Abstract

The Russian–Ukrainian conflict has led to ongoing disruptions in global agricultural prices and maritime transport markets, exacerbating food insecurity and raising concerns about the ocean transportation of food. To comprehend this complex relationship, this study employs a vector autoregression model to investigate the time-varying nonlinear connection among global economic policy uncertainty (GEPU), food prices, and maritime transport. Utilizing bivariate and multivariate wavelet frameworks, we validate and explore the lead-lag relationships, co-movements, and dynamic associations among these indicators across various time and frequency domains. The findings reveal a significant covariance among the variables, with medium- and long-term changes being more affected by short-term shocks. Furthermore, there exists both positive and negative interdependence among the variables in the long term, with the interdependence strengthening progressively from the medium to the long term. Notably, the volatility of ocean freight rates has exceeded that of food prices in recent years, thus, impacting future economic policy directions. These results provide a warning to food trade participants as well as governments that focusing on transport market volatility to smooth out food market and economic policy volatility ought to be an important preoccupation, together with increased attention to the potential consequences of global economic policy changes, in order to ensure greater market stability and sustainability in the transportation of food.

Similar content being viewed by others

Data availability

The data that support the findings of this study are available from the corresponding author, [Zijiang Hu], upon reasonable request.

Notes

The use of the word ‘food’ in this paper refers to grains, other staples, and animal feedstock, usually transported by sea with bulk carriers of the smaller sizes.

GEPU is available at http://www.policyuncertainty.com/about.html.

CRB Foodstuffs Spot Price Index is available at https://macrovar.com/commodities/crb-foodstuffs-index/.

Route P1A_82: Delivery Skaw-Gibraltar range, loading 15–20 days from the index date, for a trans-Atlantic round voyage of 40–60 days, redelivery Skaw-Gibraltar range. 5.00% total commission.

Route P2A_82: Delivery Skaw-Gibraltar range, loading 15–20 days from the index date, for a trip of 65–80 days, redelivery Hong Kong-South Korea range including Taiwan. 5.00% total commission.

Route P3A_82: Delivery Hong Kong-South Korea range including Taiwan, loading 15–20 days from the index date, for a 35–50 days Pacific round trip redelivery Hong Kong-South Korea range including Taiwan. 5.00% total commission.

Route P4_82: Delivery Hong Kong-South Korea range including Taiwan, loading 15–20 days from the index date, for a 55–70 day trip redelivery Skaw-Gibraltar range. 5.00% total commission.

Route P6_82: Delivery Singapore, loading 30–35 days from the index date, for a 90–105 day trip via Atlantic redelivery Hong Kong-South Korea range including Taiwan. 5% total commission.

References

Alabi, M.O., and O.K. Ngwenyama. 2022. Food security and disruptions of the global food supply chains during COVID-19: building smarter food supply chains for post COVID-19 era. British Food Journal. https://doi.org/10.1108/bfj-03-2021-0333.

Alsuwailem, A.A., E. Salem, A.K.J. Saudagar, A. AlTameem, M. AlKhathami, M.B. Khan, and M.H.A. Hasanat. 2022. Impacts of COVID-19 on the food supply chain: A case study on Saudi Arabia. Sustainability 14 (1): 254. https://doi.org/10.3390/su14010254.

Arain, H., A. Sharif, B. Akbar, and M.Y. Younis. 2020. Dynamic connection between inward foreign direct investment, renewable energy, economic growth and carbon emission in China: Evidence from partial and multiple wavelet coherence. Environmental Science and Pollution Research 27 (32): 40456–40474. https://doi.org/10.1007/s11356-020-08836-8.

Atanga, R., and V. Tankpa. 2021. Climate change, flood disaster risk and food security nexus in Northern Ghana. Frontiers in Sustainable Food Systems. https://doi.org/10.3389/fsufs.2021.706721.

Baker, S.R., N. Bloom, and S.J. Davis. 2016. Measuring economic policy uncertainty. The Quarterly Journal of Economics 131 (4): 1593–1636.

Ben Hassen, T., and H. El Bilali. 2022. Impacts of the Russia-Ukraine war on global food security: Towards more sustainable and resilient food systems? Foods 11: 2301. https://doi.org/10.3390/foods11152301.

