Abstract

China has long exercised environmental control through the imposition of sewage charges. The start of the environmental protection tax on January 1, 2018, means that China has entered a new phase of environmental control. Unlike many previous studies on the role of environmental taxes at the firm level, this paper examines whether environmental taxes affect pollution emissions by influencing the behavioral choices of micro-actors. This paper first reviews the Pyrrhic tax, the Porter hypothesis, and the “double dividend effect.” We then construct provincial panel data for 30 provinces in China from 2012 to 2019 as a sample, use the environmental protection tax as a natural experiment to evaluate the policy of this environmental protection tax using propensity score matching and difference-in-differences model, investigate the intermediate transmission mechanism of the policy implementation, and then analyze the differences in policy effects between provinces with different levels of economic development. The increased tax burden in 2018 led to a general reduction in provincial pollution emissions in which technological innovation by various groups, including firms and universities, had a mediating role.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

The 2018 environmental protection tax is a major policy for China in terms of environmental protection. The law taxes 117 major pollutants in four categories: air pollutants, water pollutants, solid wastes, and noise nationwide. Other countries have implemented environmental taxation systems earlier than China, and the development of more mature ones is mainly in the USA, Denmark, Sweden, etc. For example, the development of environmental protection tax in the USA, mainly from the 1970s, has formed the federal government and state governments two levels of the environmental protection tax system; Denmark has been a leader in environmental taxation, and Denmark’s carbon tax has a greater impact on emissions than other Nordic countries (Harrison 2010; Sumner et al. 2011). The effects of environmental tax–related policies in these countries have been studied in the literature finding environmental taxes and R&D in reducing carbon emissions (Safi et al. 2021). However, there is a non-linear relationship between the impacts of carbon tax revenues on energy innovation (Cheng et al. 2021). Furthermore, some studies have found that the stringency of environmental policies has different effects across technology countries and firms with different productivity (Albrizio et al. 2017), which has considerable implications for understanding the assessment of the policy effects of environmental taxes being constructed in China.

Internationally, environmental taxes are not intended to generate revenue for governments but to change the behavior of households and companies (Delgado et al. 2022). Due to the historical issue of “fee to tax,” China’s environmental protection tax law only targets the act of pollutant emission, others related to environmental issues need further improvement. Like the environmental tax collection rules in other countries, China’s environmental protection tax is based on the number of emissions of pollution factors with the same degree of pollution hazard. It sets a differentiated pollution equivalent value for polluting factors with different degrees of harm. At the same time, it also sets a related tax benefit. Compared to emission fees, imposing environmental protection tax on the polluters concerned will create a stable expectation of paying environmental protection tax.

Therefore, the research in this paper is associated with two types of studies. One is the study on reducing pollutant emissions due to environmental taxes. From the existing literature, it can be found that it is controversial whether environment-related taxes lead to a reduction in energy consumption and emissions (Shahzad 2020); some studies affirm the positive effect of environmental taxes on reducing pollutant emissions and improving the environment (Borozan 2019; Chien et al. 2021); other studies argue that whether environmental taxes work depends on other factors (Lin and Li 2011), such as the stringency of the policy (Wolde-Rufael and Mulat-Weldemeskel 2021). Second, studies on environmental taxes affect pollutant reductions by influencing the technological innovation pathways (Acemoglu et al. 2016; Aghion et al. 2016). Some studies demonstrate that environmental taxes drive technological innovation in high- and middle-income countries (Karmaker et al. 2021). However, the effects of technological innovation are heterogeneous at the firm level because of path dependence (Aghion et al. 2016); also, the benefits of technological innovation do not necessarily outweigh the costs of regulation (Dechezleprêtre and Sato 2017), while some studies argue that environmental taxes do not have a theoretical boost for technological innovation (Kemp and Pontoglio 2011). Some scholars argue that in the absence of capacity constraints, firms do not generate the effect of the Porter hypothesis in the face of environmental tax pressures and will instead resort to capacity expansion to offset tax costs, thereby inhibiting the ability to innovate green (** et al. 2017; Lu et al. 2019). Some studies suggest that the reason for this is that the impact of tax costs on firms’ choice of green technology is not entirely linear but has an inverted “U”–shaped relationship; thus, the promotion effect has a certain lag (Wang et al 2021). That is, in the short run, the environmental tax increases the cost of business, but in the long run, it achieves the theoretical result of the Porter hypothesis of “compensation for innovation” (Guo 2021).

There are many literatures that have explored the emission reduction effect of China’s environmental protection tax (Liu and Zhang 2018) and the impact on the business performance of specific provinces, specific industries, and listed enterprises (Yu et al. 2019; Long et al. 2021). However, existing research remains controversial as to what the specific effects of environmental protection taxes are and how they affect the mechanism of action by influencing the behavioral choices of micro-actors and thus the reduction of pollution emissions in a given region. This paper argues that the contradictory findings of previous studies stem from the differences in the samples and time periods selected by different research articles. However, it appears that environmental protection taxes have a positive impact on firms’ technological innovation and business performance in the long run. While previous studies have not concluded what the mechanism of influence between the two is nor have they combined micro-actor choice and macro-performance, this paper focuses on the mechanistic path of whether environmental protection taxes affect the total amount of pollution emissions by influencing the technological innovation of each micro-actor.

