Abstract

The Diamond paradox demonstrates that when learning prices is costly for consumers, each firm has market power. However, making firms privately informed about their quality and cost restores competitive pricing if quality and cost are negatively correlated. Such correlation arises from, e.g. regulation, differing equipment or skill, or economies of scale. If good quality firms have lower costs, then they can signal quality by cutting prices, in which case bad quality firms must cut prices to retain customers. This price-cutting race to the bottom ends in an equilibrium in which all firms price nearly competitively and cheap talk reveals quality.

Similar content being viewed by others

Notes

Nelson et al. (2009) find that among medical innovations, cost reduction is positively correlated with quality improvement. Bloom et al. (2013) show that better management practices cause higher quality, profit and TFP, thus lower unit cost. Among mutual funds, Gil-Bazo and Ruiz-Verdú (2009) show not just a correlation, but that higher fees even predict lower future before-fee returns. Olbrich and Jansen (2014) find negative correlation of price and quality among private label foods, Caves and Greene (1996) for 55 out of 196 product categories, Bartelink (2016) for public tender offers, Reuter and Caulkins (2004) for street heroin. Sheen (2014) shows that larger firms have both higher quality and lower price.

If prices are chosen from a discrete grid (as in reality: one cent increments), then a good quality firm sets price strictly below the bad in equilibrium, and cheap talk can be dispensed with.

The cheap talk is needed for types to separate when they both price at the marginal cost of the bad type. Otherwise equilibrium does not exist, unless prices are restricted to a discrete grid. The proof is in an earlier version of this paper, available on https://sanderheinsalu.com/.

This is a special case of the optional monitoring defined in Miyahara and Sekiguchi (2013).

The indicator function 1\(\left\{ X\right\} \) equals 1 if condition X holds, and 0 otherwise.

The discrete drop of belief is due to discrete types. The results are robust to a continuum of types.

Uniqueness is up to permutation of the cheap talk messages. Formally, there are two equilibria: in one, each type \(\theta \) sends message \(t_{\theta }=\theta \); in the other, each \(\theta \) sends \(t_{\theta }\ne \theta \).

The range is the nonempty open set of parameters defined by \(h(v)\ge v\), \(h'\ge 1\), \(h(\overline{v})<\infty \), \(s\le \mu _0 (h(c_{B})-c_{B})\), \(c_{B}\ge h(0)>0\) and \(\frac{\mathrm{d}}{\mathrm{d}P}P[1-F_v(h^{-1}(P))]>0\) for \(P\in [0,c_{B}+\epsilon ]\).

The robustness checks and extensions mentioned here are covered in greater detail in an earlier version of this paper, available on https://sanderheinsalu.com/.

References

Anderson, S .P., Renault, R.: Pricing, product diversityand search costs: a Bertrand–Chamberlin–Diamond model. RAND J. Econ. 30(4), 719–735 (1999)

Bagwell, K., Ramey, G.: The Diamond paradox: a dynamic resolution. Discussion paper 1013 (1992)

Bartelink, J.A.: Price-quality correlation in tenders. B.S. thesis, University of Twente (2016)

Benabou, R.: Search market equilibrium, bilateral heterogeneity, and repeat purchases. J. Econ. Theory 60, 140–158 (1993)

Bloom, N., Eifert, B., Mahajan, A., McKenzie, D., Roberts, J.: Does management matter? Evidence from India. Q. J. Econ. 128(1), 1–51 (2013)

Burdett, K., Judd, K.L.: Equilibrium price dispersion. Econometrica 51(4), 881–894 (1983)

Butters, G.R.: Equilibrium distributions of sales and advertising prices. Rev. Econ. Stud. 44, 465–491 (1977)

Caves, R.E., Greene, D.P.: Brands’ quality levels, prices, and advertising outlays: empirical evidence on signals and information costs. Int. J. Ind. Organ. 14(1), 29–52 (1996)

Cho, I.-K., Kreps, D.M.: Signaling games and stable equilibria. Q. J. Econ. 102(2), 179–221 (1987)

Daughety, A.F., Reinganum, J.F.: Competition and confidentiality: signaling quality in a duopoly when there is universal private information. Games Econ. Behav. 58(1), 94–120 (2007)

Daughety, A.F., Reinganum, J.F.: Imperfect competition and quality signalling. RAND J. Econ. 39(1), 163–183 (2008)

Diamond, P.A.: A model of price adjustment. J. Econ. Theory 3, 156–168 (1971)

Gil-Bazo, J., Ruiz-Verdú, P.: The relation between price and performance in the mutual fund industry. J. Finance 64(5), 2153–2183 (2009)

Heinsalu, S.: Price competition with uncertain quality and cost. Working paper (2019)

Janssen, M.C., Roy, S.: Signaling quality through prices in an oligopoly. Games Econ. Behav. 68, 192–207 (2010)

Janssen, M.C., Roy, S.: Competition, disclosure and signalling. Econ. J. 125(582), 86–114 (2015)

Kihlstrom, R.E., Riordan, M.H.: Advertising as a signal. J. Polit. Econ. 92(3), 427–450 (1984)

Klemperer, P.: Markets with consumer switching costs. Q. J. Econ. 102, 375–394 (1987)

Miyahara, Y., Sekiguchi, T.: Finitely repeated games with monitoring options. J. Econ. Theory 148(5), 1929–1952 (2013)

Nelson, A.L., Cohen, J.T., Greenberg, D., Kent, D.M.: Much cheaper, almost as good: decrementally cost-effective medical innovation. Ann. Intern. Med. 151(9), 662–667 (2009)

Olbrich, R., Jansen, H.C.: Price-quality relationship in pricing strategies for private labels. J. Prod. Brand Manag. 23(6), 429–438 (2014)

Poeschel, F.G.: Why do employers not pay less than advertised? directed search and the diamond paradox. Working paper, OECD (2018)

Reuter, P., Caulkins, J.P.: Illegal ‘lemons’: price dispersion in cocaine and heroin markets. Bull. Narc. 56(1–2), 141–165 (2004)

Robert, J., Stahl, D .O.: Informative price advertising in a sequential search model. Econ. J. Econ. Soc. 61(3), 657–686 (1993)

Salop, S., Stiglitz, J.: Bargains and ripoffs: a model of monopolistically competitive price dispersion. Rev. Econ. Stud. 44(3), 493–510 (1977)

