Abstract

In recent time, Turkey could be said to have experienced different levels of Economic Risk, Financial Risk, and Political Risk from low- to high-level. This study investigates the linkage between country risks, namely Financial Risk, Economic Risk, and Political Risk (FEP risk) in Turkey for the period 1984Q1 to 2019Q1 by using threshold cointegration, Markow-switching regression (given the nonlinearity and structural breaks observed in the time series variables), and frequency domain causality approaches. The empirical findings of this study reveal that (i) nonlinear cointegration between Economic Risk, Financial Risk, and Political Risk in Turkey is statistically significant given the evidence of threshold cointegration test, which determines the structural breaks endogenously; (ii) there is positive linkage among the component of country risk at different volatility periods; (iii) there is a significant Granger causal linkage between Economic Risk, Financial Risk and Political Risk at the different frequency levels. The study is likely to open debate about the literature since the study concludes with a discussion on short-run and long-run implications for economic, political, and financial stabilises, thus offering policy suggestions for the policymakers in Turkey.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Since the global crisis in 1929, researchers have given considerable attention to the impact and consequence of the political, financial, and economic crises. In the relevant economic literature, although numerous empirical and theoretical studies have investigated (i) the nexus between economic growth and finance development and (ii) the effect of political instability on economic growth. However, two-way relationship between country risk components, namely Economic Risk, Financial Risk, and Political Risk is yet to receive considerable attention and especially for the case of Turkey. Although Turkey has continued to experience economic setback in recent times arising from high inflation and currency tumoil, the country experienced significant transformation since the late 1980s by liberalizing their markets, accelerating reforms, the opening of the Turkish economy to liberal trade and adopting modern banking systems. Therefore, the main innovation of the present study is to construct time series-based models to explore the relationship between Economic Risk, Financial Risk, and Political Risk which has not widely been investigated for the case of Turkey especially by exploring more recently developed econometrical tools, namely threshold cointegration, Markow-switching regression and frequency domain causality tests which takes into account structural breaks. Thus, the study is billed to the fill gap in the literature at a timely manner given Turkey’s currency and exchange rate tumoil alongside affirming the appropriateness of the time series-based models. Therefore, by opening a a new debate in the literature, the findings of this investigation expectedly brings out a remarkable suggestion for policymakers in Turkey.

2 Study relevance and literature

The vulnerabilities in the Turkish economy and political environments have encourages researchers to ponder and investigate potential causals and its associated effects. Chronologically, the Turkish economy is dramatically affected by the 1988 stock market and currency crisis, the 1994 economic crisis, the 1998 textile crisis, the 2000 banking crisis, the 2001 economic crisis, the 2007–08 global economic crisis, the 2018 exchange rate crisis. As mentioned previously, in the last decade, Tureky has experienced economic setbacks characterized by rising inflation, currency depreciation among other monetary policy issues, not mentioning the fact that recent development has also shown the country’s vulnerability to political tension. It has witnessed a mass uprising characterized by several protests at Istanbul's Taksim Gezi Park in 2013 and for other reasons such as the local election in March 2014, a presidential election in August 2014, two general elections in June and November 2015, a failed coup attempt in July 2016, the declaration of a state of emergency in that same month, and finally, the April 16, 2017 referendum" (Akcay 2018).

2.1 Related literature

It is widely accepted that vulnerability in the political system is likely to destabilize macroeconomic dynamics. This hypothesis was initially put forward by the study of Olson (1963), which underlined that political stability is a crucial condition for the development and encouragement of entrepreneurs and forecasting a nation's long-term economic performance. Therefore, the scholars- Brunetti (1997), Chen and Feng (1996), Jong-a-Pin (2009), Alesina and Perotti (1996), Darby et al. (2004), Aisen and Veiga (2013)- have constructed ample literature documenting the adverse impact of political uncertainty on macroeconomic dynamics, namely GDP growth, private investment, taxation, public expenditures, and investment, debt, and inflation. Also, the financial system and market are adversely affected by rising political tension in a country. Cutler, Poterba, and Summers (1989) and Hibbs (1986) argue that government policy changes lead to changes in the stock market returns. Pantzalis et al. (2000), Li and Born (2006), and Bialkowski, Gottschalk, and Wisniewski (2008) explored the behaviors of asset prices in the stock markets for the political elections. They concluded that the price of stock market assets is significantly affected by political elections. However, in the literature, the reverse relation has not been comprehensively investigated, including the economic/finance-led politic hypothesis.

