Abstract

Prior studies on real earnings management (REM) focus mainly on estimating abnormal operating and investing activities at the firm level. We extend this literature by providing micro-level evidence regarding how financial reporting pressures influence new product release decisions, or product-level REM. Specifically, we compare how public and private studios differentially time the release of their movies. We find that, faced with pressure to boost quarterly revenues and earnings, public studios are more likely to release movies with high expected revenues in the last month of a fiscal quarter, compared to private studios. This documented result is stronger for firms with recent poor past performance, but is not present for movies in genres with a more targeted release window (e.g., romance and horror movies) and those using directors who have a history of collaboration with the studio. These results suggest that studios choose REM activities that have a lower impact on consumer demand and that minimize conflict with talent, consistent with choosing less costly activities to achieve financial reporting goals. A negative consequence of this financial reporting–driven product release strategy is that movies released in the last month of a quarter have lower international box office revenues. Taken together, these results provide evidence of the existence and consequences of product-level REM.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The extant literature on real earnings management (REM) finds that managers meet or beat earnings targets by manipulating production (Roychowdhury 2006); discretionary expenditures such as research and development (R&D) and selling, general, and administrative expenses (SG&A) (Chapman and Steenburgh 2011); and sales (Ahearne et al. 2016). Most of these studies estimate firm-level REM activities using residuals in regressions of actual costs (or operating cash flow) on firm assets, revenue, and revenue growth. While this approach takes advantage of a large sample of data, it does not consider detailed information about firm operations and could thus result in measurement errors and misinterpretation of the results (for details, see Srivastava (2019) and Cohen et al. (2020)). Except for Bruns and Merchant (1990) and Cohen et al. (2010), there is scant evidence regarding how managers make operating decisions to manipulate earnings to achieve specified performance targets. Brennan (2021) has noted that academics rarely study the detailed day-to-day practice of earnings management, most likely because of the difficulty of obtaining data.

To address this gap in the literature—and taking Brennan’s (Brennan 2021) comment into account—we examine real earnings management at a micro level pertaining to new product releases. We determine whether movie studios owned by publicly traded companies (hereafter “public studios”) strategically release movies to manage earnings to help their parent companies meet their quarterly performance targets. We use private studios—studios that are neither listed nor owned by a listed company—as a control group and study variations in these activities among public and private studios, as the two groups face different performance pressures and incentives to engage in real earnings management.

The movie industry is economically significant because it includes about 22,000 establishments with combined annual revenue of about $89 billion (Dun and Bradstreet 2021). In addition, it provides several advantages when we address our research questions. First, detailed product-level information, such as new movie release schedules and cost and revenue data, are publicly available. Such data provides a rare opportunity for conducting product-level analyses to supplement firm-level findings (Eliashberg et al. 2006). Second, the movie industry consists of a large number of private and public studios, which permits us to make comparisons. Since private studios face less financial reporting pressure from the capital market (Sheen 2020), they serve as a natural control group for public studios. This allows us to use a cleaner research design than most existing studies, which use the industry average as a control group in their estimation of REM (Srivastava 2019).

We suggest that public studios are more prone to engage in real earnings management to boost earnings vis-à-vis private studios since they face stronger scrutiny from the capital market for missing earnings targets (Sheen 2020). Specifically, we predict that public studios are more likely to release movies with high expected box office revenues in the last month of a quarter, compared to private studios.Footnote 1 By the last month of a quarter, managers have a more accurate idea of their quarterly earnings. If they anticipate that quarterly performance will likely fall short of expectations, they have strong incentives to release movies with high expected box office revenues to boost their quarterly performance. We measure a movie’s expected revenue potential by its production cost and past box office revenues of the movie director’s previous movies, because prior studies have shown that production cost and a director’s track record are strong indicators of box office revenue (Ravid 1999; Gong et al. 2011). Based on a sample of 3,094 US-produced English-speaking movies released between 1997 and 2019, our results are consistent with this prediction.

We also argue that public studios face different performance pressures. Some public studios may perform well at the box office throughout a quarter while others may experience disappointing results in earlier months. We hypothesize that if a public studio’s recent performance is poor, the studio is more likely to release movies with high expected revenues in the last month of a quarter. In distinction, if a public studio’s recent performance is good, the studio is less likely to do so and might even release movies with high expected revenues in the first month of the next quarter. Our results are consistent with this prediction. Overall, we find strong evidence that public studios release movies in a pattern consistent with their motives to improve quarterly reported revenues and earnings.

While managers have a variety of ways of managing operating activities to achieve financial reporting goals, they will likely weigh the costs of such maneuvers. For instance, Cohen et al. (2008) find that companies are more likely to choose REM than accrual-based earnings management after the Sarbanes-Oxley Act (SOX) because the latter is more costly in the post-SOX era. Similarly, we predict that when public studios strategically release new films to achieve performance targets, they will use relatively less costly mechanisms. Specifically, we predict that studios are less likely to engage in real earnings management when releasing movies with seasonal appeal, because the revenues of these films can be negatively affected to a larger extent by bad timing. Instead, the studios will release movies with non-seasonal appeal to audiences throughout the year when they engage in real earnings management. Consistent with this prediction, we find that public studios, to garner higher expected revenues in the last month of a quarter, release movies in certain genres, such as adventure, comedy, and drama, which can attract audience attention at any time of the year. These genres appeal to audiences across seasons, providing studios with greater flexibility regarding the timing of their releases.

We also hypothesize that studios avoid potential damage to long-term relationships with their collaborators when engaging in real earnings management using movie releases. We find that when public studios release movies with high expected revenues in the last month of a quarter, they target movies produced by directors with whom they have not worked previously. Thus, studios try to preserve their long-term relationships with directors with whom they have already worked. This and the above results are consistent with our conjecture that public studios try to minimize unintended consequences when they release new movies based on financial reporting concerns.

Next, we examine the consequences of REM. Prior literature presents mixed evidence regarding the impact of REM on future performance (Bhojraj et al. 2009; Gunny 2010). We find that movies released in the last month of a quarter generate lower international box office revenues, which may be due to their premature release and the difficulty in coordinating international distribution at the last minute. Thus, there are negative consequences when public studios release movies with high expected revenues in the last month of a quarter to meet earnings expectations, especially in the international market. In addition, we find that these films have lower Google search popularity in the month of release, but their popularity increases in the subsequent month, suggesting that the negative impact of rushed movie releases could diminish over time.

This paper contributes to the growing literature on real earnings management. While there is general agreement on the existence of real earnings management, there is debate pertaining to its prevalence, magnitude, and methods of detection (Srivastava 2019; Cohen et al. 2020). Distinct from prior studies that use Compustat data to estimate residuals as a measure of firm-level abnormal operating and investing activities, we use more micro-level (product and quarterly level) data on management decisions of new product releases to document the existence of real earnings management.

Recently, the REM literature has shifted from firm-level, residual-based analysis to industry-specific analysis (e.g., Grieser et al. 2021). This industry-specific research design provides researchers with the advantage of using knowledge of institutional arrangements to characterize management activities (McNichols 2000; Luft 2021). In our analysis, we show that when engaging in REM, studios target movies with non-seasonal appeal to audiences, and those made by directors who have not previously collaborated with the studio. An implication is that firms choose the path with the least cost or least resistance to manage revenues and earnings in order to meet financial reporting goals.

