Abstract

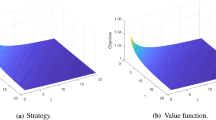

Motivated by empirical evidence for rough volatility models, this paper investigates continuous-time mean–variance (MV) portfolio selection under the Volterra Heston model. Due to the non-Markovian and non-semimartingale nature of the model, classic stochastic optimal control frameworks are not directly applicable to the associated optimization problem. By constructing an auxiliary stochastic process, we obtain the optimal investment strategy, which depends on the solution to a Riccati–Volterra equation. The MV efficient frontier is shown to maintain a quadratic curve. Numerical studies show that both roughness and volatility of volatility materially affect the optimal strategy.

Similar content being viewed by others

Notes

See, for example, Oxford-Man Institute’s realized library at https://realized.oxford-man.ox.ac.uk/data.

There are several equivalent formulations.

Available at https://github.com/differint/differint.

References

Gatheral, J., Jaisson, T., Rosenbaum, M.: Volatility is rough. Quant. Financ. 18, 933–949 (2018)

El Euch, O., Rosenbaum, M.: The characteristic function of rough Heston models. Math. Financ. 29, 3–38 (2019)

Guennoun, H., Jacquier, A., Roome, P., Shi, F.: Asymptotic behavior of the fractional Heston model. SIAM J. Financ. Math. 9, 1017–1045 (2018)

Heston, S.L.: A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 6, 327–343 (1993)

Fukasawa, M.: Asymptotic analysis for stochastic volatility: martingale expansion. Financ. Stoch. 15, 635–654 (2011)

El Euch, O., Fukasawa, M., Rosenbaum, M.: The microstructural foundations of leverage effect and rough volatility. Financ. Stoch. 22, 241–280 (2018)

El Euch, O., Rosenbaum, M.: Perfect hedging in rough Heston models. Ann. Appl. Probab. 28, 3813–3856 (2018)

Abi Jaber, E., Larsson, M., Pulido, S.: Affine Volterra processes. Ann. Appl. Probab. 29, 3155–3200 (2019)

Keller-Ressel, M., Larsson, M., Pulido, S.: Affine rough models. ar**v:1812.08486 (2018)

Fouque, J.P., Hu, R.: Optimal portfolio under fast mean-reverting fractional stochastic environment. SIAM J. Financ. Math. 9, 564–601 (2018)

Fouque, J.P., Hu, R.: Optimal portfolio under fractional stochastic environment. Math. Financ. 29, 697–734 (2018)

Bäuerle, N., Desmettre, S.: Portfolio optimization in fractional and rough Heston models. ar**v:1809.10716 (2018)

Zhou, X.Y., Li, D.: Continuous-time mean–variance portfolio selection: a stochastic LQ framework. Appl. Math. Optim. 42, 19–33 (2000)

Lim, A.E., Zhou, X.Y.: Mean–variance portfolio selection with random parameters in a complete market. Math. Oper. Res. 27, 101–120 (2002)

Lim, A.E.: Quadratic hedging and mean–variance portfolio selection with random parameters in an incomplete market. Math. Oper. Res. 29, 132–161 (2004)

Černý, A., Kallsen, J.: Mean-variance hedging and optimal investment in Heston’s model with correlation. Math. Financ. 18, 473–492 (2008)

Jeanblanc, M., Mania, M., Santacroce, M., Schweizer, M.: Mean-variance hedging via stochastic control and BSDEs for general semimartingales. Ann. Appl. Probab. 22, 2388–2428 (2012)

Shen, Y.: Mean–variance portfolio selection in a complete market with unbounded random coefficients. Automatica 55, 165–175 (2015)

Glasserman, P., He, P.: Buy rough, sell smooth. Quant. Financ. 1–16 (2019)

Revuz, D., Yor, M.: Continuous martingales and Brownian motion, vol. 293. Springer, New York (1999)

Gripenberg, G., Londen, S.O., Staffans, O.: Volterra Integral and Functional Equations, vol. 34. Cambridge University Press, Cambridge (1990)

Kraft, H.: Optimal portfolios and Heston’s stochastic volatility model: an explicit solution for power utility. Quant. Financ. 5, 303–313 (2005)

Zeng, X., Taksar, M.: A stochastic volatility model and optimal portfolio selection. Quant. Financ. 13, 1547–1558 (2013)

Shen, Y., Zeng, Y.: Optimal investment-reinsurance strategy for mean–variance insurers with square-root factor process. Insur. Math. Econom. 62, 118–137 (2015)

