Abstract

Due to the non-separability of the variance term, the dynamic mean–variance (MV) portfolio optimization problem is inherently difficult to solve by dynamic programming. Li and Ng (Math Finance 10(3):387–406, 2000) and Zhou and Li (Appl Math Optim 42(1):19–33, 2000) develop the pre-committed optimal policy for such a problem using the embedding method. Following this line of research, researchers have extensively studied the MV portfolio selection model through the inclusion of more practical investment constraints, realistic market assumptions and various financial applications. As the principle of optimality no longer holds, the pre-committed policy suffers from the time-inconsistent issue, i.e., the optimal policy computed at the intermediate time t is not consistent with the optimal policy calculated at any time before time t. The time inconsistency of the dynamic MV model has become an important yet challenging research topic. This paper mainly focuses on the multi-period mean–variance (MMV) portfolio optimization problem, reviews the essential extensions and highlights the critical development of time-consistent policies.

Similar content being viewed by others

Notes

The filtration \({\mathcal {F}}_t\) represents the information available at time t (see [10] for detail of discrete-time market model).

If the first asset is the benchmark, the wealth dynamic becomes \(x_{t+1} = r^1_t x_t + {\hat{\varvec{r}}}_t^{\top } {\hat{\varvec{u}}}_t\), where \({\hat{\varvec{r}}}_t=(r^2_t - r^1_t, r^3_t - r^1_t,\cdots , r^n_t- r^1_t)^{\top }\) is the excess return vector and \({\hat{\varvec{u}}}_t \in {\mathbb {R}}^{n-1}\) is the truncated decision vector of \(\varvec{u}_t\).

Similar model is also considered in [11].

If the risk-free rate is random, then it becomes the similar model with all assets being risky.

In this paper, we define the boundary of the product term as \(\prod _{k=t_1}^{t_2} a_k =1\) if \(t_1>t_2\).

We re-calibrate the date given in Example 1 in [5] from yearly based statistics to the monthly based ones. Then, \(T=12\) means that the investment horizon is 12 months.

We adopt the similar data for Fig. 1(a) and set \(T=12\) months. As for the static MV model, we regard the whole horizon \(T=12\) as a single period and solve the static MV portfolio selection for the buy and hold policy. We then simulate 5000 sample paths of the return vector and compute the terminal wealth for different policies.

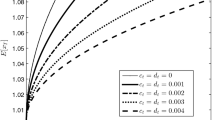

Comparing with [9], one important extension given in [22] is that it drops the nonnegative assumption \(\text {E}[\varvec{p}_t\varvec{p}_t^{\top }]^{-1}\text {E}[\varvec{p}_t]\geqslant 0\) for \(t=0,\cdots ,T-1\). The new setting fits the fact that the expected value of premium vectors may be negative in the time-varying market.

Take the practice of AIS as an example. For investors with assets under management (AUM) between US$100,000 and US$250,000, the annual fee charged by AIS is 0.80% of AUM or US$1,500, whichever is greater.

The time-consistent mean–variance policies in the market with all risky assets can be found in [56].

A more detailed comparison between the pre-committed policy and different types of time-consistent policies can be found in [60].

References

Markowitz, H.M.: Portfolio selection. J. Financ. 7(1), 1063–1070 (1952)

Ao, M.M., Li, Y.Y., Zheng, X.H.: Approaching mean-variance efficiency for large portfolios. Rev. Financ. Stud. 32(7), 2890–2919 (2019)

Kolm, P.N., Tütüncü, R.: 60 years of portfolio optimization: practical challenges and current trends. Eur. J. Oper. Res. 234(2), 356–371 (2014)

Mencarelli, L., Ambrosio, C.D.: Complex portfolio selection via convex mixed-integer quadratic programming: a survey. Int. Trans. Oper. Res. 26(2), 389–414 (2019)

Li, D., Ng, W.L.: Optimial dynamic portfolio selection: multiperiod mean-variance formulation. Math. Finance 10(3), 387–406 (2000)

Zhou, X.Y., Li, D.: Continuous-time mean-variance portfolio selection: a stochastic LQ framework. Appl. Math. Optim. 42(1), 19–33 (2000)

Gârleanu, N., Pedersen, L.H.: Dynamic trding with predictable returns and transaction cost. J. Financ. 68(6), 2309–2340 (2013)

Li, B., Hoi, S.C.H.: Online portfolio selection: a survey. ACM Comput. Surev. 46(3), 1–36 (2014)