This paper also contributes to the literature on new product releases, particularly movie release strategies. We find that financial reporting concerns affect the timing and types of new product releases, with potential negative consequences for movies’ international box office revenues.

While our paper focuses on the movie industry, similar patterns are likely to exist in other industries. For example, based on statistics from RavenPack, a leading data analytics company, nearly 10% of firms had news coverage specifically related to new product releases in 2019, the most recent year in our sample period. These firms might use new product releases to boost revenues as well. The film industry is an ideal setting to examine such behavior, given its standardized and publicly available product-level information.

The remainder of the paper proceeds as follows. Section 2 reviews relevant literature and develops our hypotheses. Section 3 discusses the research design and our measures of primary variables, while Section 4 presents our findings. Section 5 summarizes and concludes the paper.

2 Related literature and hypothesis development

In this section, we review the real earnings management literature and discuss the institutional background of the movie industry. This discussion leads to the development of our hypotheses.

2.1 Real earnings management

Extensive literature has documented that public companies have incentives to meet or beat important earnings benchmarks, such as earnings for the same quarter of the previous year and analyst forecasts (Burgstahler and Dichev 1997; Dechow and Skinner 2000; Bartov et al. 2002). Missing these benchmarks could result in consequences such as reduced credibility with the capital market, decreases in stock price, damage to management reputation, and losses in employee bonuses (Graham et al. 2005). As a result, when the performance of a company is below the desired level, managers may use various methods to boost their earnings.

Although managers could use accounting choices, such as accruals, to increase earnings, prior studies suggest that managers also engage in economic activities that deviate from normal operational practices—including real earnings management—to achieve these financial reporting goals (Cohen and Zarowin 2010; Zang 2012). For instance, Graham et al. (2005) find that 80% of chief financial officers would decrease discretionary spending to meet an earnings target. Their survey results are supported by empirical evidence related to reductions in discretionary expenditures, such as research and development (R&D), advertising, maintenance, and investment, towards the end of the financial period (Baber et al. 1991; Cohen et al. 2010; Eldenburg et al. 2011; Vorst 2016). Other REM methods include excessive product discounting to increase revenues, accelerating the timing of sales, and overproducing to reduce the cost of goods sold to improve margins (Jackson and Wilcox 2000; Herrmann et al. 2003; Roychowdhury 2006; Mizik and Jacobson 2007; Dechow and Shakespeare 2009; Sellami 2015; Ahearne et al. 2016).

One limitation of the literature on REM is that researchers use residuals from regressions to estimate real earnings management activities such as abnormal production costs and abnormal discretionary expenditures. The residuals are calculated from multiple regression models of a firm’s costs and expenses as a function of its revenues, assets, growth in revenues, and other control variables (e.g., Roychowdhury 2006; Cohen and Zarowin 2010; Zang 2012; Kothari et al. 2016). While such proxies are widely available for most firms, they may contain measurement errors, as they fail to take into consideration the differences among firms, especially given their different business strategies (Srivastava 2019; Cohen et al. 2020). In this study, we use a different approach by employing an industry-specific setting to study the REM, similar to Grieser et al. (2021).

2.2 The motion picture industry

Our research setting is the motion picture industry, a central segment of the US economy. The movie industry is economically significant, as it includes 22,000 organizations, accounts for 2.5 million jobs and annual revenues of $89 billion (Dun and Bradstreet 2021), and leads to downstream revenues in other sectors of the economy, such as video games, music, toys and other forms of merchandising, not to mention ripple effects on local businesses. For instance, the six live-action Transformers movies not only generated $6.23 billion in global box office revenue but also grossed over $22.67 billion from downstream markets of merchandising, television shows, licensing, animated films, and soundtracks for the franchise owners, Hasbro and Takara Tomy.Footnote 2 As part of the larger picture, total global spending on entertainment and media (including film, television, internet, radio, publishing, and video games) is expected to reach $2.9 trillion in 2023 (PricewaterhouseCoopers LLP (PwC) 2022).

Studios hire a variety of talent such as writers, actors/actresses, directors, and producers who are involved in a complex process that includes develo** a script, securing financing and talent, greenlighting the film, producing the film, and post-production editing (Young et al. 2009). High-profile movies can incur millions of dollars in development costs, driven by the costs of special effects and high salaries for talent (IBISWorld Inc 2021). Once a studio has produced a movie and negotiations with theater chains are completed, the movie is exhibited in theaters. The studios and theaters each garner a certain percentage of the box office revenues. Theatrical box office releases are one of the most important channels from which studios generate revenues, and a large percentage of theatrical box office revenues are earned in the first week of release (Gilchrist and Sands 2016). Downstream revenues, such as DVD and Blu-ray sales, streaming, and cable and network deals, all rely on theatrical box office performance (Gong and Young 2016).

The movie release scheduling decision is a complex process, but studios have control of release dates in the domestic market. International release scheduling is more difficult due to piracy concerns and the number of countries involved. Once a movie’s release date is set, studios can alter the date, although this involves additional coordination with theaters.Footnote 3 As theaters do not start selling tickets until the actual film release date, it is difficult to systematically observe all movies’ initial release dates and subsequent changes.

Studios recognize box office revenues and expense movie development costs according to Statement of Position 00-2 (SOP 00-2), Accounting by Producers or Distributors of Movies (American Institute of Certified Public Accountants (AICPA) 2000). SOP 00-2 effectively requires studios to capitalize the costs of develo** and producing a movie, and to recognize revenue after the movie is shown in theaters and through other distribution channels. The capitalized cost will be amortized as a matched cost against revenue from released films over a maximum period of 10 years. The amortization is equal to the current year’s revenue divided by the total estimated revenue within 10 years after the theatrical release; however, producers and distributors must re-evaluate the capitalized cost every year using fair value accounting (calculated from expected cash flow) and record any changes in fair value on the income statement. Thus, if a movie’s box office revenue is lower than expected, studios have to write off a larger portion of the capitalized development cost because there is a low probability that the studio will be able to recover it.

While predicting box office revenues is uncertain, the literature has shown that movies with higher production costs, which, in turn, are associated with higher advertising costs, and movies by directors whose previous works have had strong box office performance, usually garner higher box office revenues (Gong et al. 2011). Anecdotal evidence suggests that during the opening weekend of a movie’s release, studio executives wait for the initial box office performance of a movie, which helps guide subsequent investment decisions (e.g., more advertising and a sequel) (Gong et al. 2011).

2.3 Real earnings management through movie release timing

Prior literature has shown that managers manage earnings upward near the last month (quarter) of a quarter (year) to boost earnings (Dhaliwal et al. 2004; Jacob and Jorgensen 2007; Kerstein and Rai 2007; Das et al. 2009; Cohen et al. 2010) when the excess or shortfall from the target becomes known. Hence, the timing of manipulation is a critical distinguishing feature that can provide a means to detect such target management behavior. Typical real earnings management methods include accelerating sales, cutting discretionary spending (including R&D expenses, maintenance costs, and investment), and overproduction to reduce production costs (Graham et al. 2005; Roychowdhury 2006; Sellami 2015; Ahearne et al. 2016).