Abi Jaber, E., El Euch, O.: Multifactor approximation of rough volatility models. SIAM J. Financ. Math. 10, 309–349 (2019)

Mytnik, L., Salisbury, T.S.: Uniqueness for Volterra-type stochastic integral equations. ar**v:1502.05513 (2015)

Gerhold, S., Gerstenecker, C., Pinter, A.: Moment explosions in the rough Heston model. Decis. Econ. Financ. 42, 575–608 (2019)

Yong, J., Zhou, X.Y.: Stochastic Controls: Hamiltonian Systems and HJB Equations, vol. 43. Springer, New York (1999)

Luenberger, D.G.: Optimization by Vector Space Methods. Wiley, Hoboken (1968)

Veraar, M.: The stochastic Fubini theorem revisited. Stochastics 84, 543–551 (2012)

Diethelm, K., Ford, N.J., Freed, A.D.: A predictor-corrector approach for the numerical solution of fractional differential equations. Nonlinear Dynam. 29, 3–22 (2002)

Diethelm, K., Ford, N.J., Freed, A.D.: Detailed error analysis for a fractional Adams method. Numer. Algorithms 36, 31–52 (2004)

Li, C., Tao, C.: On the fractional Adams method. Comput. Math. Appl. 58, 1573–1588 (2009)

Abi Jaber, E.: Lifting the Heston model. Quant. Financ. 19, 1995–2013 (2019)

Brunner, H.: Volterra Integral Equations: An Introduction to Theory and Applications, vol. 30. Cambridge University Press, Cambridge (2017)

Gatheral, J., Keller-Ressel, M.: Affine forward variance models. Financ. Stoch. 23, 501–533 (2019)

Acknowledgements

The authors would like to thank two anonymous referees and the Editor for their careful reading and valuable comments, which have greatly improved the manuscript.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflicts of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix A: Solutions of Riccati–Volterra Equations

To demonstrate the existence and uniqueness of the solution to a Riccati–Volterra equation, we first rephrase the following result from a recent monograph [35] with more general assumptions. The underlying idea of the proof is the Picard iteration.

Theorem A.1

Suppose kernel \(K(\cdot )\) is bounded or is the fractional kernel with \(\alpha \in (0, 1)\). Let \(c_0, c_1, c_2\) be constant. Then there exists \(\delta >0\) such that

has a unique continuous solution f on \([0, \delta ]\).

Proof

Note that quadratic function is locally Lipschitz; then according to Theorem 3.1.2 and Theorem 3.1.4 in [35], the claim holds. \(\square \)

However, \(\delta \) in Theorem A.1 is not explicit. Tighter results exist if more assumptions are imposed.

We investigate g(a, t) in (2.8) first. Based on [36, Theorem A.5], we have

Lemma A.1

Suppose Assumption 2.1 holds and \(\kappa ^2 - 2a\sigma ^2 > 0\). Then (2.8) has a unique global continuous solution. Moreover,

where \(w_* \triangleq \frac{\kappa - \sqrt{\kappa ^2 - 2a \sigma ^2}}{\sigma ^2}\) and \(r_2(t) \triangleq Q^{-1}_2 \Big ( \int ^t_0 K(s) ds \Big )\); that is, the inverse function of \(Q_2\), given by

Proof

To apply the result in [36, Theorem A.5], we define

Then H(w) satisfies Assumption A.1 in [36] with \(w_{max} \triangleq \frac{\kappa }{\sigma ^2}\) and \(w_*\) defined above. The claim follows from [36, Theorem A.5(c)] with \(a(t) \equiv 0\) in their theorem. \(\square \)

For the specific fractional kernel \(K(t) = \frac{t^{\alpha -1}}{\varGamma (\alpha )}\), [7, Theorem 3.2] obtains the following tighter results and the proof is based on the scaling limits of the Hawkes processes.

Lemma A.2

If \(K(t) = \frac{t^{\alpha -1}}{\varGamma (\alpha )}\), \(\alpha \in (1/2, 1)\), then g(a, t) in (2.8) satisfies

with \(a_0(t) = \frac{1}{2\sigma ^2} \Big [ \kappa + \frac{t^{-\alpha }}{\varGamma (1-\alpha )} \Big ]^2\) and a constant \(c>0\). In other words, if \( a < a_0(T)\), then Assumption 2.3 is satisfied.

