Abstract

Since markets are undergoing severe turbulent economic periods, this study investigates the information transmission of energy stock markets of five regions including North America, South America, Europe, Asia, and Pacific where we differentiated the regional energy markets based on their develo** and developed state of economy. We employed time–frequency domain from Jan 1995 to May 2021 and found that energy stocks of developed regions are highly connected. The energy markets of North America, South America, and Europe are the net transmitters of spillovers, whereas the Asian and Pacific energy markets are the net receivers of spillovers. The results also reveal that the connectedness of regional energy markets is time and frequency dependent. Regional energy stocks were highly connected following the Asian financial crisis (AFC), global financial crisis (GFC), European debt crisis (EDC), shale oil revolution (SOR), and COVID-19 pandemic. Time-dependent results reveal that high spillovers formed during stress periods and frequency domain show the higher connectedness of regional energy stock markets in the short run followed by an extreme economic condition. These results have significant implications for policymakers, regulators, investors, and regional controlling bodies to adopt effective strategies during short run to avoid economic downturns and information distortions.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Measuring and monitoring the information transmission and interdependence between the major financial markets is a major concern among the academic research researchers, policymakers, government institutions, investors, and business practitioners (Shen et al. 2018). It is critical to understand the information transmission mechanism in the regional energy stock market as it helps the investors, hedge funds, and insurance companies in making investment and hedging decisions (Hasan et al. 2021; Naeem et al. 2021a, b; Dagar et al. 2021). Given the globalized nature of the world economy and rapid development of the commodity market, understanding the information transmission mechanism in the energy market is not only extremely important to improve the portfolio selection and allocation strategies but also extremely helpful in devising best policy response for maintaining financial stability (Karim et al. 2020a, b) and avoiding any possible financial contagion. Against such a backdrop, we examine the information transmission between the regional energy stock markets by using the time–frequency domain provided by Diebold and Yilmaz (2012) and Baruník and Křehlík (2018).

The energy markets across the globe are interconnected as the shocks in the oil market substantially increase the risk in the natural gas and other energy markets (Shen et al. 2018). The regional, geographical, and political differences make it worthwhile to study the regional connectedness of the energy market (Hasan et al. 2021). Many studies have investigated the volatility spillover between the energy, stock, bond, cryptocurrency, crude oil, and commodity market including the interdependence structure between these markets (Akram et al. 2020; Ferrer et al. 2018; Naeem et al. 2020; Tiwari et al. 2020). For example, it is believed that the energy transmission across the adjacent countries is faster than the non-adjacent countries and it is expected that the energy connectedness in the regional electricity markets is higher in the closer vicinities. Similar findings are obtained by Bunn and Gianfreda (2010), de Menezes and Houllier (2015), and ** regions are receiving spillovers. Hence, we compared the economic orientation of these regions and provided unique insights. Fifth, our sub-sample analysis provided robust results with full sample period indicating higher connectedness during the periods of financial distress. Finally, we framed various implications for policymakers, regulation bodies, investors, and portfolio managers.

The findings of the study reveal that North American (NAMR) and South American (SAMR) energy stock markets are the net transmitters of information spillovers. Europe (EURO) transmitted moderate spillovers whereas Asia (ASIA) and Pacific (PACF) are the net recipients of information spillovers. Moreover, the connectedness of energy markets was high during stress periods where global economic fragility, uncertainty, and world-wide closure of business operations resulted in the formation of higher spillovers. The frequency dependent analysis showed that regional energy markets showed significant spikes in the short run whereas connectedness becomes lower in the long run. Followed by the uncertainties in the global working conditions and economic distress, the energy markets of five regions showed varying patterns of connectedness. Additionally, the sub-sample analysis also confirmed that NAMR is the net transmitter of information spillovers followed by SAMR and EURO. And, ASIA and PACF are the net recipients of the information spillovers.

The remaining study proceeds as follows. In the next section, we provide the review of relevant literature related to the regional connectedness of energy markets. In “Methodology,” we provide the methodology used for the study and “Empirical results” presents the empirical analysis and findings of the study. Finally, in “Conclusion,” we conclude with several policy and regulatory implications.