Little research has examined the role of new product releases—a key decision that managers can control—in attempts to boost earnings. A recent McKinsey survey suggests that launching new products or services is a shrewd way to boost revenue growth, as more than 25% of total revenue and profits are driven by new products (McKinsey and Company 2017). One possible reason for the lack of empirical evidence regarding real earnings management via new product releases is data limitation, as researchers rarely have the opportunity to systematically observe all new product releases across a large number of firms.

The movie industry offers an ideal setting in which to study the effects of new product releases, as studio managers frequently release movies, and detailed information about these movies is publicly available. Furthermore, compared to industries where it takes years to generate a new product, the frequent releases of new movies make it possible to observe an ample number of releases in a given period. When a studio is not performing well in the early part of a quarter (especially after facing recent box office failures), studio managers might see an opportunity to release additional movies in the last month to boost their revenues, earnings, and cash flows.Footnote 4 For high-potential movies that were originally scheduled to be released in the last month, studio managers may exert more effort to prevent delays. It seems prudent to only release movies with a high probability of success and high expected revenues (e.g., blockbusters). Alternatively, low-potential movies are more likely to fail and generate lower-than-expected box office revenue, which would result in a write-off of the capitalized production costs and lead to a negative impact on earnings. Thus, we expect that studios are more likely to release movies with high expected revenues in the last month of a fiscal quarter.

Although both private studios and public studios want to boost their quarterly earnings, public studios have much stronger incentives to do so, given the additional capital market pressure they or their parent companies face. The stock prices of public studios or their parents are likely to suffer after a worse-than-expected quarter, while private studios are more protected from such short-termism (Sheen 2020). In addition, unlike private studios with a small number of shareholders, public studios do not have a credible way to communicate with their diverse shareholders, which strengthens their incentives to boost earnings. This discussion leads to our first hypothesis:

-

Hypothesis 1: Compared to private studios, public studios are more likely to release movies with high revenue potential in the last month of a fiscal quarter.

Is there a credible null hypothesis to counter this expectation? We believe there are at least three reasons why public studios might not act in our predicted way. First, managers may not want to release movies with high expected revenues prematurely because if the movie fails at the box office, they will have to write off a significant portion of the high capitalized development costs, making the reported earnings even worse. Second, other stakeholders of a movie, such as the above-the-line participants,Footnote 5 will try their best to prevent a premature release because their share of the movie’s revenue or profit will be cut. Third, studios do not have complete control over theaters’ scheduling decisions. Each studio has a team of experts to negotiate with theaters on movie release schedules. Theaters will not do anything that really angers studio managers, especially those of the major studios; however, the theaters ultimately make the scheduling decision.Footnote 6 Studios might not be able to secure enough showings for their movies if they change the release schedule on short notice.

2.4 Recent performance and movie releases among public firms

While managers always have the motivation to increase their earnings, their incentives to do so are stronger when earlier performance in the quarter or year has been poor, as the probability of missing the earnings benchmarks increases. Consistently, the literature has documented that firms with poor initial performance in a quarter (or a year) adjust their advertising expenses and other discretionary items in the third month (or the last quarter of the year) to increase earnings (Das et al. 2009; Cohen et al. 2010).

In the motion picture industry, public studio managers face the same tradeoff between the costs and benefits of earnings management, and they are more likely to commit earnings management when recent performance is poor. Releasing high-expected-revenue movies can improve quarterly earnings. Anecdotally, in 2015, Walt Disney Studios’ box office revenues had slowed considerably in the third quarter. In December of the fourth quarter, Disney released Star Wars: The Force Awakens, which drove a strong fourth quarter and had the highest grossing opening weekend of all time (to that point) (Fritz 2016). Releasing movies with higher expected revenues also involves additional advertising costs and the risk of a box office flop. Studio managers are more likely to bear these costs when their recent performance has been poor. On the other hand, when a studio performs well, it might be more inclined to release some high-potential movies at the beginning of the next quarter. Thus, we expect:

-

Hypothesis 2: If a public studio’s recent performance is poor, it is more likely to release movies with high revenue potential in the third month of a fiscal quarter.

2.5 The costs of real earnings management through new product releases

In this section, we make predictions regarding the costs of real earnings management using new product releases and their impact on managerial decisions. Managers have multiple methods to boost their performance and usually choose the least costly of them. For example, as the SOX Act makes it more costly to engage in accrual-based earnings management, companies engage in more real earnings management (Cohen and Zarowin 2010). Similarly, we argue that when managers commit real earnings management using new product releases, they prefer the most cost-efficient method. We study two costs associated with REM in new movie releases.

The first cost of REM through new movie releases is the potential loss of revenues. Certain genres of movies have non-seasonal appeal to customers, while others have seasonal demand. For example, romantic movies and horror movies are more likely to be released in February (around Valentine’s Day) and October (around Halloween), respectively, to capture the largest consumer demand. Deviation from these optimal release windows might reduce expected box office revenues. Movies in other genres, such as adventure, comedy, and drama, have consistent year-round appeal since their box office revenues are less subject to the timing of the release. When engaging in real earnings management using movie releases, studios are likely to take such differences into consideration and avoid scheduling seasonal movies into the last month due to earnings management incentives. In summary, movie genres affect the optimal release timing and, thus, the costs of real earnings management. This leads to the following hypothesis:

-

Hypothesis 3a: Studios are less likely to engage in real earnings management when releasing movies with seasonal appeal or popularity.

The second type of REM costs using new movie releases is tied to the relationship among the main stakeholders of a movie, such as the studio and directors. Informal alliances between a studio and a director widely exist in the movie industry. For instance, 20th Century Studios has a strong relationship with James Cameron, a leading science fiction director. Over time, directors and studios develop long-term relationships to their mutual benefit. Often, the scheduling of a movie involves the input of the major parties to the film. As studios and directors build long-term relationships, rescheduling a movie due to a studio’s financial reporting incentives might damage the trust and relationships they have built over the years. Prior research has shown that trust and long-term relationships are key factors in preventing opportunistic behaviors in inter-organizational contracts (Caglio and Ditillo 2008; Susarla et al. 2020). Thus, we predict that studios are less likely to reschedule movies by directors with whom they have worked before.

-

Hypothesis 3b: Studios are less likely to engage in real earnings management when releasing movies by directors with whom they have worked previously.

2.6 Performance consequences of releasing movies in the last month

Whereas real earnings management helps to prevent a company from missing its earnings benchmarks and enduring the subsequent consequences, there is no conclusive evidence on the consequences of REM. Both academics and corporate executives acknowledge that REM involves a significant amount of costs (e.g., Roychowdhury 2006; Dichev et al. 2013). For example, excessive discounting could motivate customers to shift their future purchases forward or to negotiate similar discounts in the future. Similarly, overproducing firms may incur inventory holding costs and be exposed to risks such as obsolescence.

The improvement in current performance seems to occur at the expense of long-term profits, although the empirical evidence on this is mixed. Eldenburg et al. (2011) investigate REM in a nonprofit setting and find weak evidence suggesting the use of REM in hospitals and a possible negative impact of REM on future performance. Brüggen et al. (2011) find that overproduction results in damage to brand reputation. Cutting R&D spending to reduce cost results in negative long-term consequences such as a reduction in innovative outputs and innovative efficiency (Bereskin et al. 2018).

