Abstract

This paper investigates the impact of recent recessions on the origins of productivity growth. We show how business cycles affect productivity growth, with particular attention for the impact of job reallocation and labor hoarding. We find evidence that recessions induce productivity enhancing job reallocation in manufacturing but not in services industries and show that labor hoarding mitigates this cleansing effect of recessions. Furthermore, we show how entry and exit of firms and industry dynamics shape the evolution of aggregate productivity.

Plain English Summary

During recessions, governments support firms via temporary unemployment programs to save jobs. A side effect is that job reallocation and exit of low-productive firms can be distorted, while such cleansing effects typically spur productivity growth. This paper investigates how recessions affect productivity growth, with particular attention for the impact of job reallocation and labor hoarding. We find evidence that recessions induce productivity enhancing job reallocation in manufacturing but not in services industries and show that labor hoarding mitigates this cleansing effect of recessions. Furthermore, we show how entry and exit of firms and industry dynamics shape the evolution of aggregate productivity. As many developed economies struggle with a slowdown in productivity growth, it is important that policy makers understand the impact of recessions on the micro origins of productivity growth and are aware of how temporary policies during recessions could affect long-term productivity growth.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Recessions induce negative demand shocks in firms, which reduces the demand for input factors. In flexible labor markets like the USA, firms can easily shed jobs, thereby cleansing out unproductive labor inputs and increasing aggregate productivity. In Europe, hiring and firing employees is more costly. Labor market rigidities impose a significant financial burden on firms that want to shed jobs in economic recessions. To help firms weather economic downturns like the COVID-19 crisis and the Great Recession, many countries introduce temporary unemployment policies. Such policies typically provide tax cuts and government support for firms that reduce working hours, conditional on retaining their employees.Footnote 1 The idea of such programs is to avoid excessive layoffs so that families preserve their income and to allow firms to hoard labor, i.e., preserve human capital in order to catch up quickly when the economy recovers. While many OECD countries incorporated such programs during the Great Recession, Belgium was exceptional because it was one of the few countries where the government supported firms to the extent that they did not bear any cost of the reduction in labor hours. With a take-up rate of 6% of all employees, Belgium had the highest proportion of temporarily unemployed during the Great Recession (Hijzen & Venn, 2011). This makes Belgium an interesting case study to investigate how labor hoarding relates to job reallocation and productivity growth. To the best of our knowledge, we are the first to investigate this relation.

Recessions can induce more efficient resource allocation by driving out unproductive investments and thereby freeing up resources for more productive uses. Foster et al. (2016) show for the USA that the intensity of job reallocation during the recent Great Recession was relatively low and less productivity enhancing than in previous recessions. If productivity enhancing job reallocation was low in the USA, that has a relatively flexible labor market, did this occur at all in economies with more rigid labor markets, like those in Europe? To answer this research question, this paper will investigate different microchannels of aggregate productivity growth in Belgium, that is known to have a relatively rigid labor market.Footnote 2 More particularly, this paper will answer the following questions: did recent recessions have a “cleansing effect,” i.e., was productivity growth due to firm exit or due to job reallocation higher in recession periods than in non-recession periods? To what extent did labor hoarding mitigate job reallocation? How does productivity growth through entry and exit of firms differ between recession and non-recession periods? How do manufacturing and services industries differ in realizing productivity growth over the business cycle?

We use firm-level data on all incorporated manufacturing and services firms in Belgium for the period 1997–2014 and rely on productivity decompositions developed by Melitz and Polanec (2015) and Foster et al. (2001) to measure the contribution of job reallocation and exit to aggregate productivity growth. As in Bartelsman et al. (2013), we use the size-productivity covariance to measure how efficient job allocation is. The higher the covariance, the more jobs are allocated to more efficient firms. We also investigate how the impact of job reallocation on productivity growth is affected by labor hoarding. We can measure this since we have information on the number of full-time equivalents, which does not account for labor hoarding, and hours worked, which does account for labor hoarding.

Our results show that changes in the size-productivity covariance made a persistent contribution to aggregate productivity growth, while fluctuations in within-firm productivity drive the cyclicality of productivity growth. We find evidence on cleansing effects of recessions through job reallocation, but the magnitude of the cleansing effect is higher when jobs are measured in hours worked than when jobs are measured in full-time equivalents, which reflects labor hoarding. As labor hoarding was basically free during the Great Recession (see supra), we take the estimates based on hours worked as a proxy for the behavior of firms in a completely flexible labor market, where they would statically optimize their demand for labor. We calculate that aggregate productivity growth would have been one percentage point higher during the Great Recession if the hoarded labor would have been dismissed. Regarding the return on labor hoarding, we find short-term productivity premia after hoarding labor in young and small firms, but these were not large enough to offset the productivity deficit that was present in labor hoarding firms ex ante. All in all, labor hoarding did not improve productivity in the long run. Industry differences appear to be crucial in understanding the origins of aggregate productivity growth. Cleansing in the form of productivity enhancing job reallocation only occurred in manufacturing industries, despite the largest part of Belgian firms are active in services industries. Altogether, our findings indicate that recessions do not homogeneously cleanse the economy and that the facilitation of labor hoarding can distort job reallocation and exit of low-productive firms, while such cleansing effects of recessions spur productivity growth. During the COVID-19 crisis, the government again introduced generous labor hoarding policies. While this will save jobs in the short run, our findings indicate that we cannot expect this to increase productivity in the long run.

The remainder of this paper will be organized as follows. Section 2 provides an overview of the relevant literature. Section 3 presents the empirical framework that will be used to compose aggregate productivity levels and decompose productivity growth from the macro level to its foundations on the micro level. Section 4 describes the data. Section 5 presents and discusses the results. Section 6 concludes by summarizing our main findings.

2 Literature review

Productivity growth is not everything, but in the long run, it is almost everything (Krugman, 1997). Gains in productivity, or the efficiency with which inputs are turned into outputs, account for a substantial fraction of cross country differences in income (Hall & Jones, 1999). Therefore, understanding the evolution of aggregate productivity is a central topic in economics. Empirical research has shown that the macroeconomic idea of one representative firm does not tally with reality. Instead, there is tremendous heterogeneity in productivity between firms, even within narrowly defined industries (Syverson, 2004). Criscuolo (2018) finds the gap in productivity levels between firms the top and bottom of the productivity distribution increased over the past decades. The finding of enormous differences in productivity spurred the development of a large literature on determinants of productivity differences. Owalla et al. (2021) provide an excellent review of drivers of these productivity differences, focused on the SMEs.