Next, we study \(\psi (\cdot )\) in (4.7). (4.7) has a unique continuous solution on some interval \([0, \delta ]\) if the conditions in Theorem A.1 are satisfied. Without Theorem A.1, we also have the following result.

Lemma A.3

Suppose Assumption 2.1 holds.

-

(1)

If \(1 - 2\rho ^2 > 0\), then (4.7) has a unique global continuous solution \(\psi \in L^2_{loc}({\mathbb {R}}_+, {\mathbb {R}})\) and \(\psi < 0\) for \(t>0\).

-

(2)

If \(1 - 2\rho ^2 = 0\), then (4.7) is linear and has a unique continuous solution on [0, T].

-

(3)

If \(1 - 2\rho ^2 < 0\), further assume \(\lambda >0\) and \(\lambda ^2 + 2(1-2\rho ^2)\theta ^2\sigma ^2 >0\). Then (4.7) has a unique global continuous solution. Moreover,

$$\begin{aligned} \frac{{\bar{w}}_*}{1-2\rho ^2}< \frac{{\bar{r}}_2(t)}{1-2\rho ^2} \le \psi (t) < 0, \quad \forall \; t > 0, \end{aligned}$$(A.5)with \({\bar{w}}_* = \frac{\lambda - \sqrt{\lambda ^2 + 2(1-2\rho ^2)\theta ^2\sigma ^2}}{ \sigma ^2}\) and \({\bar{r}}_2(t) \triangleq {\bar{Q}}^{-1}_2 \Big ( \int ^t_0 K(s) ds \Big )\), where

$$\begin{aligned} {\bar{Q}}_2(w) = \int ^w_0 \frac{du}{ \frac{\sigma ^2}{2} u^2 - \lambda u - (1-2\rho ^2)\theta ^2}. \end{aligned}$$(A.6)

Proof

The claim in (1) follows from [8, Theorem 7.1]. The continuity follows from the uniqueness of the global solution and [21, Theorem 12.1.1]. The claim in (2) is classic and can be found in [35, Theorem 1.2.3]. For (3), we consider \( {\tilde{\psi }} = (1 - 2 \rho ^2) \psi \). Then \({\tilde{\psi }} \) satisfies

Define

Then \({\bar{w}}_*\) is the unique root of \(H(w) = 0\) on \((-\infty , {\bar{w}}_{max}]\) with \({\bar{w}}_{max} = \frac{\lambda }{\sigma ^2}\). H(w) satisfies Assumption A.1 in [36]. Therefore, [36, Theorem A.5 (c)] with \(a(t) \equiv 0\) implies (A.7) has a unique global continuous solution and

Note \( {\tilde{\psi }} = (1 - 2 \rho ^2) \psi \). This gives the result desired. \(\square \)

Appendix B: Positivity of Integrals with Forward Variance

Lemma B.1

Suppose Assumption 2.1 holds. The forward variance \(\xi _t(s)\) in (4.3) satisfies \(\int ^T_t \xi _t(s) ds > 0\), \({\mathbb {P}}\)-\({\mathrm{a.s.}}\), for every \( t \in [0, T)\).

Proof

As \(\int ^T_t \xi _t(s) ds = \mathbb {{\tilde{E}}}[\int ^T_t V_s ds| {{\mathcal {F}}}_t]\) and \(V_s\) is non-negative by Theorem 2.2, it is sufficient to show that \(\int ^T_t V_s ds > 0\), \({\mathbb {P}}\)-\({\mathrm{a.s.}}\).

Given \(t \in [0, T)\), for \(\omega \in \varOmega \) such that \(V_s(\omega )\) is continuous in s, we suppose \(\int ^T_t V_s(\omega ) ds = 0\). By the continuity of \(V_s(\omega )\), \(V_s(\omega ) = 0\) for \(s \in [t, T]\). Using the argument given in [8, Theorem 3.5, Equation (3.8)], for \(0< h < T - t\), we have

As \(V_s (\omega ) = 0,\, s \in [t, t+h]\), then

This contradiction implies that \(\int ^T_t V_s ds > 0\), \({\mathbb {P}}\)-\({\mathrm{a.s.}}\), and the claim follows. \(\square \)

Rights and permissions

About this article

Cite this article

Han, B., Wong, H.Y. Mean–Variance Portfolio Selection Under Volterra Heston Model. Appl Math Optim 84, 683–710 (2021). https://doi.org/10.1007/s00245-020-09658-3

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00245-020-09658-3