Cui, X.Y., Gao, J.J., Li, X., Li, D.: Optimal multi-period mean-variance policy under no-shorting constraint. Eur. J. Oper. Res. 234(2), 459–468 (2014)

Föllmer, H., Schied, A.: Stochastic Finance: An Introduction in Discrete Time. De Gruyter Studies in Mathematics. Walter De Gruyter, Berlin (2004)

Yao, H.X., Li, Z.F., Li, X.Y.: The premium of dynamic trading in a discrete-time setting. Quant. Financ. 16(8), 1237–1257 (2016)

Gao, J.J., Li, D., Cui, X.Y., Wang, S.Y.: Time cardinality constrained mean-variance dynamic portfolio selection and market timing: a stochastic control approach. Automatica 54, 91–99 (2015)

Gao, J.J., Li, D.: Multiperiod mean-variance portfolio optimization with general correlated returns. IFAC Proc. 47, 9007–9012 (2014)

Chiu, C.H., Zhou, X.Y.: The prmium of dynamic trading. Quant. Financ. 11, 115–123 (2011)

van Staden, P.M., Dang, D.M., Forsyth, P.A.: On the distribution of terminal wealth under dynamic mean-variance optimal investment strategies. SIAM. J. Financ. Math 12(2), 566–603 (2020)

van Staden, P.M., Dang, D., Forsyth, P.A.: The surprising robustness of dynamic mean-variance portfolio optimization to model misspecification error. Eur. J. Oper. Res. 289, 774–792 (2021)

Yao, H., Lai, Y., Ma, Q., Jian, M.: Asset allocation for a dc pension fund with stochastic income and mortality risk: a multi-period mean-variance framework. Insur. Math. Econ. 54, 84–92 (2014)

Chiu, M.C., Wong, H.Y.: Mean-variance asset-liability management with asset correlation risk and insurance liabilities. Insur. Math. Econ. 59, 300–310 (2014)

Yao, H., Chen, P., Li, X.: Multi-period defined contribution pension funds investment management with regime-switching and mortality risk. Insur. Math. Econ. 71, 103–113 (2016)

Zhang, L., Zhang, H., Yao, H.: Optimal investment management for a defined contribution pension fund under imperfect information. Insur. Math. Econ. 79, 210–224 (2018)

Sun, Z., Zhang, X., Yuen, K.C.: Mean-variance asset-liability management with affine diffusion factor process and a reinsurance option. Scand. Actuar. J. 2020(3), 218–244 (2020)

Wu, W.P., Gao, J.J., Li, D., Shi, Y.: Explicit solution for constrained scalar-state stochastic linear-quadratic control with multiplicative noise. IEEE Trans. Autom. Control 64, 1999–2012 (2019)

Li, X., Zhou, X.Y., Lim, A.E.B.: Dynamic mean-variance portfolio selection with no shorting constraints. SIAM J. Control Optim. 40(5), 1540–1555 (2002)

Hu, Y., Zhou, X.Y.: Constrained stochastic LQ control with random coefficients, and application to portfolio selection. SIAM J. Control Optim. 44(2), 444–466 (2005)

Cui, X.Y., Li, D., Li, X.: Mean-variance policy for discrete-time cone constrained markets: the consistency in efficiency and minimum-variance signed supermartingale measure. Math. Financ. 27(2), 471–504 (2017)

Costa, O.L.V., Oliveira, A.D.: Optimal mean-variance control for discrete-time systems with Markovian jumps and multiplicative noises. Automatica 48(2), 304–315 (2012)

Zhu, S.S., Li, D., Wang, S.Y.: Risk control over bankruptcy in dynamic portfolio selection: a generalized mean-variance formulation. IEEE Trans. Autom. Control 49(3), 447–457 (2004)

Li, C., Li, Z.: Multi-period portfolio optimization for asset-liability management with bankrupt control. Appl. Math. Comput. 218, 11196–11208 (2012)

Costa, O., Nabholz, R.: Multiperiod mean-variance optimization with intertemporal restrictions. J. Optim. Theory Appl. 134(2), 257–274 (2007)

Xu, Y., Li, Z.F.: Dynamic portfolio selection based on serially correlated return-dynamic mean-variance formulation. Syst. Eng. Theory Pract. 18(8), 123–131 (2008)

Dokuchaev, N.: Discrete time market with serial correlations and optimal myopic strategies. Eur. J. Oper. Res. 177, 1090–1104 (2007)

Çakmak, U., Özekici, S.: Portfolio optimization in stochastic markets. Math. Methods Oper. Res. 63, 151–168 (2005)