Due to heterogeneity in productivity at the firm level, aggregate productivity growth can arise when resources are reallocated towards high-productivity firms. Olley and Pakes (1996) and Bartelsman et al. (2013) compute the covariance between size and productivity. The larger this covariance, the more market share is allocated to more productive firms and thus the more efficient the resource allocation. They show that changes in this covariance between size and productivity play a key role in the aggregate productivity evolution and in explaining cross country differences in productivity. Van Beveren and Vanormelingen (2014) find resource reallocation to be the most stable determinant of aggregate productivity growth in Belgium. Decker et al. (2017) observe a deceleration of reallocation in the USA and find this to be closely related to the slowdown in aggregate productivity growth.

Caballero and Hammour (1994) developed a formal model that incorporates the cleansing of less efficient production arrangements such that more resources become available for production arrangements that are relatively more productive. Another way through which recessions can cleanse the economy, without actual firm exit, is through job losses in incumbent firms. When low-productive firms shed jobs, aggregate productivity will increase because of a composition effect, as in Solon et al. (1994) and Petrosky-Nadeau (2013). Recently, the COVID-19 crisis had a strong negative impact on firm-level productivity growth, but this effect is partially offset because the least productive sectors and firms are most affected (Bloom et al., 2020). The cleansing mechanism would suggest increased gross job reallocation during recessions from job destruction that is higher than job creation (Davis & Haltiwanger, 1992).

The literature proposes various factors that could distort the cleansing mechanism. Firms could do labor hoarding, which would mitigate job reallocation in recession periods. Also, recessions could affect plant level productivity negatively and this could in itself dominate the increase in aggregate productivity due to cleansing. Furthermore, Barlevy (2002) argues that recessions could have a sullying effect because they tend to slow down the matching of newly unemployed with high-productivity jobs. Moscarini and Postel-Vinay (2016) introduce a model where high-productivity firms are growing faster than less-productive firms in expansions as they can offer higher wages while less-productive firms must rely on the pool of unemployed workers to fill their vacancies. In recessions, this mechanism collapses, thereby lowering productivity growth. Altogether, it is not obvious a priori how the business cycle affects the contribution of job reallocation on aggregate productivity. Haltiwanger et al. (2021) use linked employer-employee data and find prove of both cleansing and sullying effects. All in all, worker reallocation contributes more to overall productivity growth during recessions than during upturns as the sullying effects are more present after the crisis when unemployment is still above average.

Entry and exit also have an important role in aggregate productivity dynamics (Clementi & Palazzo, 2016). Micro-level studies find that entrants have, on average, lower productivity than incumbents because, for example, they set lower prices than incumbents to gain market share, which will result in lower productivity levels (Foster et al., 2008). Over time however, the more productive firms in the entry cohorts survive and their productivity levels may converge to those of incumbent firms (Aw et al., 2001) and even surpass the productivity levels of the oldest firms, resulting in an inverted U-shaped productivity effect of firm age (Cowling & Tanewski, 2019). Ouyang (2009) argues that recessions could have a scarring effect on entrants. Recessions are typically characterized by low demand and low profitability. For infant firms, this can be hard to overcome, resulting in high exit rates of young firms that probably would have survived in non-recession periods. Amongst these young exiting firms could be firms that would have become highly productive incumbents later on in their life cycle. Therefore, the scarring effect of recessions could lead to lower aggregate productivity in the long run.

Regarding the contribution of exit to aggregate productivity, the long-run equilibrium model of Hopenhayn (1992) suggests that firms decide to exit when they face low individual productivity shocks. Hence, exit of low-productive firms contributes positively to aggregate productivity. Empirical studies affirm these theoretical predictions. For example, Foster et al. (2001) find this to be true for US manufacturing. In recession periods, the probability that firms have low individual productivity shocks increases, thereby resulting in higher exit rates.

3 Empirical framework

3.1 Measuring productivity

The concept of total factor productivity (TFP) dates back to the work of Solow (1957), who defined rising TFP as rising output with constant capital and labor inputs.Footnote 3 The TFP estimates in this paper follow from semiparametric estimation as in Olley and Pakes (1996) using value added production functions with investments to proxy for unobserved productivity. All production functions are estimated at the NACE two-digit industry level with the Wooldridge (2009) one-step estimator.Footnote 4 Firm-level TFP measures are indicated by tfpijt in which i refers to firm, j identifies the affiliation of a firm to an industry, and t refers to year. The specification through which we obtain tfpijt is:

in which lowercase letters indicate logarithmic transformations. vaijt is deflated value added, lijt is number of hours worked, and kijt is deflated capital. \({\hat{\beta}}_{l_j}\) and \({\hat{\beta}}_{k_j}\) are the estimated production function coefficients of labor and capital.

3.2 Decomposing productivity

Decomposition models typically distinguish three channels of aggregate productivity growth. A first channel consists of incumbent firms that succeed in moving their productivity frontier (within) or succeed in attracting resources from firms with lower productivity (reallocation). A second potential driver of aggregate productivity growth is entry of highly productive firms. A third potential channel is exit of low-productive firms. Baily et al. (1992) were the first to propose a comprehensive model to identify the contribution from each of these channels. Their model was criticized because the entry and exit components of their model are biased by construction. Therefore, Griliches and Regev (1995) and Foster et al. (2001, hereafter FHK) introduced modifications that improve on this issue. All these models rely on the evolution of the productivity level and market share of individual firms over time. Another strand of models relies on the mean and covariance of the joint distribution of productivity and market shares. The first model of this kind was introduced by Olley and Pakes (1996). Recently, Melitz and Polanec (2015, hereafter MP) developed the so-called dynamic Olley and Pakes decomposition which extends the static Olley and Pakes (1996) decomposition into a dynamic model that includes entry and exit.Footnote 5 The MP model does not suffer from the measurement bias which is present in decomposition models that rely on the firm-level evolution of productivity and market share. Because of its attractive properties, we rely on the MP decomposition and complement it with the FHK model where necessary to answer the research questions.

Aggregate productivity is defined as a weighted average of firm-level productivity levels.Footnote 6 In regard of the pursued research questions, we choose to aggregate firm-level productivity measures using employment shares.Footnote 7 The labor share of firm i in industry j at year t is indicated by msijt. Aggregate productivity is defined as:

Since productivity is expressed in logs, aggregate productivity growth in percentages can then be obtained by:

Equation (4) shows how the MP model decomposes aggregate productivity growth:

in which variables in lowercase letters are at the firm level and variables in capital letters at the aggregate level. Variables that are overlined with a bar denote averages. The subscripts S, E, and X denote the group of surviving, entering, and exiting firms, respectively. The subscripts i, j, and t refer to firm, group, and year. We refer to Appendix C for the derivation of this decomposition and limit ourselves to how each line of Eq. (4) relates to the research questions.