Literature review

The relationship and interconnectedness among the regional energy markets have been investigated and analyzed from different perspectives. Hasan et al. (2021) examined the time–frequency connectedness between the Asian electricity markets by using the Baruník and Křehlík (2018) and Diebold and Yilmaz (2012). Macroeconomic factors of the energy market such as geographical location, supply, and demand play an important role in information transmission and the connectedness of the regional energy markets (Singh et al. 2019; Muhammad and Khan 2021; Karim and Naeem 2021). Despite the economic and political differences between the countries in Asian region, a great potential for the connectedness of energy sector in the Asian region exists (Oseni and Pollitt 2016). Several efforts have been made to connect the energy sector in the Asia region in the last couple of decades and some advancements have also been made in this regard (Bhattacharyay 2010). Under the CAREC program strategy, the TAPI gas pipeline project was approved to help and improve the regional energy trade between the TAPI countries (Turkmenistan, Afghanistan, Pakistan, and India). The expansion of central Asian power system is intended to enhance the regional energy trade and connectedness of new energy markets such as Afghanistan and Turkmenistan with the central Asian markets (Zobaa and Lee 2006). These connectivity initiatives highlight towards the fact that, although the regional trade practices among the Asian nations have been low, the right steps are being undertaken to strengthen the regional energy connectedness among the Asian nations (Hasan et al. 2021).

Many scholars have focussed on the network connectedness of the energy market in Europe (Geng et al. 2021; **ao et al. 2019). The energy market has become increasingly integrated in Europe due to the market coupling and interconnection capacity and further integration plan is expected in the early 2020s (Lockwood et al. 2017). The UK’s exit strategy from European Union will have a long-term impact on the energy market integration and information transmission in the European region (Lockwood et al. 2017; Lowe 2017; Karim et al. 2021a, b). Lin and Li (2015) applied VAC-MGARCH approach to study the spillover effects across natural gas and concluded that oil and natural gas markets are co-integrated across the European market within the first and second moments. The information transmission is expected to have multiple possible impact on the energy integration including the availability and cost of finance, energy market and security of supply, nuclear power, and supply chain of all energy markets across Europe and energy efficiency policy (Egan 2019; Mayer et al. 2019).

The rest of the studies are summarized in Appendix 1 (Table 3).

Methodology

Connectedness of the regional energy markets in the time–frequency domain

Following the methodology proposed by Diebold and Yilmaz (2012, 2014), this study employed the time-based connectedness using the static VAR model of p order, as indicated in Eq. (1)

The vector \(y_t=(R_{1t},\ldots ,R_{nt})\) is an \(n\times 1\) vector that contains the net connectedness or partial connectedness of Australian electricity markets and \(\Phi (L)\) shows lagged variable. ɛt shows random error term where the mean value is zero and the matrix variance is\(\sum\); we also observed no problem of serial correlation with ɛt. As indicated above, the VAR model offers static estimations in the time domain, Eq. (1) can be re-written given the infinite order of moving average process, for instance, VMA(∞), say\({\mathrm y}_{\mathrm t}=\psi(\mathrm L){\varepsilon}_{\mathrm t}+{\psi}_0{\varepsilon}_{\mathrm t}+{\psi}_1{\varepsilon}_{\mathrm t-1}+\ldots +{\psi}_{\mathrm h}{\varepsilon}_{\mathrm t-\mathrm h}+\ldots\). Here,\({\psi}_h\) denotes moving average coefficient analogous to the h-th lag time. When h-th lag time is zero, the \({\psi}_0\) is adjusted to \(\mathrm{I}\) which is the identity matrix.

Time-dependent connectedness

Following Pesaran and Shin (1998) for estimating time-based connectedness, a generalized forecast error variance decomposition (FEVD) to the static VMA(∞) was developed as indicated in Eq. (1). By employing the H-step ahead analysis, the contribution of realized daily returns of the j-th to the estimated error variance of the realized returns of the i-th variable is as follows:

where the ij-th item of \(\Sigma\) is denoted as \({\sigma }_{ij}\), and the diagonal item of j-th is represented as \({\sigma }_{jj}\); and \({\mathrm{e}}_{j}\) denotes zeros conditioned that the j-th item is one. For the analysis carried out for estimating the connectedness of regional energy markets, a forecast horizon (H) of 100 days was chosen and we equally standardized the contribution across all variables in terms of \((j=1,2,\ldots ,n)\), in this way, following the Diebold and Yilmaz (2012, 2014) approach, the connectedness of regional energy markets can be computed.

Frequency-dependent connectedness

Following the Eq. (1) VMA p-order model, we initiated the estimation process to obtain frequency-dependent connectedness. After getting the VMA (∞) illustration, for instance,\({\mathbf y}_t=\boldsymbol{\psi}(L)\varepsilon_t\), the Fourier transform on the lagged coefficient element, was applied and \(\boldsymbol{\psi}\left(\mathrm e^{-\mathrm i\omega}\right)=\sum\nolimits_{h=0}^\infty\mathrm e^{-\mathrm i\omega h}{\boldsymbol{\psi}}_h\) was obtained where \(\omega\) denotes particular frequency. Afterward, we took power spectrum of \(y_t\) as \(S_y\left(\omega\right)=\sum\nolimits_{h=-\infty}^\infty E\left[{\mathrm y}_t{\mathrm y}_{t-h}\right]\mathrm e^{-\mathrm i\omega h}=\psi\left(\mathrm e^{-\mathrm i\omega}\right)\sum\psi\left(\mathrm e^{\mathrm i\omega}\right)\). The j-th variable contribution (i.e., the connectedness of the j-th element) to the forecast error variance of the i-th variable (i.e., the connectedness of the i-th element) is as follows:

Time-dependent connectedness vs. frequency-dependent connectedness

Table 1 provides the definitions of several time-dependent connectedness measures based on Diebold and Yilmaz (2012, 2014). Moreover, the table also provides definitions of frequency-dependent connectedness given by Baruník and Křehlík (2018). It can be observed that the variation in the two measures (time and frequency) only comes from the variable j related to i, i.e., the forecast error variance variable.

