Abstract

The main aim of the present research is to consider a monetary union’s economy consisting of N countries, N fiscal authorities (one for each country) and a single monetary authority. The fiscal authorities want to stabilise output and public debt through the primary government balance, and they can exhibit heterogeneous preferences about the trade-off between output and debt stability. Unlike these, the monetary authority has the aim of price and output stability. They play a non-cooperative policy game, in which they independently and simultaneously choose monetary and fiscal instruments to pursue their goals. In a dynamic setting, each authority must choose its policy instrument prevailing in the next period without knowing—at the end of each period—the choice of other authorities. By assuming static expectations, the present work shows the possibility of several dynamic outcomes. First, there exists one Nash equilibrium representing the optimal level for the macro economy; this equilibrium is stable if the average weight that fiscal authorities assign to output stability is not excessively high; therefore, this result holds even if some authorities are less willing to promote debt stabilisation. Second, in addition to this equilibrium, there exist other Nash equilibria representing steady-state values for macroeconomic variables that differ from the targets adopted by the authorities; these equilibria emerge and are stable if the authorities’ preference for output stability is even greater and with a higher degree of heterogeneity compared to the previous case. Third, the parameters of the model matter to determine the stability properties of the equilibria, and the analysis shows the possibility of nonlinear dynamics.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The financial crisis and the COVID-19 pandemic destabilised the world economy, leading to a significant contraction in economic activity. The Economic and Monetary Union (EMU) also suffered from the negative impact of the sovereign debt crisis; indeed, as Fig. 1 shows, GDP only returned to pre-financial crisis levels in 2014, to fall again heavily in 2020 due to the health measures implemented to contrast the COVID-19 pandemic.

GDP Euro Area (selected countries). Source: Eurostat

During this period, despite adopting a strongly expansionary monetary policy, the European Central Bank could not thoroughly cushion the adverse effects of the financial and health shocks due to the limits imposed by the so-called liquidity trap, namely, the zero lower bound; as a result, national governments had to adopt expansionary fiscal policies. Figure 2 shows, however, that in the aftermath of the financial crisis, the level of the primary budget deficit is highly uneven across countries: for instance, in 2009, burdened by the substantial weight of public debt, Italy limited its recourse to expansionary fiscal policy; in contrast, Spain had a primary budget deficit of over 9.0 per cent. Differently, in the aftermath of the COVID-19 pandemic, the EMU countries moved homogeneously, recording budget deficits close to the euro area average of just over 5.0 per cent.

Primary government balance, Euro Area (selected countries). Source: our elaborations on Eurostat data

Except for Germany, Fig. 3 reveals that the main implication of these processes has been the rise in public debt, which is particularly relevant for countries such as Greece and Italy, with the debt/GDP ratio above 190.0 and 150.0 per cent, respectively, but also for France and Spain, where the ratio stood above 110.0 per cent in 2021. In the current context, these countries are called upon to undertake a process of debt stabilisation, taking into account the existing restrictive stance of monetary policy aimed at reducing the inflation rate; therefore, a question arises of optimal management of the interaction between the fiscal policies adopted by the national authorities and the monetary policy set by the ECB.

Public debt, Euro Area (selected countries). Source: Eurostat data

A strand of the literature has extensively used a reduced form of the New Keynesian macroeconomic model (Woodford, 2003) to study the strategic interaction between monetary and fiscal authorities within a monetary union (Bofinger & Mayer, 2007; Bofinger et al., 2006; Chortareas & Mavrodimitrakis, 2021; Foresti, 2015). The analytical framework consists of a static policy game, where the agents usually act independently and simultaneously; as a result, a Cournot–Nash equilibrium emerges, which is stable in the sense that each authority achieves the best possible result by minimising its objective function. The benchmark finding of this literature is defined by the concept of symbiosis, according to which if all authorities consider the same economic variables of concern, namely, inflation and output, and share the same target values, then the interaction between the individual monetary authority and the various fiscal authorities results in a Nash equilibrium in which each authority achieves the respective target values for the target variables, independently from the institutional framework and the relative weights attributed to these variables (Dixit & Lambertini, 2001, 2003a, 2003b; Kempf & Von Thadden, 2013). When regional economies are homogeneous and fiscal authorities present identical preferences, in the absence of exogenous shocks, whether symmetrical or asymmetrical, affecting the demand side or the supply side, the symbiosis result also holds if fiscal authorities care about the level of public debt, such that they do not anymore share the same target variables of the monetary authority. Thus, in this context, fiscal authorities can stabilise the debt level to its target value unless exogenous shocks occur, or countries diverge on the initial debt level (Foresti, 2015, 2018; Mavrodimitrakis, 2022).

However, the literature has emphasised that the problem of debt stabilisation needs to be studied in the context of a dynamic policy game (Chortareas & Mavrodimitrakis, 2021: p. 343, Footnote 2; Tabellini, 1986; Bacchiocchi et al., 2023); in a static policy game, indeed, where the agents act simultaneously, it is not possible to analyse the convergence process towards the Nash equilibrium. In a two-period model describing the economy of a monetary union, Beetsma and Bovenberg (1999) analyse the impact of an inflation bias on the accumulation of public debt; using the same framework, Beetsma and Bovenberg (2005) focus on the labor-market distortions while Beetsma and Bovenberg (2006) on political shocks. In this respect, Purificato and Sodini, (2023) show that in a multi-period dynamic setting, a simple decision process driven by the best response mechanism does not guarantee convergence to steady-state equilibrium if the relative weight given by the fiscal authority to output stability is sufficiently high compared to the weight given to debt stability, also with identical regional economies and fiscal authorities, and in the absence of exogenous shocks. These arguments motivate the present work, which extends the analysis by Purificato and Sodini, (2023) to the case of heterogeneous fiscal authorities for the weight given to the debt stabilisation process.