The first line of Eq. (4) is the within component of incumbent firms. According to classic macroeconomic models of representative firms, this is the main source of aggregate productivity growth. In combination with the FHK model (see infra), the second line of Eq. (4) allows to quantify the contribution from job reallocation to aggregate productivity growth. Together, the first two lines capture the total contribution from incumbent firms to aggregate productivity growth. The third and fifth lines of Eq. (4) show whether the average productivity level of entering and exiting firms is higher or lower than the average productivity level of surviving firms. Theoretically, one would expect both the average productivity of new entrants and that of exiting firms to be lower than the average productivity of incumbents. The fourth and sixth lines of Eq. (4) learn whether job allocation is more efficient in entering or exiting firms than in incumbent firms. If we assume that firms learn about their productivity over their life cycle and hire labor according to their productivity levels, we expect both the components from lines four and six to be negative.

A drawback of decomposition models based on cross-sectional distributions is the inability to distinguish the evolution of market share (in our case, expressed in labor) from the evolution in productivity. The covariance components of two decompositions presented above learn whether job allocation is aligned with productivity. However, they do not distinguish between changes in market share and changes in productivity.Footnote 8 Hence, it is theoretically possible to find a positive impact of job reallocation even if market shares remain fixed, i.e., when the effect is solely driven by productivity changes. To rule out this confounding channel, we complement our analysis with the FHK decomposition model that tracks firms over time instead of relying on cross-sectional distributions. Eq. (5) shows how the FHK model decomposes aggregate productivity growth:

The first line in Eq. (5) refers to the contribution from within-firm productivity growth. The between component on the second line fixes the deviation of an incumbent firm’s productivity level compared to aggregate productivity in t − 1 and regards the change in market share between t − 1 and t. This component is particularly interesting with regard to the cleansing hypothesis because the MP decomposition regards simultaneous changes in productivity and market share while the between component captures solely the contribution to aggregate productivity from job reallocation. It is positive when jobs are reallocated to firms with high productivity. The cleansing hypothesis suggests this component to be positive, and particularly during or right after recession periods. The third line is usually labeled as the covariance component, although it is not a covariance from a mathematical perspective. The covariance component shows whether or not productivity evolves in the same direction as market share. The fifth and sixth lines show the contribution from entry and exit to aggregate productivity growth.Footnote 9

4 Data

We identify recessions based on GDP growth. According to the textbook definition—two consecutive quarters of negative GDP growth—Belgium experienced three recessions over the sample period: Q1-2001–Q4-2001; Q3-2008–Q2-2009; Q2-2012–Q1-2013. Obviously, the Great Recession of 2008–2009 was the most severe of the three.Footnote 10

We obtain financial data from a dataset of the National Bank of Belgium which holds the annual accounts of all limited liability firms that were active in Belgium in the period 1997–2014. From this database, we collect panel data on employment (the number of FTE’s and number of hours worked), capital, investments, firm age, and value added for all firms in the private sector (NACE rev. 1.1 industry 1-74).Footnote 11 We use deflators from the National Bank of Belgium and Eurostat to transform nominal values into real values.

In a granular approach such as the one taken in this paper, it is important to include firms that are in the upper tail of the distribution because these can drive aggregate fluctuations. Therefore, we limited data cleaning to a minimum.Footnote 12 Table 1 shows summary statistics for our sample of about 100.000 firms that we use in the decompositions. Together, these firms represent 40% of the people working in the private sector and 42% of total value added created.

The summary statistics show that both tails of the employment distribution are represented in our sample; we have micro firms as well as firms with more than 10,000 employees. The average firm counts about 15 employees, has a capital stock of 1.1 million EUR, is 11 years old, and creates around 1.1 million EUR added value.

5 Results

5.1 Aggregate productivity growth

Before investigating cleansing effects from recessions, we discuss some general findings about aggregate productivity growth in incumbent, entering, and exiting firms. Table 2 shows the results of the MP decomposition. We make a distinction between recession and non-recession periods.Footnote 13

For this section, we restrict the discussion to the bottom row of Table 2. Over the sample period 1997–2014, aggregate yearly productivity growth in the private sector was on average 1.17%. In incumbent firms, we find large volatility in within-firm productivity over time. Yet, on average, the impact of within-firm productivity changes on aggregate productivity is minimal at −0.17% points. The procyclical nature of average within-firm productivity is in line with the literature (Van Beveren & Vanormelingen, 2014). According to Basu and Fernald (2001), this can be explained by procyclical technology, capacity utilization, imperfect competition, and increasing returns to scale. The size-productivity covariance can be taken as a measure of how efficient the resource allocation is. The higher the covariance, the more resources are allocated to more efficient firms. The covariance consistently increased over time, except in the years preceding recessions. This source of aggregate productivity growth was responsible for on average 1.07% point aggregate productivity growth over the period 1997–2014. To sum up, while changes in the size-productivity covariance made a persistent contribution to aggregate productivity growth, fluctuations in within-firm productivity drive the cyclicality of productivity growth.

Average productivity is consistently lower in the cross section of entering and exiting firms than in incumbent firms. This is consistent with firm exit when productivity is low (Hopenhayn, 1992) and competitive pricing from entering firms to gain market share (Foster et al., 2008).Footnote 14 Exit of low-productive firms contributed on average 0.63% points to aggregate productivity growth while lower productivity in firms during the first year of their economic activity had on average an impact of −0.20% points on aggregate productivity growth.Footnote 15 Finally, the size-productivity covariance is higher in incumbent firms than in entering and exiting firms. As a result, firm entry (exit) lowered (increased) the overall efficiency of resource allocation in the economy with an average impact on aggregate productivity growth of −0.28% (0.12%) points.

5.2 Cleansing effects of recessions

5.2.1 Cleansing from job reallocation

We distinguish two types of cleansing: job reallocation from low towards high-productivity firms and exit of low-productive firms. Figure 1 shows gross job reallocation, measured as in Davis and Haltiwanger (1992), over the business cycle.

Job reallocation (~Davis & Haltiwanger, 1992)

We find countercyclical gross job reallocation in Belgium. During the Great Recession, gross job reallocation rose as the job destruction increased by more than the decline in job creation. Figure 1 also shows that it matters how jobs are measured. When jobs are measured in full-time equivalents, the increase in job destruction is not as outspoken as when jobs are measured in hours worked, especially during the Great Recession. This indicates that firms did labor hoarding: firms reduced the number of hours worked, but this did not always come with shedding employment. We discuss this phenomenon and its impact on cleansing below. Figure 2 shows which firms created and destroyed jobs during the Great Recession. For defining firm age classes, we followed the classification of Cowling and Tanewski (2019) and for defining firm size classes, we followed the classification of the OECD (2019).