There is also evidence that REM is associated with positive future performance among samples such as small firms (Beyer et al. 2018). Similarly, Gunny (2010) finds that REM firms that meet zero-profit or prior-year profit benchmarks have better future performance than non-REM firms that miss these benchmarks, as managers use REM to signal future performance. Zhao et al. (2012) also find evidence of a positive relationship between REM and future performance.

In the movie industry, a less well-planned release, such as one motivated by financial reporting concerns, will hurt a movie’s box office performance, especially given the logistic difficulties in international markets. Therefore, the box office revenues of movies released in the third month of a quarter might fall short of their optimal level.

-

Hypothesis 4: Movies released in the third month of a quarter due to financial reporting concerns earn lower domestic and international box office revenues.

We also note that there are competing alternatives to this hypothesis. As studios release movies with high expected box office revenues in the last month of a quarter, they have strong incentives to make sure these movies perform well. Otherwise, they face pressures to write off the capitalized development costs, resulting in even worse performance.

3 Data and research design

3.1 Data and sample selection

To test our hypotheses, we rely on detailed information on movies in the OpusData provided by Nash Information Services LLC, a premier provider of movie industry data and research services. The database contains each movie’s production costs, release schedules, box office revenues, and other characteristics. Our sample consists of 3,094 US-produced, English-language movies released between 1997 and 2019 with relevant information regarding production costs and director track records.

3.2 Variable measurement

Our key conceptual dependent variable is the timing of movie releases. Since a studio’s performance reports are on a quarterly basis, we define movie release timing on a quarterly level. Our empirical proxy is an indicator variable that captures whether a movie is released in the last month of a quarter (Last month in a quarter). In our sample of public firms, a fiscal quarter coincides with a calendar quarter.

When testing the consequences of movie release strategies, our key conceptual dependent variable is movie performance in the market. We measure movie performance with the revenues and return on investment generated by a movie. We have two proxies for the revenue variable. The first proxy is the box office revenue in the domestic market (ln(B.O.)). The second proxy is the box office revenue in the international market (ln(International B.O.)). The return on investment is measured by the sum of domestic and international revenues divided by production cost (Return on investment).

Our first key independent variable is Public Studio, an indicator variable that captures whether a movie is released by a public studio or a private studio. Studios are considered public if they or their parent companies are listed on one of the stock markets.Footnote 7 A private studio is an independent studio that is not owned by a publicly traded company. Large private studios in our sample include IFC Films, Magnolia Pictures, and Indican Pictures; these studios have released movies such as Olympus Has Fallen and Paddington. Major public studios include Warner Bros. Pictures, Walt Disney Studios, and Paramount Pictures, among others.

Our second set of key conceptual independent variables is a movie’s revenue potential. We use two proxies for this variable. The first is production cost (ln(Production costs)). Production costs include all costs related to making the film. The second proxy is director power (Director power), which represents the past track record of the movie’s director, as measured by the average box office revenue of the movies he/she directed in the past. The literature has suggested that both variables are highly predictive of box office revenues (Gong et al. 2011).

We include several movie-level and consumer demand related control variables that could influence a movie’s probability of being released in the last month of a quarter and its box office performance. The first control variable, Sequel, is an indicator variable that represents whether a movie is a sequel. Past studies have shown that sequels generate higher revenues than non-sequels (Gong et al. 2011). The second control variable is a categorical variable based on the parental guidance suggestion rating (PG rating), with a higher value indicating more restrictive content. PG rating equals zero for films offered to the general audience; “1” for PG-13 films, where strong parental caution is suggested; and “2” for restricted films, where children under 17 require an accompanying parent or adult guardian. We control for two variables related to release timing. First, Friday is a dummy variable that is equal to 1 if the movie is released on Friday and 0 otherwise. Holiday is a dummy variable that represents whether a movie is released around a major holiday, such as Independence Day or Thanksgiving. We also control for genre fixed effects and year fixed effects in our specifications.

3.3 Statistical models

We use the following logit model (1) to test our first hypothesis (on the probability that a movie will be released in the last month of a fiscal quarter to address financial reporting concerns).

In Model (1), the dependent variable is the odds ratio of whether the movie is released in the last month of a quarter, i.e., March, June, September, or December. We use a logit model, given the binary nature of the dependent variable. The variable of interest is the interaction between a dummy variable (Public Studio) and the proxy for revenue potential movies. α2 measures the impact of film potential on the probability of its being released in the last month of a quarter among private studios. A positive coefficient for α1 would indicate that public studios are more likely to release movies with high expected box office revenues in the last month of a quarter, compared to their private counterparts. We include the above-mentioned control variables indicating whether a film is a sequel (Sequel), released on Friday (Friday), and released during a holiday (Holiday), as well as its rating (PG rating). We also include genre fixed effects and year fixed effects in our specifications.

To test Hypothesis 2 (regarding whether public studios are more likely to release movies with high revenue potential in the last month of a quarter when their recent performance is poor), we use the following logit model:

We use the mean and median box office revenues of movies released by the public studios (Mean performance in month t-2 and Median performance in month t-2) as our proxy for Recent performance. If public studios are more likely to release high-potential movies near the quarter-end following poor performances, we would expect α1 to be negative.

To test Hypotheses 3a and 3b (regarding how the costs of real earnings management affect movie release strategies for both public and private studios), we replicate Model (1) using subsamples with different costs of real earnings management. Specifically, we estimate Model (1) for each major genre and for directors who have or have not worked with the studio in the past, to test H3a and H3b, respectively.

To test Hypothesis 4 (regarding the consequences of releasing a movie in the last month of a quarter for both public and private studios), we use the following OLS specification:

We use multiple measures to capture movie performance, including domestic box office revenues (ln(B.O.)), international box office revenues (ln(International B.O.)), and the return on investment (Return on investment). A positive (negative) coefficient for α1 indicates that compared to their private counterparts, movies released by a public studio in the last month of a quarter perform better (worse), after the control variables are considered.

3.4 Sample description

Our final sample includes 3,094 movies released in US cinemas—2,347 by public studios and 747 by private studios—between 1997 and 2019.Footnote 8 In Table 1 Panel A, we present the summary statistics for these movies. The median production budget is approximately $28 million. Slightly more than one-third are released in the last month of a quarter. The majority require some level of parental guidance. About 13% are sequels. Most (87%) are released on Fridays, and 17% are released during the holiday seasons. The median domestic box office is larger than $3 million. Among movies released internationally, another $3 million of box office revenue was generated.

In Panel B, we tabulate the number of movies released each month. In each month, there are more movies released by public studios than by private ones. We also notice that there are a larger number of movies released by public studios in November and December, compared to movies released by private studios.

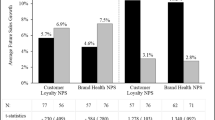

Figure 1 tabulates the number of high-expected-revenue movies based on the release month and the producer type. Among movies produced by a private or public studio, movies with production costs higher than the median are considered high-expected-revenue movies. While the number of movies released by private studios is evenly distributed across the three months within a quarter, public studios release more movies with high expected revenues in the last month of the quarter. The figure is quite similar if movies’ box office potential is classified based on director power.