The analytical framework of the model is as follows. Based on Mavrodimitrakis (2022), the dynamic model describes a monetary union’s economy, consisting of N homogeneous regions: there are no asymmetries across individual economies. A supply and demand model defines the economic structure for each region and the whole monetary union. The single monetary authority sets the policy rate to pursue the objective of macroeconomic stability, which implies both price and output stability; in contrast, national fiscal authorities aim at output stability and debt stability through the determination of the primary government balance, and they may exhibit heterogeneous preferences regarding the trade-off between output and debt stability. The monetary authority and national fiscal authorities interact through a policy game, where both authorities act independently and simultaneously; therefore, their best reaction functions imply that the policy rate is a function of the average primary government balance implemented by fiscal authorities while each primary government balance is a function of the policy rate implemented by the monetary authority. However, in a dynamic setting, at the end of each period, since the authorities independently and simultaneously set the level of their policy instruments for the next period, they do not know the choice of other authorities for the subsequent period; therefore, the critical assumption is that one of the static expectations, such that each authority sets the level of its policy instrument for the next period considering the current levels of policy tools set by other authorities.

As the first result of our analysis, we find that if all national fiscal authorities are perfectly homogeneous, then there is only one steady-state Nash equilibrium, where the equilibrium values of the variables are equal to the target level adopted by the authorities, which is the optimal level for macroeconomic stability. However, this target equilibrium becomes unstable whether the fiscal authorities’ preferences overly favour output stability rather than debt stability. Specifically, as the weight given to output stability increases, the dynamics first do not converge to the stationary state but are captured by a limit cycle showing persistent oscillations, and then they become explosive. This result also holds if national fiscal authorities are heterogeneous concerning their preferences; nevertheless, the threshold that discriminates between the different dynamics of the model depends on the average weight that fiscal authorities attach to the output stability. In this context, despite several fiscal authorities can have extreme preferences for output stability, the target equilibrium defines a steady state that is still locally stable, with all economies and successfully pursuing a debt stabilisation process. As the second result, given N the number of regions belonging to the monetary union, the presence of heterogeneous preferences of the fiscal authorities leads to the emergence of \(N-1\) Nash equilibria, in addition to the one with the steady-state values coinciding with the optimal values adopted by the authorities. In this case, though, the equilibrium values of the inflation rate, the output gap and the debt level diverge from the one adopted by the authorities as the target; therefore, each authority fails in pursuing its own macroeconomic goal. These no-target equilibria are stable if the average weight assigned by the fiscal authorities to output stability is greater than the threshold determining the stability of the other steady-state equilibrium and if its variance is sufficiently high; similarly to the previous case, as the weight attributed to output stability increases, the dynamics of the model are first captured by a limit cycle, and then they become explosive. As the third result, the parameters of the model matter to determine the stability properties of the equilibria by noting also that if one equilibrium is stable the other is unstable. Moreover, regarding both the target equilibrium and no-target equilibria, if the preferences of the fiscal authorities are not too biased in favour of the output gap stabilisation and are quite similar, then numerical simulations reveal that the basins of attraction are large enough to include initial conditions associated with all debt levels that have a minimum of economic significance. In this context, there is always a sufficiently gradual convergence process for the debt level to prevent explosive dynamics or excessive economic instability.

The rest of the article proceeds as follows. Section 2 presents the analytical framework and the details concerning the structure of the economy and the authorities’ behaviour. Section 3 moves towards the dynamic analysis of the model to detect the presence of steady-state equilibria and their stability conditions while Sect. 4 concludes the article.

2 The Model

A strand of the literature has extensively used a reduced form of the New Keynesian macroeconomic model to study the interaction between monetary and fiscal authorities within a monetary union (Foresti, 2018). In a static policy game, the agents usually act independently and simultaneously; as a result, a Cournot–Nash equilibrium emerges, which is stable in the sense that each authority achieves the best possible result by minimizing its objective function. Nevertheless, since it is a simultaneous game, it is not possible to analyse the convergence process towards the equilibrium; moreover, the literature has emphasised that the problem of debt stabilisation needs to be studied in the context of a dynamic policy game (Chortareas & Mavrodimitrakis 2021: p. 343, Footnote 2).

These arguments motivate our choice to present a dynamic version of the reduced form of the New Keynesian macroeconomic model to analyse the issue of debt stabilisation within a monetary union.

Section 2.1 describes the structure of the economy, while Sects. 2.2 and 2.3 present the decision problem of the monetary authority and the fiscal authorities.

2.1 The Economic Block

The economic structure of the monetary union consists of N regions or countries; referring to their size and the parameters describing the characteristics of their economies, these regions are assumed to be perfectly homogeneous. For the entire monetary union and each region belonging to it, the model’s economic block describes the economy’s supply and demand sides and the law of debt accumulation.

The supply equation for region k reads as follows:

In (1), the variable \(\pi _{t}^{k}\) identifies the inflation rate for region k at time t, which positively depends on the inflation rate expected by private agents \(\left( \pi _{t}^{e}\right)\) and the output gap for region k at time \(t\) \(\left( y_{t}^{k}=\frac{ Y_{t}^{k}-Y_{P}^{k}}{Y_{P}^{k}}\right)\), which defines the difference, measured in percentage points of the potential output \(\left( Y_{P}^{k}\right)\), between the actual output \(\left( Y_{t}^{k}\right) \) and the potential output \(\left( Y_{P}^{k}\right)\); notice that the potential output is constant over time and identifies the maximum level of production that economies can achieve. Finally, the parameter \(\gamma >0\) represents the sensitivity of the inflation rate with respect to the output gap. Notice that the expected inflation rate by private agents is equal to the target inflation rate set by the monetary authority \(\left( \pi _{t}^{e}=\pi ^{T}\right)\); therefore, we assume that inflation expectations are anchored and do not vary across regions, namely, these expectations are common knowledge throughout the union. Thus, this means that we are assuming that the monetary authority is credible.