Regarding the channels of transmission, Campos and Nugent (2002) argue that slowing down economic development is likely to change governments' structure due to changing the power balance in the government. Thus, political instability in a country might be raised due to the collapse of the government. The finding of Telatar (2003) also supports the argument of Campos and Nugent (2002). By focusing on 122 countries, Milijkovic and Rimal (2008) put it forward that social, economic conditions such as income level lead to changes in the political system. Therefore, political vulnerability is likely to be triggered by a vulnerability in economic growth.

Although numerous empirical and theoretical studies have been explored the nexus between economic growth and financial development in the relevant economic literature, there is no consensus about the direction of the widespread phenomenon of the relationship between financial development and economic growth since the finance-led growth hypothesis put it forward by Schumpeter (1912). In examining the linkage between economy and finance, scholars have mainly tested three different hypotheses, namely "finance lead growth," "growth lead finance", and "feedback," to be able to understand their causal natures. Financial development is the fundamental tool for economic development as financial institutions could accelerate economic growth via improving risk management, making financial transactions, exchanging goods and services, and saving mobility easier (Levine et al. 2000). This hypothesis has been supported by the well- documented studies of King and Levine (1993), Levine et al. (2000), McKinnon (1973), Rajan and Zingales (1998), Galindo et al. (2007), Marashdeh and Al-Malkawi (2014), Cournède and Denk (2015), Cojocaru et al. (2016)-. According to growth led finance hypothesis, a well-functioning financial system is the consequence of economic growth. Robinson (Robinson, 1952) was the pioneer economist who states that finance is not an important factor in the growth process, but economic growth may boost the financial industry. The studies of Shaw and Gurley (1967), Stiglitz (1994), Zang and Kim (2007), Odhiambo (2008), Jenkins and Katircioglu (2010) also underlined the importance of economic growth on financial development. Lastly, the third hypothesis argues that there is a bidirectional causal relationship between financial development and economic growth (Blackburn and Hung 1998; Liang and Jian-Zhou 2006). A few studies also supported the neutrality hypothesis and showed no causal relationship between these two financial and economic growth variables (Lucas 1988; Stern 1989; Nyasha and Odhiambo 2015). Moreso, recent studies have also linked economic policy and its aspects to other socio- and economic indicators such as energy and environment (Anser et al., 2021; Adams et al., 2020; Akadiri et al., 2020).

Exploring the relationship between Economic Risk, Financial Risk, and Political Risk in Turkey is the paper's primary objective. It is crucial for governors, investors and also academics. Still, to the best of our knowledge, specifically, there is no study of Turkey in the literature that have examined the aforementioned relationship especially by using threshold cointegration, Markow-Switching regression, and frequency domain causality tests simultaneously. As its main innovation, the present study constructs a time series-based model to fill this literature gap. The present study is likely to open a new debate in the literature, and the findings bring out the noteworthy implication for governors in Turkey.

3 Data description and methodology

This study employs data sets of Political Risk Index, Economics Risk Index, and Financial Risk Index as variables of concern for Turkey's case. The datasets that span 1984Q1 to 2019Q1 were retrieved from the Political Risk Services (PRS) Group. As indicated below, the categorical description of Political Risk Index, Economics Risk Index, and Financial Risk Index are harmonized explicitly as:

-

The Political Risk Index: "It is a country type of risk associated with the vulnerabilities and changes in the political dynamics or structure of a state. Political risk could be traced to the unusual temperate and uncertainty in government stability, bureaucratic quality, internal and external conflicts, religious and ethnic problems, and others. The PRS Group assesses the Political Risk Index on a scale of 0 (maximum risk) to 100 (minimum risk)."

-

The Economic Risk Index: "it measures the economic weaknesses and strengths, with an assigned value between 0 and 50. While the value 0 corresponds to the highest economic risk, the lowest economic risk is assigned 50. The assessment of the PRS Group is based on the GDP per capita, GDP growth, inflation, and the current account as a percentage of GDP, along with the budget balance as a percentage of GDP variables."