Salop, S., Stiglitz, J.: The theory of sales: a simple model of equilibrium price dispersion with identical agents. Am. Econ. Rev. 72(5), 1121–1130 (1982)

Sengupta, A.: Competitive investment in clean technology and uninformed green consumers. J. Environ. Econ. Manag. 71, 125–141 (2015)

Sheen, A.: The real product market impact of mergers. J. Finance 69(6), 2651–2688 (2014)

Shieh, S.: Incentives for cost-reducing investment in a signalling model of product quality. RAND J. Econ. 24(3), 466–477 (1993)

Simester, D.: Signalling price image using advertised prices. Market. Sci. 14(2), 166–188 (1995)

Spence, M.: Job market signaling. Q. J. Econ. 87(3), 355–374 (1973)

Spulber, D.F.: Bertrand competition when rivals’ costs are unknown. J. Ind. Econ. 43(1), 1–11 (1995)

Stahl, D.O.: Oligopolistic pricing with heterogenous consumer search. Int. J. Ind. Organ. 14, 243–268 (1996)

Wildenbeest, M.R.: An empirical model of search with vertically differentiated products. RAND J. Econ. 42(4), 729–757 (2011)

Wolinsky, A.: True monopolistic competition as a result of imperfect information. Q. J. Econ. 101(3), 493–511 (1986)

Zhou, J.: Multiproduct search and the joint search effect. Am. Econ. Rev. 104(9), 2918–39 (2014)

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The author would like to thank Larry Samuelson, George Mailath, Gabriel Carroll, Gabriele Gratton, Jack Stecher, David Frankel, Simon Anderson, Idione Meneghel, Vera te Velde, Andrew McLennan, Rakesh Vohra, Rohit Lamba and the audiences at the conferences SAET (Taipei, 11–13 June 2018), ESAM (Auckland, 1–4 July 2018) and CEA (Banff, 31 May–2 June 2019) and at Monash University; the University of Melbourne; Aalto University; the University of Tartu; the University of California, San Diego; the University of California, Los Angeles; Yale University; the University of Toronto and the University of Alberta for their comments and suggestions.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Appendices

Equilibrium definition and existence

A consumer’s posterior belief about firm i after observing its price P and message t and expecting the firm to choose strategy \(\sigma _i^*\) is

whenever the denominator is positive. A discontinuity of height \(h_{\theta }\) in the cdf \(\sigma _i^{\theta *}\) is interpreted in the pdf as a Dirac \(\delta \) function times \(h_{\theta }\). Therefore, an atom in \(\sigma _i^{G*}(\cdot ,t)\), but not \(\sigma _i^{B*}(\cdot ,t)\) at P results in \(\mu _i(P,t)=1\), and an atom in \(\sigma _i^{B*}(\cdot ,t)\), but not \(\sigma _i^{G*}(\cdot ,t)\) yields \(\mu _i(P,t)=0\). If \(\sigma _{i}^{\theta *}\) has an atom of size \(h_{\theta }\) at P for \(\theta \in \left\{ G,B\right\} \), then \(\mu _i(P,t)=\frac{\mu _0h_{G}}{\mu _0h_{G}+(1-\mu _{0})h_{B}}\). Finally, if the denominator of (1) is zero, then belief is arbitrary.

The demand that firm i expects at price P and message t given the expected strategies of firm j and the consumers is

The first term in (2) reflects the consumers initially at i who buy immediately. The second term describes consumers who buy from i after learning both prices and messages, which consists of (the first term in the curly braces) consumers at i who learn and then buy from i and (the second term in the braces) the consumers initially at j who learn and then buy from i.

Denote \(\mu _0d\sigma _j^{G*}(P_{j},t_{j}) +(1-\mu _0)d\sigma _j^{B*}(P_{j},t_{j})\) by \(d\sigma _j^{\mu _0*}(P_{j},t_{j})\), and recall \(w(v,i,P,t):=\mu _i(P,t)h(v)+(1-\mu _i(P,t))v-P\).

Definition 1

An equilibrium consists of \(\sigma _{X}^*,\sigma _{Y}^*,\sigma _1^*,\sigma _2^*\) and \(\mu _{X},\mu _{Y}\) satisfying the following for \(\theta \in \left\{ G,B\right\} \), \(v\in [0,\overline{v}]\), \(i,j\in \left\{ X,Y\right\} \), \(i\ne j\):

-

(a)

if \(w(v,i,P_{i},t_{i})\ge \max \left\{ 0,\;w(v,j,P_{j},t_{j})\right\} \), then \(\sigma _2^*(v,P_{i},P_{j},t_{i},t_{j})(b_i)=1\), and if in addition \(w(v,i,P_{i},t_{i})> w(v,j,P_{j},t_{j})\), then \(\sigma _2^*(v,P_{j},P_{i},t_{j},t_{i})(b_i)=1\),

-

(b)

if \(\max \left\{ w(v,i,P_{i},t_{i}),\; w(v,j,P_{j},t_{j})\right\} <0\), then \(\sigma _2^*(v,P_{i},P_{j},t_{i},t_{j})(n_{\ell })=1\),

-

(c)

if \(w(v,i,P_{i},t_{i})> \max \{0,\; \int _{0}^{\infty }\sum _{t_{j}\in \left\{ G,B\right\} }\max \{w(v,i,P_{i},t_{i}),\;w(v,j,P_{j},t_{j})\}\mathrm{d}\sigma _j^{\mu _0*}(P_{j},t_{j}) -s\}\), then \(\sigma _1^*(v,P_{i},t_{i})(b)=1\),

-

(d)

if \(w(v,i,P_{i},t_{i})\le \int _{0}^{\infty }\sum _{t_{j}\in \left\{ G,B\right\} }\max \{0,\;w(v,i,P_{i},t_{i}),\;w(v,j,P_{j},t_{j})\}\mathrm{d}\sigma _j^{\mu _0*}(P_{j},t_{j}) -s\ge 0\), then \(\sigma _1^*(v,P_{i},t_{i})(\ell )=1\),

-

(e)

if \(\max \{w(v,i,P_{i},t_{i}),\; \int _{0}^{\infty }\sum _{t_{j}\in \left\{ G,B\right\} }\max \{0,\;w(v,j,P_{j},t_{j})\}\mathrm{d}\sigma _j^{\mu _0*}(P_{j},t_{j}) -s\}< 0\), then \(\sigma _1^*(v,P_{i},t_{i})(n)=1\),

-

(f)

if \((P_{i},t_{i})\) is in the support of \(\sigma _i^{\theta *}\), then \((P_{i},t_{i})\in \arg \max _{P,t} (P-c_{\theta })D_i(P,t)\), where \(D_i(P,t)\) is given by (2),

-

(g)

if (P, t) is in the support of \(\sigma _i^{G*}\) or \(\sigma _i^{B*}\), then \(\mu _i(P,t)\) is derived from (1).