Considering that the regions are identical in terms of economic size and the expected inflation rate coincides with the target inflation rate \(\left( \pi _{t}^{e}=\pi ^{T}\right)\), the supply equation for the whole monetary union becomes:

Equation (2) defines the inflation rate for the whole monetary union \(\left( \pi _{t}\right)\) as a positive function of the average output gap, which is nothing more than the average of the output gap obtained in each region \(\left( y_{t}^{k}\right)\). Particularly, if the average output gap is greater than zero, then the actual inflation rate is higher than the target inflation rate \(\left( \pi _{t}>\pi ^{T}\right)\); conversely, the actual inflation rate is lower than the target inflation rate \(\left( \pi _{t}<\pi ^{T}\right)\). In this context, even if the regions’ output gap differ from zero, a sufficient condition for the actual inflation rate to coincide with the target adopted by the monetary authority is that the actual output equals the potential output at the level of the whole monetary union \(\left( \sum _{k=1}^{N}y_{t}^{k}=0\right)\).

Regarding the demand side of the economy, the demand equation for region k reads as follows:

In Eq. (3), the variable \(i_{t}\) identifies the nominal interest rate, which is equal to the policy rate autonomously set by the monetary authority, while the parameter \(\delta >0\) represents the sensitivity of the aggregate demand with respect to the expected real interest rate \(\left( i_{t}-\pi _{t}^{e}\right)\). In this case, we follow Mavrodimitrakis (2022), rather than Foresti (2015) that assumes that the aggregate demand depends on the actual interest rate \(\left( i_{t}-\pi _{t}\right)\), since this assumption allows us to simplify the algebraic manipulation without affecting analytical findings. The variable \(g_{t}^{k}\) identifies the primary government balance for region k and is expressed as a percentage of the potential output: if \(g_{t}^{k}>0\), then the regional government is adopting an expansionary fiscal stance through a primary deficit; on the contrary, if \(g_{t}^{k}<0\), then there is a contractionary fiscal stance through a primary surplus. The parameter \(\omega >0\) captures the sensitivity of the aggregate demand with respect to the primary government budget, so that this parameter represents the fiscal multiplier. Finally, the parameter \(a>0\), expressed as a percentage of the potential output, captures the autonomous components of the aggregate demand, not affected by the economic policy tools as the policy rate and the primary government balance, which only depend on the behaviour of private agents.

By averaging the aggregate demands of all identical regions and remembering that the expected inflation rate is equal to the target inflation rate \( \left( \pi _{t}^{e}=\pi ^{T}\right)\), the demand equation for the monetary union becomes:

In Eq. (4), the average output gap for the whole monetary union \(\left( y_{t}\right)\) depends positively on the average primary government balance \(\left(g_{t}= \frac{1}{N}\left( \sum _{k=1}^{N}g_{t}^{k}\right) \right)\) and negatively on the policy rate \( \left( i_{t}\right)\). If the sum of the regional primary government balances is equal to zero \(\left( \sum _{k=1}^{N}g_{t}^{k}=0\right)\), then the policy rate that determines an average output gap for the monetary union equal to zero \(\left( y_{t}=0\right)\) is given by the following expression:

The expression in (5) identifies the natural interest rate \( \left( i_{n}\right)\), and Eq. (5) shows that the higher the parameter \(\delta\), the lower the natural rate of interest \( \left( i_{n}\right)\); conversely, the higher the parameter a, the higher the natural rate of interest \(\left( i_{n}\right)\). Thus, we avoid following the literature that assumes \(a=0\) to simplify exposition (Mavrodimitrakis, 2022), since this would mean assuming an artificially low value for the natural rate of interest; moreover, as emphasised by Purificato and Sodini, (2023), the value of a influences key features of the dynamic behaviour of the system.

The last element of the economic block of the model consists of the law of debt accumulation. Recalling that this strand of literature assumes a medium-term time perspective and a constant potential output over time, we follow Foresti (2015; 2018) and Mavrodimitrakis (2022) in defining the law of debt accumulation concerning the generic region k; it reads as follows:

The variable \(d_{t}^{k}\), expressed as a percentage of the potential output, identifies the debt level for region k at time t. Equation (6) assumes that the regional government issues bonds at a fixed interest rate, which corresponds to the policy rate, and carries out a complete rollover of the debt net of repayments at the end of any period. Under these hypothesis, the debt level at the end of time \(t+1\) is equal to the debt accumulated at the end of time t \(\left( d_{t}^{k}\right)\), plus the debt service \(\left( i_{t}d_{t}^{k}\right)\), plus the primary government balance accrued during the period \(t+1\) \(\left( g_{t+1}^{k}\right)\). Notice that the law of debt accumulation also represents a budget constraint for the regional fiscal authority when it chooses the primary government balance.

2.2 The Monetary Authority

The monetary authority aims to achieve the goal of macroeconomic stability, handling the trade-off between price and output stability. Specifically, the monetary policy determines the level of the policy rate to target specific long-run values for the inflation rate \(\left( \pi ^{T}\right)\) and the output gap \(\left( y_{M}^{T}\right)\) at the level of the monetary union; therefore, the information set of the monetary authority only considers aggregate data, regardless of the economic situation of individual regions. To keep the exposition and algebraic manipulation of the analytical model as simple as possible, we take the standard assumption that the targets for both the average inflation rate and the average output gap are equal to zero \(\left( \pi^{T}=y_{M}^{T}=0\right)\). Under these assumption, the objective function of the monetary authority reads as follows (Bacchiocchi & Giombini, 2021):

In Eq. (7), the parameter \(\beta \ge 0\) represents the relative weight of output stability with respect to price stability. If the monetary authority only cares price stability \(\left( \beta =0\right)\), then a regime of strict inflation targeting prevails; differently, if the authority considers both price and output stability \( \left( \beta >0\right)\), then a regime of flexible inflation targeting holds. The timing of the model implies that the monetary authority sets the policy rate at the end of a generic period \((t-1,t]\) for the next period \( (t,t+1]\); therefore, the variables \(E_{M}\left[ \pi _{t+1}\right]\) and \( E_{M}\left[ y_{t+1}\right]\) define the monetary authority’s expectation about the value of the average inflation rate and the average output gap at time \(t+1\), respectively. Notice that the actual value of these variables depends on the average primary government balance determined by the decisions of the regional fiscal authorities; nevertheless, all authorities act simultaneously and independently of each other, so that the information set of the monetary authority does not include the actual choice concerning the primary government balance. In this context, the monetary’s authority expectation about the value of the average inflation rate and the average output gap at time \(t+1\) only depends on its expectation concerning the average primary government balance determined by the decisions of the regional fiscal authorities \(E_{M}\left[ g_{t+1}\right]\).