The empirical results of this paper show that China’s environmental protection tax has led to a general decrease in emissions at the provincial level by promoting technological innovation among provincial micro-actor and that the effect of the policy is more pronounced in the provinces with better economic development. The contribution of this paper is to enrich the research on the mechanism of how environment-related taxes can achieve macro-pollution reduction by influencing technological innovation of micro-actors.

Therefore, this paper establishes the hypotheses of this paper by combing the relevant literature in the second part, then organizes and analyzes the panel data at the provincial level in China in the third part, applies propensity score matching and difference-in-differences (PSM-DID) to test the impact of environmental protection tax on pollution emissions in specific provincial administrative regions, and discusses whether the technological innovation capacity of each group within the province plays a mediating role in the impact of environmental protection tax on pollution emissions in each province. Robustness tests are also conducted. Finally, in the “Conclusions and policy recommendations” section, the corresponding policy recommendations are presented.

Theoretical analysis and hypothesis derivation

Tullock first introduced the double dividend effect in 1976. A company adopting environmentally friendly technological innovation will create a double dividend (Pearce 1991). The first dividend is environmental: pollution emissions are reduced, thus protecting the environment. The second dividend effect is the economic dividend: enterprises’ green technology research and development will lead to enterprise and social economic development. The double dividend effect is often found in the literature that studies corporate environmental behavior, stimulates environmental protection, and examines policies’ environmental and non-environmental goals.

In studies related to environmental protection taxes, there is the question: did the introduction of environmental protection taxes in 2018 achieve a double dividend effect? To answer this question, one must examine the environmental and non-environmental objectives achieved by the environmental protection tax. As mentioned earlier, most researchers have focused on the performance of firms at the research level and their ability to innovate; i.e., they have studied the non-environmental objectives of the environmental protection tax but have not conducted in-depth research on the impact of pollution emissions (Sun and Yuan 2020; Guo 2021; Liu and Shao 2021). This paper, on the other hand, aims to investigate the environmental objectives of environmental protection taxes, i.e., whether the motivation for technological innovation among provincial groupsFootnote 1 follows the double dividend effect.

By combing the literature and researching and discussing, this paper can tentatively conclude that the collection of environmental protection tax will lead to the reduction of corporate emissions, which will then lead to the reduction of provincial emissions. The mechanism that leads to such a situation is unknown for the time being. In order to explore the mechanism, according to which, this paper proposes the first hypothesis:

-

H1: Environmental protection taxes act as a disincentive for pollutant emissions in the provinces.

There have been many theoretical studies on how to solve the problem of externalities caused by private production since Pigou. For example, some scholars have argued that excessive environmental taxes impose production costs on firms and discourage their willingness and ability to innovate greenly, thus discouraging the reduction of pollution emissions and making it difficult to achieve the purpose of the tax. On the other hand, the “Porter hypothesis” suggests that if the environmental tax is moderate, even though the cost of the tax will increase in the short run, in the long run, firms will be able to gain future efficiency gains from technological innovation, which will lead to increased innovation behavior. Thus, “innovation compensation” is the main element of Porter’s hypothesis. In other words, if firms are willing to actively innovate under environmental regulations, they can achieve what was mentioned before: they can improve their productivity and competitiveness while attracting consumer attention and investment opportunities.

That is, environmental protection taxes achieve a reduction in corporate emissions by increasing the technological innovation behavior of firms. Existing studies have also investigated whether green innovation technologies can play a mediating effect (Li et al 2021; Wang et al 2021). However, it is still controversial whether environmental protection taxes can force firms to increase their technological innovation behavior. Based on this, this paper delves further and proposes a second hypothesis:

-

H2: Innovative technologies play a role in mediating the effect of environmental protection taxes on the process of pollution emission reduction.

EPT policy evaluation and its intermediary effect empirical analysis

The data in this paper include panel data for 30 provinces in China from 2012 to 2019. The main data features include industrial sulfur dioxide emissions, year’s average GDP, annual industrial added value, actual foreign investment, and annual green patent applications. The data comes from the “China Statistical Yearbook,” “China Statistical Yearbook On Environment,” “China Urban Construction Statistical Yearbook,” and the statistical yearbooks of cities in provinces and other network data. Due to the lack of data in Tibet, this paper collected a total of 240 observations from 30 provincial-level administrative regions in 8 years and manually collated the above datasets to form the complete panel data of the empirical part of this paper. Data preprocessing and subsequent regression are completed by Excel and stata15.1.

Variable selection, descriptive statistics, and correlation analysis

Variable selection

In this paper, we take the official implementation of the environmental protection tax on January 1, 2018, as the exogenous policy shock point in time and construct the time-point dummy variable D2: D2 = 0, when the data are from before 2018, and D2 = 1, when the data are from after 2018. The 30 provinces in China have their taxation standards for environmental protection tax, which are divided into “tax burden raising” and “tax burden shifting.” The provinces implementing the “tax rate increase” are Hebei, Jiangsu, Shandong, Henan, Hunan, Sichuan, Chongqing, Guizhou, Hainan, Guangxi, Shanxi, and Bei**g. The provinces implementing the “tax rate shift” are Hubei, Zhejiang, Fujian, Jilin, Anhui, Jiangxi, and Shaanxi. The group of “tax burden raising” is the treatment group, and the group of “tax burden shifting” is the control group, generating the group dummy variable D1: D1 = 0, when the data comes from the control group; D1 = 1, when the data comes from the treatment group. The interaction term of D1 and D2 is the core explanatory variable. In order to evaluate the policy effect of environmental protection tax from the perspective of environmental governance, we choose industrial sulfur dioxide, the main emission gas, as the instrumental variable, i.e., the explanatory variable. In addition, this paper selects the number of green patent applications by the province to measure the mediating variable, technological innovation. This paper selected the following control variables based on the available literature and model considerations: economic size, industrial size, and openness to the outside world. We standardize the variables here to eliminate their magnitudes. The specific variables are listed in Table 1.