-

The Financial Risk Index: "This measures the country's ability to pay its debts in general. The variable risk range is between 0 (maximum risk) and 50 (minimum risk). The exchange rate, liquidity variables, foreign debt as a percentage of GDP, current account as a percentage of goods and services are among many of the variables utilized in assessing the Financial Risk Index."

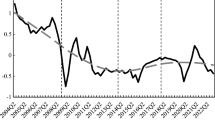

While Table 1 presents the descriptive statistics of the variables of interest and their respective codes, Fig. 1 visually indicates the potential breaks and patterns of the time series variables.

Financial Risk, Economic Risk and Political Risk in TurkeySource: PRS Group

3.1 Methodology

3.1.1 Stationarity and linearity tests

In examining the linkage between country-specific (Turkey) risks vis-à-vis ERI, FRI, and PRI, the approaches of threshold cointegration, Markow-switching regression, and the frequency domain causality tests are employed to advance the studies of Kirikkaleli (2016) and Gokmenoglu, Kirikkaleli, and Eren (2019). Before this, a handful of preliminary tests are performed. To begin with, stationarity test is performed for the variables of interest. Preceding the cointegration mentioned above tests, the Zivot and Andrews (2002) stationarity approach is employed because it accounts for potential evidence of single structural break. In this case, the result of the unit root test with single structural break reveals evidence of as indicated in Table 2. The result implies that there is significant evidence of breaks in 1997Q3 and 2002Q1 for ERI. For FRI and PRI, the significant evidence of single structural break respectively exists in 1993Q2 and 2002Q1 and 1991Q2 and 1992Q4.

Additionally, the portmanteau test which known as the Brock– Dechert–Scheinkman (BDS) test by Brock et al. (1996)Footnote 1 (a detailed procedure is omitted here) is further employed to examine the nonlinear dependency property of the variables. The essence of the test is to confirm the applicability and relevance of using the nonlinear causality approach instead of the linear causality test. In evidence, the BDS test result implies that the null hypothesis that the investigated series is an iid process is rejected. Thus there is a nonlinear dependency for all the series (see Table 3). Consequently, the investigation proceeds to apply the nonlinear cointegration techniques.

3.1.2 The cointegration tests

Considering the nonlinearity evidence from the BDS test (from Table 3 above), the threshold cointegration test with one regime shift is performed by employing Gregory-Hansen Cointegration Test (Gregory and Hansen, 1996). The evidence of nonlinearity due to potential structural changes, therefore, causing the cointegration vector to shift. Hence, these changes could be due to technological shocks or regime changes. Given that the Engle and Granger (1987) investigates the linear combination of variables (y1 = dependent variable and y2 = independent variable) by obtaining the residuals for the standards model from

where \(y_{1t}\) is I (1), for i = 1, 2, and \(e_{t}\) is I (0), it is further modified by Gregory and Hansen (1996). In so doing, Gregory and Hansen (1996) adjust the intercept (\(\mu\)) and/or the slope (\(\alpha\)) such that the modified residual-based cointegration test now allows for structural changes. Then, the adjustments proposed by Gregory and Hansen (1996) present; the shift of the intercept (as in Eq. 2), the shift of the intercept with time trend (as in Eq. 3), and the shift in the intercept slope (as in Eq. 4). The modified equations are presented as

such that the i = 1, 2 of \(\mu\) is the respective periods before and after the regime shift, \(\alpha\) is the slope coefficient, \(\beta_{t}\) is the time trend, and \(\varphi_{t\tau }\) is the introduced dummy variable where \(\varphi_{t\tau }\) = 1 if t \(\ge\) \(\left[ {n\tau } \right]\) or \(\varphi_{t\tau }\) = 0 if t ˂ \(\left[ {n\tau } \right]\) and \(\tau\) ε\(\left(0, 1\right)\). Hence, the null hypothesis of no cointegration is examined by observing the residuals of the Ordinary Least Square (OLS) of Eqs. 2–4, and the single break date in each is endogenously determined. In this case, each of the variables, ERI, FRI, and PRI, is employed as a function of the other two variables in three unique models (see Table 4). The ADF test statistics are also employed to examine the significance of the break date, which is a key advantage of the Gregory and Hansen (1996) approach. The result, as presented in Table 4, shows that the null hypothesis of no cointegration is rejected in each of the models for one regime shift where the data is truncated by 15% on each side, i.e. (\(\tau\) = (0.15, 0.85)).