Considering the constraints represented by the supply and demand equation for the whole monetary union (Eqs. (2) and (4)), the monetary authority sets the policy rate to minimise deviations of the average output gap and the average inflation rate from their target values; therefore, the optimisation problem of the monetary authority becomes:

where \(i_{low}\) defines the so-called lower bound faced by the monetary authority.

By substituting the constraints in the objective function and differentiating with respect to the policy rate \(\left( i_{t+1}\right)\), we obtain the reaction function of the monetary authority:

Equation (9) shows that the policy rate is a positive function of the expected fiscal stance at the union level \(\left( \frac{1}{N} \sum _{k=1}^{N}E\left[ g_{t+1}^{k}\right] \right)\) and the autonomous component of the aggregate demand \(\left( a\right)\). Notice that the monetary policy and the expected fiscal policy for the whole monetary union are perfect substitutes: if regional fiscal authorities are expected to implement an expansionary fiscal policy \(\left( \sum _{k=1}^{N}E\left[ g_{t+1}^{k}\right] >0\right)\), then the monetary authority will set the policy rate above the natural level \(\left( i_{t+1}>i_{n}=\frac{a}{\delta } \right)\) in order to offset the positive effects of fiscal stance on the aggregate demand and, in turn, on the inflation rate; otherwise, if a contractionary fiscal policy is expected \(\left( \sum _{k=1}^{N}E\left[ g_{t+1}^{k}\right] <0\right)\), then the monetary authority will set the policy rate below the natural level \(\left( i_{t+1}<i_{n}=\frac{a}{\delta } \right)\), in order to offset the negative effects of fiscal stance on the aggregate demand and, in turn, on the inflation rate. Notice that the reaction function of the monetary authority does not depend on either the sensitivity of the inflation rate with respect to the output gap \(\left( \gamma \right)\) or the weight attached to output stability compared to price stability \(\left( \beta \right)\). As we have assumed the absence of exogenous supply-side shocks in order to focus the analysis on the role of preferences and the behaviour of the fiscal authority. In this context, the so-called “divine coincidence” holds (Blanchard & Galí, 2017), whereby the monetary authority can always stabilise the inflation rate at its target level while simultaneously stabilising the output gap at its target level; essentially, the trade-off between price stability and output stability disappears.

2.3 The Fiscal Authority

By implementing its decision concerning the primary government balance, the fiscal authority for region k has to handle the trade-off between debt and output stability. It targets specific long-run values for the debt level \(\left( d_{F}^{k,T}\right)\) and the output gap \(\left( y_{F}^{k,T}\right)\); precisely because of the time horizon that characterises the decisions taken by the regional fiscal authority, it seems more appropriate to take the level of debt as a fiscal policy’s goal rather than the primary government balance (Mavrodimitrakis, 2022). To simplify the exposition and algebraic manipulation, we hold the standard assumption that both the target debt level and the target output gap are equal to zero \(\left( d_{F}^{k,T}=y_{F}^{k,T}=0\right)\). Under these assumption, the objective function of the regional fiscal authority reads as follows:

In Eq. (10), the parameter \(\alpha ^{k}\ge 0\) represent the relative weight that the fiscal authority for region k attaches to output stability with respect to debt stability: the higher \( \alpha ^{k}\), the greater the government’s preference to keep the level of economic activity as close to the target as possible. Symmetrically to the case of the monetary authority, the timing of the model implies that the regional fiscal authority sets the primary government balance at the end of a generic period \((t-1,t]\) for the next period \((t,t+1]\); therefore, the variable \(E_{F}^{k}\left[ y_{t+1}^{k}\right]\) defines the fiscal authority’s expectation about the output gap at time \(t+1\). Since its actual value depends on the policy rate determined simultaneously and independently by the monetary authority, the information set of the fiscal authorities does not include the actual choice concerning the policy rate; as a consequence, the regional fiscal authority’s expectation about the output gap at time \(t+1\) only depends on its expectation concerning the policy rate determined by the decisions of the monetary authority \(E_{F}^{k}\left[ i_{t+1}\right]\). Notice that the regional government issues bonds at a fixed interest rate, which corresponds to the policy rate, and carries out a complete rollover of the debt net of repayments at the end of any period. Under these hypothesis, Eq. (6) implies that the policy rate at time \(t+1\) does not affect the debt level at time \(t+1\), which only depends on the policy rate of the previous period.

Considering the constraints represented by the demand equation and the law of debt accumulation (Eqs. (4) and (6)), the fiscal authority for region k sets the primary government balance to minimise deviations of the debt level and the output gap from their target values; therefore, the optimisation problem of the regional fiscal authority becomes:

where \(g_{low}<0\) defines a lower bound for the primary government surplus since we assume that the fiscal authority cannot implement an excessively restrictive fiscal policy due to the possible opposition from voters.

By substituting the constraints in the objective function and differentiating with respect to the primary government balance \(g_{t+1}^{k}\), we obtain the reaction function of the fiscal authority for region k:

Equation (12) shows that the fiscal stance of a generic region responds to two separate drivers. First, the expected monetary policy \(\left( E\left[ i_{t+1}\right] \right)\): if the regional fiscal authority’s expectations about the policy rate imply that its expected value is lower than the natural interest rate \(\left( E\left[ i_{t+1}\right] <i_{n}=\frac{a }{\delta }\right)\), then the fiscal stance tends to be contractionary to offset the positive monetary stimulus in support of the aggregate demand; differently, if the expected value of the policy rate is higher than the natural interest rate \(\left( E\left[ i_{t+1}\right] >i_{n}=\frac{a}{\delta } \right)\), then the fiscal stance tends to be expansionary to offset the negative monetary stimulus. Second, regarding the accumulated debt level \( \left( d_{t}^{k}\right)\), if the regional fiscal authority needs to implement a debt reduction process \(\left( d_{t}^{k}>0\right)\), then it tends to adopt a contractionary fiscal stance by achieving primary government surplus. Notice that the parameter \(\alpha ^{k}\) defines how much each of the two drivers weighs in the choices of the fiscal authority; in fact, if \(\alpha ^{k}=0\), only the accumulated debt affects the fiscal stance, while if \(\alpha ^{k}\rightarrow \infty\), only the objective of output stability influences the fiscal stance.