Bessler, D., and S. Lee. 2022. Money and prices: U.S. Data 1869–1914 (A study with directed graphs). Empirical Economics 27: 427–446. https://doi.org/10.1007/s001810100089.

Bessler, D., and M. Haigh. 2004. Causality and price discovery: An application of directed acyclic graphs. The Journal of Business 77: 1099–1121. https://doi.org/10.22004/ag.econ.19057.

Breisinger, C., O. Ecker, R. Thiele, and M. Wiebelt. 2016. Effects of the 2008 flood on economic performance and food security in Yemen: A simulation analysis. Disasters 40 (2): 304–326. https://doi.org/10.1111/disa.12147.

Davis, S.J. 2016. An index of global economic policy uncertainty (No. w22740). National Bureau of Economic Research. https://doi.org/10.3386/w22740.

Davis, S.J. 2019. Rising policy uncertainty (No. w26243). National Bureau of Economic Research. https://doi.org/10.3386/w26243.

Fang, Y., and Z.Q. Shao. 2022. The Russia-Ukraine conflict and volatility risk of commodity markets. Finance Research Letters 50: 103264. https://doi.org/10.1016/j.frl.2022.103264.

Frimpong, S., E.N. Gyamfi, Z. Ishaq, S.K. Agyei, D. Agyapong, and A.M. Adam. 2021. Can global economic policy uncertainty drive the interdependence of agricultural commodity prices? Evidence from partial wavelet coherence analysis. Complexity 2021: 8848424. https://doi.org/10.1155/2021/8848424.

Green, R., L. Cornelsen, A.D. Dangour, R. Turner, B. Shankar, M. Mazzocchi, and R.D. Smith. 2013. The effect of rising food prices on food consumption: Systematic review with meta-regression. British Medical Journal (clinical Research Edition) 346: f3703. https://doi.org/10.1136/bmj.f3703.

Gu, B.M., and J.G. Liu. 2022. Determinants of dry bulk ship** freight rates: Considering Chinese manufacturing industry and economic policy uncertainty. Transport Policy 129: 66–77. https://doi.org/10.1016/j.tranpol.2022.10.006.

Gu, Y.M., X.X. Dong, Z.X. Chen, and D. Lien. 2022. Evaluating the impact of COVID-19 on capesize and panamax sectors: The method of empirical mode decomposition. Maritime Policy and Management. https://doi.org/10.1080/03088839.2022.2143591.

Hayes, A. 2022. Commodity Research Bureau Index (CRBI): Definition and weightings. https://www.investopedia.com/terms/c/crb.asp.

High, I., S. Cheng, and X.R. Li. 2023. How economic policy uncertainty affects asymmetric spillovers in food and oil prices: Evidence from wavelet analysis. Resources Policy 86: 104086. https://doi.org/10.1016/j.resourpol.2023.104086.

Hua, J., H. Li, Z. He, J. Ding, and F.T. **. 2022. The microcosmic mechanism and empirical test of uncertainty on the non-linear fluctuation of Chinese grain prices-based on the perspective of global economic policy uncertainty. Agriculture 12 (10): 1526. https://doi.org/10.3390/agriculture12101526.

Hung, N.T. 2022. Effect of economic indicators, biomass energy on human development in China. Energy & Environment 33 (5): 829–852. https://doi.org/10.1177/0958305X211022040.

Leonov, Y., and V. Nikolov. 2012. A wavelet and neural network model for the prediction of dry bulk ship** indices. Maritime Economics Logistics 14: 319–333. https://doi.org/10.1057/mel.2012.10.

Liu, Y., X. ** network-transaction mechanism joint design model considering carbon tax and liner alliance. Ocean Coastal Management 212: 105817. https://doi.org/10.1016/j.ocecoaman.2021.105817.

Li, Y., and J. Li. 2021. How does China’s Economic Policy uncertainty affect the sustainability of its net grain imports? Sustainability 13: 6899. https://doi.org/10.3390/su13126899.

Long, S.B., J.Y. Li, and T.Y. Luo. 2023. The asymmetric impact of global economic policy uncertainty on international grain prices. Journal of Commodity Markets 30: 100273. https://doi.org/10.1016/j.jcomm.2022.100273.

