Abstract

The vigorous development of green markets and the effective mitigation of economic policy fluctuations are current hotspots that intrigue our interest in exploring the causal relationships between green market returns and economic policy uncertainty (EPU). Green bonds, corporate environmental responsibility, green technology investment, and the carbon trading market are our research objects to comprehensively understand the interaction among them, from both macro and micro perspectives. Considering the importance of temporal heterogeneity and spillover direction in causation, we employ the time-varying Granger causality method to obtain bidirectional real-time identification. We find that green market returns exhibit a time-varying bidirectional causality with EPU over most of the sample period. In contrast, green markets are more a risk spillover than a recipient. Notably, this causality is vulnerable to exogenous financial risks, especially structural changes caused by the COVID-19 pandemic. Overall, this paper provides insights into the deep-seated causes of price fluctuations, volatile market uncertainty, and the interaction mechanism between them, as well as implications for market participants and policymakers.

Similar content being viewed by others

Data availability

Most of the basic data are publicly available, mainly from the Wind and IFind financial databases. Other data are calculated by authors, and the calculation method is shown in the text of this paper.

Notes

Due to space limitations, we put the introduction of the specific differences between the three algorithms and the formulas for generating Wald statistics in the appendix.

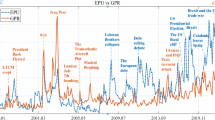

The data is obtained from the official website of S&P Dow Jones Indices: http://www.spglobal.com/spdji/en/.

References

Aimer N, Lusta A (2022) Asymmetric effects of oil shocks on economic policy uncertainty. Energy 241:122712

Algarni MA, Ali M, Albort-Morant G et al (2022) Make green, live clean! Linking adaptive capability and environmental behavior with financial performance through corporate sustainability performance. J Clean Prod 346:131156

Arora V, Shi S (2016) Energy consumption and economic growth in the United States. Appl Econ 48(39):3763–3773

Bai C, Yan H, Yin S et al (2021) Exploring the development trend of internet finance in China: perspective from club convergence. North Am J Econ Finance 58:101505

Bai L, Zhang X, Liu Y, Wang Q (2019) Economic risk contagion among major economies: new evidence from EPU spillover analysis in time and frequency domains. Physica A 535:122431

Baker SR, Bloom N, Davis SJ (2016) Measuring economic policy uncertainty. Q J Econ 131(4):1593–1636

Boutabba MA, Rannou Y (2021) Investor strategies in the green bond market: the influence of liquidity risks, economic factors and clientele effects. Int Rev Financ Anal 81:102071

Braouezec Y, Joliet R (2019) Time to invest in corporate social responsibility and the value of CSR operations: the case of environmental externalities. Manag Decis Econ 40(5):539–549

Chai G, You D, Chen J (2019) Dynamic response pattern of gold prices to economic policy uncertainty. Trans Nonferrous Met Soc China 29(12):2667–2676

Cheung YW, Lai KS (1995) Lag order and critical values of the augmented Dickey-Fuller test. J Bus Econ Stat 13(3):277–280

Dash SR, Maitra D (2021) Do oil and gas prices influence economic policy uncertainty differently: multi-country evidence using time-frequency approach. Q Rev Econ Finance 81:397–420

Deng Y, You D, Wang J (2022) Research on the nonlinear mechanism underlying the effect of tax competition on green technology innovation - an analysis based on the dynamic spatial Durbin model and the threshold panel model. Resour Policy 76:102545

Dogan E, Majeed AT, Luni T (2022) Are clean energy and carbon emission allowances caused by bitcoin? A novel time-varying method. J Clean Prod 347:131089

Dolado JJ, Lütkepohl H (1996) Making Wald tests work for cointegrated VAR systems. Economet Rev 15(4):369–386

Dou Y, Li Y, Dong K, Ren X (2022) Dynamic linkages between economic policy uncertainty and the carbon futures market: does Covid-19 pandemic matter? Resour Policy 75:102455

Elsayed AH, Naifar N, Nasreen S, Tiwari AK (2022) Dependence structure and dynamic connectedness between green bonds and financial markets: fresh insights from time-frequency analysis before and during COVID-19 pandemic. Energy Econ 107:105842

Ermoliev Y, Ermolieva T, Jonas M et al (2015) Integrated model for robust emission trading under uncertainties: cost-effectiveness and environmental safety. Technol Forecast Soc Chang 98:234–244

