta ^{k}\kappa _{t-k}\) is replaced by \(\beta \underset{k=0}{\overset{+\infty }{\varSigma }}\delta ^{k}\kappa _{t-k}\). Rabin and Vayanos focused on the idea that \(V_t\) is not constant but instead evolves as follows: \(V_t=\rho V_{t-1}+(1-\rho )\eta _t\) where \(\rho \in [0,1]\) is a constant and \(\eta _t\) is i.i.d. normal, with mean zero and constant variance \(\delta _{\eta }^2\). Rabin and Vayanos [37] mainly studied the signal shock’s effect on the steady state when \(\delta _{\eta }^2\) is non-zero. When \(\delta _{\eta }^2=0\), the investors are all able to predict the fundamental value correctly, despite the gambler’s fallacy.

We plot \(t=5\) to \(T-1\). The first four periods are eliminated from the figure in order to remove the initial effects.

The equilibrium price process is determined by an investor’s expectations of future values; these, in turn, are determined by their beliefs about the signals. Therefore, the perceived random processes of the real prices are different from the perspective of each type as they hold different views about the signal-generating process.

Expectations of the true states of the economy; e.g., \(E_R[V_{t+k}|{\mathscr {F}}_t] \ne E_G[V_{t+k}|{\mathscr {F}}_t]\).

Expectations of the other type’s expectations; e.g., \(E_R[E_G[V_{t+k}|{\mathscr {F}}_t]|{\mathscr {F}}_t]=E_G[V_{t+k}|{\mathscr {F}}_t]\).

In a standard Grossman model, the mean-variance efficient portfolio takes this format: \(X=\dfrac{E(V-P)}{\lambda Var(V)}\)

Simulation results are similar for a wide range of parameters.

We assume that both types share the same prior on the fundamental with no information observed before a public signal arrives. The new signal is different from the prior expectation ,and therefore creates a signal shock (information shock) for both types as indicated by \(v_t^i\) in the inference process described by Proposition 1. To better understand the effect of the signal, we simply assume that all future signal realizations take the same value as the first one. Intuitively, this assumption implies that the signal is a complete revelation of the fundamental value.

An example is [22]. The equilibrium price is

$$\begin{aligned} P=\left( \dfrac{1}{1+r}\right) \dfrac{\sum _{i=1}^{n}\dfrac{\mu +\frac{\sigma ^{2}}{\sigma ^{2}+\sigma _{i}^{2}}\left( s_{i}-\mu \right) }{\alpha _{i}\sigma ^{2}\left( 1-\dfrac{\sigma ^{2}}{\sigma ^{2}+\sigma _{i}^{2}}\right) }-Z}{\sum _{i=1}^{n}\dfrac{1}{\alpha _{i}\sigma ^{2}\left( 1-\dfrac{\sigma ^{2}}{\sigma ^{2}+\sigma _{i}^{2}}\right) }}, \end{aligned}$$where \(\mu +\frac{\sigma ^{2}}{\sigma ^{2}+\sigma _{i}^{2}}\left( s_{i}-\mu \right) \) is agent i’s expectation. Z is the net supply of the stock. r is the risk free return. By setting the risk-free rate r to 0 and the supply of stock to 0, the equilibrium price is a weighted average of the expectations of all agents trading in the market.

Grossman [22] showed that risk-tolerant agents with lower Arrow-Debreu risk-aversion parameters have a more substantial influence on the equilibrium price. This result can be seen from their equilibrium price, where \(\alpha _i\) is agent i’s risk-aversion parameter.

This result can be seen from the simulation in Fig. 8.

This can be seen from the simulation results featuring a signal shock in Fig. 3.

The problem of the rational type is very simple. The reason for applying Kalman Filter to this problem is to make the rational case comparable to the fallacy one.

We do not differentiate between the realizations and the stochastic process here in the notations. But we point out that conditional on each information set \({\mathscr {F}}_t\), \(P_t\), \(Q_t\), and \(\varPsi _t\) are no longer random variables and are public information for both types. However, \(P_{t+k}\), \(Q_{t+k}\), and \(\varPsi _{t+k}\) are still random based on information set \({\mathscr {F}}_t\). Therefore, conditional on the \({\mathscr {F}}_t\), we have \(P_t^i=P_t\), \(Q_t^i=Q_t\), and \(\varPsi _{t}^i=\varPsi _{t}\), all take their realizations. Here we implicitly assume the information set \({\mathscr {F}}_j\) has \(j<t\). Furthermore, \(P_t^i\), \(Q_t^i\), and \(\varPsi _t^i\) are different processes for different information sets \({\mathscr {F}}_j\). However, because we only care about the one step ahead expression, the information set j is eliminated from the expression.

In Proposition 4, the optimal holdings \(X_t^i\) is now a function of \(\varPsi _t\) rather than \(\varPsi _t^i\). At time t, both \(\varPsi _t\) and \(P_t\) are non-random variables and are public information contained in the information set \({\mathscr {F}}_t\). Their realizations are common knowledge to both types of traders so that \(\varPsi _t^i=\varPsi _t\), \(P_t^i=P_t\) and \(Q_t^i=Q_t\).