Maiyar, L.M., and J.J. Thakkar. 2022. Robust optimisation of sustainable food grain transportation with uncertain supply and intentional disruptions. International Journal of Production Research 58 (18): 5651–5675. https://doi.org/10.1080/00207543.2019.1656836.

Mbah, R.E., and D. Wasum. 2022. Russian-Ukraine 2022 war: A review of the economic impact of Russian-Ukraine crisis on the USA, UK, Canada, and Europe. Advances in Social Sciences Research Journal 9 (3): 144–153. https://doi.org/10.14738/assrj.93.12005.

Mensi, W., M.U. Rehman, D. Maitra, K.H. Al-Yahyaee, and X.V. Vo. 2021. Oil, natural gas and BRICS stock markets: Evidence of systemic risks and co-movements in the time–frequency domain. Resources Policy 72: 102062. https://doi.org/10.1016/j.resourpol.2021.102062.

Mohammadi, Z., F. Barzinpour, and E. Teimoury. 2023. A location-inventory model for the sustainable supply chain of perishable products based on pricing and replenishment decisions: A case study. PLoS ONE 18 (7): e0288915. https://doi.org/10.1371/journal.pone.0288915.

Nuhu, A.S., L.S.O. Liverpool-Tasie, T. Awokuse, and S. Kabwe. 2021. Do benefits of expanded midstream activities in crop value chains accrue to smallholder farmers? Evidence from Zambia. World Development 143: 105469. https://doi.org/10.1016/j.worlddev.2021.105469.

OECD/FAO. 2021. OECD-FAO agricultural outlook 2021–2030. Paris: OECD Publishing. https://doi.org/10.1787/agr_outlook-2021-en.

OECD/FAO. 2022. OECD-FAO agricultural outlook 2022–2031. Paris: OECD Publishing. https://doi.org/10.1787/f1b0b29c-en.

Ozili, P.K. 2022. Global economic consequence of Russian invasion of Ukraine. SSRN. https://doi.org/10.2139/ssrn.4064770.

Schroeder, T.C., and B.K. Goodwin. 1991. Price discovery and cointegration for live hogs. Journal of Futures Markets 11: 685–696. https://doi.org/10.1002/fut.3990110604.

Sohag, K., M.M. Islam, Žiković I. Tomas, and H. Mansour. 2022. Food inflation and geopolitical risks: Analyzing European regions amid the Russia-Ukraie war. British Food Journal. https://doi.org/10.1108/BFJ-09-2022-0793.

Su, F., Y. Liu, S. Chen, and S. Fahad. 2023. Towards the impact of economic policy uncertainty on food security: Introducing a comprehensive heterogeneous framework for assessment. Journal of Cleaner Production. https://doi.org/10.1016/j.jclepro.2022.135792.

Torrence, C., and G.P. Compo. 1998. A practical guide to wavelet analysis. Bulletin of the American Meteorological Society 79 (1): 61–78. https://doi.org/10.1175/1520-0477(1998)079%3c0061:APGTWA%3e2.0.CO.2.

Torrence, C., and P.J. Webster. 1999. Interdecadal changes in the ENSO–monsoon system. Journal of Climate 12 (8): 2679–2690. https://doi.org/10.1175/1520-0442(1999)012%3c2679:ICITEM%3e2.0.CO.2.

USDA. 2020. Grain Prices, Basis, and Transportation 2020. https://agtransport.usda.gov/stories/s/Grain-Prices-Basis-and-Transportation/sjmk-tkh6/.

Vanek, F., and Y. Sun. 2008. Transportation versus perishability in life cycle energy consumption: A case study of the temperature-controlled food product supply chain. Transportation Research Part D: Transport and Environment 13 (6): 383–391. https://doi.org/10.1016/j.trd.2008.07.001.

Wellesley, L., F. Preston, J. Lehne, and R. Bailey. 2017. Chokepoints in global food trade: Assessing the risk. Research in Transportation Business & Management 25: 15–28. https://doi.org/10.1016/j.rtbm.2017.07.007.

Wright, B.D. 2012. International Grain Reserves: And Other Instruments to Address Volatility in Grain Markets. The World Bank Research Observer, World Bank Group 27 (2): 222–260.