2.4 The Dynamic Model

In order to analyse the dynamic behaviour of the system, it is necessary to complete the model with mechanism underlying the formulation of expectations by the monetary and fiscal authorities. In this respect, the key assumption is that agents adopt a static process of expectation formation; namely, the monetary authority’s expectation concerning the average primary government budget at time \(t+1\) is equal to the average government budget at time t \(\left( \text {i.e. }\frac{1}{N}\left( \sum _{k=1}^{N}E\left[ g_{t+1}^{k}\right] \right) =\frac{1}{N}\left( \sum _{k=1}^{N}g_{t}^{k}\right) \right)\), while the regional fiscal authority’s expectation concerning the policy rate at at time \(t+1\) is equal to the policy at time t \(\left( E\left[ i_{t+1}\right] =i_{t}\right)\).

Under this assumption, the dynamics determining the time evolution of the economy are given by the following system:

comprised by \(2N+1\) equations.

In what follows, in order to characterise some properties of the economic model, we will often refer to the following dynamic system, in which the best response (Puu, 1991) of the authorities do not involve the bounds introduced on \(i_{low}\) and \(g_{low}\):

3 Dynamic Analysis

As the first step, in Sect. 3.1, we analyse the dynamic system defined in Eq. (14), representing the benchmark case. As the second step, in Sect. 3.2, we modify the model to represent the institutional framework of the EMU by introducing the 3% limit set by the Stability and Growth Pact (SGP) to the ratio of budget deficit to potential output. Thus, the benchmark model describes an economic context where this constraint is essentially ineffective, taking into account that the member states of the EMU have repeatedly violated the constraint defined by the SGP over time, both with the consent of the European Commission, in the case of severe recessions such as the one caused by the COVID-19 pandemic, and without the consent of the Commission.

3.1 The Benchmark Case

It is easy to show that there is no fixed point involving the lower bounds \( i_{low}\) or \(g_{low}\) because of the optimisation process; therefore, we directly focus on (14). Regarding the map (14), we obtain that the basic equilibrium \(d^{k}=g^{k}=0\) \(\forall k\) and \(i=\frac{a}{\delta }\) always exists and represents the steady-state equilibrium targeted by all authorities (henceforth target equilibrium). The target equilibrium implies that the policy rate converges the Wicksellian natural interest rate, namely, the interest rate that is consistent with a stable price level (Blanchard, 2017); moreover, all macroeconomic variables equal their target and optimal values: the inflation rate is equal to zero, as the output gap and the debt level.

For the analysis of the existence of other equilibria, from the first and third blocks in (14), it is possible to obtain the stationary-state expressions of \(g^{k}\) and i as functions of \(d^{k}\) (with \(d^{k}\ne \delta /\omega\) \(\forall k\)):

Substituting out the previous expressions in the second block of the system in (14),we get the following equations in the variables \( d^{k}\):

By removing the N-th equation of (16) from the other \(N-1\) equations of (16) we obtain that each stationary debt level for the remaining \(N-1\) countries can be expressed as a function of the debt of the N-th country:

Therefore, the steady-state level of the debt of country N is the solution of a polynomial of degree \(N-1\) with \(N-1\) possible roots. Once these values are determined, the other steady-state values follow from the Eqs. (17) and (15).

Specifying the model for \(N=2,\) we obtain that, other than the target equilibrium, another stationary equilibrium of the system exists if and only if \(\alpha _{1}\ne \alpha _{2}\) and in this case explicit expressions are available, which read as:

Going back to the general case, to study the stability properties of the stationary points, we consider the Jacobian matrix associated with the dynamic system (14), that is

where

evaluated at the steady states of the model.

Because of the size of (18) (\(\ge 5\)), the calculation of the eigenvalues becomes quite cumbersome meanwhile the Schur criterion, based on the coefficients of the characteristic polynomial (Fadali & Fisioli, 2013), represents a useful analytical and numerical tool for analysing the local stability of stationary equilibria.

In particular for the case \(N=2\), it is possible to identify the following necessary, but no sufficient, condition that has to hold for the stability of the targeted equilibrium:

Thus, given the fiscal authorities’ preferences, an increase in the natural interest rate or the fiscal multiplier determines a decrease in the size of the stability region of the Nash equilibrium where each authority achieves his target values in the steady state. Remember that the natural interest rate determines the speed of debt accumulation, while the fiscal multiplier represents the sensitivity of aggregate demand to a change in the primary government balance. The economic intuition behind inequality (19) is as follows. When the value of the parameter \(\omega\) is higher, the objective cost for the fiscal authority to stabilise the debt level increases in terms of output gap; at the same time, nevertheless, the need to resort to debt to offset the negative impact of a restrictive monetary policy decreases. Consequently, if the subjective cost of stabilising debt, defined by the preferences of the fiscal authority \(\left( \alpha \right)\), is sufficiently high, then the former effect is greater than the latter, leading to increasing instability in the economic system. Concerning \(i_{N}\), it aggravates the average debt burden associated with interest payments, increasing the objective cost of stabilising the debt level.