Who created and destroyed jobs during the Great Recession

In absolute numbers, most jobs were created and destroyed in firms that are old and large, consistent with the findings of Haltiwanger et al. (2013). However, the bulk of firms that created and destroyed jobs during the Great Recession count less than 10 employees: 34.68% of the firms that created jobs were old micro firms, and 41.92% of the firms that destroyed jobs were old micro firms. This is not surprising since old micro firms also make up the largest share of the population of firms. In fact, the distribution over size and age classes of the full population of firms closely aligns with the distribution over size and age classes of firms that create and destroy jobs.

To verify whether the observed increase in job reallocation was effectively associated with an increase in aggregate productivity growth, we rely on the ∆ cov (TFP, MS)surv component from the MP decomposition and the ∆Betweensurv component from the FHK decomposition.Footnote 16 Based on the cleansing hypothesis, one would expect ∆ cov (TFP, MS)surv and ∆Betweensurv to be higher during and right after the recessions (Table 3).

Regardless whether jobs are measured in full-time equivalents or hours worked, Table 3 shows that the contribution of ∆Betweensurv to aggregate productivity growth is almost double as high in recession years compared to non-recession years. This indicates that recessions were associated with cleansing through job reallocation from low productivity towards high-productivity firms. The same conclusion can be drawn from the observed increase in the contribution of ∆ cov (TFP, MS)surv to aggregate productivity growth in recessions. During and right after the Great Recession, the contribution of ∆ cov (TFP, MS)surv to aggregate productivity growth was on average 1.58% points when employment is measured in hours worked and 1.55% points when employment is measured in full-time equivalents (cf. Tables A-2 and A-4 in Appendix A.3).

Both in the MP and FHK decomposition, the contribution of job reallocation to aggregate productivity growth is larger when jobs are measured in number of hours worked. As shown in Fig. 1, job reallocation patterns differ depending on how jobs are measured, especially in the Great Recession. This reflects labor hoarding—a practice that was facilitated by the government during the Great Recession (see infra)—which impacts the number of hours worked but not the number of full-time equivalents. The results based on hours worked thus overestimate cleansing effects from job reallocation, since changes in hours worked do not imply that low-productive jobs are effectively “cleansed out.” In 2009, which is the most severe crisis year in our sample (see Figure A-4 in Appendix A.6), ∆Betweensurv is equal to 1.48% points with jobs measured in the number hours worked and only 0.53% points with jobs measured in the number of full-time equivalents (cf. Tables A-3 and A-5 in Appendix A.3). So the contribution to aggregate productivity growth from job reallocation would be overstated with a factor of three when employment changes are measured in the number of hours worked. Another way to look at this result is that when firms would optimize the demand for labor completely flexible in a static world without costs from changes in the stock of labor, aggregate productivity growth from 2008 to 2009 would have been (1.48 % − 0.53%) ≈ 1% point higher.

5.2.2 Labor hoarding

The differences in job reallocation, depending on whether employment is measured through the number of hours worked or the number of full-time equivalents, suggest that firms did labor hoarding during recession periods.Footnote 17 Between 2009 and 2010, the Belgian government facilitated labor hoarding by providing financial support to firms that reduced the worktime of employees because of economic reasons. Hijzen and Venn (2011) estimate that the facilitation of labor hoarding saved between 14,000 and 55,000 jobs in Belgium. However, it is not clear ex ante whether aggregate productivity growth benefits from labor hoarding. Labor hoarding is beneficial for aggregate productivity growth if firms that hoard labor increase their productivity relatively faster when economic conditions improve, and detrimental for productivity growth if it locks employment in low-productive activities. To investigate the impact of labor hoarding on productivity, we compare productivity between hoarding and non-hoarding firms after the Great Recession with the following model:

in which Hoarding is a dummy variable equal to 1 if the firm does labor hoarding during the years 2008–2010.Footnote 18 AfterRecession is a dummy variable equal to 1 from 2011 to 2014 and equal to 0 from 1997 to 2007. Zit are two-digit industry dummies. The coefficient of the hoarding variable shows the difference in average productivity between hoarding and non-hoarding firms. The coefficient of the AfterRecession dummies shows the difference in average productivity, for both hoarding and non-hoarding firms, before and after the Great Recession. The interaction between the hoarding variable and the recession indicator learns whether the change in productivity from pre- to post-Great Recession in hoarding firms was larger than the change in productivity in non-hoarding firms. This model allows to estimate whether firms that did labor hoarding during the Great Recession enjoyed a productivity premium after the Great Recession compared to those firms who did not do labor hoarding.Footnote 19 After estimating Eq. (6) for the full sample, we run split sample estimations to understand whether labor hoarding affects productivity differently in small, large, young, and old firms.

The first row in Table 4 shows that, regardless which subclass we regard, firms that did labor hoarding had on average significantly lower productivity than firms that did not hoard labor. These results confirm the self-selection of low-productive firms into labor hoarding, which is not surprising since labor hoarding was facilitated exactly with the purpose of saving jobs in firms that were suffering from the economic downturn.

The third row in Table 4 shows that—in the full population of firms—firms who did labor hoarding during 2008–2010 did not have significantly different productivity levels compared to other firms afterwards. However, when uncovering this aggregate affect across firm size and age classes, we find that old firms and large firms who hoarded labor in 2008–2010 had an average productivity deficit of respectively 1.7% and 4.2% afterwards compared to old firms and large firms who did not hoard labor. Only in small firms, we find a marginally significant productivity premium of 1% for those that hoarded labor in 2008–2010 compared to the small firms that did not hoard labor in the Great Recession.

Rows 4–7 in Table 4 split up the average productivity differences from row 3 over the years 2011–2014. Taking all firms together, we find that the insignificant average effect hides that firms who hoard labor in 2008–2010 are falling behind 1% in productivity after 2 years compared to those that did not hoard labor in the Great Recession. Also in small and young firms, the effect of labor hoarding on productivity only had a temporary positive effect on productivity. In old and large firms, the productivity deficit in labor hoarding firms is persistent over time. Altogether, we do not find persistent positive effects from labor hoarding on productivity, and even when positive effects appear, these are not large enough to offset the productivity deficit that is present in labor hoarding firms (cf. row 1 of Table 4).

5.2.3 Cleansing from firm exit

The MP decomposition is the most adequate model to map the contribution of firm exit to aggregate productivity growth, see Melitz and Polanec (2015) for a discussion. Although the impact is limited, the contribution of \({\overline{TFP}}_{sur{v}_{t-1}- exi{t}_{t-1}}\) in Table 2 is higher in recession periods. Indeed, the left panel in Fig. 3 shows that the share of employment in exiting firms slightly increased during the Great Recession. When low-productive firms exit, aggregate productivity in the remaining set of firms is higher, resulting in aggregate productivity growth. Yet, there is a part from cleansing through exit that cannot be captured in productivity decompositions. Productivity can only be estimated for firms with positive value added, while firms with negative value added are most likely to be cleansed out by recessions. The right panel of Fig. 3 shows the percentage of firms that reports negative value added and the percentage of firms that exit.