Wu, H., Li, Z.F.: Multi-period mean-variance portfolio selection with regime switching and a stochastic cash flow. Insur. Math. Econ. 50(3), 371–384 (2012)

Yao, H., Lai, Y., Hao, Z.: Uncertain exit time multi-period mean-variance portfolio selection with dndogenous liabilities and markov jumps. Automatica 49(11), 3258–3269 (2013)

Wu, H., Zeng, Y., Yao, H.X.: Multi-period Markowtiz’s mean-variance portfolio selection with state-dependent exit probability. Econ. Model. 36, 69–78 (2014)

Herzog, F., Dondi, G., Geering, H.P.: Stochastic model predictive control and portfolio optimization. Int. J. Theor. Appl. Finance 10(2), 981–1000 (2007)

Boyd, S., Busseti, E., Diamond, S., Kahn, R.N., Koh, K., Nystrup, P.: Multi-period trading via convex optimization. Found. Trends Opt. 3(1), 1–76 (2017)

Nystrup, P., Boyd, S., Lindström, E., Madsen, H.: Multi-period portfolio selection with drawdown control. Ann. Oper. Res. 282, 245–271 (2017)

Cong, F., Oosterlee, C.W.: Multi-period mean-variance portfolio optimization based on Monte–Carlo simulation. J. Econ. Dyn. Control 64, 23–38 (2016)

Basak, S., Chabakauri, G.: Dynamic mean-variance asset allocation. Rev. Financ. Stud. 23(8), 2970–3016 (2010)

Strotz, R.H.: Myopia and inconsistency in dynamic utility maximization. Rev. Econ. Stud. 23(3), 165–180 (1955)

O’Donoghue, T., Rabin, M.: Doing it now or later. Am. Econ. Rev. 89(1), 103–124 (1999)

Grenadier, S.R., Wang, N.: Investment under uncertainty and time-inconsistent preferences. J. Financ. Econ. 84(1), 2–39 (2007)

Wu, H.: Time-consistent strategies for a multiperiod mean-variance portfolio selection problem. J. Appl. Math., Article ID , 841627 (2013)

Wu, H., Chen, H.: Nash equilibrium strategy for a multi-period mean-variance portfolio selection problem with regime switching. Econ. Model. 46, 79–90 (2015)

Wang, L., Chen, Z.: Nash equilibrium strategy for a dc pension plan with state-dependent risk aversion: a multiperiod mean-variance framework. Discrete. Dyn. Nat. Soc., Article ID , 7581231 (2018)

**ao, H., Ren, T., Bai, Y., Zhou, Z.: Time-consistent investment-reinsurance strategies for the insurer and the reinsurer under the generalized mean-variance criteria. Mathematics 7(9), 857 (2019)

Zeng, Y., Li, Z., Lai, Y.: Time-consistent investment and reinsurance strategies for mean-variance insurers with jumps. Insur. Math. Econ. 52(3), 498–507 (2013)

Lin, X., Qian, Y.: Time-consistent mean-variance reinsurance-investment strategy for insurers under CEV model. Scand. Actuar. J. 2016(7), 646–671 (2016)

Zhang, Y., Wu, Y., Li, S., Wiwatanapataphee, B.: Mean-variance asset liability management with state-dependent risk aversion. N. Am. Actuar. J. 21(1), 87–106 (2017)

Chen, K., Wong, H.Y.: Time-consistent mean-variance hedging of an illiquid asset with a cointegrated liquid asset. Financ. Res. Lett. 29, 184–192 (2019)

Zhang, L., Li, D., Lai, Y.: Equilibrium investment strategy for a defined contribution pension plan under stochastic interest rate and stochastic volatility. J. Comput. Appl. Math. 368, 112536 (2020)

Zhao, Q., Shen, Y., Wei, J.: Mean-variance investment and contribution decisions for defined benefit pension plans in a stochastic framework. J. Ind. Manag. Optim. 17(3), 1147–1171 (2021)

Björk, T., Murgoci, A., Zhou, X.Y.: Mean-variance portfolio optimization with state-dependent risk aversion. Math. Financ. 24(1), 1–24 (2014)

Hu, Y., **, H., Zhou, X.Y.: Time-inconsistent stochastic linear-quadratic control. SIAM J. Control. Optim. 50(3), 1548–1572 (2012)

Pun, C.S.: Time-consistent mean-variance portfolio selection with only risky assets. Econ. Model. 75, 281–292 (2018)

