Abstract

This paper examines the relative significance of oil supply, oil demand, and monetary policy shocks in explaining US macroeconomic variations. We analyze impulse response functions and variance decomposition to assess the relative importance of these shocks. Using a Bayesian structural VAR framework and the penalty function approach, we identify the shocks of interest. We find that oil supply shocks explain less than 3% of the variation in output, but have a relatively larger impact on inflation, accounting for around 13% of the inflation variation. Oil demand shocks explain 3% of output variation, but contribute significantly to inflation variation (around 16%). In contrast, monetary policy shocks have a greater influence on output, explaining approximately 13% of the observed variation. Monetary policy shocks are also the most influential source of inflation variation, contributing over 24% to the overall variation. Based on historical variance decomposition, we find that the recent inflation surge is attributable to both monetary expansion and oil supply factors. Overall, the study highlights the dominance of monetary policy shocks in explaining US macroeconomic fluctuations, with oil supply and demand shocks playing secondary roles.

Similar content being viewed by others

Data availability

Data will be available upon request.

Notes

Based on the authors’ calculations using data from the Federal Reserve Economic Database (FRED).

We use consumption in nominal terms and although nominal consumption might be highly correlated with the inflation covariate, we show in robustness tests that the results are not affected by excluding nominal consumption (growth).

In Sect. 5, we estimate the model with the growth rate of real GDP as well as an alternative measure of the output gap.

See https://sites.google.com/site/cjsbaumeister/datasets?authuser=0 for these series.

Since for any orthonormal matrix \({\varvec{S}}, \widetilde{{ {\varvec{A}} }}^{-1}= {\varvec{T}} {\varvec{S}}\) is also a decomposition that satisfies \([\widetilde{{ {\varvec{A}} }}\widetilde{{ {\varvec{A}} }}^{^{\prime }}]^{\prime }=\varvec{\Omega }\), where \({\varvec{T}}\) is a Cholesky factorization of \(\varvec{\Omega }\).

This refers to an issue encountered with pure sign restrictions, where multiple models with identified parameters can rationalize the data. As a result, while pure sign restrictions achieve parameter identification, they may not achieve model identification. Thus, summarizing the responses using for instance the median response and conventional error bands represent the range of response distributions across these different models. See Fry and Pagan (2011).

Note that using two quarters yields similar results but we impose the restrictions for one quarter here to reflect our desire to have less restrictive assumptions.

We re-estimated the baseline model using the shadow federal funds rate for time periods in which the effective federal funds rate had reached the zero lower bound. For conciseness, we do not report those results as they are identical to results already presented in the figures.

References

Aastveit KA (2013) Oil price shocks and monetary policy in a data-rich environment. Norges bank working paper

Atems Lam E (2013) The response of US States to exogenous oil supply and monetary policy shocks. Res Appl Econ 5(3):106

Barnett WA, Liu J, Mattson RS, van den Noort J (2013) The new CFS Divisia monetary aggregates: design, construction, and data sources. Open Econ Rev 24:101–124

Barsky RB, Kilian L (2002) Do we really know that oil caused the great stagflation? A monetary alternative. In: Bernanke BS, Rogoff K (eds) NBER macroeconomics annual 2001. MIT Press, Cambridge

Barsky RB, Kilian L (2004) Oil and the macroeconomy since the 1970s. J Econ Perspect 18(4):115–134

Baumeister C, Hamilton JD (2019) Structural interpretation of vector autoregressions with incomplete identification: revisiting the role of oil supply and demand shocks. Am Econ Rev 109(5):1873–1910

Bernanke BS, Gertler M, Watson M, Sims CA, Friedman BM (1997) Systematic monetary policy and the effects of oil price shocks. Brook Pap Econ Act 1:91–157

Bjørnland HC (2000) The dynamic effects of aggregate demand, supply and oil price shocks: a comparative study. Manch Sch 68(5):578–607

Caldara D, Fuentes-Albero C, Gilchrist S, Zakrajšek E (2016) The macroeconomic impact of financial and uncertainty shocks. Eur Econ Rev 88:185–207

Christiano LJ, Eichenbaum M, Evans CI (2005) Nominal rigidities and the dynamic effects of a shock to monetary policy. J Polit Econ 113:1–45