- $$\begin{aligned} M_{t}^{i}&=F_{t}^{\mathbf {T}}\left( B_{Q,t+1}^{i}\theta _{t+1}^{i}B_{Q,t+1}^{i\mathbf {T}}\right) F_{t}-\left( B_{\varPsi ,t+1}^{i\mathbf {T}}U_{t+1}^{i}A_{\varPsi ,t+1}^{i}\right) ^{\mathbf {T}}\theta _{t+1}\left( B_{\varPsi ,t+1}^{i\mathbf {T}}U_{t+1}^{i}A_{\varPsi ,t+1}^{i}\right) \\&\quad +A_{\varPsi ,t+1}^{i\mathbf {T}}U_{t+1}^{i}A_{\varPsi ,t+1}^{i} \end{aligned}$$

- $$\begin{aligned} F_{t}^{i}=\left( B_{Q,t+1}^{i}\theta _{t+1}^{i}B_{Q,t+1}^{i\mathbf {T}}\right) ^{-1}\left( A_{Q,t+1}-B_{Q,t+1}^{i}\theta _{t+1}^{i}B_{\varPsi ,t+1}^{i\mathbf {T}}U^i_{t+1}A_{\varPsi ,t+1}\right) . \end{aligned}$$(31)

References

Andreassen, P.B., Kraus, S.J.: Judgmental extrapolation and the salience of change. J. Forecast. 9(4), 347–372 (1990)

Asness, C.S., Liew, J.M., Stevens, R.L.: Parallels between the cross-sectional predictability of stock and country returns. J. Portfolio Manag. 23(3), 79–87 (1997)

Asness, C.S., Moskowitz, T.J., Pedersen, L.H.: Value and momentum everywhere. J. Finance 68(3), 929–985 (2013)

Bar-Hillel, M., Wagenaar, W.A.: The perception of randomness. Adv. Appl. Math. 12(4), 428–454 (1991)

Barberis, N., Shleifer, A.: Style investing. J. Financ. Econ. 68(2), 161–199 (2003)

Barberis, N., Shleifer, A., Vishny, R.: A model of investor sentiment. J. Financ. Econ. 49(3), 307–343 (1998)

Barberis, N., Greenwood, R., **, L., Shleifer, A.: X-capm: An extrapolative capital asset pricing model (2013)

Bhojraj, S., Swaminathan, B.: Macromomentum: returns predictability in international equity indices*. J. Bus. 79(1), 429–451 (2006)

Brown, D.P., Jennings, R.H.: On technical analysis. Rev. Financ. Stud. 2(4), 527–551 (1989)

Brunnermeier, M.K.: Asset Pricing Under Asymmetric Information: Bubbles, Crashes, Technical Analysis, and Herding. Oxford University Press, Oxford (2003)

Chen, G., Kim, K.A., Nofsinger, J.R., Rui, O.M.: Trading performance, disposition effect, overconfidence, representativeness bias, and experience of emerging market investors. J. Behav. Decis. Mak. 20(4), 425–451 (2007)

Clotfelter, C.T., Cook, P.J.: Notes: The gambler’s fallacy in lottery play. Manag. Sci. 39(12), 1521–1525 (1993). https://doi.org/10.1287/mnsc.39.12.1521

Croson, R., Sundali, J.: The gambler’s fallacy and the hot hand: empirical data from casinos. J. Risk Uncert. 30(3), 195–209 (2005). https://doi.org/10.1007/s11166-005-1153-2

Daniel, K., Hirshleifer, D., Subrahmanyam, A.: Investor psychology and security market under-and overreactions. J. Finance 53(6), 1839–1885 (1998)

Daniel, K.D., Hirshleifer, D., Subrahmanyam, A.: Overconfidence, arbitrage, and equilibrium asset pricing. J. Finance 56(3), 921–965 (2001)

DeBondt, W.F., Thaler, R.: Does the stock market overreact? J. Finance 40(3), 793–805 (1985)

Fama, E.F., French, K.R.: The cross-section of expected stock returns. J. Finance 47(2), 427–465 (1992)

Gervais, S., Odean, T.: Learning to be overconfident. Rev. Financ. Stud. 14(1), 1–27 (2001)

Gorton, G.B., Hayashi, F., Rouwenhorst, K.G.: The fundamentals of commodity futures returns. Rev. Finance 17(1), 35–105 (2013)

Greenwood, R., Shleifer, A.: Expectations of returns and expected returns. Tech. rep, National Bureau of Economic Research (2013)

Greenwood, R., Shleifer, A.: Expectations of returns and expected returns. Rev. Financ. Stud. 27(3), 714–746 (2014)

Grossman, S.: On the efficiency of competitive stock markets where trades have diverse information. J. Finance 31(2), 573–585 (1976)

He, H., Wang, J.: Differential informational and dynamic behavior of stock trading volume. Rev. Financ. Stud. 8(4), 919–972 (1995)