Descriptive statistics

Descriptive statistics on the original data is the first step in data processing. The results of descriptive statistics are shown in Table 2.

As seen in Table 2, first, the original data are discrete, and the standard deviation of each variable is large. Standardization should be applied to the data of each variable to reduce the proportion of random error terms in the model. Second, the data dispersion is large, mainly in (1) industrial sulfur dioxide emissions: the extreme difference of this data is as high as 1,543,120, mainly caused by the difference in provinces. The development focus of each province and the geographical factors lead to a large difference in the industrialization degree of each city. Therefore, the model introduces economic and industrial scales as control variables. (2) Number of green patent applications: the extreme difference in this data is as high as 67,171. The reason for such a difference is still caused by the differences in the development strategy choice and economic scale of provinces. The data after standardization is shown in Table 3.

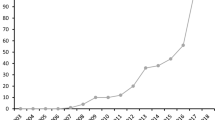

After the standardization process, the degree of dispersion of each data was well controlled. In addition, we averaged the explanatory variables stdso2 for each of the treatment and control groups to generate the more common trend plots of the explanatory variables. See the following figure for details.

The result shown in Fig. 1 shows that the average explained variables of the treatment group and the control group are relatively ideal and can form a quasi-natural experiment. Significantly, we should point out the data in 2015 and 2016. The noticeable collapse exists because the Environmental Protection Law of the People’s Republic of China was officially implemented on January 1, 2015, a national-scale curbing of pollution emissions. The data in the figure are year-end cross-sectional data, and the abscissa data in 2018 is the year-end cross-sectional data in 2018, so the policy implementation point should be in 2017 in the figure. Therefore, it can be seen from the figure that exogenous policies impact the explained variables at the time point in 2017, both groups show a downward trend, and it is obvious that the absolute value of the curve slope of the treatment group is larger. So the policy effect is initially observed. Group differences and year differences constitute a “double difference.”

Source: output result of stata15.1

Trend chart.

In addition, we also calculated the average GDP per capita and industrial SO2 emissions for each province for 8 years from the collected data. We used them to draw a heat map of GDP and a heat map of SO2. Figure 2 shows that the developed provinces in China are concentrated in the eastern coastal region and the capital city of Bei**g. This is due to the high degree of openness, abundant human capital, and active private economy in eastern China in the early years, which have kept the economic development in the eastern coastal provinces. From Fig. 3, we can find that the cities with higher industrial SO2 emissions in China are concentrated in the north, because in the early industrialization process of China, the northern cities developed heavy industries vigorously, and this trend has been influenced until now. Therefore, the sulfur dioxide emissions from northern provinces show a more obvious clustering effect on the heat map.

Source: output result of stata15.1

GDP heat map.

Source: output result of stata15.1

SO2 heat map.

Correlation analysis

Before establishing the econometric model for regression analysis, it is necessary to analyze the correlation between the variables. We simply carry out correlation analysis and research the correlation of various variables. The output results of correlation analysis are as follows (Table 4):

Through the correlation analysis, the results show that the correlation between the explained variables and the explanatory variables is significant. However, correlation analysis is the preliminary processing of the data. It is necessary to wait for the subsequent regression results and mechanism analysis to know the causal relationship between them. In addition, we can mainly see that the explained variable and the explanatory variable show a significant negative correlation. The explained variable and the intermediary variable also show a significant negative correlation. And there is a significant positive correlation between the intermediary and explanatory variables. With the correlation analysis, we will establish the parametric regression model of this paper.

Econometric model establishment

Based on the data preprocessing and correlation analysis, we establish a difference-in-differences (DID) two-way fixed effect model. Specific model 1, model 2, and model 3 are as follows:

Model 1 is the rudimentary model of hypothesis 2, which is used to research the impact of EPT on technology innovation, and the interaction term is the core explanatory variable. Model 2 is used to research hypothesis 1, which is the policy evaluation of the protective effect of EPT. At the same time, model 2 and model 3 become the second step in researching the intermediary effect of this paper. The research method refers to the mature mechanism analysis method of articles (Nicola et al 2004; Li and Feng 2021). We establish model 3, which adds the intermediary variable of technology innovation to model 2 to study the mechanism from the implementation of EPT to the effect of pollution control. With the regression results of model 1, we can judge whether this mechanism exists by comparing the coefficient estimation differences before the explanatory variables in model 2 and model 3. The implementation of EPT has led different groups in various provinces to choose technology innovation, which has reduced pollutant emissions. Therefore, the specific logical generalization of this paper is as follows: the first step is to research the relationship between explanatory variable X and intermediary variable M and determine that explanatory variables affect intermediary variables. The second step is to conduct the regression between the explanatory variable X and the explained variable Y and record the coefficient of X and then record the coefficient of X in model 3 that the intermediary variable M is introduced. Finally, the third step is to compare the difference between the two X coefficients. In this paper, H1 is proved to be true if the coefficient of X in model 2 is significantly negative. On the other hand, if the coefficient of M in model 1 is significantly positive, the coefficients of X and M in model 3 are significantly negative, and the X coefficient in model 3 increases compared with the coefficient of X in model 2. It can be considered that the negative effect provided by X is transferred to the intermediary variable M, and the intermediary effect in mechanism analysis is realized. Therefore, H2 can be proved.