Consumers are clearly best responding to their beliefs in parts 3–5 of the guessed equilibrium. Beliefs in part 1 are consistent with part 2. It remains to check whether firms are best responding in part 2. First, deviations of type \(G\) to lower prices are ruled out. The preparative Lemma 7 derives the profit function of \(G\) from setting \(P< c_{B}\).

Lemma 7

In the guessed equilibrium, the profit of type \(G\) from \(P< c_{B}\) and t is

Proof

The profit (3) is derived from (2) by substituting in the consumers’ strategies in the guessed equilibrium: \(\sigma _1^*(v,P_i,t)(b)=1\) and \(\sigma _1^*(v,P_i,t)(\ell )=0\) for consumers initially at i, because \(P_i< c_{B}\) and \(\mu _i(P_i,t)=1\). Consumers with \(v\ge h^{-1}(P_i)\) buy from i, and they form a fraction \(1-F_v(h^{-1}(P_i))\) of the mass of consumers initially at i.

If firm j is type \(G\), then \(P_{j}=c_{B}\), \(t_{j}=G\) and \(\sigma _1^*(v,P_j,t_{j})(\ell )=0\). With probability \(1-\mu _0\), firm j is type \(B\), in which case consumer v at firm j learns \(P_i\) with probability \(\sigma _1^*(v,c_{B},B)(\ell )\) and then buys if \(v\ge h^{-1}(P_i)\). \(\square \)

Next, the technical Lemma 8 simplifies (3) by showing that if \(\sigma _i^{B*}\) puts probability 1 on \((P,t)=(c_{B},B)\) and \(\sigma _i^{G*}\) puts probability 1 on \((c_{B},G)\) for \(i\in \left\{ X,Y\right\} \), then \(\sigma _1^*(v,c_{B},B)(\ell )\) is a step function increasing in v.

Lemma 8

For customers initially at a type \(B\) firm, there exists \(v_{01}\in [h^{-1}(c_{B}),\overline{v}]\) s.t. \(\sigma _1^*(v,c_{B},B)(\ell )=0\) for \(v<v_{01}\) and 1 for \(v>v_{01}\).

Proof

Suppose firm i has type \(B\). Due to \(P_j\le c_{B}\), in Definition 1(d), \(v-c_{B}\) may be dropped under the \(\max \) w.l.o.g. If \(\int _{0}^{\infty }\sum _{t_{j}\in \left\{ G,B\right\} }\max \{0,\;w(v,j,P_{j},t_{j})\}[\mu _0\mathrm{d}\sigma _j^{G*}(P_{j},t_{j}) +(1-\mu _0)\mathrm{d}\sigma _j^{B*}(P_{j},t_{j})] -s\ge 0\), for consumer v, then for all \(\hat{v}>v\), the inequality is strict.

If \(w(v,j,P_{j},t_{j})\le 0\), then \(v-c_{B}<0\), so the first inequality in Definition 1(d) holds. If \(w(v,j,P_{j},t_{j})> 0\), then 0 may be dropped under the \(\max \) w.l.o.g. Then from \(h'\ge 1\) and \(\int _{0}^{\infty }\sum _{t_{j}\in \left\{ G,B\right\} }[\mu _0\mathrm{d}\sigma _j^{G*}(P_{j},t_{j}) +(1-\mu _0)\mathrm{d}\sigma _j^{B*}(P_{j},t_{j})]=1\), the first inequality in Definition 1(d) holds for all \(\hat{v}\ge v_1\). So if \(\sigma _1^*(v,c_{B},B)(\ell )>0\), then for all \(\hat{v}\ge v\), \(\sigma _1^*(\hat{v},c_{B},B)(\ell )=1\). Taking \(v_{01}:=\inf \left\{ v:\sigma _1^*(v,c_{B},B)(\ell )>0\right\} \) ensures that \(\sigma _1^*(\hat{v},c_{B},B)(\ell )=0\) for \(\hat{v}<v_{01}\) and 1 for \(\hat{v}>v_{01}\).

To prove \(v_{01}\ge h^{-1}(c_{B})\), note that \(h^{-1}(x)<x\;\forall x\), so \(h^{-1}(c_{B})-c_{B}<0\). If \(P_j\ge c_{B}\), then \(w(h^{-1}(c_{B}),j,P_{j},t_{j})\le 0\) for any \(t_{j}\). The \(-s\) term in Definition 1(d) then ensures \(\sigma _1^*(h^{-1}(c_{B}),c_{B},B)(\ell )=0\). \(\square \)

Downward price deviations by a type \(G\) firm are ruled out in the following Lemma. After that, the incentives of firm type \(B\) are discussed, and then, the deviations of \(G\) to \(P_{G}>c_{B}\) are ruled out.

Lemma 9

A type \(G\) firm’s best response to the strategies of other players in the guessed equilibrium satisfies \(P\ge c_{B}\).

Proof

Based on Lemma 8, \(\sigma _1^*(v,c_{B},B)(\ell )=0\) for all \(v\le h^{-1}(c_{B})\ge h^{-1}(P)\), where \(P\le c_{B}\). Therefore (3) reduces to \(\frac{1}{2}P[1-F_{v}(h^{-1}(P))+(1-\mu _0)[1-F_{v}(v_{01})]]\), with \(v_{01}\) independent of P.