Hong, H., Stein, J.C.: A unified theory of underreaction, momentum trading, and overreaction in asset markets. J. Finance 54(6), 2143–2184 (1999)

Hong, H., Kubik, J.D., Stein, J.C.: Thy neighbor’s portfolio: Word-of-mouth effects in the holdings and trades of money managers. J. Finance 60(6), 2801–2824 (2005)

Jegadeesh, N., Titman, S.: Returns to buying winners and selling losers: implications for stock market efficiency. J. Finance 48(1), 65–91 (1993)

Kausar, A., Taffler, R.J.: Testing behavioral finance models of market under-and overreaction: do they really work? (2006)

Kroll, Y., Levy, H., Rapoport, A.: Experimental tests of the mean-variance model for portfolio selection. Organ. Behav. Hum. Decis. Process. 42(3), 388–410 (1988)

Lee, W.: Decision theory and human behavior (1971)

Loh, R.K., Warachka, M.: Streaks in earnings surprises and the cross-section of stock returns. Manage. Sci. 58(7), 1305–1321 (2012)

Long, J.B., Shleifer, A., Summers, L.H., Waldmann, R.J.: Positive feedback investment strategies and destabilizing rational speculation. J. Finance 45(2), 379–395 (1990)

Merton, R.C.: An intertemporal capital asset pricing model. Econometrica: J. Econom. Soc. 867–887 (1973)

Moskowitz, T.J., Grinblatt, M.: Do industries explain momentum? J. Finance 54(4), 1249–1290 (1999)

Muth, J.F.: Rational expectations and the theory of price movements. Econometrica: J. Econom. Soc. 315–335 (1961)

Odean, T.: Are investors reluctant to realize their losses? J. Finance 53(5), 1775–1798 (1998)

Rabin, M.: Inference by believers in the law of small numbers. Q. J. Econ. 117(3), 775–816 (2002)

Rabin, M., Vayanos, D.: The gambler’s and hot-hand fallacies: theory and applications. Rev. Econ. Stud. 77(2), 730–778 (2010)

Shapira, Z., Venezia, I.: Patterns of behavior of professionally managed and independent investors. J. Bank. Finance 25(8), 1573–1587 (2001)

Singleton, K.J.: Asset prices in a time series model with disparately informed, competative traders (1986)

Tsay, R.S.: Analysis of financial time series, vol. 543. Wiley, Hoboken (2005)

Tversky, A., Kahneman, D.: Belief in the law of small numbers. Psychol. Bull. 76(2), 105 (1971)

Tversky, A., Kahneman, D.: Judgment under uncertainty: Heuristics and biases. Science 185(4157), 1124–1131 (1974)

Wang, J.: A model of competitive stock trading volume. J. Polit. Econ. 127–168 (1994)

Weber, M., Camerer, C.F.: The disposition effect in securities trading: an experimental analysis. J. Econ. Behav. Org. 33(2), 167–184 (1998)

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

This paper is written in partial fulfilment of the requirements for the degree of D.Phil. in Economics at University of Oxford, UK. The author has received financial support from Royal Economics Society and Department of Economics at University of Oxford.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

I am very grateful to my D.Phil. supervisors Sujoy Mukerji, Han Ozsoylev and Vincent Crawford for their support in writing this paper. I am also grateful to constructive comments of three referees. I also thank Subir Bose, Sylaja Srinivasan, YX Wang, Wen Xu and other seminar participants at The Chinese University of Hong Kong, Shenzhen, Royal Economics Society Annual Meeting, Maastricht University, Queen Mary University, University of Oxford for their helpful comments. I thank the Royal Economics Society and Department of Economics at University of Oxford for financial support. This paper is written in partial fulfilment of the requirements for the degree of D.Phil. in Economics at University of Oxford, UK.

Appendices

Mathematical Appendix A

Proof of Proposition 1: (Kalman Filtering)

We first reformulate agents’ beliefs into state space models. The beliefs evolution therefore is described by Kalman FilteringFootnote 20. To be specific, the beliefs of the rational type described by (2) is already a standard state space model and is presented as below in (12), (13):

where \(V_1\sim {\mathscr {N}}(\mu ,\sigma ^2_V)\), \(\xi _{t}^{R}\sim N(0,\sigma _{\xi }^{2})\), \(\omega _{t}^{R}\sim N(0,\sigma _{\omega }^{2})\) and \(\sigma _{\omega }^{2}=0\).

Instead, the beliefs of type G in (3), (4) can be reformulated into a state space model as in (14), (15) by letting \(\epsilon _{t}\equiv \underset{k=0}{\overset{t}{\varSigma }}\delta ^{k}\kappa _{t-k}\):

where

Similar to the rational case, we assume \(V_1\sim {\mathscr {N}}(\mu ,\sigma ^2_V)\), \(\xi _{t}^{G}\sim N(0,\sigma _{\xi }^{2}),\;\omega _{t}^{G}\sim N(0,\sigma _{\omega }^{2}),\) and \(\sigma _{\omega }^{2}=0\). We further assume \(\epsilon _0=\kappa _{0}=\xi _0^G\) and is randomly drawn from \({\mathscr {N}}(0, \sigma ^2_\xi )\) implying both types of investors have the same priors on V so that the assumption \({\mathscr {F}}_0^i={\mathscr {F}}_0\) above is satisfied. Compared to the state space model for the rational agents with \(V_t\) as the state variable, the fallacy agents’ problem have two state variables, \(V_t\) and \(\epsilon _t\).