Farza K, Ftiti Z, Hlioui Z et al (2021) Does it pay to go green? The environmental innovation effect on corporate financial performance. J Environ Manage 300:113695

Feng S, Zhang R, Li G (2022) Environmental decentralization, digital finance and green technology innovation. Struct Chang Econ Dyn 61:70–83

Feng Y, Wang X, Liang Z (2021) How does environmental information disclosure affect economic development and haze pollution in Chinese cities? The mediating role of green technology innovation. Sci Total Environ 775:145811

Gao Y, Li Y, Wang Y (2021) Risk spillover and network connectedness analysis of China’s green bond and financial markets: evidence from financial events of 2015–2020. North Am J Econ Finance 57:101386

Garel A, Petit-Romec A (2021) Investor rewards to environmental responsibility: evidence from the COVID-19 crisis. J Corp Finan 68:101948

Gong X, Shi R, Xu J, Lin B (2021) Analyzing spillover effects between carbon and fossil energy markets from a time-varying perspective. Appl Energy 285:116384

Gong Y, He Z, Xue W (2022) EPU spillovers and stock return predictability: a cross-country study. J Int Finan Markets Inst Money 2022:101556

Gu K, Dong F, Sun H, Zhou Y (2021a) How economic policy uncertainty processes impact on inclusive green growth in emerging industrialized countries: a case study of China. J Clean Prod 322:128963

Gu X, Zhu Z, Yu M (2021b) The macro effects of GPR and EPU indexes over the global oil market—are the two types of uncertainty shock alike? Energy Econ 100:105394

Hammoudeh S, Ajmi AN, Mokni K (2020) Relationship between green bonds and financial and environmental variables: a novel time-varying causality. Energy Econ 92:104941

Han X, Cao T (2021) Study on corporate environmental responsibility measurement method of energy consumption and pollution discharge and its application in industrial parks. J Clean Prod 326:129359

Hou D, Chan KC, Dong M, Yao Q (2022) The impact of economic policy uncertainty on a firm’s green behavior: evidence from China. Res Int Bus Financ 59:101544

Hu D, Jiao J, Tang Y et al (2022) How global value chain participation affects green technology innovation processes: a moderated mediation model. Technol Soc 68:101916

Hu M, Zhang D, Ji Q, Wei L (2020) Macro factors and the realized volatility of commodities: a dynamic network analysis. Resour Policy 68:101813

Huynh TLD (2020) The effect of uncertainty on the precious metals market: new insights from Transfer Entropy and Neural Network VAR. Resour Policy 66:101623

Iacobuţă GI, Brandi C, Dzebo A, Duron SDE (2022) Aligning climate and sustainable development finance through an SDG lens. The role of development assistance in implementing the Paris Agreement. Glob Environ Chang 74:102509

Jiao L, Liao Y, Zhou Q (2018) Predicting carbon market risk using information from macroeconomic fundamentals. Energy Econ 73:212–227

Kartal MT (2022) The role of consumption of energy, fossil sources, nuclear energy, and renewable energy on environmental degradation in top-five carbon producing countries. Renewable Energy 184:871–880

Li G, Xue Q, Qin J (2022a) Environmental information disclosure and green technology innovation: empirical evidence from China. Technol Forecast Soc Chang 176:121453

Li X, Li Z, Su C et al (2022b) Exploring the asymmetric impact of economic policy uncertainty on China’s carbon emissions trading market price: do different types of uncertainty matter? Technol Forecast Soc Chang 178:121601

Liao B, Li L (2022) Spatial division of labor, specialization of green technology innovation process and urban coordinated green development: evidence from China. Sustain Cities Soc 80:103778

Lin B, Ma R (2022) Green technology innovations urban innovation environment and CO2 emission reduction in China: fresh evidence from a partially linear functional-coefficient panel model. Technol Forecast Soc Chang 176:121434

Ma R, Zhou C, Cai H, Deng C (2019) The forecasting power of EPU for crude oil return volatility. Energy Rep 5:866–873

Madaleno M, Dogan E, Taskin D (2022) A step forward on sustainability: the nexus of environmental responsibility, green technology, clean energy and green finance. Energy Econ 109:105945

Mccollum DL, Zhou W, Christoph B et al (2018) Energy investment needs for fulfilling the Paris agreement and achieving the sustainable development goals. Nat Energy 3(7):589–599

Pham L (2021) Frequency connectedness and cross-quantile dependence between green bond and green equity markets. Energy Econ 98:105257