Similarly, Hatemi-J's (2008) 's approach that allows for two (regime) structural shifts during the time period is further employed. Hence, this approach offers the suitability of accounting for the two structural breaks on both the intercept and the slopes in place of one regime shift by Gregory and Hansen's (1996) approach. Although the detail and step-by-step procedure of the Hatemi-J (2008)Footnote 2 are not provided here, the result of the estimate and especially for each model (each variable as a function of the other two) as applied above, is also provided in Table 4. The null hypothesis of no cointegration is rejected in all the cases, thus showing that there is statistical evidence of cointegration even with two regime shifts.

3.1.3 Markov switching regression and frequency domain causality

Given that the investigation reveals statistically significant evidence of cointegration in two regime shifts, the robustness is further investigated by employing the Markov-switching regression of Hamilton (1989) approach. A multivariate approach model such that the ordinary least squares (OLS) regression model is first implemented as

where t is the quarterly periods, \(\varepsilon_{t}\) is the error term, and slope parameter to be estimated (\(\widehat{\beta }\)) for each corresponding independent variable. Also, the estimation of Eq. 5 (Model A) is repeated as Eq. 6 (Model B) and Eq. 7 (Model C), where FRI and PRI are respectively the dependent variable in each case, as indicated below

Given that for all \(\mathop \varepsilon \nolimits_{t} \sim N(0,\mathop \sigma \nolimits_{st}^{2} )\), the switching intercept and variance of error are respectively \(\mathop \beta \nolimits_{0,i,rt}\) and \(\mathop \sigma \nolimits_{st}^{2}\). Also, each of the independent variables on the dependent variable in each of the models (A, B, and C) and different regimes are respectively \(\mathop \beta \nolimits_{1,i,rt}\) and \(\mathop \beta \nolimits_{2,i,rt}\) where rt (regime dependent) is a discrete regime variable. In addition, the latent unobserved state variable, i = 1 and 2 such that state one and state 2 (state of the economy) are respectively known as the high and low regimes as indicated in Table 5. The results illustrating the statistical evidence of the (2) regime shifts as shown in Table 5 offers robustness to the nonlinear cointegration evidence earlier implied in the previous cointegration tests.

Additionally, the frequency domain Granger causality test is employed to provide a robustness check to the previous estimates. Following the earlier works of Geweke (1982) and Hosoya (1991), Breitung and Candelon (2006) advanced and developed the frequency domain causality approach. The Breitung and Candelon (BC) (2006) approach provides a specific degree of variation, unlike the time-domain approach, which only offers the period of variation. Hence, the method is robust to seasonal variation and provides information from nonlinearity and causality cycles (i.e., low or high frequency). The stepwise procedure of the BC approach is detailed below:

Given a three-dimensional vector \(X_{t}\) = [\(ERI_{t} , FRI_{t,} PRI_{t}\)] of endogenous and stationary variables where time t = 1, …, T, then \(X_{t}\) is assumed to have a finite-order VAR representation of the form

where, \(\Theta \left( L \right)\) is a 3 by 3 lag polynomial of order p which is presented as, \(\Theta \left( L \right)\) = \(I\) – \({\Theta }_{1} L^{1}\)−⋯−\({\Theta }_{p} L^{p}\) with \(L^{k} X_{t}\) = \(X_{t - k}\). The \({\upvarepsilon }_{{\text{t}}}\) follows the white noise process with an expectation of zeros and \(\left({\varepsilon }_{t}{\varepsilon }_{t}^{^{\prime}}\right)=\Sigma\), where \(\Sigma\) is positive and symmetric. The suitability and ease of implementing the Breitung and Candelon (2006) are also that no deterministic terms are added to the Eq. 8 above. Since \(\Sigma\) is positive definite and symmetric, it then offers Cholesky decomposition such as\({G}^{^{\prime}}G= {\Sigma }^{-1}\), where \(G\)= lower triangular matrix and \({G}^{^{\prime}}\) = upper triangle matrix. Also, \(E\left({\upeta }_{t}{\upeta }_{t}^{^{\prime}}\right)=I\) and\({\upeta }_{t}=G{\varepsilon }_{t}\). In this case, the Cholesky decomposition, the MA representation of the system is given as:

If \(\Phi \left( L \right) = \Theta \left( L \right) ^{ - 1}\), then \(\Psi \left( L \right) = \Phi \left( L \right)G^{ - 1}\). Consequently, the spectral density of \(ERI_{t}\) can be expressed as

The sum of two uncorrelated MA processes is represented by Eqs. 9 and 10 above. The components are driven by the past realization of ERI and the predictive power of the FRI and PRI variables. The predictive power of the FRI and PRI variables are formulated from each frequency \({{\varvec{\upomega}}}\) in relation to the predictive component of the spectrum with the intrinsic component at that frequency. The approach of Breitung and Candelon (2006) offers a null hypothesis of no Granger causality i.e. X variable does not granger cause Y variable at frequency \({\varvec{\upomega}}\) if the predictive factor of the Y variable spectrum at frequency \({{\varvec{\upomega}}}\) is zero which is indicated by the causality tests of Geweke (1982) and Hosoya (1991) provided below

Also, according to Geweke (1982), the measure of causality will be zero when \(\left| {{\Psi }_{12} \left( {e^{{ - i{\upomega }}} } \right)} \right|^{2} = 0\). However, Geweke (1982) offered a simplified liner restriction on the VAR of Eq. 1 such that

where αi and βi (i = 1, 2, …, p) are the coefficients of the lag polynomials.

Therefore, the null hypothesis \({\text{ M}}_{{{\text{ERIFRI}}}} \left( {\upomega } \right) = 0\) is equivalent to the linear restriction such that,

where \({\upbeta } = \left[ {{\upbeta }_{1} ,{ } \ldots ,{\upbeta }_{{\text{p}}} } \right]{^{\prime}}\) is the vector of the coefficients of ERI, while \({\text{R}}\left( {\upomega } \right)\) is as follow;

The ordinary F statistic for the above VAR model of order p representation is approximately distributed as F (2, T—2p) for \(\upomega\) є (0, π), where 2 is the number of restrictions and T is the number of observations. The above test results that offer significant evidence of causality and robustness to the previous estimations are provided in Fig. 2.

The Frequency Domain Causality Test of Breitung and Candelon (2006) Note: denotes the direction of the causality

4 Results and discussion

From each of the above estimations, additional information is provided supporting the statistical evidence of causal linkage of economic risk index, financial risk index, and the political risk index. The descriptive statistics (see Table 1) inform that the series ERI and FRI are not normally distributed while evidence of normal distribution is observed for the PRI. While ERI and FRI are negatively skewed, the PRI series is skewed to the right (positive skewness). The result of the Zivot-Andrew unit root test, as provided in Table 2, shows that the series are all not stationary at level. Hence, the series are all stationary after first difference (i.e. I (0)). There is substantial and statistical evidence that the structural break could have influenced the stationarity property with significant break dates. The economic risk index's observed break period is 2002Q1, 1993Q2, and 2002Q1 for the financial risk index, then 1991Q2 and 1992Q4 for the political risk index. The break periods 1991Q2 and 2002Q1 coincide with Turkey's general election years (Çancı and Şen, 2011).

Notably, the significant evidence of nonlinearity was preliminarily investigated and affirmed by the BDS test, thus paving the way to explore cointegration among the variables of interest. In doing this, the implemented Gregory and Hansen (1996) approach reveals evidence of cointegration in the three models adopted (see Table 4). The significant evidence of cointegration among the ERI, FRI, and PRI did not only support the results of previous studies (Kirikkaleli, 2016; Gokmenoglu, Kirikkaleli, and Eren, 2019) but in indeed suggests that the effects of risk associated with the economic, financial, and political indicators are expectedly inter-woven. Similarly, the cointegration result offered by Hatemi-J (2008), as indicated in Table 4, further affirms that there exists statistical evidence of nonlinear cointegration. The proof of cointegration provided by the two approaches employed (Gregory and Hansen 1996; Hatemi-J, 2008) implies that cointegration among the ERI, FRI, and the PRI is independent of the specificity of the dependent variable.