The rational investor’s recursive-filtering problem is standard. The results are directly from Tsay [40], Chapter 11.1. We only prove the problem for the fallacy investors.

The problem described in (14), (15) can be reformulated as below:

And we have

Use the formula for the conditional expectation of the bivariate normal distribution, we have

where

Furthermore, it is easily to show that

Let \(K_{t}=\varUpsilon Cov_{G}\left( S_{t},\; v_{t}^{G}\right) Var_{G}\left( v_{t}\right) ^{-1}\), we proved that

Next, we prove the recursive equation for the conditional variance.

It is easy to show that

Bring it back to the original formula, we prove that

The formula of \(K_t\) can be easily derived from here.

The definitions of \(\varOmega _t\), \(L_t\), \(H_t\) and Y are defined as below:

\(\square \)

Proof of Proposition 2(Linear Equilibrium) and Proposition 4(Optimal Holdings )

Step 1: Conjectured Price

Assumption 1

Given the economy defined in Sect. 2.1 and two type of investors with beliefs defined in Equation (2)-(4), there exists a competitive equilibrium, in which the price of the risky asset is a linear function of the state variables of the economy:

where \(\alpha _{t}=\left[ \alpha _{0,t},\;\alpha _{1,t},\;\alpha _{2,t},\;\alpha _{3,t}\right] \) is a \(1\times 4\) vector.

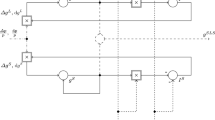

We use \(P_{t}\) and \(Q_{t}\) to denote the stochastic process of real price and return. Because beliefs are different, we further use \(P_{t}^i\) and \(Q_{t}^i\) to denote the beliefs of type i on the stochastic process of \(P_t\) and \(Q_t\), and \(\varPsi _t^i\) to denote the beliefs on the stochastic process \(\varPsi _t\)Footnote 21. Given the assumption in Step 1, we have the following Lemma 3.

Lemma 3

(Price and Return Process) In a linear equilibrium where \(P_t=\alpha _t\varPsi _t\), \(Q_t\) and \(\varPsi _t\) are both measurable with respect to \({\mathscr {F}}_t\) and take the following Gaussian processes under information \(\{{\mathscr {F}}_{t}:1\le t\le T\}\) for type i, \(i\in {R,G}\):

where \(v_{t+1}^i\) are signal shocks defined as before and are normally distributed conditional on \({\mathscr {F}}_t\); \(A_{\varPsi ,t}^i\) are \(4\times 4\) matrices, \(A_{Q,t}^i\) are \(1\times 4\) vectors, \(B_{\varPsi ,t}^i\) are \(4\times 1\) vectors and \(B_{Q,t}^i\) are constants given below.

Assume \(P_t=\alpha _t\varPsi _t\) holds, we first prove the Lemma 3. The way to derive \(A_{\varPsi ,t}^i\) and \(B_{\varPsi ,t}^i\) is from the recursive process presented in Proposition 1. We only give the proof for \(A_{\varPsi ,t}^G\) and \(B_{\varPsi ,t}^G\) and use similar method, we can derive \(A_{\varPsi ,t}^R\) and \(B_{\varPsi ,t}^G\).

From G’s perspective,

similarly,

These equations above give us the expression that

Similarly, we have

Furthermore, given the assumption that \(P_t=\alpha _t\varPsi _t\), we can show that from G’s perspective,

Reorganise the right hand according to \(V_{t+1|t}^R\), \(V_{t+1|t}^G\), \(\epsilon ^{G}_{t+1|t}\) and \(v_t^G\) will give give us the matrix \(A_{Q,t+1}^G\) and \(B_{Q,t+1}^G\) in the Proposition, that is: \(A_{Q,t}^{G}=\alpha _{t}A_{\varPsi ,t}^{G}-\alpha _{t-1} \), \(B_{Q,t}^{G}=\alpha _{t}B_{\varPsi ,t}^G\). Similarly, we have \(A_{Q,t}^{R}=\alpha _{t}A_{\varPsi ,t}^{R}-\alpha _{t-1}\), \(B_{Q,t}^{R}=\alpha _{t}B_{\varPsi ,t}^R. \) \(\square \)

Notice that based on Definition 1 and given the Proposition 2 holds, the real stochastic process of the state vector of the economy and excess return must coincide with the beliefs of the rational investors because their beliefs \(y^i_t\) are correct. Therefore, the real process of \(\varPsi _t\) and \(Q_t\) can be written as

We further move on to the optimization problem which determines the optimal portfolios of two types of investors.