By analysing the Schur conditions for \(\alpha _{1}\ne \alpha _{2}\), when the two stationary equilibria exist it can be deduced that the two equilibria cannot be simultaneously stable (but can still be simultaneously unstable). This is because the quantity \(\frac{1}{i_{N}}-\frac{\left( \alpha _{1}+\alpha _{2}\right) }{2}\cdot \omega ^{2}\) must assume an opposite value. Following Blanchard et al. (2018), we can define a range of economically feasible values for the sensitivity of the aggregate demand with respect to the primary government budget \(\left( \omega \right)\) and the sensitivity of the aggregate demand with respect to the expected real interest rate \(\left( \delta \right)\); precisely, the parameter \(\omega\) must lie between 0.2 and 2.0, while the parameter \(\delta\) must be between 0.6 and 1.4. Regarding the natural interest rate \(\left( i_{N}\right)\), Barsky et al. (2014) and Brand et al. (2018) detect that its value has fluctuated considerably over time for both the US and euro area economies. To account for these fluctuations, we assume that \(i_{N}\) can vary between \(-3\%\) and \(8\%\). As a result, assuming values for the benchmark case \(\omega =1.4\) and \(\delta =0.8\), \(i_{N}=3\%\), the parameter a must necessarily be set to 0.024. Based on these values, Fig. 4a characterises the stability properties of the two stationary equilibria in the plane \((\alpha _{1},\alpha _{2})\) as expressed by Schur conditions.

Parameter values: \(\delta =0.8\), \(\omega =1.4\), \(i_{N}=3\%\), \(a=0.024\) with \(i_{low}=-0.01\) and \(g_{low}=0.2\). Panel (a) illustrates the stability/instability regions in the \((\alpha _{1},\alpha _{2})\) plane of the stationary equilibria by means of the Schur conditions. Panel (b) numerically illustrates the dynamic properties of the map in the \( (\alpha _{1},\alpha _{2})\) plane

The red and dark grey regions identify the space of parameters \((\alpha _{1},\alpha _{2})\) for which the target equilibrium and the no-target equilibrium are locally asymptotically stable, respectively; these two regions are largely separated by the straight line \(\frac{1}{i_{N}}-\frac{ \left( \alpha _{1}+\alpha _{2}\right) }{2}\cdot \omega ^{2}=0\). The yellow region identifies the parameter space \((\alpha _{1},\alpha _{2})\) for which no attracting equilibria exist. It can be deduced from the figure that heterogeneity of preferences with respect to the stability of the output gap does not necessarily imply instability of the economic system, which may converge to one of two steady states. The blue line highlights the emergence of oscillatory dynamics due to the Neimark–Sacker bifurcation when transitioning from the red or dark grey regions to the yellow region, while kee** one of the \(\alpha \) fixed and varying the other. More precisely, it identifies the union of two Neimark–Sacker bifurcation curves (touching at points A and B in the figure) determined by the stability/instability conditions of the model’s stationary equilibria. To investigate what happens also in the instability (yellow) region of stationary equilibria, Fig. 4b considers what occurs from initial conditions close to stationary equilibria. In particular, the tiny blue and white regions highlight the parameter space for which the dynamics are cyclical. In this case the trajectories are captured by a limit cycle born via Neimark–Sacker bifurcation around the target equilibrium and non-target equilibrium, respectively. Moving into the black and orange regions, the lower bound on the policy rate becomes binding and the trajectories involve this bound (after the border collision bifurcation). The light grey region identifies the parameter space for which the trajectories diverge. Namely, debt dynamics become explosive and regional economies fail to stabilise debt levels so that these economies risk to exit from the monetary union.

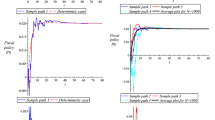

The results are further illustrated in the following set of figures. In Fig. 5a–e in which \(\alpha _{2}=20\), we let \(\alpha _{1}\) vary in the interval (13, 20). Through bifurcation diagrams of the variables of the model, we observe the onset of cyclic dynamics around the target equilibrium at around \(\alpha _{1}=16\) that involve the bound for i from \(\alpha _{1}=16.65\) onwards. The last figure (Fig. 5f) shows the dynamics of the variable \(i_{t}\) when \(\alpha _{1}=20\) highlighting the role played by \( i_{low}\).

Panel (a–e): bifurcation diagrams with respect to \(\alpha _{1}\). Panel (f): time series of \(i_{t}\) after the border collision bifurcation

Panel (a–e): bifurcation diagrams with respect to \(\alpha _{1}\); Panel (f): time series of \(i_{t}\) after the border collision bifurcation

In Fig. 6 we consider \(\alpha _{2}=43\) and we let \(\alpha _{1}\) vary in the interval (14, 17). After the Neimark–Sacker bifurcation we observe the onset of cyclic dynamics around the non-target equilibrium (from \(\alpha _{1}\simeq 15.14\) approx.), involving also \(i_{low}\) from \(\alpha _{1}\simeq 15.43\). In the numerical examples depicted in Figs. 5 and 6 the lower bound of g in not involved. The set of figures in Fig. 7 shows the evolution of the dynamics of the model with a higher value of \(g_{low}\) becoming binding from \(\alpha _{1}\simeq 16.528\).

Panel (a–e): bifurcation diagrams with respect to \(\alpha _{1}\); Panel (f): time series of \(g_{t}\) after the border collision bifurcation. The figure is plotted for \(g_{low}=-0.01\)

Although the analysis of basins of attraction for a dynamic system of dimension equal to 5 is somewhat difficult, from an extensive Monte Carlo study, it turns out that in the range of parameters introduced above, given a set of parameters such that one of the equilibria is stable, if the \( \alpha\) parameters differ from each other by less than \(70\%\) then the (unique) locally asymptotically stable equilibrium of the system captures all economically relevant initial conditions (setting \(i_{0}=a/\delta\) and \( g_{0}^{1}=g_{0}^{2}=0\), i.e., assuming that initially the policy authorities set the control variables at the target equilibrium level). If the parameters \(\alpha \) are further apart, it is possible that some initial levels of D do not guarantee convergence to the system’s equilibrium, even if they are locally attractive (see Fig. 8).

Basin of attraction of the target-equilibrium (red) and the set of initial conditions such that trajectories diverge (yellow). Parameter values: \(\alpha _{1}=13.1148\), \(\alpha _{2}=0.7142\), \( \delta =1.3472\), \(\omega =1.7284\) \(a=0.0602\), \(g_{low}=-0.2,\) \(i_{low}=-0.01\)

Compared to the case studied above, we now go on to analyse how variations in the model parameters change the stability/instability regions of the equilibria.