The assumption \(P_{G}^{m} :=\arg \max _P P[1-F_{v}(h^{-1}(P))] \ge c_{B}\) then implies \(\arg \max _P \frac{1}{2}P[1-F_{v}(h^{-1}(P))+(1-\mu _0)[1-F_{v}(v_{01})]]\ge c_{B}\), because if \(P_{G}^{m}D(P_{G}^{m})\ge PD(P)\) for all \(P\le P_{G}^{m}\), then for any \(\bar{D}>0\) and \(P\le P_{G}^{m}\), we have \(P_{G}^{m}D(P_{G}^{m})+P_{G}^{m}\bar{D}\ge PD(P)+P\bar{D}\). So type \(G\) optimally sets a price \(P\ge c_{B}\). \(\square \)

Lemma 10

In the guessed equilibrium, a type \(B\) firm’s best response to the strategies of other players is \(P=c_{B}\) and \(t=B\).

Proof

A type \(B\) firm clearly does not deviate to \(P< c_{B}\) with any message. Consider \(B\)’s deviations to \(P> c_{B}\) and some \(t\in \left\{ G,B\right\} \). Parts 1 and 4 of the guessed equilibrium ensure that each customer initially at firm i charging \(P> c_{B}\) either leaves the market or learns the price and message of j. By part 5 of the guessed equilibrium, a customer who learns at firm i will choose firm j, which has both a lower price \(P_{j}=c_{B}<P\) and a higher belief \(\mu _{j}(c_{B},t_{j})\ge 0=\mu _{i}(P,t)\) for any \(t_{j},t\).

At \(P=c_{B}\), type \(B\) is indifferent between demand levels and thus between messages \(t\in \left\{ G,B\right\} \). Therefore, \(t=B\) is part of a best response. \(\square \)

Having ruled out deviations by \(B\), the final step (Lemma 11) is to eliminate deviations by a type \(G\) firm.

Lemma 11

A type \(G\) firm’s best response to the strategies of other players in the guessed equilibrium is \(P= c_{B}\) and \(t=G\).

Proof

Lemma 9 established \(P\ge c_{B}\). If firm i’s type \(G\) sets \(P>c_{B}\), with any \(t\in \left\{ G,B\right\} \), then it gets zero demand in the guessed equilibrium, because \(\mu _i(P,t)=0\) and the other firm j is expected to set price \(P_j\le c_{B}<P\). At \(P=c_{B}\), message \(t=B\) leads to belief \(\mu _i(c_{B},B)=0\), but message \(t=G\) to \(\mu _i(c_{B},G)=1\), thus greater demand. Therefore, \((c_{B},G)\) is the unique best response for type \(G\). \(\square \)

Proofs omitted from the main text

Proof of Proposition 1

Both types obtain positive profit in any equilibrium, because by the assumption \(\bar{v}>c_{B}\), setting \(P =c_{B}+\epsilon \) for \(\epsilon >0\) small enough results in positive demand at any message t, even at the worst belief \(\mu (P,t)=0\). Positive profit implies for any t that \(\sigma ^{G*}(0,t)=0\) and for all \(P\le c_{B}\), \(\sigma ^{B*}(P,t)=0\), i.e. weakly dominated strategies are never played in any equilibrium. Because demand is positive for both types, by Lemma 3 (the proof of which does not depend on any other results or on two firms), \(P_{G}\le P_{B}\) for any \(P_{\theta },t_{\theta }\) in the support of \(\sigma ^{\theta *}\).

Denote the profit of type \(\theta \) in a candidate equilibrium by \(\pi _{\theta }^*\). Define

so type \(B\) does not set \(P< P_1\) for any message t even at \(\mu (P_1,t)=1\). Clearly \(P_1>c_{B}\).

Positive \(f_{v}\) implies continuous \(F_{v}\). Differentiable strictly increasing h implies continuous \((P-c_{B})[1-F_{v}(h^{-1}(P))\), thus the \(\sup \) defining \(P_1\) is a \(\max \) and \((P_1-c_{B})[1-F_{v}(h^{-1}(P_1))]=\pi _{B}^*\).

Suppose that there exist (semi)pooling \(P_0,t_0\) s.t. \(\sigma ^{\theta *}(P_0,t_0)>0\) for both types. Then \((P_0-c_{B})D(P_0,\mu (P_0,t_0))=\pi _{B}^*\) and \(P_0D(P_0,\mu (P_0,t_0)) =\pi _{G}^* =\pi _{B}^* +c_{B}D(P_0,\mu (P_0,t_0)) <\pi _{B}^*+c_{B}[1-F_{v}(h^{-1}(P_1))] =\pi _{B}^*+c_{B}D(P_1,1) =P_1D(P_1,1)\), so for \(\epsilon >0\) small enough, \(G\) strictly prefers \(P_1-\epsilon \) at belief 1 to \(P_0\) at belief \(\mu (P_0,t_0)\). The strict preference of \(B\) not to deviate to \(P<P_1\) and \(G\) to deviate justifies belief 1 at any \(P<P_1\) by the Intuitive Criterion, and contradicts (semi)pooling on \(P_0\).

Because the types separate, belief is 0 at any P, t in the support of \(\sigma ^{B*}\). Thus, belief threats cannot deter \(B\) from deviating to \(P^{m}_{B}\) and any message t. The assumption that \(P^m_{B}\) is unique ensures that \(B\) chooses a pure price. The cheap talk message t is arbitrary.

The assumption that the full-information monopoly profit of \(G\) strictly increases in price on \([0,\min \left\{ P^m_{B},P^m_{G}\right\} ]\) ensures that \(G\) chooses a pure \(P_{G}=\min \left\{ P_1,P^m_{G}\right\} \). If \(P_1\le P^m_{G}\) and \(\mu (P_1,t_{G})<1\) for the message \(t_{G}\) that type \(G\) sends, then the best response of \(G\) does not exist, because of the open set problem. Thus in any equilibrium if \(P_1\le P^m_{G}\), then \(\mu (P_1,t_{G})=1\) and \(P_{G}=P_1\). Therefore, the equilibrium is unique up to changing the cheap talk messages. Consumer beliefs are constant in the cheap talk, so omitting it does not change the equilibrium prices. \(\square \)

Proof of Proposition 2

Type \(G\) setting \(P\in (0,c_{B})\) obtains positive demand and profit with probability at least \(1-\mu _0\) (when the rival firm is a bad type). Thus in any equilibrium, the price, demand and profit of \(G\) are positive. Then \(P_{G}\le P_{B}\) for any \(P_{\theta }\) in the support of \(\sigma ^{\theta *}_i\) by Lemma 3, the proof of which is independent of other results.