Following the studies of Balli et al. (2019), Naeem et al. (2020), Caporin et al. (2021), and Shahzad et al. (2021), our study also used both time and frequency domains. The use of time–frequency domains simultaneously offers two benefits. First, the directional spillovers are obtained, exhibited by a network diagram. Second, the short- and long-run components can be segregated following the frequency domain.

Empirical results

Data and preliminary analysis

This study endeavors to investigate the information transmission among five regional energy markets by employing the methodology of Diebold and Yilmaz (2012) and Barunik and Krehlik (2018) for the period encompassing January 2, 1995, to May 27, 2021. For analysis purpose, we have taken the data of regional energy sectors: Asian energy sector (ASIA), European energy sector (EURO), North American energy sector (NAMR), Pacific energy sector (PACF), and South American energy sector (SAMR). The data have been sourced from DataStream of the relevant energy sectors. Table 2 illustrates the descriptive statistics of markets under study where highest average values are reflected by SAMR, PACF, and NAMR followed by EURO. ASIA yield the least average returns for the complete sample period. The highest variability of average returns is indicated by SAMR followed by NAMR while EURO and PACF depicted comparable exposure to risk. Finally, ASIA exhibited lowest variability in the average returns among the rest of the regional energy sectors. The Jarque–Bera test of normality indicates that values are substantially higher and there is abnormality in the average returns.

Network connectedness of regional energy markets

This study attempts to investigate the information transmission of five regional energy markets, namely, North American region (NAMR), South American region (SAMR), European region (EURO), Asian region, (ASIA), and Pacific region (PACF). The information transmission has been estimated through time and frequency dependence structure provided by Diebold-Yilmaz (2012) and Barunik-Krehlik (2018) approaches respectively. Figure 1 presents the network connectedness of five regions based on Diebold-Yilmaz (2012) method, where two distinct clusters are formed. The first cluster reveals connectedness between NAMR, SAMR, and EURO regions where markets are highly connected with each other and transmit spillovers to other markets. We argue that NAMR, SAMR, and EURO are developed regions and due to strong economic and financial stability, these regions are transmitting spillovers to develo** regions. Accordingly, PACF and ASIA form the other cluster and are highly connected with each other. The network diagram displays NAMR and SAMR which are the net transmitters of spillovers whereas ASIA and PACF are the net recipients of spillovers. The connectedness among the regional energy markets is evident for the regions which are adjacently located with each other. The geographical proximity of these markets makes the information transmission feasible and easily accessible resulting in the higher connectedness of the energy regions. The findings are in line with the arguments of Han et al. (2020), Manner et al. (2019), and Yan and Truck (2020) who also reported similar findings claiming higher connectedness of markets of closer vicinities. Meanwhile, we also segregate the regions of energy stock markets based on their developed and develo** economic stature.

Figure 2 illustrates the connectedness of regional energy markets in the short and long run following Barunik-Krehlik (2018) approach. Figure 2a presents the spillovers of information transmission in the short run which reiterate the formation of two main clusters. The information spillovers are higher among NAMR, SAMR, and EURO in the short run. And, these regions show higher connectedness in the short run and are net transmitters of information spillovers. On the other hand, PACF and ASIA regions form second cluster of connectedness and are the net recipients of information spillovers. Meanwhile, the short-run analysis points to the crisis periods where majority of the regional markets are highly connected following the uncertain economic downfall and disruptions in the information transmission. For this reason, our findings corroborate Balli et al. (2019) who argue that various commodities, like energy commodities, form high spillovers in the short run following a particular crisis.