Panel (a–f): Stability/instability regions in the \((\alpha _{1},\alpha _{2})\) plane of the stationary equilibria

Parameter a plays a destabilising role with respect to the equilibria of the system. This means that as a increases, the parameter space \((\alpha _{1},\alpha _{2})\) for which the equilibria are stable decreases. This behaviour can be seen by looking at Figs. 9a and b, which are respectively drawn for \(a=-0.024\) (where the target equilibrium is stable for every value of \((\alpha _{1},\alpha _{2})\)) and \(a=0.064\). Unlike this, \( \omega \) plays a stabilising role, as shown by Figs. 9c and d, which are respectively drawn for \(\omega =0.2\) and \(\omega =2\). Finally \(\delta\), like the parameter \(\omega\), plays a stabilising role, as shown in Figs. 9e and f, drawn for \(\delta =0.6\) and \(\delta =1.4\), respectively. The economic intuition behind the results detailed above is as follows. The higher a, the higher the natural rate of interest; therefore, the debt growth rate increases due to the higher the debt burden and this contributes to destabilising the equilibrium of the system. The stabilising role of \( \omega\) is due to a lower primary deficit is sufficient to stabilise output and this, in turn, requires a lower debt burden. Like \( \omega\), parameter \(\delta\) is stabilising because the greater \(\delta\) is, the less interest rate change is required to stabilise the inflation rate.

The economic intuition behind the results detailed above is as follows. The higher a, the higher the natural rate of interest must be; therefore, the debt growth rate increases due to the higher the debt burden and this contributes to destabilise the equilibrium of the system. The role of \( \omega\) is stabilising because a lower primary deficit is sufficient to stabilise output and this, in turn, requires a lower debt burden. Like \( \omega\), parameter \(\delta\) is stabilising because the greater \(\delta\) is, the less is interest rate change required to stabilise the inflation rate.

3.2 The Institutional Framework of the EMU

The institutional framework of the EMU is characterised by the 3% limit set by the SGP to the ratio of budget deficit to potential output; therefore, this constraint concerns the sum of the debt burden, given by the product of the interest rate times the debt level, and the primary budget balance \(\left( g_{t}^{k}+i_{t}d_{t}^{k}\leqslant 0.03\right)\).

In this context, we note that the constraint \(g_{t}^{k}+i_{t}d_{t}^{k}=0.03\) in each country k can be binding either in a transient phase towards the target equilibrium (clearly in the target equilibrium where \(g^{k}\) and \( d^{k}\) are zero such a constraint cannot be binding) or it can make non-target equilibria unfeasible or, as shown in Fig. 10, it can partially modify the system’s dynamics in the presence of cycles. Comparing Figs. 4b and 10, which are plotted with the same parametric set, the role of the SGP is ambiguous as there are non-divergent trajectories in Fig. 4b and divergent trajectories in Fig. 10 and vice versa. On one hand, the analysis shows that this constraint is not able to stabilise the business cycle. On the other hand, it plays an ambiguous role in reducing divergence within the union because of the nonlinear interactions of the model. Indeed, the SGP restricts too high increases in the primary balance (government expenditure) and also reduces the possibility of intervening through government expenditure on income to reach the target.

The figure numerically illustrates the dynamic properties of the map in the \((\alpha _{1},\alpha _{2})\) plane. Parameter values: \(\delta =0.8\), \(\omega =1.4\), \(i_{N}=3\%\), \(a=0.024\) with \( i_{low}=-0.01\) and \(g_{low}=0.2\)

4 Conclusions

This article tackled a dynamic view of a monetary union’s economy consisting of N countries and N fiscal authorities (one for each country), which have the aim to stabilise output and debt over time, and a single monetary authority aiming to stabilise output and inflation. The fiscal authorities may exhibit heterogeneous preferences about the trade-off between output and debt stability. All authorities are independent of each other and choose simultaneously the policy tools to reach the target. The model is set up as a dynamic non-cooperative policy game in which, at the end of each period, the authorities do not know the choice of other authorities for the next period when choosing optimally the policy instruments prevailing in the next period.

The article belongs to a burgeoning literature about debt stabilisation and follows, more specifically, Foresti (2015) and Mavrodimitrakis (2022). It is generally motivated by the increasing pressure on public interventions followed by the Global Financial Crisis (2007–2008) and the recent COVID-19 pandemic, both events leading to a significant contraction of economic activity at the aggregate level. This contraction, indeed, called for the attention of fiscal and monetary authorities all over the world to sustain the macroeconomy. The theoretical modelling setting analysed in the present paper is closer to describing a monetary union economy, in which there exists one and only one monetary authority and N fiscal authorities (one authority for each member country) that must non-cooperatively and simultaneously try to get the target of output, inflation and debt stability over time through their own best reply (reaction) function. The dynamic game is studied by assuming static expectations so that each authority sets the level of its policy instrument for the next period considering the current level of other policy tools.

The analysis focuses on the role of fiscal authorities’ preferences about the trade-off between output and debt stability, pinpointing several outcomes. First, if all national fiscal authorities are perfectly homogeneous, then there is only one steady-state Nash equilibrium, where the equilibrium values of the variables are equal to the optimal level for macroeconomic stability. However, this target equilibrium becomes unstable whether the fiscal authorities’ preferences overly favour output stability rather than debt stability: as the weight given to output stability increases, the dynamics first are captured by a limit cycle showing persistent oscillations, and then they become explosive. Most interesting, this result also holds if national fiscal authorities are heterogeneous concerning their preferences, with the threshold that discriminates between the different dynamics of the model that depends on the average weight attributed by fiscal authorities to the output stability. In this context, despite several authorities being less willing to promote debt stabilisation, the target equilibrium identifies a steady state that is still stable, with all economies continuously and successfully pursuing a debt stabilisation process. Second, in addition to the target equilibrium, the presence of heterogeneous preferences leads to the emergence of several Nash equilibria; in this case, though, the equilibrium values of the inflation rate, the output gap and the debt level diverge from the one adopted by the authorities as the target, such that each authority fails in pursuing its own macroeconomic goal. These no-target equilibria are stable if the average weight assigned by the fiscal authorities to output stability is greater than the threshold determining the stability of the other target equilibrium and if its variance is sufficiently high; similarly to the previous case, as the weight attributed to output stability increases, the dynamics of the model are first captured by a limit cycle, and then they become explosive. Finally, all steady-state equilibria are alternatives to each other since a specific combination of fiscal authorities’ preferences is only compatible with one steady-state equilibrium; moreover, for reasonable values of macroeconomic variables, initial conditions do not matter to determine the convergence towards the equilibrium. Thus, the article can give several macroeconomic policy recipes depending on the extent of the preferences of the authorities.