Expected revenues and frequency of movies released in months of a quarter. Figure 1 above tabulates the number of movies with high expected box office revenues based on release month and studio type. Among movies produced by a private or public studio, movies with above-median production costs are considered movies with high expected box office revenues

4 Empirical results

4.1 Movie releases in the last month of a quarter by public studios

Results testing Hypothesis 1 are presented in Table 2. In Column 1, the production cost is used to proxy for high-potential movies; director power, as measured by the director’s average box office revenue in the past, is used to proxy for high-potential movies in Column 2. Both models have relatively low pseudo R-squared, indicating the difficulty of predicting movie release timing.

We test the differences between public studios and private studios using the interactions between Public studio and ln(Production costs) and between Public studio and Director power in Columns 1 and 2, respectively. Both coefficients are positive and significant, indicating that public studios are more likely than private studios to release movies with high expected box office revenues in the last month of a quarter. As public studios face additional performance pressure from the capital market, this is consistent with their releasing new movies to boost quarterly revenues. Neither production cost nor director power has a significant direct impact on the probability of a last-month release.

4.2 Past performance and releasing high-expected-revenue movies

To further establish that public studios release movies with high expected revenues in the last month due to performance pressure, we conduct additional analyses related to how past performance affects the possibility of releasing movies with high expected box office revenues in the last month of a quarter among public studios. Specifically, we test interactions between studio performances in month t-2 (Mean performance in month t-2 and Median performance in month t-2) and proxies for high-potential movies. Studio performance is measured by the mean or median box office revenues of movies released in the month. A negative coefficient would suggest that studios are less likely to release movies with high box office potential in the last month of a quarter when their past performance is good. We focus on performance in month t-2 rather than the last month. Our discussions with industry executives suggest that it takes time for studios to develop release plans and it is difficult to analyze performance in the last month and then adjust next month’s movie release plans.

The results are reported in Table 3 Panel A, where the first two columns use production costs and the last two columns use Director Power to proxy for expected box office revenues. To measure past performance, Columns 1 and 3 use Mean performance in month t-2, whereas Columns 2 and 4 use Median performance in month t-2. Consistent with our expectation that public studios have weaker incentives to release movies with high expected revenues in the last month of a quarter when their performance is good, we find negative coefficients for all the interactions. We note that the negative coefficient for the interaction in Column 3 is not statistically significant at the 0.1 level. This could be due to measurement errors which increase the noise in estimation.

When their recent performance is strong, public studios’ incentives to release high-potential movies in the last month of a quarter are reduced. Further, the studios might delay the release of high-potential movies until the next quarter. To test this possibility and to complement the results above, we examine the relationship between the probability of a high-potential movie being released in the first month of a quarter and a studio’s past performance. We use the same regression model as in Table 3 Panel A, except that the dependent variables are the probability of movie release in the first month of a quarter. The results are reported in Table 3 Panel B.

We find positive coefficients for the interaction terms between the movie-potential variables and a studio’s past performance, suggesting that public studios are more likely to release movies with high expected revenues in the first month of the next quarter when their recent past performance is good. This provides further support for Hypothesis 2.

4.3 The costs of real earnings management and movie releases

Managers incur direct or indirect costs when they manipulate real operations activities. Some decisions are costlier than others. Our setting provides a rare opportunity to test the relationship between implicit costs of REM and observed REM activities. Anecdotal evidence suggests certain types of movies are costlier to reschedule to the last month of a quarter. Specifically, certain movie genres are costlier to shuffle than others. For example, the horror and thriller genres appeal most to audiences in October (Halloween), while romance appeals most to audiences in February (Valentine’s Day). Movies in other genres have similar revenue-generating potential throughout the year. We expect the horror, thriller, and romance categories to be less likely to be moved to the last month of a quarter, due to their seasonal demands. In Table 4, we replicate Eq. (1) for each major genre. To proxy for movies with high expected revenues, Panel A uses production costs and Panel B uses director power. In both panels, we find that our previously documented pattern of releasing high-expected-revenue movies in the last month of a quarter does not exist among horror, thriller, and romantic movies but is concentrated in adventure movies and comedies, consistent with our expectations.

Directors are important stakeholders of a movie, as their careers are directly affected by the box office revenue of the movies they produce. They are likely to have their own preferences on when to release their movies, which may not always coincide with the studio’s preference. As studios and directors might work with each other multiple times, implicit and informal contracts are likely. We thus explore how a director’s past cooperation with a studio affects the probability of their movies being released in the last month of a quarter (possibly due to performance pressure). Given the uncertainties and difficulties in rescheduling a movie, studio managers will try to avoid rescheduling a movie by a director with whom they have repeatedly cooperated. That is, we would expect that studios are less likely to engage in this behavior with a director they have worked with in the past, as this could jeopardize the trust and relationship built from past interactions. In Table 5, we replicate Eq. (1) in subsamples where the directors have (or do not have) past cooperation with the studio. We find that our main results are concentrated in movies whose directors are working with the producer for the first time.

4.4 Performance consequences of releasing movies in the last month

We test the consequences of releasing a movie in the last month of a quarter and report the results in Table 6. We compare the performance differences between movies released in the last month of a quarter by public and private studios. We acknowledge that this is a conservative test, as not all movies released in the last month are scheduled due to performance pressure. Despite this, we do have some evidence that compared to their private counterparts, movies released by public studios in the last month of a quarter have lower international box office revenues, as shown in Panel A. This is consistent with premature or rushed releases; however, these movies do not have significantly lower domestic box office revenue or overall return on investment.Footnote 9 This result could be due to studios already taking into consideration the costs of rescheduling (especially for genres with relatively higher rescheduling costs, such as horror and romance).

Panel B of Table 6 reports our analysis of the impact of release timing on Google search popularity and video-on-demand revenues, to provide additional insights about long-term consequences. We find that compared to private studios, films released in the last month of a quarter by public studios are less popular in the month before film release and in the month of release, consistent with the possibility that these films are released in a rush; however, these films’ Google search popularity becomes higher in the month following the film release, and the films also have higher video-on-demand revenues, which usually become available after a film’s theatrical release. This suggests that even though a film’s initial performance might be affected by a rushed release, the negative impact could diminish over time. This could also explain the lack of an overall impact on domestic box office revenues and, more generally, the mixed long-term consequences of real earnings management documented in the literature.

4.5 Additional tests

In this section, we conduct multiple cross-sectional and robustness tests and provide additional evidence based on changes in release dates. We first examine the impact of the emergence of digital video discs (DVDs) on our results. DVD, with its affordable prices and high video quality, surpasses video home system (VHS) tapes and provides additional revenue channels for studios after theatrical release. These channels reduce a film’s reliance on theatrical box office revenues and could further reduce the potential costs of real earnings management using film releases. Thus, we investigate such a structural change by creating a window for five years before and five years after the release of DVDs in 2002 and report the results in Table 7 Panel A. The three-way interaction between Post*Public studio*High potential films is positive and significant. This is consistent with the idea that real earnings management using new movie releases only becomes statistically significant after the invention of DVD, which provides alternative distribution channels and makes such real earnings management methods less costly.