Network connectedness using Barunik and Krehlik (2018). a Short run (1–5 days). b Long run (> 5 days). This figure indicates the full sample connectedness among regional energy markets using Barunik and Krehlik (2018) with 100 days ahead forecast error variance and lag 1 using SIC criteria

Correspondingly, Fig. 2b presents the connectedness of regional energy markets in the long run which illustrates that NAMR and SAMR are transmitting spillovers to other energy regions. EURO region is transmitting moderate spillovers to PACF and ASIA regions. Meanwhile, PACF and ASIA are the net recipients of information spillovers in the long run. The nodes on the regional energy markets (highlighted with red) determine the net transmitting and net receiving capacity of spillovers. In this way, it is suggested that the regional energy markets which are sharing their geographies are highly connected to each other whereas the energy markets which are located at distant places tend to show disconnection with other energy regions. The other significant takeaway of the analysis reveals that the energy regions of developed economies are highly connected with each other and transmit information spillovers to the energy regions of develo** economies. Thus, regional energy markets of developed economies are net transmitters of spillovers whereas energy markets of develo** economies are net recipients of spillovers.

Time-varying connectedness of regional energy markets

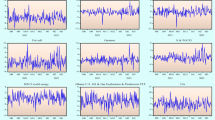

Figure 3 presents the time-varying connectedness of regional energy markets based on Diebold-Yilmaz (2012) and Barunik-Krehlik (2018) models. The time-varying connectedness of regional energy markets suggests that connectedness among the markets is time-varying and patterns of spillovers vary based on different time periods. Figure 3a presents the time-varying connectedness based on DY[12] model with significant spikes and troughs highlighting various time-periods of economic uncertainty and stress. The first spike is observed during Asian financial crisis (1997–1998) where regional energy markets showed higher connectedness as the crisis period resulted in information asymmetry and several markets shared information to overcome the drastic impact of the crisis. Hence, the graph depicts high spillovers during Asian financial crisis period. Soon after the crisis, markets tend to normalize and regained their normal working conditions illustrating the decline in the connectedness of the markets in the graph. Regional energy markets revealed spikes during global financial crisis (GFC) for the period 2007–2008 where high spillovers were formed among the markets. Reiterating, the energy markets of five regions were highly connected during the period of economic fragility. Concurrently, markets revealed high spillovers during 2010–2012 indicating the European debt crisis (EDC) where markets were significantly influenced by the anti-inflation policy from the European Central Bank (Blundell-Wignall 2012). Similarly, a spike during 2014–2016 points to the shale oil crisis where US oil markets suffered crisis during the shale oil revolution (SOR). The higher connectedness among regional energy markets revealed that asymmetrical information patterns and crisis led the markets to form high spillovers. Correspondingly, the spike during 2019–2020 highlights the current COVID-19 pandemic which significantly influenced the economic status around the globe. The higher connectedness of regional energy markets shows that spillovers were high during the crisis period and economic stress. Our findings are in line with Greenwood-Nimmo et al. (2016) and Sehgal et al. (2017) arguing that spillovers get intense during the period of economic severity and when markets are stabilized, the connectedness becomes lower.

Time-varying connectedness. a Diebold and Yilmaz (2012). b Barunik and Krehlik (2018). This figure indicates the time-varying connectedness using a rolling window (260 days) among regional energy markets. Panel a indicates Diebold and Yilmaz (2012) and Panel b indicates Barunik and Krehlik (2018) with 100 days ahead forecast error variance and lag 1 using SIC criteria

Figure 3b reveals frequency dependent connectedness of regional energy markets following the model of Barunik-Krehlik (2018) where short run is highlighted with orange and long run is presented by yellow. Similar to Fig. 3a, the graph shows substantial spikes and troughs. The initial spike in the short-run points towards Asian financial crisis (1997–1998) where energy markets of five regions showed higher connectedness followed by a market-wide contagion. As the aftermaths of the shock disappeared, markets started to stabilize and connectedness becomes lower. The spike during 2006–2008 shows higher spillovers during global financial crisis where majority of the financial markets collapsed. Soon after GFC, markets showed higher connectedness during 2010–2012 pointing to the European debt crisis (EDC) where markets formed high spillovers revealing economic uncertainty and fragility. Correspondingly, the shale oil crisis during 2014–2016 depicted a spike in the graph where energy markets are significantly impacted by the shale oil revolution. The final spike in the graph highlights the ongoing pandemic condition generated due to COVID-19 signifying higher connectedness of regional energy markets where emergency situation of global lockdowns and closure of business operations has formed high spillovers of energy markets. The spikes in the short run mainly reveal that frequency connectedness of regional energy markets is affected in the short run and lasts for a shorter period of time (Londono 2019). Conversely, the connectedness of regional energy markets in the long run suggests that markets remain disconnected in the long run as it highlights normal market and economic conditions (Bouri et al. 2020).

Sub-sample analyses

Figure 4 illustrates sub-sample analysis of regional energy markets using Diebold-Yilmaz (2012) approach for three crisis periods, namely, global financial crisis (GFC), shale oil revolution (SOR), and COVID-19 crisis (COV). The connectedness among the regional energy markets shows similar patterns in all of the crisis periods where NAMR, SAMR, and EURO are net transmitters of the spillovers and show higher connectedness whereas ASIA and PACF are the net recipients of the information spillovers and show lower connectedness with other energy markets. Our findings recall the arguments of Hasan et al. (2021) on connectedness among Asian electricity markets, who reported that the connectedness of energy markets becomes high during a crisis period. Moreover, the regional markets of developed economies are net transmitters and vice versa.