Regression results and analysis based on PSM-DID

The result and analysis of PSM

In the documents mentioned above on the analysis of intermediary effect mechanism, the authors mostly use the method of 2SLS to regress to avoid the endogenous problem of the econometric model. Because this paper combines policy evaluation and the research of intermediary effect, we choose propensity score matching and a difference-in-differences model to suppress endogenous problems and approximate a random experiment. The choice of policy implementation is often linked to many aspects of the implementation location, such as economical scale, population density, and industrial proportion. Therefore, the core function of propensity score matching (PSM) is to find the samples in the control group that are the most suitable counterparts of the treatment group, which is to approximate a random experiment and to find the optimal ATE to estimate ATT. In addition, the advantage of the DID model is to solve the endogenous problem. The advantages of combining the two methods are reflected in many documents and are suitable for this paper, so we chose this research method. PSM needs to use cross-sectional data, so we select each observation’s data before implementing the matching policy. The matching method is a caliper nearest neighbor matching with N equal to 2 to obtain the weight of each observation. The matching effect and balance test results are shown in Fig. 4.

Propensity score before and after matching

Figure 4 shows that the degree of heterogeneity among samples is still quite large after the standardization of each sample data, i.e., the kernel density curves of groups before matching are more different. By caliper nearest neighbor matching with N equal to 2, the degree of sample dispersion becomes smaller; if we take N equal to 1, we will get a better clustering effect but will discard one-third of the sample number. On balance, the PSM with N equal to 2 is chosen in this paper. After PSM matching, the kernel density curves are relatively close, indicating good matching. As can be seen in Fig. 5, the deviation of the normalized mean values of the two data groups before matching is larger. After PSM, the standardized mean deviation of the three covariates is optimized. There is no significant difference between the samples before and after matching, so it passes the balance test. Furthermore, after PSM, the differences in stdagdp, stdind, and stdinv between the treatment group and the control group are reduced. In addition, we use a two-way fixed effect model, and the empirical model in this paper eliminates the heterogeneity. In stata15.1, we generate the average weight of each observation for subsequent DID model regression.

Source: output result of stata15.1

The result of the balance test.

Regression results and analysis of DID

After obtaining the weight of each observation through the PSM, aweight is used to introduce into the subsequent DID regression. The empirical results are as shown in Table 5.

For hypothesis 1, the implementation of EPT has an average inhibitory effect on the emission of pollutants in the treatment group. From the regression results of model 2 in Table 5, it can be seen that the estimated coefficient of the explanatory variable in model 2 is significantly negative, which means that the implementation of the policy has reduced the value of the explained variable by an average of 0.635 units. It shows that EPT can indeed play a role in restraining pollutant emissions at the provincial level. Hypothesis 1 is proved.

In response to hypothesis 2, the environmental protection tax causes a decrease in pollutant emissions in each province by pushing technological innovation in each province. The regression results of model 1 in Table 5, i.e., the regression results of the mediating variables as explanatory variables result in positive and significant coefficients of the pre-interaction term estimates of the explanatory variables, and the implementation of the policy did stimulate the technological innovation behavior of the organizations in the treatment group. Combined with the regression results of model 2 and model 3, it can be seen that the coefficient estimate of explanatory variables in model 3 is still significantly negative. And compared with the estimate in model 2, it becomes larger, or even its significance becomes weaker, which shows its own negative effects transfer to other variables. Under the condition that the estimated coefficient of each control variable does not change significantly, the coefficient of the intermediary variable is estimated to be significantly negative, so it can be understood that it decomposes the negative effect of the explanatory variable in model 2. To sum up, the multiple regression results show that the explanatory variable positively affects the intermediary variable. Then, the intermediary variable negatively affects the explained variable, which is the negative transmission mechanism in the intermediary effect. The practical significance is that under the implementation of EPT, organizations in various provinces tend to choose technology innovation behavior, which leads to the decline of pollutant emissions. Hypothesis 2 is proved.

Based on the above operation of the stata15.1 software, we have obtained intuitive empirical analysis results. However, for the empirical process and result analysis, we still need to carry out the robustness test to consolidate the persuasiveness of the empirical results.

Robustness test

Parallel trend test

Generate the time dummy variables pre, current, and post in stata15.1. Then, continue to generate the interaction terms of year dummy variables and group dummy variables, and then, remove the pre_1 before the policy as the benchmark variable. Finally, the above interaction terms are used as an explanatory variable for regression, and the following results and trend chart are obtained (Table 6 and Fig. 6).

Source: output result of stata15.1

Results of regression.

From the output, it can be seen that only the dummy variable coefficient of 2012 is significantly positive. On the whole, the regression results of dummy variables before the implementation of the policy are not significant, while the regression results of dummy variables after the implementation of the policy are significant. Moreover, PSM is selected to correct the observations’ heterogeneity in this paper. From the perspective of practical significance, the results show that before the implementation of EPT, the difference in sulfur dioxide emissions between the treatment group and the control group has no significant difference. Combined with the output of the parallel trend chart and the use of PSM, it shows that the results are robust through the parallel trend test.