Next, we examine how our results vary with the economic significance of a movie studio in its parent company. We define economic significance as the proportion of revenues the studios contribute to their parent companies. For some studios—like Disney Studios, which is owned by the Walt Disney Company, and Universal Pictures, which is now owned by Comcast—the revenue from a movie is small compared to that of the conglomerate. Studios that make up a larger percentage of parent revenues might have higher pressure to meet financial targets. At the same time, studios generating a smaller percentage of parent revenues still have their own performance pressure. In our test, we split our sample into two groups based on the proportion of studio revenue relative to the total revenue of the parent company in the previous year. We report the results in Panel B of Table 7. Columns 1 and 3 (Columns 2 and 4) focus on the subsample where the revenue share of the parent company is above (below) the median. When using production costs as the proxy for film potential, we find that its coefficient is higher in the high-revenue-share subsample and that the difference between the two groups is not significant. When we use director power to proxy for film potential, the coefficient remains higher in the high-revenue-share subsample than in the low-revenue-share subsample; and the difference is statistically significant. Overall, there is some evidence that the results are stronger for studios with a higher revenue share of their parent company.

As a robustness test, we examine whether our results based on observations in the first three quarters are different from those in the last fiscal quarter. Prior studies have shown that managers face strong incentives to meet annual performance targets. Therefore, they tend to commit more earnings management activities in the fourth quarter than in the previous three quarters (Das et al. 2009). In Table 8, we interact our main variables with a dummy variable indicating whether it is the fourth quarter of the fiscal year and find stronger results for the fourth quarter. This result indicates that managers have stronger incentives to meet earnings expectations in the fourth quarter, which is consistent with what Das et al. (2009) find.

In untabulated results, we explore release patterns among movies released in the first or second month of a quarter. We re-estimate Eq. (1), but with a different dependent variable. We use a dummy variable that indicates the first-month release or second-month release as a dependent variable. We find some evidence that public studios are more likely to release low potential movies in the first month, consistent with studios rescheduling movies with high revenue potential in the third quarter and then releasing those with low revenue expectations in the first quarter.

Finally, we compile additional evidence based on changes in movie release dates to provide more micro evidence about how studios revise their scheduling decisions. Once a movie’s release date is announced, studios still have the option to change it. As theaters do not start to sell tickets until much closer to the actual film release date, a significant portion of these date changes might not be publicly announced (Follows 2019). With these caveats in mind, we collect initial and final movie release dates from IMDb. Among the 3,094 movies in our sample, IMDb captures a release announcement for 2,042 movies. The first announcements are, on average, 414 days (365 days in median) ahead of the initial release date. Given the early announcements, it is not surprising that 54% of these movies, or 1,105 movies, rescheduled their release dates since their final release date is different from that shown in IMDb’s database. On average, movies are rescheduled 1.7 times (1 is the median). As there may be announcements not captured by IMDb, we speculate that the actual number of reschedulings per movie could be higher. The final release dates are, on average, 115 days (21 days is the median) later than the initially announced release dates.

Next, we conduct analyses based on these observed release dates. First, we examine whether the release pattern documented in our paper holds if we use the initial release dates as the dependent variable. As our main results in Tables 2 and 3 suggest that studios adjust their scheduling decisions near quarter-ends for financial reporting purposes, we expect that the regression results should be more significant when we use the final release dates as the dependent variable than when we use the initial release dates. Thus, we replicate our main model using the dependent variable (Last month in a quarter) based on both initial release dates and final release dates, and report the results in Table 9 Panel A. The sample is limited to movies with observed changes in release dates.

In Table 9 Panel A, Columns 1 and 2 are the results when the dependent variable is initial release dates, while Columns 3 and 4 are the results when the dependent variable is final release dates. Columns 1 and 3 use production costs as the proxy for movie potential, while Columns 2 and 4 use director power. Consistent with our expectations, the results are significant only when we use the final release dates as the dependent variable. Specifically, when production costs are the proxy, the coefficient of Public studio*ln(Production costs) is statistically more significant when we use the final release dates, with a p-value of 0.001. When director power is the proxy, Public studio*Director power is only significant when we use the final release dates. These results corroborate our main findings that the final movie release dates are often motivated by real earnings management.

Next, we provide evidence about how studios make differential decisions on schedule changes for movies with high vs. low revenue potential. In Panel B of Table 9, we report an analysis based on the subsample of movies with initial release dates in the last month of a quarter. We investigate what percentage of these movies end up being released in the last month of a quarter, based on their potential and studio types. We define high-potential movies as movies with above-median production costs in their category. We find that for high-potential films originally scheduled to be released in the third month, public studios are more likely than private studios to keep the original release schedule (72% vs. 62% of the time, respectively). In contrast, for low-potential movies initially scheduled to be released in the last month, public studios are more likely than private studios to change their release dates. The public studios release 70.9% of these films in the last month, compared to 85.2% for private studios. In sum, we find that public studios are more (less) likely to keep high-potential (low-potential) movies in the last month of a quarter. This result provides additional evidence that public studios use real earnings management in the last month of a quarter.

We then explore whether the above release strategy leads to shorter delays for high-potential movies released by public studios. In Panel C of Table 9, we report our analysis of the average number of delay days (i.e., the number of days between actual release dates and initially announced release dates) based on movie potential and public status. We find that high-potential movies released by public studios are, on average, delayed by 65 days. If we assume that the initial release date is in the first month of a quarter, then the rescheduled date is more likely to be in the last month of a quarter. In contrast, delays of high-potential movies released by private studios are 2.6 times longer, with a mean of 235 days. These results show that public studios are more likely to ensure that the rescheduled release date does not slip into the next quarter, compared to private studios. For low-potential movies, those released by public studios face shorter delays, too, but the differences in delays between public and private studios are much smaller.

As a robustness check, we replicate the results in Panel C using a subsample of movies not originally scheduled to be released in the third month of a quarter. Among those films, we fail to find consistent evidence that public studios have shorter delays. Overall, the changes in release dates are consistent with our hypothesis that public studios change movie release schedules to boost their financial performance.

5 Conclusion

Detecting earnings management is a challenge (Dechow et al. 1995; Dechow and Dichev 2002; Dechow et al. 2010). Prior studies on real earnings management use firm-level data to estimate firm-level abnormal operating and investing activities as evidence of earnings management. In this paper, we extend the literature on real earnings management by focusing on product-level managerial decisions on when to launch a new product. While new product release is a key operational area over which executives have much control, no research thus far has examined its role in real earnings management.

Based on analyses of movie release timing in the US motion picture industry, we find that compared to private studios, public studios are more likely to release movies with high expected revenues in the last month of a quarter. This is consistent with the proposition that public studios face stronger performance pressure from the capital market and have stronger incentives to boost quarterly revenues. We further find that public studios are more likely to do so when their recent performance is poor.

We present evidence that studios weigh the costs and benefits of releasing movies with high revenue potential in the last month of a quarter. To minimize the costs of such behaviors, studios are less likely to schedule two types of movies into the last month of a quarter: those with seasonal appeal to audiences and those produced by directors with whom they have worked before. Releasing movies with seasonal appeal outside their optimal release window would result in low customer demand and reduced box office revenues. Rescheduling movies by directors with whom studios have strong working relationships might damage the mutual trust between the studio and the director, hurting long-term opportunities. Our results suggest that a firm’s strategy to manage earnings is influenced by its product characteristics.