Sub-sample analysis using Diebold and Yilmaz (2012). a Global financial crisis (GFC). b Shale oil revolution (SOR). c COVID-19 crisis (COV). These figures indicates the sub-sample connectedness among regional energy markets using Diebold and Yilmaz (2012) with 100 days ahead forecast error variance and lag 1 using SIC criteria

Figure 5 illustrates sub-sample analysis using Barunik-Krehlik (2018) approach for three crises periods in the short run. Figure 5a, b, and c show that regional energy markets formed moderate spillovers and there is moderate connectedness among the regional energy markets. However, NAMR, SAMR, and EURO are marked as the net transmitters of information spillovers whereas ASIA and PACF are the net recipients of spillovers. Given the short-run period, the regional energy markets of closer borders tend to show higher connectedness during the crisis periods. In line with various studies of connectedness (Naeem et al. 2021a, b; Karim and Naeem 2021; Karim et al. 2022a, b, c), we report that spillovers are fashioned based on the development of the regional economic and financial power. Thus, markets are connected when there are distressed times and are weakly connected during stable times.

Sub-sample analysis using Barunik and Krehlik (2018) — Short-run. a Global financial crisis (GFC). b Shale oil revolution (SOR). c COVID-19 crisis (COV). These figures indicates the short-run sub-sample connectedness among regional energy markets using Barunik and Krehlik (2018) with 100 days ahead forecast error variance and lag 1 using SIC criteria

Figure 6 gives the analysis of sub-sample using Barunik-Krehlik (2018) model in the long run for three significant crises periods, i.e., GFC, SOR, and COV. For the results in each sub-sample, Fig. 6a, b, and c reveal higher connectedness of regional energy markets where NAMR is the net transmitter of spillovers followed by SAMR and EURO. Contrarily, ASIA and PACF are the net recipients of spillovers in the long run for each sub-sample. Our findings recall the studies of Naeem et al. (2021b), Elsayed et al. (2020), Le et al. (2021), and Salisu and Vo (2020), and it is asserted that the crisis period, driven by the market sentiment of fear, spreads across the globe that resulted in higher spillovers among the energy markets.

Sub-sample analysis using Barunik and Krehlik (2018) — Long-run. a Global financial crisis (GFC). b Shale oil revolution (SOR). c COVID-19 crisis (COV). These figures indicates the long-run sub-sample connectedness among regional energy markets using Barunik and Krehlik (2018) with 100 days ahead forecast error variance and lag 1 using SIC criteria

Overall, our findings illustrate that information transmission among the regional energy markets showed spillovers differentiated into developed regions’ energy markets and develo** regions. Notably, the connectedness among the markets was higher during the periods of economic stress and fragility followed by uncertain global financial condition and unstable business operations.

Conclusion

This research presented the information transmission of regional energy markets using the Diebold and Yilmaz (2012) and Barunik and Krehlik (2018) models of time-and-frequency-dependent structures. The time-based connectedness of five regional energy markets showed NAMR and SAMR as the net transmitters of information spillovers. EURO transmitted moderate spillovers whereas ASIA and PACF are the net recipients of information spillovers. We segregated the spillovers based on the financial and economic strength of five regions. We documented that developed regions (NAMR, SAMR, and EURO) are transmitting spillovers while develo** regions (ASIA and PACF) are receiving spillovers. Moreover, the connectedness of energy markets was high during stress periods where global economic fragility, uncertainty, and world-wide closure of business operations resulted in the formation of higher spillovers. The frequency-dependent analysis showed that regional energy markets experienced significant spikes in the short run whereas connectedness becomes lower in the long run. Followed by the uncertainties in the global working conditions and economic distress, the energy markets of five regions showed varying patterns of connectedness. Additionally, the sub-sample analysis also confirmed that NAMR is the net transmitter of information spillovers followed by SAMR and EURO. And, ASIA and PACF are the net recipients of the information spillovers.