**e, Q.W., L. Cheng, R.R. Liu, X.L. Zheng, and J.Y. Li. 2022. COVID-19 and risk spillovers of China’s major financial markets: Evidence from time-varying variance decomposition and wavelet coherence analysis. Finance Research Letters 52: 103545–103545. https://doi.org/10.1016/j.frl.2022.103545.

Xu, H., B. Tao, Y. Shu, and Y. Wang. 2021. Long-term memory law and empirical research on dry bulks ship** market fluctuations. Ocean and Coastal Management 213: 105838. https://doi.org/10.1016/j.ocecoaman.2021.105838.

Zhang, Z., R. Brizmohun, G. Li, and P. Wang. 2022. Does economic policy uncertainty undermine stability of agricultural imports? Evidence from China. PLoS ONE 17 (3): e0265279. https://doi.org/10.1371/journal.pone.0265279.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Acknowledgements

The authors are grateful for financial support from the national key research and development program of China (2022YFF0903403).

Appendices

Appendix 1: Methodology

1.1 Vector autoregression

A VAR model with k lags of N variables is expressed as follows.

where \({Y}_{t}={\left({y}_{1,t}{y}_{2,t}\dots {y}_{N,t}\right)}^{\mathrm{^{\prime}}}\), \(\mu ={\left({\mu }_{1}{\mu }_{2}\dots {\mu }_{N}\right)}{\prime}\), \({u}_{t}={\left({u}_{1t}{u}_{2t}\dots {u}_{Nt}\right)}^{^\prime}\),

\({\Pi }_{j}=\left[\begin{array}{ccc}{\pi }_{11.j}& \cdots & {\pi }_{1N.j}\\ \vdots & \ddots & \vdots \\ {\pi }_{N1.j}& \cdots & {\pi }_{NN.j}\end{array}\right]\), j = 1,2,…k.

\({Y}_{t}\) is the \({\text N}\times 1\)-order time-series column vector. \(\mu\) is the \({\text N}\times 1\)-order constant term column vector. \({\Pi }_{1}\), …,\({\Pi }_{k}\) are \({\text N}\times {\text N}\) parameter matrices. \({u}_{t}\sim\mathrm{IID}\left(0,\Omega \right)\) is a random error column vector of order \({\text N}\times 1\), where each element is non-autocorrelated, but there may be correlations between the random error terms corresponding to different equations. Since the right-hand side of each equation in the VAR model contains only lagged terms of the endogenous variables, which are uncorrelated with \({{\text{u}}}_{{\text{t}}}\), each equation can be estimated in turn using the OLS method, and the parameter estimates obtained are consistent.

In addition to satisfying the smoothness condition, the VAR model should be built with correctly determined lags k. If there are too few lags, the autocorrelation of the error terms can be severe and lead to non-consistent estimates of the parameters. This study utilizes the Akaike Information Criterion (AIC) for the selection of k values.

where \({\widehat{u}}_{t}\) denotes the residual, \({\text T}\) denotes the sample size, and k denotes the maximum lag order. The principle of choosing the value of k is to make the value of AIC as large as possible in the process of increasing the value of k.

The VAR model can be used to test whether there is a causal relationship between two variables. The test of whether there is a causal relationship between \({x}_{t}\) and \({y}_{t}\) can be done by testing whether all lags of \({x}_{t}\) can be eliminated from the equation in the VAR model with \({{\text{y}}}_{{\text{t}}}\) as the explanatory variable. For example, the equation in the VAR model with \({{\text{y}}}_{{\text{t}}}\) as the explanatory variable is expressed as follows.

Then the null hypothesis for testing the existence of Granger non-causality of \({x}_{t}\) on \({y}_{t}\) is \({{\text{H}}}_{0}:{\beta }_{1}={\beta }_{2}=\dots ={\beta }_{{\text{k}}}=0\). If there is significance in the estimates of the regression parameters for any of the lagged variables of \({x}_{t}\), the original hypothesis is rejected and there is Granger causality of \({x}_{t}\) on \({y}_{t}\).

1.2 Continuous wavelet transform

The XWT \({W}_{x}\left(s\right)\) finds regions in time–frequency space where the time series show high common power. The wavelet is given as follows:

where * represents the complex conjugate and the scale parameter \({\text{s}}\) determines whether the wavelet can recognize higher or lower elements of the series \(x\left(t\right)\), possible when the admissibility condition yields.