Regarding consequences, movies released in the third month of a quarter by public studios have lower international box office revenues, although box office revenues from the domestic market and the overall return on investment are less affected. This finding is consistent with mixed evidence regarding the consequences of real earnings management (since managers take into consideration the potential costs). Managers seem to engage in the real earnings management activities that are the least costly and cause the minimum disruption to their alliance with key business collaborators.

Overall, we provide new evidence on real earnings management at the product level. While our empirical results focus on the movie industry, the implications can apply to new product release decisions in other industries as well. New products not only bring in additional revenues but also help companies to smooth earnings and meet performance targets. We leave it to future research to examine the impact of financial reporting pressure on new product releases in other industries.

Data availability

The data is available from public sources.

Notes

Fiscal quarters coincide with calendar quarters for all of the public studios in our sample.

The box office numbers were calculated data reported in Box Office Mojo The other downstream revenues were calculated using various sources including, https://web.archive.org/web/20120402201834/http://digital.asahi.com/articles/TKY201111020783.html (in Japanese).

After studios announce their release schedule, the actual release date may change, based on each film. There are a variety of reasons for studios to pick release dates in advance. Disney recently put its stake in the ground by announcing that it would release Avatar 5 on December 17, 2027. Whether that becomes the actual release date remains to be seen.

We examined the annual bonus plans of parents of public studios. All of them use cash flows and some form of earnings (EBITDA, EPS, or ROIC). Anecdotal evidence suggests that public studio executives are evaluated on a similar set of performance measures.

Above-the-line talent includes directors, actors, and actresses, who often participate in sharing a movie’s revenue as part of the contract between them and the studio.

For many years, the Paramount Consent Decree prevented studios from owning theaters over antitrust concerns; however, the decree ended in 2020, which was after our sample period.

While there is some overlap between the classification of studios into public vs. private and the distinction between major studios (Paramount Pictures, Warner Bros. Pictures, Walt Disney Pictures, Universal Pictures, and Columbia Pictures) and the mini-majors (e.g., Lionsgate, STX Entertainment, and Amblin Entertainment) and independent studios, there are differences between the two classification schemes. The public/private classification is based on ownership structure. The major/mini-major/independent classification is based on production capacity. For instance, not all public studios are large. Orion Pictures and Vestron, which are relatively small, are public since their parent companies are listed on one of the stock exchanges. On the other hand, one of the mini-major studios, STX Entertainment, remains private during our sample period.

We choose to end our sample period in 2019 because Covid-19 disrupted the movie market significantly. For example, the number of films released in 2020 was only about one-third the number released in 2019. Nevertheless, we examine the impact of the pandemic by extending our sample period to 2021, and our main results remain robust. Our sample does not include movies solely released on streaming platforms, given the lack of streaming revenue data.

In additional tests, we do not find a significant association between release timing and revenues from DVD sales and Blu-Ray sales.

References

Ahearne, M.J., J.P. Boichuk, C.J. Chapman, and T.J. Steenburgh. 2016. Real earnings management in sales. Journal of Accounting Research 54 (5): 1233–1266.

American Institute of Certified Public Accountants (AICPA). 2000. Statement of Position 00-2, Accounting by Producers or Distributors of Films. AICPA.

Baber, W., P. Fairfield, and J. Haggard. 1991. The effect of concern about reported income on discretionary spending decisions: the case of research and development. The Accounting Review 66 (4): 818–829.

Bartov, E., D. Givoly, and C. Hayn. 2002. The rewards for meeting-or-beating earnings expectations. Journal of Accounting and Economics 33 (2): 173–204.

Bereskin, F.L., P.H. Hsu, and W. Rotenberg. 2018. The real effects of real earnings management: Evidence from innovation. Contemporary Accounting Research 35 (1): 525–557.

Beyer, B.D., S.M. Nabar, and E.T. Rapley. 2018. Real earnings management by benchmark-beating firms: Implications for future profitability. Accounting Horizons 32 (4): 59–84.

Bhojraj, S., P. Hribar, M. Picconi, and J. McInnis. 2009. Making sense of cents: An examination of firms that marginally miss or beat analyst forecasts. The Journal of Finance 64 (5): 2361–2388.

Brennan, N.M. 2021. Connecting earnings management to the real world: What happens in the black box of the boardroom? British Accounting Review 53 (6): 1–15.

Brüggen, A., R. Krishnan, and K.L. Sedatole. 2011. Drivers and consequences of short-term production decisions: Evidence from the auto industry. Contemporary Accounting Research 28 (1): 83–123.

Bruns, W.J., and K. Merchant. 1990. The dangerous morality of managing earnings. Management Accounting 72 (2): 22–25.

Burgstahler, D., and I. Dichev. 1997. Earnings management to avoid earnings decreases and losses. Journal of Accounting and Economics 24 (1): 99–126.

Caglio, A., and A. Ditillo. 2008. A review and discussion of management control in inter-firm relationships: Achievements and future directions. Accounting, Organizations and Society 33 (7-8): 865–898.

Chapman, C.J., and T.J. Steenburgh. 2011. An investigation of earnings management through marketing actions. Management Science 57 (1): 72–92.

Cohen, D., A. Dey, and T.Z. Lys. 2008. Real and accrual-based earnings management in the pre– and post–Sarbanes-Oxley periods. The Accounting Review 83 (3): 757–787.

Cohen, D., R. Mashruwala, and T. Zach. 2010. The use of advertising activities to meet earnings benchmarks: Evidence from monthly data. Review of Accounting Studies 15 (4): 808–832.

Cohen, D., S. Pandit, C.E. Wasley, and T. Zach. 2020. Measuring real activity management. Contemporary Accounting Research 37 (2): 1172–1198.

Cohen, D.A., and P. Zarowin. 2010. Accrual-based and real earnings management activities around seasoned equity offerings. Journal of Accounting and Economics 50 (1): 2–19.

Das, S., P.K. Shroff, and H. Zhang. 2009. Quarterly earnings patterns and earnings management. Contemporary Accounting Research 26 (3): 797–831.

Dechow, P., W. Ge, and C. Schrand. 2010. Understanding earnings quality: A review of the proxies, their determinants and their consequences. Journal of Accounting and Economics 50 (2-3): 344–401.

Dechow, P., and C. Shakespeare. 2009. Do managers time securitization transactions for their accounting benefits? The Accounting Review 84 (1): 99–132.

Dechow, P., R. Sloan, and A. Sweeney. 1995. Detecting earnings management. The Accounting Review 70 (2): 193–225.

Dechow, P.M., and I.D. Dichev. 2002. The quality of accruals and earnings: The role of accrual estimation errors. The Accounting Review 77 (s-1): 35–59.

Dechow, P.M., and D.J. Skinner. 2000. Earnings management: reconciling the views of accounting academics, practitioners, and regulators. Accounting Horizons 14 (2): 235–250.

Dhaliwal, D., C. Gleason, and L. Mills. 2004. Last chance earnings management: Using the tax expense to meet analysts’ forecasts. Contemporary Accounting Research 21 (2): 431–459.

Dichev, I.D., J.R. Graham, C.R. Harvey, and S. Rajgopal. 2013. Earnings quality: Evidence from the field. Journal of Accounting and Economics 56 (2-3): 1–33.