Cleansing from exit

The sharp increase in firm exit amongst firms with negative value added in the aftermath of the Great Recession is evidence of cleansing through firm exit. Our findings on a post-recession increase in firm exit are consistent with Carreira and Teixeira (2016) and Dumont et al. (2016). The long time series of our data allows us to uncover another interesting trend, which is the overall decline in firm exit and an increase in the share of firms with negative values, at least until 2008. From 1997 to 2008, the share of firms that have negative added value increased from 11 to 15%, after which this share remained flat and even slightly decreased due to increased exit of firms with negative value added from cleansing. Moreover, the share of such firms that exit declined from 13 to 9% over the same period. This pattern is consistent with declining business dynamism (Bijnens & Konings, 2018) and the rise of zombie firms, which was shown to be an important determinant of the stagnation of labor productivity growth in OECD countries (McGowan et al., 2018).

Fort et al. (2013) investigated how young, old, small, and large firms are affected by business cycles in the USA and find that young/small firms are more sensitive to business cycles than large/old firms. Figure 4 provides more details on the aggregate numbers reported in Fig. 3 and shows the distribution of firms that report negative value added and exit during and after the Great Recession.

Negative value added and exit

In absolute numbers, most job losses were a consequence of old firms that exit, especially old micro firms. Within the population of firms with negative value added that exit, 45.41% are old micro firms. This is not surprising since old micro firms also make up the largest share of the population of firms with negative value added. In fact, the distribution over size and age classes of the population of firms with negative value added closely aligns with the distribution over size and age classes of firms with negative value added that exit. One exception are the young micro firms, which make up one quarter (25.92%) of the firms that struggle to create added value but only one fifth (19.01%) of the firms who struggle to create added value and exit. The behavior of young firms is particularly interesting since they drive economic growth (Stel et al., 2005). Recessions can have a scarring effect by killing high potential entrants in their infancy, thereby negatively impacting aggregate productivity in the long run (Ouyang, 2009). While, in the population of firms with negative value added, 19% of the firms that exit were less than 3 years old, we find for the full sample that in 2008–2009 the percentage of exiting firms that was less than 3 years old was 21%. This was higher than in the rest of our sample period, where the percentage of exiting firms with less than 3 years of age was fairly constant at about 17%. So it is harder for young firms to survive in crisis period. This suggests the Great Recession did have a scarring effect in Belgium.

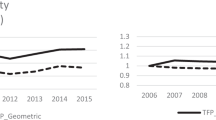

5.3 Manufacturing vs services

An advantage of our rich dataset is that we observe both the manufacturing and services and can contrast them with each other. Over the sample period, yearly aggregate productivity growth is on average only 0.54% per year in the services sector while it is 1.72% in the manufacturing sector (cf. first column Tables A-8 and A-12 in Appendix A-4). Part of this difference is due to within-firm productivity growth which is on average positive in the manufacturing sector while it is negative in the services sector (cf. third column of Tables A-8 and A-12 in Appendix A-4). This is in line with the premise that it is harder to realize productivity growth in services activities by nature. Looking at the average contributions from incumbent, entering, and exiting firms to aggregate productivity growth, we find that in the manufacturing sector, productivity growth is largely driven by incumbent firms while in the services sector also exit of low productivity firms is important for productivity growth.

Figure 5 shows the evolution of the difference in the covariance component of the MP decomposition, i.e., ∆ cov (TFP, MS)surv, manufacturing − ∆ cov (TFP, MS)surv, services, and the evolution of the difference in the between component of the FHK decomposition, i.e., ∆Betweensurv, manufacturing − ∆Betweensurv, services. These differences are positive in recession periods, especially in the Great Recession, indicating stronger cleansing through productivity enhancing job reallocation in manufacturing than in services industries. Especially in 2009, which is the deepest recession year of the sample period (cf. Figure A-4 in Appendix A-6), ∆ cov (TFP, MS) is equal to 3.73% in manufacturing and −0.68% in services while ∆Between is equal to 1.78% in manufacturing and 0.12% in services, resulting in the reported differences of respectively 4.41% and 1.66% for 2009 in the right panel of Fig. 5.

Productivity enhancing job reallocation manufacturing vs services

In 2009 and 2010, there is an aggregate productivity growth in the manufacturing sector of respectively 3.73% and 5.80% due to an increase in the covariance between jobs and productivity, while the average contribution of this component for all other years is only 0.35%. The between component from the FHK decomposition is also far above average in 2009 and 2010, which confirms that job reallocation rather than changes in productivity did induce productivity growth in the manufacturing sector. For services industries, there is no noteworthy change in the ∆ cov (TFP, MS) and ∆Between components during and right after the Great Recession. This demonstrates that the finding on cleansing effects of recessions due to productivity enhancing job reallocation for the aggregate economy originates from the manufacturing industry.

As demonstrated in Section 5 about the entire private sector, the measure used for aggregation could cause a composition bias. Tables A-7–A-14 in Appendix A-4 show that productivity enhancing job reallocation in manufacturing is much higher when jobs are measured by the number of hours worked than if jobs are measured by the number of full-time equivalents. As detailed in Section 5.2, these differences can be explained by labor hoarding. Since we do not observe differences in the decompositions based on hours worked or full-time equivalents in services industries, does this imply that labor hoarding did not take place in services? This appears not to be the case: 52% of the labor hoarding firms are active in services industries, and only 22% of labor hoarding firms are active in manufacturing industries. The reason why the decomposition results in the services sector hardly differ depending on whether jobs are measured in hours worked or full-time equivalents is that productivity of labor hoarding firms was relatively high. We find that, within the group of labor hoarding firms, manufacturing firms had on average 50% lower productivity than services firms. This is an interesting insight because the facilitation of labor hoarding for economic reasons introduced by the Belgian government in the period 2009–2010 was the first time that services industries could benefit from such a system. This raises the question whether the policy was not too generous and allowed firms to enjoy tax benefits for labor that they would hoard anyway, thereby resulting in a deadweight loss.

