Abstract

We review the implications of an intertemporal representative consumer model for the analysis of housing prices, describing the choice between non-housing and housing consumption, and provide an explanation for the excess return of housing over the riskless rate based on weakly separable preferences. Further considerations are presented regarding the role of liquidity constraints. A Bayesian structural vector autoregression predicts relations between real rent growth, interest rates and housing prices consistently with the representative consumer model. The orthogonalized impulse response functions show, that housing prices are relatively unresponsive to shocks to fundamental value. The logarithmic rent/price ratio increases or does not significantly change following shocks to the real rent growth and relative bill rates. The dynamics of housing prices over the business cycle is mainly determined by financial factors. A shock to the natural logarithm of the rent/price ratio does not have significant predictive properties for subsequent real rent growth and relative bill rates. Moreover, the logarithmic rent/price ratio is a highly persistent variable displaying momentum and long term reversal.

Similar content being viewed by others

Data Availability

The datasets analysed in the present study are available in the Mendeley Data repository at https://doi.org/10.17632/db2s7rj27g.1.

Notes

The assumption of quasiconcavity requires the single period utility and the housing aggregator functions to have convex upper contour sets. The assumption of homotheticity requires the housing aggregator function to be an increasing transformation of a linearly homogeneous function. This in turn implies that the marginal rate of substitution between services from the housing stock and rentals is constant along a ray from the origin. In the text partial derivatives are denoted using subscript indices representing the function arguments.

The representative consumer can substitute rentals for owner occupied housing services and while owner occupied services are available from the stock purchase period, asset dividends accrue in the subsequent one. Therefore, asset prices are measured ex dividend in any time period, whereas housing stock prices are cum rent. Accounting for these differences the definitions of the real gross returns for assets and housing are comparable. The no arbitrage condition in addition requires the stochastic discount factor \(M_{t +1}\) to be identical with probability one in the two markets.

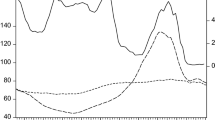

While aggregate measures have some limitations, due to the heterogeneity of the housing services produced from several different property types, both the housing price and rent indices are compiled applying procedures that account for quality changes. The Bank of Italy housing price series aggregates individual quotations controlling for dwelling size, type and location. The HICP actual rentals for housing series applies standard quality correction procedures. We find it convenient to introduce the statistical sources at this stage, in order to present some important stylized facts regarding housing price dynamics in Italy that will inform the interpretation of the econometric evidence in the following sections. Some further description of the statistical sources is given in Online Appendix D

The functions in (5.1) and (5.2) are not defined when either the intertemporal or the intratemporal elasticity of substitution is equal to one, although it can be shown that \(u\left( {\widetilde{X}}_{t}\right) \rightarrow \log {\widetilde{X}}_{t}\) for \(\sigma \rightarrow 1\) and \({\widetilde{X}}_{t} \rightarrow X_{ct}^{\alpha }X_{ht}^{1 -\alpha }\) for \(\epsilon \rightarrow 1\). The logarithmic or Cobb-Douglas specifications of the intertemporal and intratemporal aggregators should be used when \(\sigma =1\) or \(\varepsilon =1\).

Comparable results regarding the implications of observed excess returns for the coefficient of relative risk aversion and the intertemporal rate of time preference are usually obtained in financial markets, as for instance reviewed in Mehra (2003). In order to address the equity premium puzzle Lettau and Ludvigson (2001a, 2001b) following Campbell and Mankiw (1989) have suggested modelling the stochastic discount factor as a function of the consumption-asset-income ratio (cay), which is defined as a cointegrating residual between the logarithmic transformation of aggregate consumption, asset wealth and labour income variables. Similarly to more traditional indicators as the natural logarithm of the dividend/price ratio, the cay has good predictive properties for financial market returns.

In order to specify the model lag length, we exploited the property that Bayesian posterior distributions converge to ordinary least squares (OLS) estimates as the sample size grows. Selection criteria applied to OLS estimates of the reduced form model suggest a lag of order three. With this specification the model is stable and therefore the endogenous variables may be assumed to be stationary. Furthermore, Lagrange multiplier tests of residual serial correlation and heteroskedasticity tests support the assumption that the model disturbances are independent and identically distributed over time.