The Intuitive Criterion rules out (semi)pooling and sets belief to 1 for any \(P<c_{B}\) by the same argument as in Proposition 1 and Lemma 4. All consumers learn, so leave a type \(B\) firm if the other firm is type \(G\). Bertrand competition between the bad types then implies \(P_{B}=c_{B}\) in any equilibrium.

Suppose \(\inf \left\{ P:\exists t,\;\sigma ^{G*}_j(P,t)>0\right\} =:\underline{P}_{jG}< \underline{P}_{iG}\). Then, the profit of \(jG\) (firm j’s type \(G\)) from \(P\in (\underline{P}_{jG},\underline{P}_{iG})\) is \(P[1-F_{v}(h^{-1}(P))]\), which strictly increases in P by assumption. This contradicts the optimality of \(\underline{P}_{jG}\). Therefore, \(\underline{P}_{jG}= \underline{P}_{iG}\), denoted \(\underline{P}_{G}\) from here on. Gaps in the support of \(\sigma _j^{G*}\) are ruled out by the same reasoning.

Suppose that \(\sigma ^{G*}_i\) has an atom at some \(P_{iG}\). Then by the standard Bertrand undercutting argument, there exist \(\epsilon _1,\epsilon _2>0\) s.t. \(jG\) profitably deviates from any \(P_j\in [P_{iG},P_{iG}+\epsilon _1)\) to \(P=P_{iG}-\epsilon _2\). This rules out atoms in \(\sigma ^{G*}_i\).

Suppose \(\sup \left\{ P:\exists t,\;\sigma ^{G*}_j(P,t)>0\right\} =:\overline{P}_{jG}< \overline{P}_{iG} \le c_{B}\). Because \(\mu _i(P,t)=1\) for any \(P<c_{B}\) and any t, the profit of \(iG\) from \(P\in (\overline{P}_{jG},c_{B})\) is \((1-\mu _0)P[1-F_{v}(h^{-1}(P))]\), which strictly increases in P by assumption. This contradicts the optimality of \(P\in (\overline{P}_{jG},c_{B})\), and a gap in the support of \(\sigma ^{G*}_i\) was ruled out above. Therefore, \(\overline{P}_{jG}=\overline{P}_{iG} =c_{B}\).

Profit must be constant on the support of \(\sigma ^{G*}_i\), i.e. \(\mu _0P[1-F_{v}(h^{-1}(P))][1-\sum _{t_j\in \left\{ G,B\right\} }\sigma _{j}^{G*}(P,t_j)] +(1-\mu _0)P[1-F_{v}(h^{-1}(P))] =(1-\mu _0)c_{B}[1-F_{v}(h^{-1}(c_{B}))]\). Rearranging yields \(\sum _{t_j\in \left\{ G,B\right\} }\sigma _{j}^{G*}(P,t_j) =\frac{1}{\mu _0}-\frac{(1-\mu _0)c_{B}[1-F_{v}(h^{-1}(c_{B}))] }{\mu _0P[1-F_{v}(h^{-1}(P))]}\). Taking \(P\in \left\{ \underline{P}_{G}, \overline{P}_{G}\right\} \) yields \(\underline{P}_{G}\left[ 1-F_{v}(h^{-1}(\underline{P}_{G}))\right] =(1-\mu _0)c_{B}\left[ 1-F_{v}(h^{-1}(c_{B}))\right] \). \(\square \)

Proof of Lemma 3

In any equilibrium, the incentive constraints (ICs) \(P_{G} D_i(P_{G},t_{G})\ge P D_i(P,t)\) and \((P_{B}-c_{B}) D_i(P_{B},t_{B})\ge (P-c_{B}) D_i(P,t)\) hold for any \(P,P_{\theta },t,t_{\theta }\) with \((P_{\theta },t_{\theta })\) in the support of \(\sigma _i^{\theta *}\). Demand and price are nonnegative and finite by definition. From \((P_{B}-c_{B}) D_i(P_{B},t_{B})\ge (P_{G}-c_{B}) D_i(P_{G},t_{G})\) and \(P_{G} D_i(P_{G},t_{G})\ge P_{B} D_i(P_{B},t_{B})\), we get \((P_{B}-c_{B}) D_i(P_{B},t_{B})\ge P_{G} D_i(P_{G},t_{G})-c_{B}D_i(P_{G},t_{G})\ge P_{B} D_i(P_{B},t_{B})-c_{B}D_i(P_{G},t_{G})\), so \(D_i(P_{B},t_{B})\le D_i(P_{G},t_{G})\).

If \(0<D_i(P_{B},t_{B})\le D_i(P_{G},t_{G})\) and \((P_{B}-c_{B}) D_i(P_{B},t_{B})\ge (P_{G}-c_{B}) D_i(P_{G},t_{G})\), then \(P_{B}-c_{B}\ge P_{G}-c_{B}\), so \(P_{B}\ge P_{G}\). \(\square \)

Proof of Lemma 4

Suppose \(\pi _{iG}^*=0\) and use the Intuitive Criterion to derive a contradiction. Fix some \(P_{i}\in (0,\min \left\{ s,c_{B}\right\} )\) and \(t\in \left\{ G,B\right\} \). Set belief to \(\mu _{i}(P_{i},t)=1\). No consumer learns at \(P_{i},t\) and belief \(\mu _{i}(P_{i},t)=1\), because firm j is expected to have weakly lower quality and a price \(P_{j}\ge 0\) lower by at most \(s\). The greatest possible price decrease \(|P_{j}-P_{i}|< s\) from switching to j does not justify paying the learning cost \(s\). By assumption, \(h(P_{i})>P_{i}>0\), so consumers with valuations \(v\le P_{i}\) buy at \(P_{i},t,\mu _{i}(P_{i},t)\) and yield positive demand and profit to type \(G\). Type \(B\) can ensure nonnegative profit by setting \(P\ge c_{B}\), thus must get nonnegative equilibrium profit \(\pi _{iB}^*\ge 0\). Choosing \(P_{i},t\) gives \(B\) positive demand, so strictly negative profit. Thus, belief \(\mu _{i}(P_{i},t)=1\) is justified and any supposed equilibrium with \(\pi _{iG}^*=0\) is eliminated.