Finally, we investigate whether cleansing through firm exit is more or less prominent in manufacturing or services industries. The \(\Delta {\overline{TFP}}_{sur{v}_{t-1}- exi{t}_{t-1}}\) and \(\Delta \mathit{\operatorname{cov}}{\left( TFP, MS\right)}_{sur{v}_{t-1}- exi{t}_{t-1}}\) in manufacturing increased substantially during the 2001 recession, but not as much in the Great Recession. Together with our findings on reallocation, this indicates that Belgian manufacturing firms were able to avoid market exit during the Great Recession through the use of facilitated labor hoarding. After the Great Recession, however, there is a noticeable increase in the MP and FHK components that show the contribution of exit to aggregate productivity. Also, the number of exiting firms in manufacturing industries increased (cf. Tables A-19 and A-20 in Appendix A-20). This suggests that cleansing through firm exit did happen in manufacturing industries, albeit with a lag. In services industries, a similar pattern can be observed.

6 Conclusion

This paper investigates how recessions affected the micro origins of aggregate productivity growth in Belgium between 1997 and 2014. The central question of the paper is whether recessions display countercyclical productivity growth through a cleansing effect from firm exit and productivity enhancing job reallocation. We rely on productivity decompositions developed by Melitz and Polanec (2015) and Foster et al. (2001) to measure the contribution of job reallocation and exit to aggregate productivity growth. We also investigate how the impact of job reallocation on productivity growth is affected by labor hoarding. We can measure this since we have information on the number of full-time equivalents, which does not account for labor hoarding, and hours worked, which does account for labor hoarding. This is particularly interesting in the context of Belgium, where the government introduced a generous program that facilitated labor hoarding to save jobs during the Great Recession with the result that the share of employment in labor hoarding firms was larger in Belgium than in any other OECD country during the Great Recession (Hijzen & Venn, 2011). To the best of our knowledge, we are the first to relate labor hoarding with productivity growth through job reallocation.

As in Bartelsman et al. (2013), we use the size-productivity covariance to measure how efficient job allocation is. The higher the covariance, the more jobs are allocated to more efficient firms. Our results show that changes in the size-productivity covariance made a persistent contribution to aggregate productivity growth, while fluctuations in within-firm productivity drive the cyclicality of productivity growth. This is in line with earlier literature (Van Beveren & Vanormelingen, 2014). The contribution to aggregate productivity from job reallocation increases substantially during and right after recession periods, suggesting that recessions, especially the Great Recession, displayed a cleansing effect. However, the magnitude of this cleansing effect depends on how jobs are measured. When measuring jobs by the number of full-time equivalents instead of the number of hours worked, the contribution of job reallocation to aggregate productivity growth drops from 1.48 to 0.53% points in 2009. So the contribution to aggregate productivity growth from job reallocation is overstated with a factor of three when employment changes are measured in number of hours worked. Another way to look at this result is that when firms would optimize the demand for labor completely flexible in a static world without costs from changes in the stock of labor, aggregate productivity growth from 2008 to 2009 would have been (1.48 % − 0.53%) ≈ 1% point higher.

Differences in job reallocation, depending on whether employment is measured in hours worked or full-time equivalents, indicate that firms did labor hoarding. The economic arguments for facilitating labor hoarding during economic downturns like the Great Recession or the COVID-19 crisis from the point of view of a social planner are (i) to avoid excessive layoffs such that families preserve their income and (ii) to preserve human capital in firms that face negative demand shocks so that they can raise their productivity when the economy recovers. However, such initiatives can also result in lower productivity growth when it allows low-productive firms that would otherwise reduce employment or exit, to keep their stock of labor. We find short-term productivity premia after hoarding labor in young and small firms, while old firms and large firms that hoarded labor during the Great Recession had a persistent productivity deficit afterwards compared to old firms and large firms that did not hoard labor. Even when labor hoarding resulted in a positive productivity premium, this was not large enough to offset the productivity deficit that was present in labor hoarding firms ex ante. All in all, labor hoarding did not improve productivity in the long run.

Besides cleansing through job reallocation, we investigate whether the contribution from firm exit to aggregate productivity growth increases during recessions. The contribution from firm exit to aggregate productivity growth during and right after recessions is moderately higher than in normal times. An interesting phenomenon occurs in the exit rate of firms that report negative value added. The share of firms that report negative value added increased until 2008, and at the same time, the share of such firms that exit the market decreased until 2008. This indicates there was a rise in the share of zombie firms (McGowan et al., 2018). After the Great Recession, both trends reversed: the share of firms with negative value added stagnated and the share of these firms that exit increased, suggesting that cleansing effects of recessions put a hold on the rise of zombie firms in Belgium. Most firms with negative value added are old micro firms. Within the population of firms with negative value added that exit, 45.41% are old micro firms.

Finally, we investigated whether cleansing effects of recessions differ between manufacturing and services industries. We find no evidence for cleansing effects due to job reallocation in the services sector, which covers 46% of total employment. This indicates that recessions have no homogeneous cleansing effect on the economy and that accounting for differences across industries is important to understand the aggregate impact of cleansing effects of recessions. Within the group of labor hoarding firms, manufacturing firms had on average 50% lower productivity than services firms while 52% of the labor hoarding firms are active in services industries. This raises the question whether the policy on the facilitation of labor hoarding was not too generous by allowing services firms with relatively high productivity to enjoy tax benefits for labor that they would hoard anyway, thereby resulting in a deadweight loss.

Towards policy makers, a relevant takeaway from this paper is that the facilitation of labor hoarding can distort job reallocation and exit of low-productive firms, while such cleansing effects of recessions spur productivity growth. During the COVID-19 crisis, the government again introduced generous labor hoarding policies. While this will save jobs in the short run, our findings indicate that we cannot expect this to increase productivity in the long run.

Notes

Twenty two countries of the OECD reported either setting up new measures or adjusting existing measures as a response to the Great Recession. On June 25, 2009, the Belgian government approved a bill to promote the reduction of working hours to save jobs during the economic recession. The social security office compensated the salary of employees who’s working hours were reduced. It is important to note that all private sector and autonomous public firms could use this law and that employees kept all their rights and remained full-time equivalents. This law was in place until January 31, 2011.

While the USA ranks 1st on labor market flexibility in the Global Competitiveness Index of 2018, Belgium only ranks 40th, well behind neighboring countries like The Netherlands (10th), Germany (7th), and Great Britain (8th).

The emphasis of our paper is on aggregate total factor productivity (TFP). However, the methodology also applies to other productivity measures, e.g., labor productivity, for which we present some results in Appendix A.5.

We refer to Appendix B for a comprehensive overview of the estimation procedure and Table A-22 in Appendix B for an overview of the estimated production function coefficients per industry. In Appendix A.5, we present robustness checks to the results based on the more flexible Translog production function.

This is standard in the literature. One notable exception is the decomposition model of Petrin and Levinsohn (2012) However, their model deviates by not incorporating separate terms for entering and exiting firms. Therefore, we do not regard their model.

By choosing employment shares, we implicitly assume that the employment market share of a firm represents a firm’s weight in the economy.