Placebo test

The placebo test comes from the experimental design in biology or medicine. With the development of social science and the brilliance of causal inference, the placebo test has been introduced into the robustness test of many empirical articles. There are many similarities and differences between the placebo test in this paper and the randomized, double-blind experiment in drug experiments. The same is the repeated random experiment with many times or observations; different from the real two-group control in drug trials, the placebo test in this paper randomly selects the observations of the treatment group and the control group for multiple simulated regression. There are many forms of placebo tests. The method selected in this paper is suitable for DID to verify whether the conclusion is affected by unobserved factors. The results of three placebo tests for the three models in this paper are shown in Fig. 7.

Source: output result of stata15.1

The results of three placebo tests

The simulation times of the three placebo tests were 500. In the placebo test of model 1, only 19 of the 500 experiments have abnormal values higher than the benchmark regression, so the p-value of this experiment is 0.038, indicating that the results are significant. In the experiments of model 2 and model 3, there is no abnormal value in the simulation experiment, so the results are significant. It shows that the regression results and conclusions above are not affected by unobserved factors and pass the placebo test.

Benchmark regression analysis

This paper’s third robustness test method is the regression method selection’s robustness test. From the previous approximate hypothesis and parallel trend test, we understand the robustness of the above research methods. However, due to the complexity of researching practical problems, we still need more matching and regression methods to support the conclusion. Tables 7, 8, and 9 are the test results of various regression methods.

Tables 7, 8, and 9 show the result of four different regression methods of three models. The first column is the benchmark regression, which is the regression without propensity score matching using the mixed least square method. The second column is the result of regression using observations with non-empty weights after propensity score matching. The third column is the results of regression using observations that meet the common support hypothesis in propensity score matching. The fourth column is the result of regression with aweight. An important reason why we do not choose fweight is that fweight is a frequency weight, so it must be an integer. Introducing fweight into regression will cause problems, and the nuclear density curve generated with fweight is different from the nuclear density curve generated by the stata15.1 official generation propensity score matching test. The reason should still be the rounding of weights.

After analyzing the differences between the above regression methods, we further research the results of the four regression methods. It can be seen from Table 7 that by the benchmark regression, the coefficient of the explanatory variable is not significant, and we can find that the heterogeneity of the original data is serious. If DID is directly used for regression, the regression results are poor, because unbiased estimation cannot be obtained. There is no significant difference in the estimated coefficients of the results of the last three regression methods, and the estimated coefficients of the explanatory variables are all significantly negative and at the significance level of 1% or 5%. It shows that the relationship between policy implementation and technology innovation is verified by the three regression methods after using PSM, and model 1 is robust. It can be seen from Table 8 that the estimated coefficients of each variable of model 2 by the four regression methods are different, and the p-values are also different. But hypothesis 1 can be confirmed in these four regression methods, and model 2 is robust. It can be seen from Table 9 that compared with the regression results of model 2 the coefficient of the explanatory variable of model 3 increases, and the significance level weakens. Coupled with the foreshadowing of the regression results of model 1, we can think that the negative effect of the explanatory variable of model 2 becomes weaker. At the same time, the estimated coefficients of intermediary variables are significantly negative, which can prove hypothesis 2. The above analysis shows that the empirical regression method selected in this paper is robust (Table 10).

This part shows the data acquisition methods, data preprocessing, data empirical analysis, and the final robustness test. From collecting the data of each variable in the statistical yearbook to a series of processing the data, the empirical analysis of the two hypotheses in this paper is carried out systematically, and the conclusion shows that hypothesis 1 and hypothesis 2 pass the test. From the specific empirical analysis, we know that first, with the influence of the EPT in 2018, the pollutant emissions of all provinces have decreased on average, and the number of provinces with higher tax rates has decreased more. Second, combined with the regression results of model 3, we found that the implementation of EPT in 2018 affected the increase in technology innovation behavior of organizations, which led to the decline of pollutant emissions. Finally, this part carries out three robustness tests to verify the robustness of the model and the logic of the conclusion.

The triple difference estimator (DDD)

Inspired by Fig. 2, the previous differences-in-differences analysis may impact the estimation due to the difference in the degree of development of provinces. Further, we base the grou** on the average GDP per capita median for 8 years and divide the 30 provinces into developed and underdeveloped provinces, thus conducting a DDD study. The newly generated grou** variable is d3, with d3 = 1, when the sample is from developed provinces, and d3 = 0, when the sample is from underdeveloped provinces. Compared with models 1 through 3 mentioned earlier, 4 through 6 only change the dependent variable to DDD. The model and regression results are shown below:

As seen from the regression results: hypotheses 1 and 2 of the previous section still hold. In addition, the absolute values of the coefficients in this regression result are greater than those of the DID. This indicates that the implementation of this EPT has a more profound impact in developed provinces; i.e., developed provinces will have more financial resources for technological innovation in this policy impact, thus achieving a better emission reduction effect.

Conclusions and policy recommendations

Main conclusions

This paper mainly collects data from various statistical yearbooks to form provincial panel data from 2012 to 2019 and respectively researches the policy effect of EPT as an exogenous event in 2018 and the transmission mechanism of EPT acting through technology innovation as an intermediary variable during this period. Through the treatment of the dataset, the establishment of three econometric models, regression of PSM-DID, and the corresponding robustness test, then using DDD to analyze the policy effects between provinces with different levels of development, the following conclusions are drawn:

-

Firstly, 2018 is the impact time point of the EPT. Under the impact of this exogenous event, the pollutant emissions of all provinces have decreased on average. Through the regression results of model 2, we know that exogenous events play a significantly negative effect in the model, which is that the EPT inhibits the emission of pollutants in provinces, and the stricter tax burden standard does fulfill its responsibility of pollution control. Hypothesis 1 passed the test.