Next, the Intuitive Criterion is used to eliminate pooling and semi-pooling on any \(P_{i0}>c_{B}\), \(t_{i0}\). By \(\pi _{iG}^*>0\), demand is positive at \(P_{i0},t_{i0}\), so \(\pi _{iB}^*>0\). Lemma 3 implies that any price in the support of \(\sigma _i^{B*}\) is above \(P_{i0}\) and any price in the support of \(\sigma _i^{G*}\) is below \(P_{i0}\).

Denote demand at the fixed belief \(\mu \) by \(D_{i}^{\mu }(P)\); it does not depend on t due to the fixed \(\mu \). Demand \(D_{i}^{\mu }(P)\) increases in \(\mu \) and decreases in P, so the profit \((P-c_{\theta })D_{i}^{\mu }(P)\) as a function of P does not have upward jumps. At \(P=c_{B}\), the profit of \(B\) is \((c_{B}-c_{B})D_{i}^{\mu }(c_{B})=0\) for any \(\mu \), but at \(P_{i0}>c_{B}\), the equilibrium profit is \(\pi _{iB}^*>0\). Pooling implies \(\mu _{i}(P_{i0},t_{i0})<1\), so \(D_{i}(P_{i0},t_{i0})<D_{i}^{1}(P_{i0})\) and therefore \((P_{i0}-c_{B})D_{i}^{1}(P_{i0})>\pi _{iB}^* >0\). Thus, there exists \(P_{d*}\in (c_{B},P_{i0})\) s.t. for any \(P< P_{d*}\), \((P-c_{B})D_{i}^{1}(P)<\pi _{iB}^*\). Focus on the maximal such \(P_{d*}\). The lack of upward jumps in \((P-c_{B})D_{i}^{1}(P)\) implies that for any \(\epsilon >0\) there exists \(\delta >0\) s.t. \((P_{d*}-\delta -c_{B})D_{i}^{1}(P_{d*}-\delta )\ge \pi _{iB}^*-\epsilon \). If \(\delta \) is small enough s.t. \(\epsilon <D_{i}^{1}(P_{d*}-\delta ) -D_{i}(P_{i0},t_{i0})\), then type \(G\) strictly prefers to deviate to \(P_{d*}-\delta \) and t at \(\mu _{i}(P_{d*}-\delta ,t)=1\), because \((P_{d*}-\delta -0)D_{i}^{1}(P_{d*}-\delta ) \ge \pi _{iB}^*+ (c_{B}-0)D_{i}^{1}(P_{d*}-\delta )-\epsilon > \pi _{iB}^*+ (c_{B}-0)D_{i}(P_{i0},t_{i0})=\pi _{iG}^* \). By the definition of \(P_{d*}\), type \(B\) strictly prefers the equilibrium to \(P_{d*}-\delta \), which justifies \(\mu _{i}(P_{d*}-\delta ,t)=1\) and eliminates pooling on any \(P_{i0}>c_{B}\) and \(t_{i0}\).

Pooling and semi-pooling on \(P_{i0}=c_{B}\) and some \(t_{i0}\) is eliminated by the Intuitive Criterion as follows. For \(\epsilon >0\) small and some \(t_{i}\), set \(\mu _{i}(c_{B}-\epsilon ,t_{i})=1\). Due to pooling, \(\mu _{i}(c_{B},t_{i0})<1\), so \(D_{i}^{1}(c_{B})> D_{i}^{\mu _{i}(c_{B},t_{i0})}(c_{B}) =D_{i}(c_{B},t_{i0})\). At \(c_{B}-\epsilon \) and \(t_{i}\), demand is \(D_{i}^{1}(c_{B}-\epsilon )> D_{i}^{\mu _{i}(c_{B},t_{i0})}(c_{B}) =D_{i}(c_{B},t_{i0})\). Thus for \(\epsilon \) small enough, \(G\) strictly prefers \(c_{B}-\epsilon ,t_{i}\) to \(c_{B},t_{i0}\). By \(\pi _{iG}^*>0\), demand is positive at \(c_{B},t_{i0}\), so \(B\) strictly prefers \(c_{B},t_{i0}\) to \(c_{B}-\epsilon ,t_{i}\). These strict preferences justify \(\mu _{i}(c_{B}-\epsilon ,t_{i})=1\) and eliminate pooling on \(c_{B},t_{i0}\).

Pooling and semi-pooling on \(P_{i0}<c_{B}\) and some \(t_{i0}\) cannot occur, because \(\pi _{iG}^*>0\) implies \(D_{i}(P_{i0},t_{i0})>0\), which would yield \(\pi _{iB}^*<0\). \(\square \)

Proof of Lemma 5

By Lemma 4, \(\pi _{iG}^*>0\) for both \(i\in \left\{ X,Y\right\} \), and type \(B\) strictly prefers its equilibrium price to any \(P_{i}<c_{B}\) for any \(t_{i}\). Thus if \(G\) strictly prefers \(P_{i},t_{i}\) to its equilibrium action when \(\mu _{i}(P_{i},t_{i})=1\), then the equilibrium fails the Intuitive Criterion.

Denote by \(\underline{P}_{i\theta } :=\inf \left\{ P:\sigma _{i}^{\theta *}(P,t)=0\;\forall t\right\} \) the lower bound of the prices that firm i’s type \(\theta \) sets. Assume w.l.o.g. that \(\underline{P}_{iG}\le \underline{P}_{jG}\). If firm i raises price to \(\underline{P}_{iG}+\epsilon \) for \(\epsilon \in (0,\min \{s,c_{B}-\underline{P}_{iG}\})\) and belief is \(\mu _{i}(\underline{P}_{iG}+\epsilon ,t)=1\) for some t, then consumers initially at firm i still choose \(\sigma _1(v,\underline{P}_{iG}+\epsilon ,t)(\ell )=0\), because a price difference less than \(s\) does not justify the learning cost. The customers at j who chose \(\ell \) anticipating \(\sigma _i^{G*}\) do not know about \(G\)’s deviation, so still choose \(\ell \). Upon learning \(\underline{P}_{iG}+\epsilon ,t\), a customer initially at j’s type \(B\) has a choice between \(B\) at \(P_{B}\ge c_{B}\) and \(G\) at \(\underline{P}_{iG}+\epsilon < c_{B}\), so still buys from i’s type \(G\). If a customer initially at j’s type \(G\) learns both firms’ prices and messages and believes \(\mu _{i}(\underline{P}_{iG}+\epsilon ,t)=1\), then he still buys from i if \(P_{jG}\ge \underline{P}_{iG}+\epsilon \). If \(P_{jG}\le \underline{P}_{iG}+\epsilon \), then no customer facing \(P_{jG}\) learns, because firm i has weakly lower quality and a price lower by at most \(\epsilon <s\). At prices \(P\le c_{B}\), the profit of \(G\) is then given by (3). By Lemmas 8–9, \(G\) strictly prefers to increase price. \(\square \)