Moreover, a robustness check is being offered by implementing the Markov-switching regression approach of Hamilton (1989) and the frequency domain causality approach by Breitung and Candelon (2006). From the Markov-switching result in Table 5; there is significant evidence of regime-switching between low volatility and high volatility in the three models employed except in the low volatility regime where the intercept of the regime shift is not significant. In the first model (i.e., ERI as a function of FRI and PRI), FRI and PRI are observed to positively impact ERI in regime 1 (high volatility period). In contrast, only PRI exerts a positive effect on the ERI in the second regime (low volatility). In the second model (FRI as a function of ERI and PRI), both ERI and PRI exert a significant and positive impact on the FRI in the second regime (low volatility period). Simultaneously, only ERI is observed to exert a substantial and positive influence on the FRI in the first period (high volatility period). In the last model (PRI as a function of ERI and FRI), both ERI and FRI exerts a significant and positive impact on the PRI in period 2 (low volatility period). Still, only the effect of FRI on PRI is significant and positive in period 1 (high volatility period). In general, the results indicate that ERI, FRI, and the PRI are largely driven by one another, especially in the same direction. Similarly, the visual information provided by the Breitung and Candelon (2006) test in Fig. (2) implies that (red) upper lines and the (brownish) lower lines respectively represent the 5% and 10% statistically significant level.

On the other hand, the (bluish) curves indicate the statistical tests at different frequencies between the intervals of (0, П). Hence, statistically significant and evidence of Granger causality between the various combinations of the variables are provided except FRI to ERI. It does imply that the no Granger causality hypothesis from FRI to ERI under the specified frequency domain is not rejected. However, there exist Granger causality among the other pairs of combination as observed in Fig. 2.

5 Conclusion and policy implication

Since Schumpeter's pioneer study (1912), the linkage between economic growth and financial development has been given considerable attention by researchers, despite there is no consensus about the relationship's direction. The effect of political uncertainty on the financial and economic dynamics is one of the most intensely studied issues in the literature. However, there is a lack of empirical studies for emerging markets about the linkage between economic, political, and financial dynamics. Since investors and policymakers need to explore the link between economic, financial, and political risks, the present study aims to fill this gap in the literature for Turkey's case using the threshold cointegration Markow-switching regression and frequency domain causality tests. The present research focuses on a period 1984Q1 to 2019Q1, which involves multiple domestic and global vulnerabilities in economic, financial, and political environments. As an emerging market, Turkey faced different economic, financial and political vulnerabilities from low level and high level, to identify linkage between economic, financial and political risks became more interesting.

This study's empirical findings reveal that significant nonlinear cointegration between Economic Risk, Financial Risk and Political Risk is observed in Turkey using threshold cointegration test, which determines the structural breaks endogenously. This indicates long-run relationships between sets of time series variables, namely economic, financial and political risks. The Markow-Switching Regression outcomes show that there is a positive linkage among the risks at different volatility periods, meaning that economic, financial, and political stabilities in Turkey positively affect each other. The outcome of the frequency domain causality test of Breitung and Candelon (2006) reveals for the case of Turkey that there is feedback causality between Economic Risk, Financial Risk, and Political Risk at the different frequency levels.

As a result of newly developed econometrics techniques, it can be concluded that if governors in Turkey aim to minimize political risk, then their attention should be focused on achieving financial and economic stabilities. Moreover, to control macroeconomic dynamics, vulnerabilities in political and financial environments should be minimized. Lastly, to avoid the vulnerability in exchange rate, liquidity, and public debt, Turkey's governors consider kee** their political and economic environment stable. The study likely to open debate about the literature since the study concludes with a discussion on short-run and long-run implications for economic, political, and financial stabilises while providing policy suggestions for the policymakers in Turkey.

Data availability

Not Applicable

Notes

Details and step-to-step procedure for the non-linearity test (BDS) is provided in Broock, W. A., Scheinkman, J. A., Dechert, W. D., & LeBaron, B. (1996). A test for independence based on the correlation dimension. Econometric reviews, 15(3), 197–235.