Our findings draw significant implications for policymakers, investors, financial institutions, financial markets, regulatory bodies, and global market players. Policymakers can evaluate their policies and reformulate certain strategies to avoid the drastic effects of crises coming in their way of progress and development. Meanwhile, policymakers of each region can redevelop their policies pertaining to energy stock markets and encourage their affiliates to invest in the stocks of energy companies as they are reportedly performing well than the develo** regions. Investors can assess their risk portfolios by adding a blend of commodities and financial instruments to diversify their risks in the face of economic downfall. Moreover, for investors, we recommend investing in the energy stocks of develo** regions as they are diversifiers among developed energy stock markets. Hence, drawing useful strategies from the study can help the investors to mitigate their risk during turbulent time periods. Regulatory bodies can redevelop their strategies to provide sufficient safety to the investments of the investors particularly during crisis times. In this way, crisis periods provide substantial insights for financial markets to consider those financial instruments and commodities which provide shelter to their mainstream investments. As future research avenues, the study recommends to include various other regions and their energy stock markets to provide a comprehensive analysis on portfolio diversification and risk assessment. Following this, our study is of particular importance to upcoming researchers, practitioners, and decision-makers to relish the findings of the study in a meaningful way.

Data availability

The data and material for this study are made available upon request from the corresponding author.

References

Akram R, Majeed MT, Fareed Z, Khalid F, Ye C (2020) Asymmetric effects of energy efficiency and renewable energy on carbon emissions of BRICS economies: evidence from nonlinear panel autoregressive distributed lag model. Environ Sci Pollut Res :1–15

Apergis N, Gozgor G, Lau CKM, Wang S (2020) Dependence structure in the Australian electricity markets: new evidence from regular vine copulae. Energy Econ 90:104834. https://doi.org/10.1016/j.eneco.2020.104834

Balli F, Naeem MA, Shahzad SJH, de Bruin A (2019) Spillover network of commodity uncertainties. Energy Econ 81:914–927

Baruník J, Křehlík T (2018) Measuring the frequency dynamics of financial connectedness and systemic risk. J Financ Econ 16(2):271–296

Bhattacharyay BN (2010) Infrastructure for ASEAN connectivity and integration. ASEAN Econ Bull 27(2):200–220

Blundell-Wignall A (2012) Solving the financial and sovereign debt crisis in Europe. OECD J Financ Mark Trends 2011(2):1–23

Bouri E, Lucey B, Saeed T, Vo XV (2020) Extreme spillovers across Asian-Pacific currencies: a quantile-based analysis. Int Rev Financ Anal 72:101605

Bunn DW, Gianfreda A (2010) Integration and shock transmissions across European electricity forward markets. Energy Economics 32(2):278–291

Caporin M, Naeem MA, Arif M, Hasan M, Vo XV, Shahzad SJH (2021) Asymmetric and time-frequency spillovers among commodities using high-frequency data. Resour Policy 70:101958

Cui J, Goh M, Li B, Zou H (2021) Dynamic dependence and risk connectedness among oil and stock markets: new evidence from time-frequency domain perspectives. Energy 216:119302

Dagar V, Khan MK, Alvarado R, Rehman A, Irfan M, Adekoya OB, Fahad S (2021) Impact of renewable energy consumption, financial development and natural resources on environmental degradation in OECD countries with dynamic panel data. Environ Sci Pollut Res :1–11

de Menezes LM, Houllier MA (2015) Germany’s nuclear power plant closures and the integration of electricity markets in Europe. Energy Policy 85:357–368

Diebold FX, Yilmaz K (2012) Better to give than to receive: predictive directional measurement of volatility spillovers. Int J Forecast 28(1):57–66

Diebold FX, Yılmaz K (2014) On the network topology of variance decompositions: measuring the connectedness of financial firms. J Econ 182(1):119–134

Egan M (2019) EU single market (s) after Brexit. Polit Gov 7(3):19–29

Elsayed AH, Nasreen S, Tiwari AK (2020) Time-varying co-movements between energy market and global financial markets: implication for portfolio diversification and hedging strategies. Energy Econ 90:104847

Ferrer R, Shahzad SJH, López R, Jareño F (2018) Time and frequency dynamics of connectedness between renewable energy stocks and crude oil prices. Energy Econ 76:1–20

Ferrer R, Shahzad SJH, Soriano P (2021) Are green bonds a different asset class? Evidence from time-frequency connectedness analysis. J Clean Prod 292:125988

Geng J-B, Chen F-R, Ji Q, Liu B-Y (2021) Network connectedness between natural gas markets, uncertainty and stock markets. Energy Econ 95:105001

Greenwood-Nimmo M, Nguyen VH, Rafferty B (2016) Risk and return spillovers among the G10 currencies. J Financ Mark. https://doi.org/10.1016/j.finmar.2016.05.001

Han L, Kordzakhia N, Trück S (2020) Volatility spillovers in Australian electricity markets. Energy Econ 90. https://doi.org/10.1016/j.eneco.2020.104782

Hasan M, Arif M, Naeem MA, Ngo QT, Taghizadeh-Hesary F (2021) Time-frequency connectedness between Asian electricity sectors. Econ Anal Policy 69:208–224. https://doi.org/10.1016/j.eap.2020.12.008