We should recall, that in the classical approach to identification the ordering of the variables in the vector \(y_{t}\) plays a key role, as both the structural and the Cholesky matrices \(A =H^{ -1}\)and H are lower triangular. In the recursive system resulting from application of the Cholesky decomposition each variable is contemporaneously related to the preceding ones in the variable ordering. The orthogonal transformation of a recursive system requires additional information for identification, for instance long run restrictions as in Blanchard and Quah (1989) and Galí (1999).

An explicit derivation of Eq. (6.3) is included in Online Appendix C.

In order to envisage the effect of the relative bill rate on the real rent growth rate, it is useful to first consider the additively separable single period utility function case: \(\sigma =\varepsilon \) and \(M_{wt +1} =1\). The result then follows from the definition of the stochastic discount factor component \(M_{ct +1}\). For weakly separable preferences we suppose the ensuing changes in the non-housing consumption good share do not have a consequence for the direction of change of the real rent growth rate. Finally, we assume the identification restrictions are robust to the presence of collateral constraints.

An advanced discussion of the subject of Bayesian inference, with emphasis on the analysis of dynamic models, can be found in Bauwens et al. (1999).

We denote with \(t^{ +}\left( \mu ,\sigma ,\nu \right) \) or \(t^{ -}\left( \mu ,\sigma ,\nu \right) \) a Student’s t random variable with location, scale and degrees of freedom parameters \(\mu \), \(\sigma \) and \(\nu \) restricted to be either positive or negative. The properties of the Student’s t distribution are a function of the degrees of freedom parameter \(\nu \). The Student’s t is equivalent to a Cauchy distribution for \(\nu =1\) and converges to the normal distribution for \(\nu \rightarrow +\infty \). The mean of a Student’s t variable is equal to the location parameter \(\mu \) for \(\nu >1\) and its variance is equal to \(\sigma ^{2}\nu /\left( \nu -2\right) \) for \(\nu >2\). Our choice of a degrees of freedom parameter \(\nu =3\) implies a higher degree of uncertainty on the assumptions about the location than specified by the scale parameters. An overview of statistical distributions and their properties can be found in Rao (1973).

The choice of the lag order in the estimated autoregression for each endogenous variable is consistent with the VAR model specification and the Minnesota prior.

In actual computations the posterior density of A is defined up to a normalizing multiplicative constant. More details on the application of the Metropolis-Hastings algorithm are specified in Baumeister and Hamilton (2015), for an overview of Markov chain Monte Carlo methods we suggest Tierney (1994) and Chib and Greenberg (1995).

The reduced form model (6.2) implies \(\Psi _{0} =I_{n}\) and \(\Psi _{\tau }\) equal to the block composed from the first n rows and columns of the \(mn \times mn\) matrix \(\genfrac[]{0.0pt}{}{\Phi _{1}}{\begin{array}{cc}I_{\left( m -1\right) n}&0\end{array}}^{\tau }\), where \(\Phi _{1}\) is the \(n \times mn\) matrix formed from the first mn columns of \(\Phi \).

References

Arias JE, Rubio-Ramírez JF, Waggoner DF (2018) Inference based on structural vector autoregressions identified with sign and zero restrictions: theory and applications. Econometrica 86(2):685–720

Baumeister C, Hamilton JD (2015) Sign restrictions, structural vector autoregressions, and useful prior information. Econometrica 83(5):1963–1999

Baumeister C, Hamilton JD (2018) Inference in structural vector autoregressions when the identifying assumptions are not fully believed: re-evaluating the role of monetary policy in economic fluctuations. J Monetary Econ 100:48–65

Bauwens L, Lubrano M, Richard J-F (1999) Bayesian inference in dynamic econometric models. Oxford University Press, Oxford

Benveniste LM, Scheinkman JA (1979) On the differentiability of the value function in dynamic models of economics. Econometrica 47(3):727–732

Blanchard OJ, Quah D (1989) The dynamic effects of aggregate demand and supply disturbances. Am Econ Rev 79(4):655–673

Campbell JY, Cocco JF (2003) Household risk management and optimal mortgage choice. Q J Econ 118(4):1449–1494

Campbell JY, Cocco JF (2007) How do house prices affect consumption? Evidence from micro data. J Monetary Econ 54(3):591–621