References

Bacchiocchi, A., & Giombini, G. (2021). An optimal control problem of monetary policy. Discrete and Continuous Dynamical Systems B, 26(11), 5769–5786.

Bacchiocchi, A., Bellocchi, A., Bischi, G.I., Travaglini, G. A non-linear model of publicdebt with bonds and money finance. Economia Politica (2023). https://doi.org/10.1007/s40888-023-00310-1

Barsky, R., Justiniano, A., & Melosi, L. (2014). The natural rate of interest and its usefulness for monetary policy. American Economic Review, 104(5), 37–43.

Beetsma, R., & Bovenberg, L. (1999). Does monetary unification lead to excessive debt accumulation? Journal of Public Economics, 74(3), 299–325.

Beetsma, R., & Bovenberg, L. (2005). Structural distortions and decentralized fiscal policies in EMU. Journal of Money, Credit and Banking, 37(6), 1001–1018.

Beetsma, R., & Bovenberg, L. (2006). Political shocks and public debt: The case for a conservative central bank revisited. Journal of Economic Dynamics and Control, 30(11), 1857–1883.

Blanchard, O. (2017). Macroeconomics. Pearson Education Limited.

Blanchard, O., & Galí, J. (2007). Real wage rigidities and the New Keynesian model. Journal of Money, Credit and Banking, 39(s1), 35–65.

Blanchard, O., Leandro, A., Merler, S., & Zettelmeyer, J. (2018). Impact of Italy’s Draft Budget on Growth and Fiscal Solvency. Working Paper Policy Brief, Peterson Institute for International Economics (PIIE), PB18-24.

Bofinger, P., & Mayer, E. (2007). Monetary and fiscal policy interaction in the Euro area with different assumptions on the Phillips curve. Open Economies Review, 18(3), 291–305.

Bofinger, P., Mayer, E., & Wollmershäuser, T. (2006). The BMW model: A new framework for teaching monetary economics. Journal of Economic Education, 37(1), 98–117.

Brand, C., Bielecki, M., & Penalver, A. (2018). The natural rate of interest: Estimates, drivers, and challenges to monetary policy. Working Paper Occasional Paper, European Central Bank (ECB), December 217.

Chortareas, G., & Mavrodimitrakis, C. (2021). Policy conflict, coordination, and leadership in a monetary union under imperfect instrument substitutability. Journal of Economic Behavior & Organization, 183(March), 342–361.

Dixit, A., & Lambertini, L. (2001). Monetary–fiscal policy interactions and commitment versus discretion in a monetary union. European Economic Review, 45(4–6), 977–987.

Dixit, A., & Lambertini, L. (2003). Symbiosis of monetary and fiscal policies in a monetary union. Journal of International Economics, 60(2), 235–247.

Dixit, A., & Lambertini, L. (2003). Interactions of commitment and discretion in monetary and fiscal policies. American Economic Review, 93(5), 1522–1542.

Fadali, S., & Fisioli, A. (2013). Digital control engineering analysis and design. Elsevier.

Foresti, P. (2015). Monetary and debt-concerned fiscal policies interaction in monetary unions. International Economics and Economic Policy, 12, 541–552.

Foresti, P. (2018). Monetary and fiscal policies interaction in monetary unions. Journal of Economic Surveys, 32(1), 226–248.

Kempf, H., & Von Thadden, L. (2013). When do cooperation and commitment matter in a monetary union? Journal of International Economics, 91(2), 252–262.

Mavrodimitrakis, C. (2022). Debt stabilization and financial stability in a monetary union: Market versus authority-based preventive solutions. International Journal of Finance & Economics, 27(2), 2582–2599.

Purificato, F., & Sodini, M. (2023). Debt stabilisation and dynamic interaction between monetary and fiscal policy: In medio stat virtus. Communications in Nonlinear Science and Numerical Simulation, 118, 106980.

Puu, T. (1991). Chaos in duopoly pricing. Chaos, Solitons and Fractals, 1(6), 573–581.

Tabellini, G. (1986). Money, debt and deficits in a dynamic game. Journal of Economic dynamics and Control, 10(4), 427–442.

Woodford, M. (2003). Interest and prices. Foundations of a theory of monetary policy. Princeton University Press.

Acknowledgements

The authors acknowledge two anonymous reviewers of the journal for valuable comments on an earlier draft of the manuscript. The usual disclaimer applies.

Funding

Open access funding provided by Università di Pisa within the CRUI-CARE Agreement. Luca Gori acknowledges financial support from the University of Pisa under the "PRA -- Progetti di Ricerca di Ateneo" (Institutional Research Grants) -- Project No. PRA_2020_64 "Infectious diseases, health and development: economic and legal effects". Mauro Sodini acknowledges the Czech Science Foundation (GACR) under the Project 23-06282S and SGS Research Project SP2024/003 of VSB Technical University of Ostrava for financial support of this work and the financial support of the European Union under the REFRESH -- Research Excellence For REgion Sustainability and Hightech Industries project number CZ.10.03.01/00/22_003/0000048 via the Operational Programme JustTransition. Mauro Sodini and Francesco Purificato acknowledge support within the project "The Impact of Crises on Complex Spatial Economic Systems (ICCSES)", Programma FRA 2022 - Università di Napoli "Federico II" (DR/2022/2055 del 17/05/2022).

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Gori, L., Purificato, F. & Sodini, M. Debt Stabilisation and Dynamic Interaction Between Monetary Authority and National Fiscal Authorities. Comput Econ (2024). https://doi.org/10.1007/s10614-024-10561-0

Accepted:

Published:

DOI: https://doi.org/10.1007/s10614-024-10561-0