Step 2: optimization

With Gaussian assumptions on the price process in Step 1 and Lemma 3 and under the CARA utility function assumption, the optimization problem defined by Eqs. (7), (8) can be solved using dynamic programming.

Let \(J(W_{t}^{i};\;\varPsi ^i_{t},\; t)\) be the value function of type i, we have the Bellman equation below:

The optimization problem (7), (8) is equivalent to the following problem:

Given the Lemma 3, we can derive Proposition 4. We prove the Proposition 4 by solving the optimization problem.

Assume the value function take the following format:

The first term represents the utility from the current investment, and the second term represents a risk adjusted utility from future investment.

We plug the Gaussian process of \(Q_{t+1}^i\) and \(\varPsi _t^i\) into the proposed value function and we have:

where

Differentiate the value function with respect to \(X_t^i\), and from the F.O.C., we have

where

The second order condition for optimality holds because \(B_{Q,t+1}^{i}\theta _{t+1}^{i}B_{Q,t+1}^{i\mathbf {T}}>0\). Since \(A_{Q,t+1}^{i}\) is defined by Eqs. (16) and (17), we have \(A_{Q,t+1}^{i}\varPsi _t=E_i(Q_{t+1}^i|{\mathscr {F}}_t)\). Define \(\varGamma _t^i\equiv \left( B_{Q,t+1}^{i}\theta _{t+1}^{i}B_{Q,t+1}^{i\mathbf {T}}\right) ^{-1}\) and \(g_t^i\equiv B_{Q,t+1}^{i}\theta _{t+1}^{i}B_{\varPsi ,t+1}^{i\mathbf {T}}U_{t+1}^{i}A_{\varPsi ,t+1}^{i}\), we then have the conclusion in Proposition 4.

Furthermore, we need to show that

is the right format of the value function. This is the correct value function if we can find the right format of \(U_t^i\). To do this, we substitute \(X_{t}^{i}=\dfrac{1}{\lambda }F_{t}^{i}\varPsi _{t}\) into the Bellman equation, that is

Footnote 22 Define

We have

From here, we can derive the right form of \(U_t^i\):

where \(I_{11}\) is a \(4\times 4\) zero matrix with only the first row, first column element equal to 1. Therefore, the conjectured format of \(-\rho ^i_{t+1}exp\left\{ -\lambda W_{t}^{i}-\frac{1}{2}\varPsi _{t}^{i\mathbf {T}}M_{t}^{i}\varPsi _{t}^{i}\right\} \) holds.

If the conjectured price is correct as in Proposition 2, we then complete the proof for Proposition 4. We prove this in Step 3.

Step 3. market-clearing and Equilibrium Price

The last step to prove the Proposition 2 and Proposition 4 is to show that the equilibrium price derived from the market-clearing condition is consistent with the proposed equilibrium price function in Step 1.

Since investors in this model are assumed to be non-myopic, given the optimal demands of both types solved in Step 2, the market-clearing conditions can be applied backwards recursively to derive the equilibrium price in each period.

To be more specific, the market-clearing condition is \(\underset{i\in {\mathscr {I}}}{\sum }X_{t}^{i}=0\), for \(t=1,\ldots ,T-1\). We first find the equilibrium price function at \(T-1\). The dollar return at T is \(Q_T=V-P_{T-1}\) and the equilibrium price can be solved explicitly. There is a continuum of investors on \([0,\; 1]\), with m proportion of rational investors and \(n=1-m\) proportion of fallacy investors in the market, investor i’s optimal demand at \(T-1\) has the linear form:

From market-clearing condition at \(T-1\):

we derive the explicit format for \(P_{T-1}=\alpha _{T-1}\varPsi _t\), where

Proposition 10 below shows that from \(\alpha _{T-1}\), the parameter vector \(\alpha _{t}\) for any period t exist and is uniquely determined recursively.

Proposition 10

(Recursive Process) The equilibrium price \(P_t\) is linear in \(\varPsi _t\) with the parameter vector \(\alpha _t\) uniquely determined by the following recursive process:

where \({\overline{E}}_{t+1}\) is a \(4 \times 4\) matrix fully determined by m, \(\lambda \), \(A_{\varPsi ,t+1}^i\), \(B_{\varPsi ,t_1}\), \(A_{Q,t+1}^i\), \(B_{Q,t_1}\), \(\varSigma ^i_{V,t|t-1}\), \(Var(v^i_{t+1})\).

The final step to complete the proof is to show that we can recursively solve the problem as shown in Proposition 10. Below, we present the proof of Proposition 10. By Definition 1, the proof for Proposition 2 can also be extended to derive a competitive equilibrium where the real signals have serial correlation. The equilibrium price process is still linear in the state variables of the economy but the real stochastic process will evolve according to the beliefs of the fallacy agents.

We first present the Proposition 10 completely and show the detailed format of related matrices involved.

Parameters in the equilibrium are determined by the following recursive process:

with II a \(4\times 4\) zero matrix except the up-left corner set to 1.