The covariance changes can be due to simultaneous job reallocation and productivity reallocation. Figure A-6 in the Appendix illustrates this. When firms move towards the 45 degree line, the covariance components will increase. This can happen both through changes in jobs and changes in productivity.

MP (2015) shows that the reference levels for these components are imperfect. Therefore, these components will solely serve as robustness checks for our findings on entry and exit with the MP decompositions.

We validate our identification of recession periods with the country-specific composite leading indicators from the OECD, which include information on consumer confidence, production, demand, export orders, employment, and passenger car registrations and find the same three crisis periods in our sample with these indicators, namely 2001, 2008–2009, and 2012.

A detailed description of the selected variables from the annual accounts can be found in Appendix B.2.

The most important constraints in terms of data originate from (i) the inability of the decompositions to cope with missing data and (ii) the use of log linear transformations of the variables, which requires all variables to be positive. We refer to Appendix B.2.5 for a description of the data cleaning, missing data, and outliers. In Appendix A.2, we discuss the representativeness of our sample for the entire private sector.

We compare the elements from the decomposition between non-recession years (1998, 1999, 2000, 2003, 2004, 2005, 2006, 2007, 2010, 2011, 2014) and recession years (2001, 2002, 2008, 2009, 2012, 2013). We include the first year after a recession because cleansing could happen with some lag. Especially in a rigid labor market like that of Belgium, decisions on changes in employment are expected to show up with a delay in the firm’s accounts. The yearly results are included in Appendix A-3.

Firms that are active for 1 year or less are labeled entrants. As a result, the contribution from young firms (older than 1 year) to aggregated productivity will be absorbed into the components of incumbent firms. The yearly entry and exit rates in our sample of firms for the decompositions are respectively 5–7% and 3–5% (see Table A-19 in the appendix) which is lower than reported in Geurts (2015). This is due to necessary data cleaning to apply the decomposition. We are aware of the potential consequences of data cleaning and discuss this in Appendix B.2.5.

As documented by Aw et al. (2001), entrants are a heterogeneous group. Some of them fail, but others grow and are important for aggregate productivity growth in the long run (Hyytinen & Maliranta, 2013). In this paper, we look only at the first year of economic activity and abstain from long-run aggregate productivity effects from entry.

It is important to remind that the MP decomposition shows productivity growth from simultaneous changes in productivity and jobs while the FHK decomposition shows productivity growth from job reallocation only.

Appendix A.1 provides further details on the facilitation of labor hoarding for the period 2009–2010 in Belgium.

Next to recession years 2008–2009, we include the year 2010 since labor hoarding was facilitated by the government in this period. The labor hoarding dummy of a firm is equal to 1 in year t if the following criteria are met: (i) the number of employees in year t is equal to or less than in year t − 1, (ii) the total number of hours worked in year t is less than in year t − 1 after correcting for the difference in the total number of hours worked due to dismissals, (iii) the average number of hours worked per employee in year t is lower than in year t − 1.

In order to interpret the estimates from the model as a causal identification of the effect of labor hoarding on productivity, one must assume that there are no differences in unobserved characteristics between hoarding and non-hoarding firms.

References

Aw, B. Y., Chen, X., & Roberts, M. J. (2001). Firm-level evidence on productivity differentials and turnover in Taiwanese manufacturing. Journal of Development Economics, 66, 51–86. https://doi.org/10.1016/s0304-3878(01)00155-9

Baily, M. N., Hulten, C., & Campbell, D. (1992). Productivity dynamics in manufacturing plants. Brookings Papers on Economic Activity: Microeconomics, 187–267. https://doi.org/10.2307/2534764

Barlevy, G. (2002). The sullying effect of recessions. The Review of Economic Studies, 69(1), 65–96. https://doi.org/10.1111/1467-937x.00198

Bartelsman, E. J., Haltiwanger, J., & Scarpetta, S. (2013). Cross-country differences in productivity: The role of allocation and selection. American Economic Review, 103(1), 305–334. https://doi.org/10.1257/aer.103.1.305

Basu, S., & Fernald, J. G. (2001). Why is productivity procyclical? Why do we care? Chicago: University of Chicago Press. New Developments in Productivity Analysis, 225-296. https://doi.org/10.7208/chicago/9780226360645.003.0007

Bijnens, G., & Konings, J. (2018). Declining business dynamism in Belgium. Small Business Economics, 54(4), 1201–1239. https://doi.org/10.1007/s11187-018-0123-4

Bloom, N., Bunn, P., Mizen, P., Smietanka, P., & Thwaites, G. (2020). The Impact of Covid-19 on productivity. National Bureau of Economic Research Working Paper Series, No. 28233. https://doi.org/10.3386/w28233

Caballero, R. J., & Hammour, M. L. (1994). The cleansing effect of recessions. The American Economic Review, 84(5), 1350–1368. https://doi.org/10.3386/w3922

Carreira, C., & Teixeira, P. (2016). Entry and exit in severe recessions: Lessons from the 2008-2013 Portuguese economic crisis. Small Business Economics, 46(4), 591–617. https://doi.org/10.1007/s11187-016-9703-3

Clementi, L. G., & Palazzo, B. (2016). Entry, exit, firm dynamics, and aggregate fluctuations. American Economic Journal: Macroeconomics, 8(3), 1–41. https://doi.org/10.1257/mac.20150017

Cowling, M., & Tanewski, G. (2019). On the productive efficiency of Australian businesses: Firm size and age class effects. Small Business Economics, 53(3), 739–752. https://doi.org/10.1007/s11187-018-0070-0

Criscuolo, C. (2018). Slow and divided: What can policies do to lift economies and restart engines of growth for all? Science, Research and Innovation Performance of the EU. https://doi.org/10.2777/14136

Davis, S. J., & Haltiwanger, J. (1992). Gross job creation, gross job destruction, and employment reallocation. The Quarterly Journal of Economics, 107(3), 819–863. https://doi.org/10.2307/2118365

Decker, R. A., Haltiwanger, J., Jarmin, R. S., & Miranda, J. (2017). Declining dynamism, allocative efficiency, and the productivity slowdown. American Economic Review, 107(5), 322–326. https://doi.org/10.1257/aer.p20171020

Dumont, M., Rayp, G., Verschelde, M., & Merlevede, B. (2016). The contribution of start-ups and young firms to industry-level efficiency growth. Applied Economics, 48(59), 5786–5801. https://doi.org/10.1080/00036846.2016.1184381

Fort, T., Haltiwanger, J., Jarmin, R., & Miranda, J. (2013). How firms respond to business cycles: The role of firm age and firm size. IMF Economic Review, 61(3), 520–559. https://doi.org/10.1057/imfer.2013.15