Dun and Brudstreet. 2021. Industry Profile: Film & Video. Available at https://www.dnb.com.

Eldenburg, L.G., K.A. Gunny, K.W. Hee, and N. Soderstrom. 2011. Earnings management using real activities: Evidence from nonprofit hospitals. The Accounting Review 86 (5): 1605–1630.

Eliashberg, J., A. Elberse, and M. Leenders. 2006. The motion picture industry: critical issues in practice, current research, and new research directions. Marketing Science 25 (2): 638–661.

Follows, S. (2019) How far in advance are movie release dates announced? Available at: https://stephenfollows.com/how-far-in-advance-are-movie-release-dates-announced/. Accessed 2 Feb 2023.

Fritz, B. 2016. Disney stresses ESPN to allay cable fears; shares of media giant fall amid cable concerns, but ‘star wars’ drives strong quarter. Wall Street Journal February 9: 2016.

Gilchrist, D.S., and E.G. Sands. 2016. Something to talk about: Social spillovers in movie consumption. Journal of Political Economy 124 (5): 1339–1382.

Gong, J.J., and S.M. Young. 2016. Financial and nonfinancial performance measures for managing revenue streams of intellectual property products: The case of motion pictures. Advances in Management Accounting 27: 1–37.

Gong, J.J., S.M. Young, and W.A. Van der Stede. 2011. Real options in the motion picture industry: Evidence from film marketing and sequels. Contemporary Accounting Research 28 (5): 1438–1466.

Graham, J.R., C.R. Harvey, and S. Rajgopal. 2005. The economic implications of corporate financial reporting. Journal of Accounting and Economics 40 (1–3): 3–73.

Grieser, W., C. Hadlock, and J. Pierce. 2021. Doing good when doing well: Evidence on real earnings management. Review of Accounting Studies 26: 906–932.

Gunny, K. 2010. The relation between earnings management using real activities manipulation and future performance: evidence from meeting earnings benchmark. Contemporary Accounting Research 27 (2): 855–888.

Herrmann, D., T. Inoue, and W.B. Thomas. 2003. The sale of assets to manage earnings in Japan. Journal of Accounting Research 41 (1): 89–108.

IBISWorld Inc. (2021). Industry Report 51211A: Movie and Video Production in the US. Available at: https://www.ibisworld.com/united-states/market-research-reports/movie-video-production-industry/. Accessed 2 Feb 2023.

Jackson, S., and W. Wilcox. 2000. Do managers grant sales price reductions to avoid losses and declines in earnings and sales? Quarterly Journal of Business and Economics 39 (4): 3–20.

Jacob, J., and B. Jorgensen. 2007. Earnings management and accounting income aggregation. Journal of Accounting and Economics 43 (2–3): 369–390.

Kerstein, J., and A. Rai. 2007. Intra-year shifts in the earnings distribution and their implications for earnings management. Journal of Accounting and Economics 44 (3): 399–419.

Kothari, S.P., N. Mizik, and S. Roychowdhury. 2016. Managing for the moment: The role of earnings management via real activities versus accruals in SEO valuation. The Accounting Review 91 (2): 559–586.

Luft, J.L. 2021. Six impossible things before breakfast. Journal of Management Accounting Research 33 (3): 1–7.

McKinsey & Company. (2017) How to make sure your next product or service launch drives growth. Available at https://www.mckinsey.com/business-functions/marketing-and-sales/our-insights/how-to-make-sure-your-next-product-or-service-launch-drives-growth. Accessed 2 Feb 2023.

McNichols, M.F. 2000. Research design issues in earnings management studies. Journal of Accounting and Public Policy 19 (4-5): 313–345.

Mizik, N., and R. Jacobson. 2007. Myopic marketing management: Evidence of the phenomenon and its long-term performance consequences in the SEO context. Marketing Science 26 (3): 361–379.

PricewaterhouseCoopers LLP (PwC). (2022) Perspectives from the Global Entertainment & Media Outlook 2022–2026. Available at https://www.pwc.com/gx/en/industries/tmt/media/outlook/outlook-perspectives.html. Accessed 2 Feb 2023.

Ravid, S.A. 1999. Information, blockbusters, and stars: A study of the film industry. The Journal of Business 72 (4): 463–492.

Roychowdhury, S. 2006. Earnings management through real activities manipulation. Journal of Accounting and Economics 42 (3): 335–370.

Sellami, M. 2015. Incentives and constraints of real earnings management: The literature review. International Journal of Finance and Accounting 4 (4): 206–213.

Sheen, A. 2020. Do public and private firms behave differently? An examination of investment in the chemical industry. Journal of Financial and Quantitative Analysis 55 (8): 2530–2554.

Srivastava, A. 2019. Improving the measures of real earnings management. Review of Accounting Studies 24 (4): 1277–1316.

Susarla, A., M. Holzhacker, and R. Krishnan. 2020. Calculative trust and interfirm contracts. Management Science 66 (11): 5465–5484.

Vorst, P. 2016. Real earnings management and long-term operating performance: The role of reversals in discretionary investment cuts. The Accounting Review 91 (4): 1219–1256.

Young, S.M., J.J. Gong, and W.A. Van der Stede. 2009. Value creation and the possibilities for management accounting research in the entertainment sector: the United States motion picture industry. Handbooks of Management Accounting Research 3: 1337–1352.

Zang, A.Y. 2012. Evidence on the trade-off between real activities manipulation and accrual-based earnings management. The Accounting Review 87 (2): 675–703.

Zhao, Y., K. Chen, Y. Zhang, and M. Davis. 2012. Takeover protection and managerial myopia: Evidence from real earnings management. Journal of Accounting and Public Policy 31 (1): 109–135.

Acknowledgement

We have benefitted from constructive comments from the editor (Elizabeth Blankespoor), an anonymous reviewer, and George Foster (Review of Accounting Studies Conference discussant). We also had productive discussions with Alex Nekrasov, Eric Allen, Sabrina Chi, Eva Labro, Matt Shaffer, Jean Ryberg Bradley (discussant at AAA Western Regional Meeting), Bingyi Chen (discussant at Hawaii Accounting Research Conference), Jeppe Christoffersen (discussant at AAA Annual Meeting), Ying Gan (discussant at AAA Western Regional Meeting), and other participants at the AAA Western Regional Meeting (2022), the AAA Annual Meeting (2022), the Hawaii Accounting Research Conference, and the Review of Accounting Studies Conference (2022). We thank Seba Gawenda, Christina Jones, and Lauren Morris for their valuable research assistance. James Gong acknowledges financial support from Moss Adams.

Funding

Open access funding provided by SCELC, Statewide California Electronic Library Consortium

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

There is not any conflict of interest when we conduct the research project.

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Gong, J.J., Young, S.M. & Zhou, A. Real earnings management and the strategic release of new products: evidence from the motion picture industry. Rev Account Stud 28, 1209–1249 (2023). https://doi.org/10.1007/s11142-023-09793-6

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11142-023-09793-6

Keywords

- Real Earnings Management

- Operating Decisions

- New Product Release Decisions

- Cost Capitalization

- Financial Reporting Concerns

- Motion Picture Industry