Proof of Theorem 6

The assumptions \(\overline{v}>c_{B}\) and \(f_{v}>0\) ensure that there exists \(\epsilon >0\) s.t. total demand is positive at \(P_{i}=c_{B}+\epsilon \) for any \(P_{j},t_{j},t_{i}\). Suppose by way of contradiction that \(\sigma _j^{B*}\) puts positive probability on \(P_{j},t_{j}\) at which \(D_{j}(P_{j},t_{j})=0\). Then the expected demand for firm i is positive at \(P_{i}=c_{B}+\epsilon \), implying that both types of firm i make positive profit, thus \(\underline{P}_{iB}>c_{B}\). By Lemma 4, the supports of \(\sigma _i^{B*}\) and \(\sigma _i^{G*}\) are disjoint, so \(\mu _{i}(P,t)=0\) for any (P, t) in the support of \(\sigma _i^{B*}\). Any \(P_{jd},t_{jd}\) with \(P_{jd}\in (c_{B},\underline{P}_{iB})\) then attracts positive demand in expectation, because \(\mu _{j}(P_{jd},t_{jd})\ge \mu _{i}(P,t)=0\). Firm j’s type \(B\) deviates from any zero-demand price to \(P_{jd},t_{jd}\) and makes positive profit. This contradicts \(D_{j}(P_{j},t_{j})=0\) for any \(P_{j},t_{j}\) in the support of \(\sigma _j^{B*}\). Therefore, demand is positive in expectation for both types of both firms in any equilibrium satisfying the Intuitive Criterion.

By Lemma 3, positive demand implies \(P_{G}\le P_{B}\ge c_{B}\) for any \(P_{\theta }\) in the support of \(\sigma _i^{\theta *}\). As shown next, all consumers initially at type \(B\) of at least one firm learn before buying. Assume \(\overline{P}_{iG}\ge \overline{P}_{jG}\) w.l.o.g. Then \(\underline{P}_{iB}\ge \overline{P}_{jG}\), so a consumer with valuation v facing \(P_{iB}\ge \underline{P}_{iB}\) and any \(t_{i}\) gets payoff \(v-P_{iB}\) from buying immediately. On the other hand, learning yields consumer v a payoff of at least \(h(v)-\overline{P}_{jG}\) with probability \(\mu _{0}\), and \(v-P_{iB}\) with probability \(1-\mu _{0}\). If \(\mu _{0}[h(v)-v]\ge s\), then consumer v prefers learning to buying. Consumers \(v<P_{iB}\) do not buy at \(P_{iB}\) and \(\mu _{i}(P_{iB},t)=0\), thus either leave the market or learn. For \(v\ge P_{iB}\ge c_{B}\), the assumption \(\mu _{0}[h(c_{B})-c_{B}]\ge s\) implies learning instead of immediate buying.

Having \(\overline{P}_{iB}>\overline{P}_{jB}\) when all consumers at i learn or leave contradicts positive demand for i. The previous paragraph proves that all customers at j learn or leave when \(\overline{P}_{iB}\le \overline{P}_{jB}\). Given that all consumers who end up buying from type \(B\) have learned both firms’ prices and messages, the \(B\) types are in Bertrand competition. The following undercutting argument then shows that \(B\) prices at \(c_{B}\) with certainty. Having \(\overline{P}_{iB}\ne \overline{P}_{jB}\) contradicts positive demand for one firm. If \(\sigma _j^{B*}\) has an atom at \(\overline{P}_{jB}=\overline{P}_{iB}>c_{B}\), then for small enough \(\epsilon >0\), firm i’s type \(B\) strictly prefers \(\overline{P}_{iB}-\epsilon \) to \(\overline{P}_{iB}\). Supposing \(\sigma _j^{B*}\) has no atom at \(\overline{P}_{jB}>c_{B}\) implies probability 1 of \(\overline{P}_{iB}>P_{jB}\), which contradicts \(D_{i}(\overline{P}_{iB},t)>0\).

Lemmas 5 and 3 with \(\overline{P}_{iB}=c_{B}\) imply that both types price at \(c_{B}\) with certainty. Lemma 4 proves disjoint supports of \(\sigma _i^{B*}\) and \(\sigma _i^{G*}\), so \(t_{iB}\ne t_{iG}\) with certainty. \(\square \)

Positively correlated cost and quality

Consumers are assumed homogeneous and cheap talk absent, both for simplicity and for better comparability to the literature. Adding cheap talk does not change the prices or consumers’ strategies. The Online Appendix studies the heterogeneous consumer case. In this section, all consumers have valuation \(v_{B}> c_{B}\) for type \(B\) and \(v_{G}:=h(v_{B})>v_{B}\) for \(G\). The marginal cost of \(G\) is \(c_{G}> c_{B}\).

There are multiple separating equilibria with the same outcome: \(P_{i\theta }=v_{\theta }\) for \(i\in \left\{ X,Y\right\} \), \(\theta \in \left\{ B,G\right\} \), no consumers learn, all buy at \(P\le v_{B}\), fraction \(\frac{v_{B}-c_{B}}{v_{G}-c_{B}}\) buy at \(P> v_{B}\). Beliefs that support these strategies are \(\mu _{i}(P)= \frac{P-v_{B}}{v_{G}-v_{B}}\) for \(P\in [v_{B},v_{G}]\), and arbitrary beliefs for \(P>v_{G}\) and \(P<v_{B}\). Other equilibria with the same outcome have \(\mu _{i}(P)\le \frac{P-v_{B}}{v_{G}-v_{B}}\) for \(P\in [v_{B},v_{G})\), \(\mu _{i}(v_{G})=1\) and fraction less than \( \frac{v_{B}-c_{B}}{P-c_{B}}\) of consumers buying at \(P\in (v_{B},v_{G})\). The fraction is 0 if \(\mu _{i}(P)< \frac{P-v_{B}}{v_{G}-v_{B}}\). The beliefs in all these separating equilibria pass the Intuitive Criterion, because if \(G\) wants to deviate to price \(P_{d}\in (v_{B},v_{G})\) with belief \(\mu _{i}(P_{d})=1\), then \(B\) strictly prefers \(P_{d}\), which yields the same demand as \(P_{iB}=v_{B}\), but strictly greater margin. The equilibrium outcome is the natural analogue of Diamond (1971). The uniqueness of this outcome is shown next.