-

Secondly, EPT affects enterprises, as the “Porter hypothesis” says, which leads to the decline of pollutant emissions. Combined with the regression results of the three models, the estimated values of explanatory variable coefficients and intermediary variable coefficients are discussed. Taking the mathematical model as the entry point, this paper gives a strict mechanism analysis process. Technology innovation plays a negative role as an intermediary variable because it decomposes the negative effects brought by exogenous events. Thus, a complete negative transmission mechanism has been formed—the implementation of EPT has led groups in the province to choose technology innovation to reduce emissions to reduce the tax burden, and the reduction of these pollutants’ emissions has led to the reduction of emissions in the whole provincial administrative region. Therefore, hypothesis 2 passed the test.

-

Thirdly, we found that the policy effects were more pronounced in developed provinces, with more significant pollutant reductions relative to less developed provinces.

-

Finally, the methodology for the analysis of the intermediary effect mechanism has not yet appeared as a universal formula, and it is difficult to find all the effect transmission chains. In addition, the research on the intermediary effect has been controversial recently. This paper aims to introduce a relatively reliable research process. In studying the mechanism analysis of the intermediary effect, this paper selects three models to demonstrate the intermediary effect. By comparing three regression results, this paper can get the complete effect transmission chain of the intermediary effect. Other similar methodologies for the study of intermediary effects include the regression between the explanatory variable and intermediary variable and the regression between intermediary variable and explained variable, obtaining two regression results for analysis. Through the rest of the methodology, scholars can also verify the intermediary effect transmission mechanism, learn from each other, and find out the advantages and disadvantages of various methods, which is the spirit of the gradual optimization of methodology. In this paper, we obtain the weight number by PSM and discuss its choice in subsequent regression, which precisely reflects this spirit. Although this paper demonstrates the existence of this effect transmission chain, we do not think that this single transmission chain can describe the entire effect transmission of the EPT. Therefore, this paper is still an exploratory research.

Policy recommendations

Government level

Firstly, we must emphasize the disclosure of policy changes or relevant tax information. For example, when searching the relevant information about whether the tax standard of EPT has changed in subsequent years, we found that the information on the web page is chaotic, and the disclosure is incomplete. On the one hand, this may be the problem of the network information environment; on the other hand, this may also be the problem of incomplete information disclosure. Information asymmetry will seriously increase friction from the perspective of transaction costs in economic activities. For academic research, incomplete information disclosure may lead to some research that cannot be carried out, and even some premise assumptions cannot be verified leading to the research results becoming nonsense. Regarding law enforcement, information asymmetry makes groups in the province spend more costs that could have been used in production when learning policies. The problem of incomplete information disclosure leads to the inefficient productivity of economic life, which cannot be ignored.

Second, some regions should appropriately raise the tax burden standard of EPT. The object of this paper is the causal relationship between the effects of EPT and pollution emissions. Although this paper has demonstrated that the tax burden increase group in the EPT has achieved a better pollution control effect, we still cannot ignore the impact of many aspects of real life on the explained variable. An ideal mathematical model should accommodate all relevant variables and solve many problems, such as collinearity and endogeneity. Specifically, we cannot think that the increase in tax burden will inevitably bring linear changes in the decline of pollutant emissions. Only in this period, compared with the provinces with low tax burden standards, the pollutant emissions of the provinces with high tax burden standards have been suppressed. It is worth mentioning that the time series of the dataset in this paper is only 8 years, the year after the implementation of the policy is only 2 years, and the subsequent years are affected by the public health event of COVID-19. It is a pity that the follow-up role of EPT cannot be observed. In addition, it is difficult for us to determine whether there is a mathematical logic of nonlinear relationships in the model. The suggestions given in this paper are only to appropriately raise the tax burden standard. Appropriately raising the tax burden standard can force technology innovation of groups in the province and then simulate the decline of pollutant emissions, as the “Porter hypothesis” says.

Thirdly, appropriately adjust the preferential measures of EPT for technology innovation groups. By verifying hypothesis 2 in this paper, we have data support for the mechanical transmission chain of EPT. From the empirical analysis, we know that the implementation of EPT in 2018 has led to the behavior of various groups to choose technology innovation, which has affected the reduction of pollutant emissions in the provincial data. Given these, if we adopt loose tax policies for groups with incentives to adopt technology innovation, we should stimulate their enthusiasm for environmental protection to further reduce pollutant emissions. The loose tax policy does not mean simply reducing tax standards but obtaining different tax reduction standards through quantifying green patent applications by various groups under certain quantitative criteria. Quantification and the behavior choice caused by tax reduction are other research directions, so they are not discussed here too much. However, it can be seen that this mechanism research opens a new perspective for policy implementation. The complete transmission chain research from policy implementation to the promotion of group behavior choice is an important way to study the effect of policy implementation.

Group level

Firstly, encourage technology innovation activities of various groups. From the “double dividend effect” in theoretical analysis and the negative effect transmission chain of EPT in empirical analysis, this paper empirically studies the intermediary effect of the EPT transmission chain and the role of technology innovation as an intermediary variable. At this time, as the main body behind the intermediary variable—enterprises, universities, and other groups in the province—it will undoubtedly make the transmission effect better if they have a solid willingness to choose the behavior of technology innovation.