Foster, L., Haltiwanger, J., & Krizan, C. (2001). Aggregate productivity growth: Lessons from microeconomic evidence. University of Chicago Press. https://doi.org/10.3386/w6803

Foster, L., Haltiwanger, J., & Syverson, C. (2008). Reallocation, firm turnover, and efficiency: Selection on productivity or profitability? The American Economic Review, 98(1), 394–425. https://doi.org/10.1257/aer.98.1.394

Foster, L., Grim, C., & Haltiwanger, J. (2016). Reallocation in the Great Recession: Cleansing or not? Journal of Labor Economics, 34(1), 293–331. https://doi.org/10.1086/682397

Geurts, K. (2015). How sensitive are measures of firm and employment dynamics to longitudinal linkage problems. Discussion paper series 15.10, Center for Economic Studies, KU Leuven. https://doi.org/10.2139/ssrn.2610577

Griliches, Z., & Regev, H. (1995). Firm productivity in Israeli industry 1979-1988. Journal of Econometrics, 65(1), 175–203. https://doi.org/10.1016/0304-4076(94)01601-u

Hall, R. E., & Jones, C. I. (1999). Why do some countries produce so much more output per worker than others? The Quarterly Journal of Economics, 114(1), 83–116. https://doi.org/10.1162/003355399555954

Haltiwanger, J., Hyatt, H. R., McEntarfer, E., & Staiger, M. (2021). Cyclical worker flows: Cleansing vs. sullying. National Bureau of Economic Research Working Paper Series, No. 28802. https://doi.org/10.3386/w28802

Haltiwanger, J., Jarmin, R. S., & Miranda, J. (2013). Who creates jobs? Small vs. large vs. young. Review of Economics and Statistics, 95(2), 347–361. https://doi.org/10.1162/rest_a_00288

Hijzen, A. and Venn, D. (2011). The role of short-time work schemes during the 2008-09 recession. OECD Social, Employment and Migration Working Papers, No. 115, OECD Publishing. https://doi.org/10.1787/5kgkd0bbwvxp-en

Hopenhayn, H. A. (1992). Entry, exit, and firm dynamics in long run equilibrium. Econometrica, 60(5), 1127–1150. https://doi.org/10.2307/2951541

Hyytinen, A., & Maliranta, M. (2013). Firm lifecycles and evolution of industry productivity. Research Policy, 42(5), 1080–1098. https://doi.org/10.1016/j.respol.2013.01.008

Krugman, P.R. (1997). The age of diminished expectations, 3rd edition: U.S. Economic Policy in the 1990s. Cambridge: MIT Press.

McGowan, M., Andrews, D., & Millot, V. (2018). The walking dead – Zombie firms and productivity performance in OECD countries. Economic Policy, 33(96), 685–736. https://doi.org/10.1093/epolic/eiy012

Melitz, M. J., & Polanec, S. (2015). Dynamic Olley-Pakes productivity decomposition with entry and exit. RAND Journal of Economics, 46(2), 362–375. https://doi.org/10.1111/1756-2171.12088

Moscarini, G., & Postel-Vinay, F. (2016). Did the job ladder fail after the great recession? Journal of Labor Economics, 34(1), 55–93. https://doi.org/10.1086/682366

OECD. (2019). OECD SME and entrepreneurship outlook 2019. OECD Publishing. https://doi.org/10.1787/34907e9c-en

Olley, G. S., & Pakes, A. (1996). The dynamics of productivity in the telecommunications equipment industry. Econometrica, 64(6), 1263–1297. https://doi.org/10.2307/2171831

Ouyang, M. (2009). The scarring effect of recessions. Journal of Monetary Economics, 56(2), 184–199. https://doi.org/10.1016/j.jmoneco.2008.12.014

Owalla, B., Gherhes, C., Vorley, T., & Brooks, C. (2021). Map** SME productivity research: A systematic review of empirical evidence and future research agenda. Small Business Economics. https://doi.org/10.1007/s11187-021-00450-3

Petrin, A., & Levinsohn, J. (2012). Measuring aggregate productivity growth using plant-level data. RAND Journal of Economics, 43(4), 705–725. https://doi.org/10.1111/1756-2171.12005

Petrosky-Nadeau, N. (2013). TFP during a Credit Crunch. Journal of Economic Theory, 148, 1150–1178. https://doi.org/10.1016/j.jet.2012.09.019

Schumpeter, J. A. (1941). Business cycles: A theoretical, historical and statistical analysis of the capitalist process. McGraw-Hill. https://doi.org/10.1017/s0034670500001170

Solon, G., Barsky, R., & Parker, J. A. (1994). Measuring the cyclicality of real wages: How important is composition bias? The Quarterly Journal of Economics, 109(1), 1–25. https://doi.org/10.2307/2118426

Solow, R. (1957). Technical change and the aggregate production function. The Review of Economics and Statistics, 39(3), 312–320. https://doi.org/10.2307/1926047

Stel, A. V., Carree, M., & Thurik, R. (2005). The effect of entrepreneurial activity on national economic growth. Small Business Economics, 24, 311–321. https://doi.org/10.1007/s11187-005-1996-6

Syverson, C. (2004). Product substitutability and productivity dispersion. Review of Economics and Statistics, 86(2), 534–550. https://doi.org/10.1162/003465304323031094

Van Beveren, I. and Vanormelingen, S. (2014). Human capital, firm capabilities and productivity growth. National Bank of Belgium Working Paper 257. https://doi.org/10.2139/ssrn.2434010

Wooldridge, J. (2009). On estimating firm-level production functions using proxy variables to control for unobservables. Economics Letters, 104(3), 112–114. https://doi.org/10.1016/j.econlet.2009.04.026

Acknowledgements

We are grateful to Bruno Cassiman, Dirk Czarnitzki, Joep Konings, Sašo Polanec, Timothy Simcoe and Jakob Vanschoonbeek for helpful comments and suggestions. We also acknowledge the insightful comments at a number of conferences and seminars. All remaining errors are our own responsibility.

Availability of data and material

We are not allowed to make the data with the annual accounts from the National Bank of Belgium publicly available. All statistical code with the necessary instructions to go from the raw data to the dataset used in the analysis can be requested from the authors.

Code availability

To obtain the statistical code for replicating the analysis, please contact the authors.

Funding

This research has benefited from FWO grant G055914N, FWO grant G071417N and National Bank of Belgium grant NBB-17-00221.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare no competing interests.

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

ESM 1

(DOCX 5663 kb)

Rights and permissions

About this article

Cite this article

Van den bosch, J., Vanormelingen, S. Productivity growth over the business cycle: cleansing effects of recessions. Small Bus Econ 60, 639–657 (2023). https://doi.org/10.1007/s11187-022-00608-7

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11187-022-00608-7