Cui, X.Y., Li, X., Li, D., Shi, Y.: Time consistent behavioral portfolio policy for dynamic mean-variance formulation. J. Oper. Res. Soc. 68(12), 1647–1660 (2017)

Wang, J., Forsyth, P.A.: Continuous time mean variance asset allocation: a time-consistent strategy. Eur. J. Oper. Res. 209(2), 184–201 (2011)

Cong, F., Oosterlee, C.W.: On pre-committed aspects of a time-consistent strategy for a mean-variance investor. J. Econ. Dyn. Control 70, 178–193 (2016)

Van Staden, P.M., Dang, D.-M., Forsyth, P.A.: On the distribution of terminal wealth under dynamic mean-variance optimal investment strategies. SIAM. J. Financ. Math 12(2), 566–603 (2021)

Cui, X.Y., Li, D., Shi, Y.: Self-coordination in time inconsistent stochastic decision problems: a planner-doer game framework. J. Econ. Dyn. Control 75, 91–113 (2017)

Ni, Y.-H., Si, B., Zhang, X.: Yet the game between precommitted policy and time-consistent policy. ar**v preprint ar**v:1908.03728 (2019)

Cui, X.Y., Li, D., Wang, S., Zhu, S.: Better than dynamic mean-variance: time inconsistency and free cash flow stream. Math. Financ. 22(2), 346–378 (2012)

Zhu, S., Li, D., Wang, S.: Myopic Efficiency in Multi-period Portfolio Selection with a Mean-variance Formulation, pp. 53–74. Global-Link Publisher, Hong Kong (2003)

Bäuerle, N., Grether, S.: Complete markets do not allow free cash flow streams. Math. Methods Oper. Res. 81(2), 137–146 (2015)

Dang, D.-M., Forsyth, P.A.: Better than pre-committed mean-variance portfolio allocation strategies: a semi-self-financing Hamilton–Jacobi–Bellman equation approach. Eur. J. Oper. Res. 250(3), 827–841 (2016)

Bengen, W.P.: Determining withdrawal rates using historical data. J. Financ. Plan. 7(4), 171–180 (1994)

Dang, D.-M., Forsyth, P.A., Vetzal, K.R.: The 4% strategy revisited: a pre-commitment mean-variance optimal approach to wealth management. Quant. Financ. 17(3), 335–351 (2017)

Cui, X.Y., Gao, J.J., Shi, Y., Zhu, S.S.: Time-consistent and self-coordination strategies for multi-period mean-Conditional Value-at-Risk portfolio selection. Eur. J. Oper. Res. 276(2), 781–789 (2019)

Gao, J.J., Zhou, K., Li, D.: Dynamic mean-LPM and mean-CVaR portfolio optimization in continuous time. SIAM J. Control. Optim. 55(3), 1377–1397 (2017)

Huang, X., Li, D.: A two-level reinforcement learning algorithm for ambiguous mean-variance portfolio selection problem. In: IJCAI, pp. 4527–4533 (2020)

Wang, H.R., Zhou, X.Y.: Continuous-time mean-variance portfolio selection: A reinforcement learning framework. Math. Financ. 30(4), 1273–1308 (2020)

Wang, H., Zariphopoulou, T., Zhou, X.Y.: Reinforcement learning in continuous time and space: a stochastic control approach. J. Mach. Learn. Res. 21(198), 1–24 (2020)

Acknowledgements

All the authors of this paper would like to thank Professor Duan Li for his guidance, help and encouragement during their Ph.D. and postdoctoral time at the Chinese University of Hong Kong.

Author information

Authors and Affiliations

Corresponding author

Additional information

This paper is dedicated to the late Professor Duan Li in commemoration of his contributions to optimization, financial engineering, and risk management.

This work is partially supported by the National Natural Science Foundation of China (Nos. 71971132, 61573244, 71671106, 71971083 and 72171138), by the Key Program of National Natural Science Foundation of China (No. 71931004), by Shanghai Institute of International Finance and Economics, by Program for Innovative Research Team of Shanghai University of Finance and Economics and by the Open Research Fund of Key Laboratory of Advanced Theory and Application in Statistics and Data Science-MOE.

Rights and permissions

About this article

Cite this article

Cui, XY., Gao, JJ., Li, X. et al. Survey on Multi-period Mean–Variance Portfolio Selection Model. J. Oper. Res. Soc. China 10, 599–622 (2022). https://doi.org/10.1007/s40305-022-00397-6

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40305-022-00397-6