Campbell JY, Mankiw NG (1989) Consumption, income and interest rates: reinterpreting the time series evidence. In: Blanchard OJ, Fischer S (eds) NBER Macroeconomics Annual 1989, vol 4. MIT Press, Cambridge, pp 185–216

Case KE, Quigley JM, Shiller RJ (2013) Wealth effects revisited: 1975–2012. Crit Finance Rev 2(1):101–128

Chib S, Greenberg E (1995) Understanding the Metropolis-Hastings Algorithm. Am Stat 49(4):327–335

Deaton A (1991) Saving and liquidity constraints. Econometrica 59(5):1121–1248

Deaton A (1992) Understanding consumption, Clarendon Lectures in Economics. Clarendon Press, Oxford

Doan T, Litterman R, Sims C (1984) Forecasting and conditional projection using realistic prior distributions. Econom Rev 3(1):1–100

Fabozzi FJ, Bhattacharya AK, Berliner WS (2008) Residential mortgages. In: Fabozzi FJ (ed) Handbook of finance. Wiley, Hoboken, pp 221–230

Galí J (1999) Technology, employment, and the business cycle: do technology shocks explain aggregate fluctuations? Am Econ Rev 89(1):249–271

Greenwood R, Shleifer A (2014) Expectations of returns and expected returns. Rev Financ Stud 27(3):714–746

Hansen LP, Jagannathan R (1991) Implications of security market data for models of dynamic economies. J Political Econ 99(2):225–262

Hansen LP, Richard SF (1987) The role of conditioning information in deducing testable restrictions implied by dynamic asset pricing models. Econometrica 55(3):587–613

Lettau M, Ludvigson S (2001a) Consumption, aggregate wealth, and expected stock returns. J Finance 56(3):815–849

Lettau M, Ludvigson S (2001b) Resurrecting the (C)CAPM: a cross-sectional test when risk premia are time varying. J Political Econ 109(6):1238–1287

Litterman RB (1986) Forecasting with Bayesian vector autoregressions: five years of experience. J Bus Econ Stat 4(1):25–38

Lustig HN, Van Nieuwerburgh SG (2005) Housing collateral, consumption insurance, and risk premia: an empirical perspective. J Finance 60(3):1167–1219

Mehra R (2003) The equity premium: why is it a puzzle? Financ Anal J 59(1):54–69

Muellbauer J (2012) When is a housing market overheated enough to threaten stability? In: Heath A, Packer F, Windsor C (eds) Property markets and financial stability. Reserve Bank of Australia, Sydney, pp 73–105

Muellbauer J (2022) Real estate booms and busts: implications for monetary and macroprudential policy in Europe. European Central Bank, ECB Forum on Central Banking

Piazzesi M, Schneider M, Tuzel S (2007) Housing, consumption and asset pricing. J Financ Econ 83(3):531–569

Rao CR (1973) Linear statistical inference and its applications. Wiley, New York

Rubio-Ramírez JF, Waggoner DF, Zha T (2010) Structural vector autoregressions: theory of identification and algorithms for inference. Rev Econ Stud 77(2):665–696

Shiller RJ (1982) Consumption, asset markets and macroeconomic fluctuations. Carnegie-Rochester Conference Series on Public Policy 17:203–238

Shiller RJ, Wojakowski RM, Ebrahim MS, Shackleton MB (2019) Continuous workout mortgages: efficient pricing and systemic implications. J Econ Behav Organ 157:244–274

Sims CA, Zha T (1998) Bayesian methods for dynamic multivariate models. Int Econ Rev 39(4):949–968

Tierney L (1994) Markov chains for exploring posterior distributions. Ann Stat 22(4):1701–1728

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The final version of this work benefited from my participation to the Fifteenth Paolo Baffi Lecture on Money and Finance delivered by Nobuhiro Kiyotaki at the Bank of Italy in 2021: “Horizons of Credit”. The comments and suggestions of two anonymous referees are also gratefully acknowledged. The views expressed herein are those of the author and do not necessarily reflect those of the Bank of Italy.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Tomat, G.M. Bayesian Inference in a Structural Model of Family Home Prices. Ital Econ J (2024). https://doi.org/10.1007/s40797-023-00259-x

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s40797-023-00259-x