Secondly, consciously abide by the Environmental Protection Law and make information disclosure more adequate. The data in this paper shows that the pollutant emissions of the treatment group in 2018 are less, and the research conclusion is derived that an appropriate tax increase can inhibit pollutant emissions. In deriving the causal effect here, we must pay attention to the main objects impacted by the policy; if these groups abide by the Environmental Protection Law and their information disclosure is adequate, the implementation effect of the policy will undoubtedly be better.

Thirdly, individuals not involved in technology innovation should enhance their environmental protection awareness. When we look up the data obtained from various statistical yearbooks, we find some indicators related to pollutant emissions, such as nitrogen oxide emissions. Among NOx emissions, vehicle emissions are almost the same as industrial motor emissions. When discussing environmental protection, we often cannot ignore the role played by citizens. Environmental pollution caused by citizens’ daily life is another important direction of academic research, and we must strengthen citizens’ awareness of environmental protection. After some academic research, we should find appropriate macro-variables to control, such as the popularization of environmental protection knowledge on the Internet, the publicity of illegal pollution discharge behavior, and the increase of commodity prices of pollution sources, and then carry out in-depth research. As policy recipients, we should also improve our awareness of environmental protection in our daily life, abide by relevant environmental protection laws and regulations, and choose an environment-friendly lifestyle.

Research limitations and prospects

Starting with theoretical and empirical analysis, this paper analyzes the policy effect of EPT in 2018 through a series of data processing and regression analysis using PSM-DID. Due to the limited research level of the author and vision, understanding many aspects of EPT and micro-behavior is not deep enough. Although this paper is a new perspective of EPT research, after reviewing the full text, we put forward the shortcomings of this study and the prospects for future research:

-

Firstly, we hope to see to have research with a longer data period in the future. The EPT was implemented in 2018. The dataset selected in this paper is the panel data from 2012 to 2019, and its time dimension after implementation of EPT is relatively short. In the future, we can get a longer dataset through the update of the statistical yearbook. However, the previously implemented pollution charge policy has a large amount of information on the change of charge and is difficult to collect. Correspondingly, the model should become a multi-point DID or progressive DID model. After solving the above problems, we can conduct empirical analysis in a longer dataset.

-

Secondly, we have the prospect of optimal research. From the perspective of environmental protection, this paper launched a policy evaluation of the EPT in 2018. As for the mathematical model, the research carried out in this paper focuses on the relationship between the implementation effect as a dummy variable policy and the pollutant emissions as the explained variable. The explanatory variable of the model is a dummy variable, which doomed the limitations of the study. It is difficult for us to carry out more interpretations of the impact of tax rates. If scholars want to pursue empirical research on tax rates, scholars should collect tax rates and previous emission fee standards, and even deal with the quantitative relationship between the two. After solving the above problems, scholars can carry out a quantitative analysis of tax rates.

-

Third, we look forward to studying control variables, optimal estimates, and intermediary effects. This paper is one of the few papers that choose provincial panel data for research. Further discussion on the selection of control variables in the mathematical model can be carried out to refine the model. Inferring causality by econometric models mostly infers logical relationships under mathematical models and uses estimated values to approach the real values infinitely. Suppose the mathematical model is wrong, for example. In that case, if there are other same trend impact effects caused by the same policy impact at the same time in this paper, it will be difficult for us to make an optimal estimate. Such rigorous assumptions are very common in the study of econometric models. Although there are limitations in using ideal econometric models to constantly approximate the real problem, this is not a bad thing, which is exactly an additional perspective of reality. As scholars continue to promote the optimization of measurement methodology, the practical significance of measurement models becomes more and more realistic. There are many papers on the analysis of the intermediary effect mechanism. This paper uses a common design framework in AER and JPE, the three-step method of studying the intermediary effect. However, since the explanatory variable of this paper is the dummy variable of policy implementation, the reasonableness of the combination of this methodology with DID remains to be studied. Therefore, this paper believes that the research content is still worthy of attention with the optimization of future methodology.

Data availability

Not applicable.

Notes

The “groups in the province” mentioned many times in this paper have a special concept. When people talk about groups in the province, they often mistakenly think that they only refer to enterprises. However, when looking up the data, we noticed that although enterprises account for a large part of the provincial level data, different groups such as universities and residents still account for a part. Therefore, the “groups in the province” mentioned in this paper refer to multiple groups composed of enterprises, universities, and individuals.

References

Acemoglu D, Akcigit U, Hanley D, Kerr W (2016) Transition to clean technology. J Polit Econ 124(1):52–104

Aghion P, Dechezleprêtre A, Hemous D, Martin R, Van Reenen J (2016) Carbon taxes, path dependency, and directed technical change: evidence from the auto industry. J Polit Econ 124(1):1–51

Albrizio S, Kozluk T, Zipperer V (2017) Environmental policies and productivity growth: evidence across industries and firms. J Environ Econ Manag 81:209–226. https://doi.org/10.1016/j.jeem.2016.06.002

Borozan D (2019) Unveiling the heterogeneous effect of energy taxes and income on residential energy consumption. Energy Policy 129:13–22

Cheng Y, Sinha A, Ghosh V, Sengupta T, Luo H (2021) Carbon tax and energy innovation at crossroads of carbon neutrality: designing a sustainable decarbonization policy. J Environ Manage 294:112957

Chien F, Ananzeh M, Mirza F, Bakar A, Vu HM, Ngo TQ (2021) The effects of green growth, environmental-related tax, and eco-innovation towards carbon neutrality target in the US economy. J Environ Manage 299:113633