We also have the following recursive equations:

From Lemma 3, we have \(A_{Q,t}^{i}=\alpha _{t}A_{\varPsi ,t}^{i}-\alpha _{t-1}\) and \(B_{Q,t}^{i}=\alpha _{t}K_{t}\). Substitute these two formulas into \(F_t^i\):

where \(E_{t+1}^{i}=A_{\varPsi ,t+1}^{i}-K_{t+1}B_{\varPsi ,t+1}^{i\mathbf {T}}\theta _{t+1}^{i}U_{t+1}^{i}A_{\varPsi ,t+1}^{i}.\) Since \(\varPsi _t^R=\varPsi _t^G\), substitute \(X_{t}^{i}=\dfrac{1}{\lambda }F_{t}^{i}\varPsi _{t}\) into the market-clearing condition \(mX_{t}^{R}+nX_{t}^{G}=0,\) we have

Furthermore, substitute (31) into (32):

Define \({\overline{E}}_{t+1}\equiv \left( \dfrac{m}{\theta _{t+1}^{R}}+\dfrac{n}{\theta _{t+1}^{G}}\right) ^{-1}\left( \dfrac{mE_{t+1}^{R}}{\theta _{t+1}^{R}}+\dfrac{nE_{t+1}^{G}}{\theta _{t+1}^{G}}\right) ,\) we have \(\alpha _t=\alpha _{t+1}{\overline{E}}_{t+1}\) and \({\overline{E}}_{t+1}\) is a \(4\times 4\) matrix. Therefore, as long as we know the \(\alpha _{T-1}\), we can solve the linear equilibrium price and the parameter matrices \(A^i_{Q,t}\) and \(B_{Q,t}^i\) at any date t recursively.

The last period problem is fairly easy to be solved. It is equivalent to the last period solution as in a 3 period model presented in Brunnermeier [10] text book. The last period \(U_{T-1}^i\) is solved directly from the last period Bellman equation. The last period \(\alpha _{T-1}\) is shown in equation 20 while the exact format of \(U_{T-1}\) is given as below:

where

A 3-period example of this proof is given in the Appendix B to demonstrate the recursive process.

Proof of Proposition 3: (Rational Benchmark)

In a single type market, at time t, because from the perspective of that type, the current equilibrium price must fully reflects all the informations up to t and the future expected returns must be 0, we have the \(i\in {\mathscr {I}}\) type’s optimal demand as follows:

Therefore, we have

We proved the part 1 of Proposition 3 and Lemma 1.

Furthermore, the result that the equilibrium price \(P_{R,t}\) is a martingale sequence comes directly from the nature of Kalman filtering because the \(P_{R,t}\) takes the expectation of the liquidation value, which is a martingale sequence under the rational investor’s belief setting. We also prove that \(E_{R}\left[ Q_{R,t+k}|{\mathscr {F}}_{t}\right] =0\) because the returns \(Q_{R,t}\) is a martingale difference sequence.

Finally, we point out that \(Corr_{R}\left( Q_{t_1}^{R},\; Q_{t_2}^{R}\right) =0\) comes directly from the property of a martingale difference sequence. We proved the Proposition 3\(\square \)

Proof of Proposition 5 and Proposition 6: (Expectations in the Mixed Market)

We only give the proof for Proposition 5. Results in Proposition 6 can be derived by expressing the state variables of the economy recursively as in the proof for Proposition 5.

We finished out proof for Proposition 5. \(\square \)

Proof of Proposition 7: (Market Dominance)

We present the proof for the last two periods. The proof of other periods are similar to the last period and can be seen from the backwardation.

As shown before in the proof of Proposition 2, we first derive that at \(t=T-1\),

where

Define \(b_{d}\equiv \dfrac{\beta }{\delta -\beta }\), we have

Furthermore, we have

For simplicity, we omit the subscription \(T-1\) and we have

where \(L^{i}=(K^{R}-K^{G})u^{i}\theta ^{i}\). We have \({\overline{E}}=\dfrac{\frac{m}{\theta ^{R}}E^{R}+\frac{n}{\theta ^{G}}E^{G}}{\frac{m}{\theta ^{R}}+\frac{n}{\theta ^{G}}}\).

We further define \({\bar{E}}\equiv \frac{m}{\theta ^{R}}E^{R}+\frac{n}{\theta ^{G}}E^{G}\) as the numerator of \({\overline{E}}\). Define \(D^{R}\equiv \dfrac{L^{R}}{\theta ^{R}}=\left( K^{R}-K^{G}\right) u^{R}\), \(D^{G}\equiv \dfrac{L^{G}}{\theta ^{G}}=\left( K^{R}-K^{G}\right) u^{G}\). Define the j’th column of \({\bar{E}}\) as \({\bar{E}}_{(:,j)}.\) We have \({\bar{E}}_{(:,1)}\) as below:

Since \(\alpha _{t}=\alpha _{t+1}{\overline{E}}_{t+1}\) where \({\overline{E}}_{t+1}\equiv \dfrac{{\bar{E}}_{t+1}}{\frac{m}{\theta ^{R}}+\frac{n}{\theta ^{G}}}\), we have

Elements in \(\alpha _{T-2}\) are the follows:

In all the elements above, on both left and right hand sides of equations, the variables without the time t notation are at \(T-1\).