Islam MM, Khan MK, Tareque M, Jehan N, Dagar V (2021) Impact of globalization, foreign direct investment, and energy consumption on CO 2 emissions in Bangladesh: does institutional quality matter? Environ Sci Poll Res :1–21

Karim S, Naeem MA (2021) Clean energy, Australian electricity markets, and information transmission. Energy Res Lett 3(Early View):29973

Karim S, Manab NA, Ismail RB (2020a) The dynamic impact of board composition on CSR practices and their mutual effect on organizational returns. J Asia Bus Stud

Karim S, Manab NA, Ismail RB (2020b) Assessing the governance mechanisms, corporate social responsibility and performance: the moderating effect of board independence. Glob Bus Rev :0972150920917773

Karim S, Naeem MA, Meero AA, Rabbani MR (2021a) Examining the role of gender diversity on ownership structure-sustainable performance nexus: fresh evidence from emerging markets. Environ Sci Pollut Res :1–16

Karim S, Akhtar MU, Tashfeen R, Raza Rabbani M, Rahman AAA, AlAbbas A (2021b) Sustainable banking regulations pre and during coronavirus outbreak: the moderating role of financial stability. Econ Res-Ekon Istraživanja :1–18

Karim S, Lucey BM, Naeem MA, Uddin GS (2022a) Examining the interrelatedness of NFTs, DeFi Tokens and Cryptocurrencies. Financ Res Lett:102696

Karim S, Khan S, Mirza N, Alawi SM, Taghizadeh-Hesary F (2022b) Climate finance in the wake of COVID-19: connectedness of clean energy with conventional energy and regional stock markets. Clim Change Econ. https://doi.org/10.1142/S2010007822400085

Karim S, Naeem MA, Mirza N, Paule-Vianez J (2022c) Quantifying the hedge and safe-haven properties of bond markets for cryptocurrency indices. J Risk Finance. https://doi.org/10.1108/JRF-09-2021-0158

Kang SH, Tiwari AK, Albulescu CT, Yoon S-M (2019) Exploring the time-frequency connectedness and network among crude oil and agriculture commodities V1. Energy Econ 84:104543

Kang S, Hernandez JA, Sadorsky P, McIver R (2021) Frequency spillovers, connectedness, and the hedging effectiveness of oil and gold for US sector ETFs. Energy Econ 99:105278

Khan MK, Babar SF, Oryani B, Dagar V, Rehman A, Zakari A, Khan MO (2021) Role of financial development, environmental-related technologies, research and development, energy intensity, natural resource depletion, and temperature in sustainable environment in Canada. Environ Sci Pollut Res :1–17

Le TH, Do HX, Nguyen DK, Sensoy A (2021) COVID-19 pandemic and tail-dependency networks of financial assets. Financ Res Lett 38:101800

Lin B, Li J (2015) The spillover effects across natural gas and oil markets: based on the VEC–MGARCH framework. Appl Energy 155:229–241

Liu N, Liu C, Da B, Zhang T, Guan F (2021) Dependence and risk spillovers between green bonds and clean energy markets. J Clean Prod 279:123595

Lockwood M, Froggatt A, Wright G, Dutton J (2017) The implications of Brexit for the electricity sector in Great Britain: trade-offs between market integration and policy influence. Energy Policy 110(August):137–143. https://doi.org/10.1016/j.enpol.2017.08.021

Londono JM (2019) Bad bad contagion. J Bank Financ 108:105652

Lowe P (2017) Brexit and energy: time to make some hard choices. EEJ 7:38

Manner H, Fard FA, Pourkhanali A, Tafakori L (2019) Forecasting the joint distribution of Australian electricity prices using dynamic vine copulae. Energy Econ 78:143–164

Mayer P, Ball CS, Vögele S, Kuckshinrichs W, Rübbelke D (2019) Analyzing brexit: implications for the electricity system of Great Britain. Energies 12(17):3212

Muhammad B, Khan MK (2021) Foreign direct investment inflow, economic growth, energy consumption, globalization, and carbon dioxide emission around the world. Environ Sci Pollut Res :1–12

Murshed M, Rashid S, Ulucak R, Dagar V, Rehman A, Alvarado R, Nathaniel SP (2021a) Mitigating energy production-based carbon dioxide emissions in Argentina: the roles of renewable energy and economic globalization. Environ Sci Pollut Res :1–20

Murshed M, Ahmed Z, Alam MS, Mahmood H, Rehman A, Dagar V (2021) Reinvigorating the role of clean energy transition for achieving a low-carbon economy: evidence from Bangladesh. Environ Sci Pollut Res 28(47):67689–67710

Naeem MA, Rabbani MR, Karim S, Billah SM (2021a) Religion vs ethics: hedge and safe haven properties of Sukuk and green bonds for stock markets pre-and during COVID-19. Int J Islam Middle East Finan Manag