An equilibrium with \(P_{iB}<v_{B}\) and \(P_{iB}\le P_{jB}\) cannot exist, because if consumers who see \(P_{iB}\) do not learn, then firm i’s type \(B\) can raise its price by \(\epsilon \in (0,s)\). For consumers who see \(P_{iB}\) to learn, they must expect \(\mu _{0}(v_{G}-P_{jG})+(1-\mu _{0})(v_{B}-P_{jB})-s\ge v_{B}-P_{iB}\), i.e. \(\mu _{0}(v_{G}-P_{jG} -v_{B}+P_{jB})\ge P_{jB}-P_{iB}+s>0\). However, if \(v_{G}-P_{jG}>v_{B}-P_{jB}\), then demand is weakly greater at \(P_{jG}\) than at \(P_{jB}\), thus type \(B\) of firm j strictly prefers to deviate to \(P_{G}\).

An equilibrium where firm i does not pool and \(P_{iG}<v_{G}\) cannot exist, because all consumers would buy at \(P_{iG}\). In this case, demand is weakly greater at \(P_{iG}\) than at \(P_{iB}\), so type \(B\) of firm i strictly prefers to deviate to \(P_{iG}\). Thus the only non-pooling equilibria feature \(P_{i\theta }=v_{\theta }\).

Pooling on any \(P_{i0}\le \mu _{0}v_{G}+(1-\mu _{0})v_{B}\) fails the Intuitive Criterion: at the deviation price \(P_{d}=v_{G}\) and the most favourable belief \(\mu _{i}(v_{G})=1\), a (mixed) best response of the consumers exists for which \(G\) prefers to deviate from \(P_{i0}\) and \(B\) prefers not to.

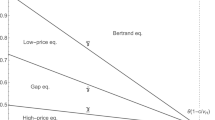

The unique separating outcome (no learning, \(P_{i\theta }=v_{\theta }\), some consumers do not buy at \(P_{iG}=v_{G}\)) stands in contrast to Janssen and Roy (2015), regardless of which equilibrium characterisation in their Proof of Proposition 2 is used. The first paragraph of Janssen and Roy (2015) Proof of Proposition 2 describes the unique symmetric D1 equilibrium as follows.

-

(a)

If \(\frac{v_{B}-c_{B}}{v_{G}-c_{B}}> \frac{1}{2}\), then \(P_{iG}=v_{G}\). If both firms are type \(G\), then some consumers do not buy, otherwise all buy.

-

(b)

If \(\frac{v_{B}-c_{B}}{v_{G}-c_{B}}\le \frac{1}{2}\), then \(P_{iG}=\max \left\{ c_{G},c_{B}+2(v_{G}-v_{B})\right\} \) and all consumers buy.

From the second paragraph on, Janssen and Roy (2015) Proof of Proposition 2 claims:

-

(a)

If \(\frac{v_{B}-c_{B}}{v_{G}-c_{B}}\ge \frac{1}{2}\), then \(P_{iG}=c_{B}+2(v_{G}-v_{B})\), type \(B\) mixes over \(P_{iB}\in [c_{B}+\mu _{0}(v_{G}-v_{B}),\; c_{B}+v_{G}-v_{B}]\), all consumers buy at the lowest price, breaking ties uniformly randomly.

-

(b)

If \(\frac{v_{B}-c_{B}}{v_{G}-c_{B}}< \frac{1}{2}\), then \(P_{iG}=v_{G}\), type \(B\) mixes over \(P_{iB}\in [c_{B}+\mu _{0}(v_{B}-c_{B}),\; v_{B}]\). If both firms charge \(v_{G}\), then a consumer buys from each with probability \(\frac{v_{B}-c_{B}}{v_{G}-c_{B}}\) and leaves the market with probability \(\frac{v_{G}-c_{B}-2v_{B}+2c_{B}}{v_{G}-c_{B}}\). If at least one firm charges \(P\le v_{B}\), then the consumer buys at the lowest price with certainty.

Unlike in the incomplete information Bertrand model of Janssen and Roy (2015), the equilibrium under costly learning in this section features \(P_{iB}=v_{B}\) (instead of \(B\) mixing on lower prices), zero consumer surplus, consumers never switching (as opposed to always switching when the types of the firms differ), and not all consumers buying when the types of the firms differ. Depending on the parameters in Janssen and Roy (2015), the equilibria also differ in \(P_{iG}\) and the probability of consumers purchasing when both firms are type \(G\).

Several of the differences are the expected ones between Bertrand and Diamond environments—no search, monopoly pricing and the corresponding surplus extraction. This paper’s low price resembles the Bertrand competition with negative correlation in the appendix of Janssen and Roy (2015), but in their Bertrand environment, a competitive outcome is to be expected, unlike here.

With heterogeneous consumers and positively related cost and quality, the Online Appendix shows that the results are analogous to the current section and Diamond (1971), thus contrasting Sect. 3. In particular, type \(B\) still prices above its complete-information monopoly level, \(G\) prices above \(B\) by at least the quality difference between the types, and consumers do not learn at \(B\). The heterogeneous consumer case differs from homogeneous in that \(G\) may set a price different from its complete-information monopoly level, some consumers learn at \(G\) and switch to \(B\) given the chance, and at both types of firms, low-valuation consumers leave the market.

Rights and permissions

About this article

Cite this article

Heinsalu, S. Competitive pricing despite search costs when lower price signals quality. Econ Theory 71, 317–339 (2021). https://doi.org/10.1007/s00199-020-01247-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00199-020-01247-3