We first prove the part 1 in the proposition, that is \(\alpha _{0,t}=0\) for all t.

Since \(\alpha _{0,t} = \alpha _{t+1} {\bar{E}}_{(:,1)}\) and the \({\bar{E}}_{(:,1)}\) has the general form shown above, with \(\alpha _{0,t+1}=0\), we have \(\alpha _{0,t} = 0\).

Next, we prove part 2 of the proposition, that is, \(\alpha _{1,t}+\alpha _{2,t} = 1\).

To do so, we sum the left and right hand sides of Eqs. 34 and 35 , and we have the followings,

The last step holds as the items in the two vectors cancel out each other.

Furthermore, on both sides of the above equation, the omitted notation t of \(\frac{m}{\theta ^{R}}+\frac{n}{\theta ^{G}}\) are at \(T-1\), and since they are scalars, we can cancel them out from both sides. Therefore, we have \(\alpha _{T-2,1}+\alpha _{T-2,2}=\alpha _{T-1,1}+\alpha _{T-1,2}=1\)

Since the proof above does not depend on t, the result can be generalised to any time t, that is \(\alpha _{t,1}+\alpha _{t,2}=1\). We complete the proof of Proposition 7. \(\square \)

Proof of Proposition 9 and Lemma 2: (Volatility)

with \(G_{t}^{R}=A_{\varPsi ,t}^{R}-\left[ \begin{array}{cccc} 0 &{} 1 &{} 0 &{} 0\\ 0 &{} K_{t}^{R} &{} 0 &{} 0\\ 0 &{} K_{t}^{G} &{} 0 &{} 0\\ 0 &{} k_{t} &{} 0 &{} 0 \end{array}\right] \) for simplicity. Furthermore, we have

Substitute equation (37) into equation (36) and reformat the equation we have

Therefore, we have

where \(D_{n}=\left( \overset{t-1}{\underset{l=n+1}{\varPi }}G_{n}\right) B_{\varPsi ,n}^{R}\).

Expand the last equation, we can easily derive the conclusion in the Proposition.

To derive the result in Lemma 2, write

We complete the proof for Lemma 2. \(\square \)

Proof of Proposition 8: (Autocorrelation)

Expand \(Q_i\) recursively and use the results in Proposition 3 on the \(Cov^R(v_i,\;v_j)\) we have

where the format of the \(Var^{R}\left( \varPsi _{t}\right) \) is shown in the proof of Proposition 9.

Mathematical Appendix B

A 3-period Proof of the Equilibrium:

Consider a simple 3-period problem where the traders’ expected utility function is given by:

Using backward induction, at period \(t=2\), the optimization problem is

From the first-order condition, we have \(X_{2}^{i}=\dfrac{V_{3|2}^{i}-P_{2}}{\lambda \varSigma _{V,3|2}^{i}}\). Together with \(P_{2}=\alpha _{2}\varPsi _{2}\), we have \(X_{2}^{i}=\dfrac{(I_{1}-\alpha _{2})\varPsi _{2}}{\lambda \varSigma _{V,3|2}^{i}}\), where \(I_{1}=[0,1,0,0]\), and \(F_{2}^{i}=\dfrac{I_{1}-\alpha _{2}}{\varSigma _{V,3|2}^{i}}\).

Plug \(X_{2}^{i}=\dfrac{(I_{1}-\alpha _{2})\varPsi _{2}}{\lambda \varSigma _{V,3|2}^{i}}\) into the original utility function, we can derive the value function at \(t=2\):

where \(U_{2}^{i}=\dfrac{(I_{1}-\alpha _{2})^{\mathbf {T}}(I_{1}-\alpha _{2})}{\varSigma _{V,3|2}^{i}}\).

Use the market-clearing condition: \(mX_{2}^{R}+nX_{2}^{G}=0\), we have

thus

Therefore, \(\alpha _{2}=[0,\dfrac{m\varSigma _{V,3|2}^{G}}{m\varSigma _{V,3|2}^{G}+n\varSigma _{V,3|2}^{R}},\dfrac{n\varSigma _{V,3|2}^{R}}{m\varSigma _{V,3|2}^{G}+n\varSigma _{V,3|2}^{R}},0]\). Plug it into \(U_{2}^{i}\), we have

This is exactly what we have in the general problem. Similar for \(U_{2}^{G}\).

Use backward induction, the problem we want to solve at \(t=1\) is

In a linear equilibrium, we have

\(Q_{2}^{i}=A_{Q,2}^{i}\varPsi _{1}+B_{Q,2}^{i}v_{2}^{i}\), and \(\varPsi _{2}^{i}=A_{\varPsi ,2}^{i}\varPsi _{1}+B_{\varPsi ,2}^{i}v_{2}^{i}\). Plug these two processes into the optimization problem, the expectation can be removed and replaced by a linear function of conditional expectations and variances. That is equation (18).

where \(C_{2}^{i}\), \(\theta _{2}^{i}\) and \(\rho _{2}\) are simply functions in \(U_{2}\) as expressed in the equation (18).