Naeem MA, Mbarki I, Alharthi M, Omri A, Shahzad SJH (2021) Did COVID-19 impact the connectedness between green bonds and other financial markets? Evidence from time-frequency domain with portfolio implications. Front Environ Sci 9:180

Naeem MA, Sehrish S, Costa MD (2021c) COVID-19 pandemic and connectedness across financial markets. Pac Account Rev

Naeem MA, Karim S (2021) Tail dependence between bitcoin and green financial assets. Econ Lett :110068

Naeem MA, Peng Z, Suleman MT, Nepal R, Shahzad SJH (2020) Time and frequency connectedness among oil shocks, electricity and clean energy markets. Energy Econ 91:104914

Oseni MO, Pollitt MG (2016) The promotion of regional integration of electricity markets: Lessons for develo** countries. Energy Pol 88:628–638

Pesaran HH, Shin Y (1998) Generalized impulse response analysis in linear multivariate models. Econ Lett 58(1):17–29

Pham L, Huynh TLD (2020) How does investor attention influence the green bond market? Finance Res Lett 35:101533

Rehman A, Radulescu M, Ma H, Dagar V, Hussain I, Khan MK (2021) The impact of globalization, energy use, and trade on ecological footprint in Pakistan: does environmental sustainability exist? Energies 14(17):5234

Saeed T, Bouri E, Alsulami H (2021) Extreme return connectedness and its determinants between clean/green and dirty energy investments. Energy Econ 96:105017

Salisu AA, Vo XV (2020) Predicting stock returns in the presence of COVID-19 pandemic: the role of health news. Int Rev Financ Anal. https://doi.org/10.1016/j.irfa.2020.101546

Sehgal S, Pandey P, Diesting F (2017) Examining dynamic currency linkages amongst South Asian economies:an empirical study. Res Int Bus Financ. https://doi.org/10.1016/j.ribaf.2017.05.008

Shahzad SJH, Bouri E, Kristoufek L, Saeed T (2021) Impact of the COVID-19 outbreak on the US equity sectors: evidence from quantile return spillovers. Financial Innov 7(14):1–23

Shen Y, Shi X, Variam HMP (2018) Risk transmission mechanism between energy markets: aVAR for VaR approach. Energy Econ 75:377–388. https://doi.org/10.1016/j.eneco.2018.08.027

Simshauser P, Tiernan A (2019) Climate change policy discontinuity and its effects on Australia’s national electricity market. Aust J Public Adm 78(1):17–36

Singh VK, Kumar P, Nishant S (2019) Global connectedness of MSCI energy equity indices: a system-wide network approach. Energy Econ 84:104477

Tiwari AK, Nasreen S, Shahbaz M, and Hammoudeh S (2020) Time-frequency causality and connectedness between international prices of energy, food, industry, agriculture and metals. Energy Econ 85:104529

**ao B, Yang Y, Peng X, Fang L (2019) Measuring the connectedness of European electricity markets using the network topology of variance decompositions. Phys A Stat Mech App 535:122279

Yan G, Truck S (2020) A dynamic network analysis of spot electricity prices in the Australian national electricity market. Energy Econ 92:1049722

Zakari A, Toplak J, Ibtissem M, Dagar V, and Khan MK (2021) Impact of Nigeria’s industrial sector on level of inefficiency for energy consumption: Fisher ideal index decomposition analysis. Heliyon 7(5):e06952

Zakari A, Khan I, Tan D, Alvarado R, and Dagar V (2022) Energy efficiency and sustainable development goals (SDGs). Energy 239:122365

Zobaa AF, Lee WJ (2006) The globalization of energy markets in Asia. IEEE Power Engineering Society General Meeting 6

Acknowledgements

The authors would like to thank the organizers and participants of International Conference on Economics, Energy and Environment-ICEEE’2021 for their helpful comments that improved the quality of our manuscript.

Author information

Authors and Affiliations

Contributions

Sitara Karim: writing — review & editing, methodology, software, formal analysis, original draft.

Muhammad Abubakr Naeem: conceptualization, data curation; methodology, software, visualization, writing — review & editing.

Mustafa Raza Rabbani: writing — review & editing, original draft.

Abdelrahman Ahmed Meero: writing — review & editing, original draft.

Suha M. Alawi: writing — review & editing; supervision.

Corresponding author

Ethics declarations

Ethics approval

Not applicable.

Consent for participate

Not applicable.

Consent for publication

Not applicable.

Competing interests

The authors declare no competing interests.

Additional information

Responsible Editor: Philippe Garrigues

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Alawi, S.M., Karim, S., Meero, A.A. et al. Information transmission in regional energy stock markets. Environ Sci Pollut Res 30, 43000–43012 (2023). https://doi.org/10.1007/s11356-022-19159-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-022-19159-1