1.3 Wavelet coherence

The wavelet coherence technique (WTC) is efficient in capturing the localized interdependence through series in the time and frequency domains (Torrence and Compo 1998). The cross-wavelet of two series \(x\left(t\right)\) and \(y\left(t\right)\) can be written as follows:

where \({\text{u}}\) denotes the position, \(s\) is the scale, and * denotes the complex conjugate (Torrence and Webster 1999). The WTC can be calculated as follows:

where \(S\) connotes the smoothing process for both time and frequency at the same time. \({R}_{n}^{2}\left(s,\tau \right)\) is in the range \(0\le {R}^{2}\left(s,\tau \right)\le 1\).

The formula of the PWC tool, which allows us to determine the WTC between two series \(\left(y,{x}_{1}\right)\) after cancelling out the impact of a third series \(\left({x}_{2}\right)\), is as follows:

The PWC is expressed in squared form, i.e., \({RP}^{2}\). The value of PWC is between 0 and 1 (Mensi et al. 2021). \({RP}^{2}\left(y,{x}_{1},{x}_{2}\right)\) and \({RP}^{2}\left(y,{x}_{2},{x}_{1}\right)\) demonstrate the impacts of \({x}_{1}\) on y after eliminating \({x}_{2,}\) and \({x}_{2}\) on y after eliminating \({x}_{1}\), respectively.

The MWC approach has the power to explore the coherence of multiple variables on a single-dependent variable. Multiple wavelet coherency, like PWC, can be understood in terms of multiple correlations. Multiple wavelet coherency, as opposed to PWC, identifies and estimates the contributions of multiple independent variables \({x}_{1}\) and \({x}_{2}\) on a dependent variable y. As a result, MWC can be written as follows:

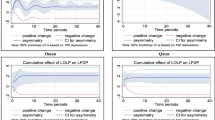

Appendix 2: A detailed analysis of Fig. 4

Figure 4 illustrates the coherence plots between GEPU, CRB, and BPI during the period of analysis for both PWC and MWC. Figure 4a displays the PWC between GEPU and CRB after removing the effect of BPI. Some significant correlations can be observed between GEPU and CRB at both low and medium frequencies at different time periods, corresponding to some red significant regions identified at different levels. Similarly, in the long term (32–64 months), there are some significant regions. However, in Fig. 4b, we observe a relatively different trend. The inclusion of the BPI indicator in the association between GEPU and CRB resulted in strong correlations in the high-frequency band regions throughout the sample period. In particular, this effect widens in 2004–2008 and 2018–2022. PWC and MWC identified a dramatic effect of BPI when examining the link between GEPU and CRB.

PWC describes the relationship between CRB and BPI after the removal of GEPU, as shown in Fig. 4c. There is a synergistic movement between CRB and BPI in the short- and long-term frequencies from 2000 to 2016, with strong fluctuations also seen in the short term from 2016 to 2018 and after 2020, as well as in some small areas in the long term. Fewer areas show stronger fluctuations in medium-term frequencies. In contrast, when considering GEPU in the context of the interrelationship between CRB and BPI, it is evident that a larger region of strong fluctuations is found in the corresponding medium-term frequencies from 2006 to 2010, as shown in Fig. 4d. Overall, PWC and MWC identified a considerable influence of GEPU when examining the relationship between CRB and BPI.

Figure 4e reports the PWC between BPI and GEPU after excluding the CRB indicator. Over the sample period, there is a more dispersed and strongly volatile relationship between BPI and GEPU on short- and medium-frequency scales. Similarly, Fig. 4f shows that this relationship is significantly stronger and spreads to higher-frequency scales. Figure 4f measures the MWC between BPI and GEPU using the effect of the CRB indicator. Extremely strong joint motion is detected at all frequencies. This implies that it is appropriate to consider the use of multivariate analysis.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Sun, L., Zhang, W., Hu, Z. et al. Food security under global economic policy uncertainty: fresh insights from the ocean transportation of food. Marit Econ Logist (2024). https://doi.org/10.1057/s41278-023-00282-w

Accepted:

Published:

DOI: https://doi.org/10.1057/s41278-023-00282-w