The first-order condition of the maximization problem gives that

Substitute \(X_{1}^{i}=\dfrac{1}{\lambda }F_{1}^{i}\varPsi _{1}\) into

we have

By the assumption that \(J(W_{1};X_{1};1)=-exp\{-\lambda W_{1}^{i}-\dfrac{1}{2}\varPsi _{1}^{\mathbf {T}}U_{1}^{i}\varPsi _{1}\}\), we let

which give us that \(U_{1}^{i}=-2ln\rho _{2}^{i}I_{11}+M_{1}^{i}\), where \(M_{1}^{i}\) is a function of \(U_{2}^{i}\) and is known. The expression of \(M_{1}^{i}\) is given in the general proof.

Similar as in the process of deriving \(\alpha _{2}\), the only undetermined parameter at this stage is \(A_{Q,2}^{i}\), which contains \(\alpha _{1}\). \(U_{1}^{i}\) is still a function of \(\alpha _{1}\). To derive the \(\alpha _{1}\), we further apply the market-clearing condition: \(mX_{1}^{R}+nX_{1}^{G}=0\).

Substitute \(X_{1}^{i}=\dfrac{1}{\lambda }F_{1}^{i}\varPsi _{1}\) into the market-clearing condition, we have

Since it holds for any value of \(\varPsi _{1}\), we have

Substitute \(A_{Q,2}^{i}=\alpha _{2}A_{\varPsi ,2}^{i}-\alpha _{1}\) and \(B_{Q,2}^{i}=\alpha _{2}K_{2}\) into

we have \(F_{1}^{i}=\dfrac{1}{\left( \alpha _{2}K_{2}\right) ^{2}\theta _{2}^{i}}\alpha _{2}E_{2}^{i}-\dfrac{1}{\left( \alpha _{2}K_{2}\right) ^{2}\theta _{2}^{i}}\alpha _{1}\), where \(E_{2}^{i}=A_{\varPsi ,2}^{i}-K_{2}B_{\varPsi ,2}^{i\mathbf {T}}\theta _{2}^{i}U_{2}^{i}A_{\varPsi ,2}^{i}\) and is known. Plug the formula into the market-clearing condition, we have

which gives us the expression of \(\alpha _{1}\) as a function of \(\alpha _{2}\), that is

where \({\overline{E}}_{2}\equiv \left( \dfrac{m}{\theta _{2}^{R}}+\dfrac{n}{\theta _{2}^{G}}\right) ^{-1}\left( \dfrac{mE_{2}^{R}}{\theta _{2}^{R}}+\dfrac{nE_{2}^{G}}{\theta _{2}^{G}}\right) \) and is known. \(\square \)

Appendix C: Non-zero net supply

Information shock on expected price. This figure plots the rational expectation in price after a signal shock at \(t=10\). Parameters are set at the following values: \(m=0.5\), \(T=50\), \(\lambda =1\), \(\delta =0.8\), \(\beta =0.6\), \(\sigma _\xi ^2=1\), \(\sigma _V^2=1\)

We assume \(\varTheta =0\) for simplicity because a positive \(\varTheta \) together with the learning process generates non-zero correlations in prices, making the analysis of a signal shock on the prices and returns less clear.

By changing the net supply of the stock \(\varTheta \) into positive, the equilibrium price now contains a constant term, that is \(\alpha _{0,t}\ne 0\).

It can be shown that \(\alpha _{1,t}\), \(\alpha _{2,t}\) and \(\alpha _{3,t}\) still evolve as in the main paragraph while \(\alpha _{0,t}\) can be derived as below:

where \({\overline{E}}_{(:,1)}\) is the first column of matrix \({\overline{E}}\). Consistent with previous studies, \(\alpha _{0,t}\) is negative, reflecting the risk-averse attitude. Simulation shows that \(\alpha _{0,t}\) increases over time because more information reduces the risk in variance, thus strengthening demands and boosting the asset price.

Another change lies in the optimal demands of two types from the simulation results. Simulations show that \(F^R_t\) and \(F^G_t\) now also contain a constant term. That is

The effect of \(F_{1,t}^i\) is independent of \(F_{d,t}\) and \(F_{\epsilon ,t}\).

Signs of the constant term \(F_{1,t}^i\) reflect that the rational investors turns from long to short positive. The constant term reflect the risk attitudes of the investors, indicating that the rational investors are comparatively more risk-averse in the market when the liquidation date is close. This result is consistent with the analysis in Proposition 7.

With a positive net supply, even the price in the pure rational market increases as the risk in variance decreases over time. Here we provide the simulation results for the prices and returns following a signal shock. Results are similar to what we have before except the price has a general increasing trend as shown in Fig. 13. Other simulation results are available on request.

Rights and permissions

About this article

Cite this article

Chen, S. Information and dynamic trading with the Gambler’s fallacy. Math Finan Econ 16, 399–446 (2022). https://doi.org/10.1007/s11579-021-00305-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11579-021-00305-1