References

Adams, S., Adedoyin, F., Olaniran, E., Bekun, F.V.: Energy consumption, economic policy uncertainty and carbon emissions; causality evidence from resource rich economies. Economic Anal. and Policy 68, 179–190 (2020)

Aisen, A., Veiga, F.J.: How does political instability affect economic growth? Eur. J. Polit. Econ. 29, 151–167 (2013)

Akadiri, S.S., Alola, A.A., Uzuner, G.: Economic policy uncertainty and tourism: evidence from the heterogeneous panel. Curr. Issue Tour. 23(20), 2507–2514 (2020)

Akcay, Ü (2018). Neoliberal populism in Turkey and its crisis. No. 100/2018. Working Paper, Institute for International Political Economy Berlin,

Alesina, A., Perotti, R.: Income distribution, political instability, and investment. Eur. Econ. Rev. 40, 1203–1228 (1996)

Anser, M.K., Syed, Q.R., Lean, H.H., Alola, A.A., Ahmad, M.: Do economic policy uncertainty and geopolitical risk lead to environmental degradation? Evidence from Emerg. Econ. Sustainability 13(11), 5866 (2021)

Białkowski, J., Gottschalk, K., Wisniewski, T.P.: Stock market volatility around national elections. J. Bank. Finance 32(9), 1941–1953 (2008)

Blackburn, K., Hung, V.T.Y.: A theory of growth, financial development and trade. Economica 65(257), 107–124 (1998)

Breitung, J., Candelon, B.: Testing for short-and long-run causality: a frequency-domain approach. J. Econom. 132(2), 363–378 (2006)

Broock, W.A., et al.: A test for independence based on the correlation dimension. Economet. Rev. 15, 197–235 (1996)

Brunetti, A.: Political variables in cross-country growth analysis. J. Econ. Survey 11, 163–190 (1997)

Campos, N.F., Nugent, J.B.: Who is afraid of political instability? J. Dev. Econ. 67, 157–172 (2002)

Çancı, H, and Şevket Serkan Şen (2011) "The Gulf War and Turkey: Regional Changes and their Domestic Effects (1991–2003)" International Journal on World Peace, 41–65.

Chen, B., Feng, Yi.: Some political determinants of economic growth: theory and empirical implications. Eur. J. Polit. Econ. 12, 609–627 (1996)

Cojocaru, L., Falaris, E.M., Hoffman, S.D., Miller, J.B.: Financial system development and economic growth in transition economies: New empirical evidence from the CEE and CIS countries. Emerg. Mark. Financ. Trade 52, 223–236 (2016)

Cournède, B., and Oliver D.,(2015) "Finance and economic growth in OECD and G20 countries." Available at SSRN 2649935

Cutler, D.M., Poterba, J.M., Summers, L.H.: What moves stock prices? J. Portfolio Manage. 15(3), 4–12 (1989). https://doi.org/10.3905/jpm.1989.409212

Darby, J., Li, C.-W., Anton Muscatelli, V.: Political uncertainty, public expenditure and growth. Eur. J. Polit. Econ. 20, 153–179 (2004)

Engle, Robert F., and Clive WJ Granger. (1987). "Co-integration and error correction: representation, estimation, and testing." Econometrica: journal of the Econometric Society : 251–276.

Galindo, A., Schiantarelli, F., Weiss, A.: Does financial liberalization improve the allocation of investment?: Micro-evidence from develo** countries. J. Dev. Econ. 83, 562–587 (2007)

Geweke, J.: Measurement of linear dependence and feedback between multiple time series. J. Am. Stat. Assoc. 77(378), 304–313 (1982)

Gokmenoglu, K., Kirikkaleli, D., & Eren, B. M.: Time and frequency domain causality testing: The causal linkage between FDI and economic risk for the case of Turkey. J. Int. Trade Econ. Dev. 28(6), 649–667 (2019). https://doi.org/10.1080/09638199.2018.1561745

Gregory, A.W., Hansen, B.E.: Practitioners corner: tests for cointegration in models with regime and trend shifts. Oxford Bull. Econ. Stat. 58, 555–560 (1996)

Gurley, J.G., Shaw, E.S.: Financial structure and economic development. Econ. Dev. Cult. Change 15, 257–268 (1967)

Hamilton, J. D.: A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica: J. Econ. Soc. 57(2), 357–384 (1989). https://doi.org/10.2307/1912559

Hatemi-j, A.: Tests for cointegration with two unknown regime shifts with an application to financial market integration. Empirical Economics 35, 497–505 (2008)

Hibbs, D.A.: Political parties and macroeconomic policies and outcomes in the United States. Am. Econ. Rev. 76, 66–70 (1986)