Dechezleprêtre A, Sato M (2017) The impacts of environmental regulations on competitiveness. Rev Environ Econ Policy 11(2):183–206. https://doi.org/10.1093/reep/rex013

Delgado FJ, Freire-González J, Presno MJ (2022) Environmental taxation in the European Union: are there common trends? Econ Anal Policy 73:670–682. https://doi.org/10.1016/j.eap.2021.12.019

Guo F (2021) Impact of environmental protection tax on environmental cost of a steel enterprise. Hunan University of Technology. https://doi.org/10.27730/d.cnki.ghngy.2021.000397

Harrison K (2010) The comparative politics of carbon taxation. Annu Rev Law Soc Sci 6:507–529

Karmaker SC, Hosan S, Chapman AJ, Saha BB (2021) The role of environmental taxes on technological innovation. Energy 232:121052

Karydas C, Zhang L (2019) Green tax reform, endogenous innovation and the growth dividend. J Environ Econ Manag 97:158–181

Kemp R, Pontoglio S (2011) The innovation effects of environmental policy instruments—a typical case of the blind men and the elephant? Ecol Econ 72:28–36

Li Z, Feng X (2021) Does internet use improve individual participation in environmental protection? J Environ Econ 6(02):100–119. https://doi.org/10.19511/j.cnki.jee.2021.02.007

Li Q, Liu Y, Liu B (2021) Quantitative analysis of new energy industry policy and its environmental protection effect. Journal of Bei**g Institute of Technology (Social Science Edition) 23(04):30–39. https://doi.org/10.15918/j.jbitss1009-3370.2021.4301

Lin B, Li X (2011) The effect of carbon tax on per capita CO2 emissions. Energy Policy 39(9):5137–5146

Liu X, Shao R (2021) Environmental protection tax, technological innovation and corporate financial performance ——a study based on the difference-in-differences method. Indust Technol Econ 40(9):24–30. https://doi.org/10.3969/j.issn.1004-910X.2021.09.003

Liu Y, Zhang X (2018) Emission reduction effects of environmental tax system and its regional differences in China. Tax Res 2018(02):41–47. https://doi.org/10.19376/j.cnki.cn11-1011/f.2018.02.008

Long F, Ge C, Lin F, Lian C, Bi F, Hu T (2021) Atmospheric environment management in China: progress and outlook. Chin J Environ Manag 13(05):127–134+60. https://doi.org/10.16868/j.cnki.1674-6252.2021.05.127

Lu H, Liu Q, Xu X, Yang N (2019) Can environmental protection tax achieve “reducing pollution” and “economic growth”? Based on the change perspective of China’s sewage charges. China Popul Resour Environ 29(06):130–137

Nicola P, Andrew P, Dan S (2004) The effect of adolescent experience on labor market outcomes: the case of height. J Polit Econ 112(5):1019–1053. https://doi.org/10.2139/ssrn.293122

Pearce D (1991) The role of carbon taxes in adjusting to global warming. Econ J 101(407):938–948

Safi A, Chen Y, Wahab S, Zheng L, Rjoub H (2021) Does environmental taxes achieve the carbon neutrality target of G7 economies? Evaluating the importance of environmental R&D. J Environ Manage 293:112908

Shahzad U (2020) Environmental taxes, energy consumption, and environmental quality: theoretical survey with policy implications. Environ Sci Pollut Res 27(20):24848–24862

Sumner J, Bird L, Dobos H (2011) Carbon taxes: a review of experience and policy design considerations. Clim Pol 11(2):922–943

Sun Y, Yuan Z (2020) Will the environmental taxation promote enterprise upgrading? Based on the mesomeric effect of innovation investment. Tax Res 2020(04):95–102. https://doi.org/10.19376/j.cnki.cn11-1011/f.2020.04.015

Wang P, Yang S, Huang S (2021) Research on the impact of environmental protection tax on enterprise environmental, social and governance performance – based on the intermediary effect of green technology innovation. Tax Res 2021(11):50–56. https://doi.org/10.19376/j.cnki.cn11-1011/f.2021.11.010

Wolde-Rufael Y, Mulat-Weldemeskel E (2021) Do environmental taxes and environmental stringency policies reduce CO 2 emissions? Evidence from 7 emerging economies. Environ Sci Pollut Res 28:22392–22408

** P, Liang R, **e Z (2017) Tax sharing adjustments, fiscal pressure and industrial pollution. J World Econ 40(10):170–192

Yu L, Zhang W, Bi Q (2019) Can environmental taxes force corporate green innovation? Audit Econ Res 34(2):79–90. https://doi.org/10.3969/j.issn.1004-4833.2019.02.008

Author information

Authors and Affiliations

Contributions

All authors contributed to the study conception and design. Material preparation and data collection and analysis were performed by Yufan Lin, ChenXu Yu, and Qisi Yang. The first draft of the manuscript was written by Yufan Lin and Lingxin Liao; all authors commented on previous versions of the manuscript. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Ethical approval

This study did not require local ethics committee approval.

Consent to participate

Not applicable.

Consent for publication

Not applicable.

Competing interests

The authors declare no competing interests.

Additional information

Responsible Editor: Nicholas Apergis

Publisher's note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Lin, Y., Liao, L., Yu, C. et al. Re-examining the governance effect of China’s environmental protection tax. Environ Sci Pollut Res 30, 62325–62340 (2023). https://doi.org/10.1007/s11356-023-26483-7

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-023-26483-7