Cologni A, Manera M (2008) Oil prices, inflation and interest rates in a structural cointegrated VAR model for the G-7 countries. Energy Econ 30:856–888

Dery C, Serletis A (2021) Interest rates, money, and economic activities. Macroecon Dyn 25:1842–1891

Dery C, Serletis A (2023) Macroeconomic fluctuations in the United States: the role of monetary and fiscal policy shocks. In: Open economies review, pp 1–17

Emmons W (2022) Measuring the Fed’s Monetary Policy Stance during COVID-19. The Regional Economisthttps://www.stlouisfed.org/publications/regional-economist/2022/apr/measuring-fed-monetary-policy-stance-covid-19

Faust J (1998) The robustness of identified VAR conclusions about money. Carnegie-Rochester Conf Ser Publ Pol 49:207–244

Fry R, Pagan A (2011) Sign restrictions in structural vector autoregressions: a critical review. J Econ Lit 49:938–60

Hamilton JD (2003) What is an oil shock? J Econ 113:363–398

Hamilton JD (2018) Why you should never use the Hodrick–Prescott filter. Rev Econ Stat 100:831–843

Hamilton JD, Herrera AM (2004) Oil shocks and aggregate macroeconomic behavior: the role of monetary policy. J Money Cred Bank 36:265–286

Hansen N, Müller SD, Koumoutsakos P (2003) Reducing the time complexity of the derandomized evolution strategy with covariance matrix adaptation (CMA-ES). Evolut Comput 11:1–18

Herrera AM, Pesavento E (2009) Oil price shocks, systematic monetary policy, and the “Great Moderation’’. Macroecon Dyn 13(1):107–137

Jadidzadeh A, Serletis A (2019) The demand for assets and optimal monetary aggregation. J Money Cred Bank 51:929–952

Kilian L (2008) Exogenous oil supply shocks: How big are they and how much do they matter for the US economy? Rev Econ Stat 90(2):216–240

Kilian L (2008) A comparison of the effects of exogenous oil supply shocks on output and inflation in the G7 countries. J Eur Econ Assoc 6(1):78–121

Kilian L (2009) Not all oil price shocks are alike: disentangling demand and supply shocks in the crude oil market. Am Econ Rev 99(3):1053–1069

Kilian L (2014) Oil price shocks: causes and consequences. Ann Rev Resour Econ 6(1):133–154

Kilian L, Lewis LT (2011) Does the Fed respond to oil price shocks? Econ J 121(555):1047–1072

Kilian L, Murphy DP (2012) Why agnostic sign restrictions are not enough: understanding the dynamics of oil market VAR models. J Eur Econ Assoc 10(5):1166–1188

Mountford A, Uhlig H (2009) What are the effects of fiscal policy shocks? J Appl Econ 24:960–992

Rahman S, Serletis A (2010) The asymmetric effects of oil price and monetary policy shocks: a nonlinear VAR approach. Energy Econ 32(6):1460–1466

Uhlig H (2005) What are the effects of monetary policy on output? Results from an agnostic identification procedure. J Monet Econ 52:381–419

Wei Y, **aoying G (2022) The impact of oil supply shocks on real economic activity: new evidence based on the proxy SVARs. Appl Econ 54(44):5035–5049

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

We have no conflicts of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

We would like to thank two referees for comments that greatly improved the paper. Cosmas Dery thanks the College of Business Administration of Sam Houston State University for a Summer Research Grant that provided support for this research.

Appendix

Appendix

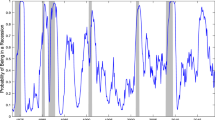

Variance decomposition of variables to oil demand shock. Note: The solid black line is the posterior median response, while the blue dashed lines are the corresponding Bayesian 68% confidence intervals. (Color figure online)

Variance decomposition of variables to monetary policy shocks. Note: The solid black line is the posterior median response, while the blue dashed lines are the corresponding Bayesian 68% confidence intervals. (Color figure online)

See Figs. 12, 13, 14, 15, 16, 17 and

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Dery, C., Serletis, A. Business cycles in the USA: the role of monetary policy and oil shocks. Empir Econ 67, 1–30 (2024). https://doi.org/10.1007/s00181-024-02556-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-024-02556-5