Hosoya, Y.: The decomposition and measurement of the interdependency between second-order stationary processes. Probab. Theory Relat. Fields 88, 429–444 (1991)

Jenkıns, H.P., Katırcıoglu, S.T.: The bounds test approach for cointegration and causality between financial development, international trade and economic growth: the case of Cyprus. Appl. Econ. 42, 1699–1707 (2010)

Jong-A-Pin, R.: On the measurement of political instability and its impact on economic growth. Eur. J. Polit. Econ. 25, 15–29 (2009)

King, R.G., Levine, R.: Finance and growth: Schumpeter might be right. Q. J. Econ. 108, 717–737 (1993)

Kirikkaleli, D.: Interlinkage between economic, financial, and political risks in the Balkan countries: Evidence from a panel cointegration. East. Eur. Econ. 54, 208–227 (2016)

Levine, R., Loayza, N., Beck, T.: Financial intermediation and growth: Causality and causes. J. Monet. Econ. 46, 31–77 (2000)

Li, J., Born, J.A.: Presidential election uncertainty and common stock returns in the United States. J. Financial Res. 29, 609–622 (2006)

Liang, Qi., Jian-Zhou, T.: Financial development and economic growth: Evidence from China. China Econ. Rev. 17, 395–411 (2006)

Lucas, R.: On the mechanics of economic development. J. Monet. Econ. 22, 3–42 (1988)

Marashdeh, H.A., Al-Malkawi, H.-A.: Financial deepening and economic growth in Saudi Arabia. J. Emerging Market Finance 13, 139–154 (2014)

McKinnon, Ronald I. (1973) "Money and capital in economic development (Washington, DC: Brookings Institution, 1973)." McKinnonMoney and Capital in Economic Development1973.

Miljkovic, D., Rimal, A.: The impact of socio-economic factors on political instability: A cross-country analysis. J. Socio-Econ. 37, 2454–2463 (2008)

Nyasha, S., Odhiambo, N.M.: The impact of banks and stock market development on economic growth in South Africa: an ARDL-bounds testing approach. Contemporary Economics 9, 93–108 (2015)

Odhiambo, N.M.: Financial depth, savings and economic growth in Kenya: A dynamic causal linkage. Econ. Model. 25, 704–713 (2008)

Olson, M.: Rapid growth as a destabilizing force. J. Econ. Hist. 23, 529–552 (1963)

Pantzalis, C., Stangeland, D.A., Turtle, H.J.: Political elections and the resolution of uncertainty: the international evidence. J. Bank. Finance 24, 1575–1604 (2000)

Rajan, R., Zingales, L.: Financial development and growth. Am. Econ. Rev. 88, 559–586 (1998)

Robinson, J.: The model of an expanding economy. Econ. J. 62(245), 42–53 (1952) https://doi.org/10.2307/2227172

Schumpeter, J A. (1912) "Theorie der Wirtschaftlichen Entwicklung. Leipzig: Dunker & Humblot." The theory of economic development.

Stern, N.: The economics of development: a survey. Econ. J. 99(397), 597–685 (1989)

Stiglitz, J.E.: Economic growth revisited. Ind. Corp. Chang. 3, 65–110 (1994)

Telatar, F. (2003). "Türkiye''de Enflasyon, Enflasyon Belirsizliği Ve Siyasi Belirsizlik Arasındaki Nedensellik İlişkileri." İktisat İşletme ve Finans 18.203: 42-51.

Zang, H., Kim, Y.C.: Does financial development precede growth? Robinson and Lucas might be right. Appl. Econ. Lett. 14, 15–19 (2007)

Zivot, E., Andrews, D.W.K.: Further evidence on the great crash, the oil-price shock, and the unit-root hypothesis. Journal of Business & Economic Statistics 20, 25–44 (2002)

Funding

Open Access funding provided by University of Vaasa (UVA). Not Applicable

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

Authors declare that there is no known competing financial interests or personal relationship that could have influenced the study.

Consent to participate

Not Applicable.

Consent to publish

Not Applicable.

Ethical approval

Not Applicable.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Kirikkaleli, D., Alola, A.A. The regime switching evidence of financial-economic-political risk in Turkey. Qual Quant 57, 3747–3762 (2023). https://doi.org/10.1007/s11135-022-01529-z

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11135-022-01529-z