Pham L, Nguyen CP (2022) How do stock oil and economic policy uncertainty influence the green bond market? Finance Res Lett 45:102128

Phillips PC, Perron P (1988) Testing for a unit root in time series regression. Biometrika 75(2):335–346

Phillips PCB, Shi S, Yu J (2015) Testing for multiple bubbles: historical episodes of exuberance and collapse in the S&P 500. Int Econ Rev 56(4):1043–1078

Psaradakis Z, Ravn MO, Sola M (2005) Markov switching causality and the money-output relationship. J Appl Economet 20(5):665–683

Rannou Y, Boutabba MA, Barneto P (2021) Are green bond and carbon markets in Europe complements or substitutes? Insights from the activity of power firms. Energy Econ 104:105651

Reboredo JC (2018) Green bond and financial markets: co-movement, diversification and price spillover effects. Energy Econ 74:38–50

Ren X, Dou Y, Dong K, Li Y (2022a) Information spillover and market connectedness: multi-scale quantile-on-quantile analysis of the crude oil and carbon markets. Appl Econ 54(38):4465–4485

Ren X, Duan K, Tao L, Shi Y, Yan C (2022b) Carbon prices forecasting in quantiles. Energy Econ 108:105862

Ren X, Li Y, Yan C, Wen F, Lu Z (2022c) The interrelationship between the carbon market and the green bonds market: evidence from wavelet quantile-on-quantile method. Technol Forecast Soc Chang 179:121611

Rjiba H, Jahmane A, Abid I (2020) Corporate social responsibility and firm value: guiding through economic policy uncertainty. Financ Res Lett 35:101553

Sajid MJ, Niu H, Liang Z, **e J et al (2021) Final consumer embedded carbon emissions and externalities: a case of Chinese consumers. Environ Dev 39:100642

Sartzetakis ES (2021) Green bonds as an instrument to finance low carbon transition. Econ Chang Restruct 54:1–25

Severo EA, Guimarães JCF, Dellarmelin ML (2021) Impact of the COVID-19 pandemic on environmental awareness, sustainable consumption and social responsibility: evidence from generations in Brazil and Portugal. J Clean Prod 286:124947

Shahzad F, Bouri E, Mokni K, Ajmi AN (2021) Energy, agriculture, and precious metals: evidence from time-varying Granger causal relationships for both return and volatility. Resour Policy 74:102298

Shen F, Liu B, Luo F et al (2021) The effect of economic growth target constraints on green technology innovation. J Environ Manage 292:112765

Shi S, Hurn S, Phillips PC (2020) Causal change detection in possibly integrated systems: revisiting the money-income relationship. J Financ Economet 18:158–180

Shi S, Phillips PC, Hurn S (2018) Change detection and the causal impact of the yield curve. J Time Ser Anal 39(6):966–987

Simeth N (2021) The value of external reviews in the secondary green bond market. Finance Res Lett 46:102306

Stolbov M, Shchepeleva M (2020) Systemic risk, economic policy uncertainty and firm bankruptcies: evidence from multivariate causal inference. Res Int Bus Financ 52:101172

Su C, Huang S, Qin M, Umar M (2021) Does crude oil price stimulate economic policy uncertainty in BRICS? Pac Basin Financ J 66:101519

Swanson NR (1998) Money and output viewed through a rolling window. J Monet Econ 41(3):455–474

Tang C, Xu Y, Hao Y et al (2021) What is the role of telecommunications infrastructure construction in green technology innovation? A firm-level analysis for China. Energy Econ 103:105576

Thoma MA (1994) Subsample instability and asymmetries in money-income causality. J Econom 64(1–2):279–306

Tiwari AK, Abakah EJA, Gabauer D et al (2022) Dynamic spillover effects among green bond, renewable energy stocks and carbon markets during COVID-19 pandemic: implications for hedging and investments strategies. Glob Financ J 51:100692

Tiwari AK, Abakah EJA, Le T et al (2021) Markov-switching dependence between artificial intelligence and carbon price: the role of policy uncertainty in the era of the 4th industrial revolution and the effect of COVID-19 pandemic. Technol Forecast Soc Chang 163:120434

Toda HY, Yamamoto T (1995) Statistical inference in vector autoregressions with possibly integrated processes. J Econom 66(1–2):225–250

United Nations Global Compact, 2019. Scaling finance for the sustainable development goals.

Wang J, He X, Ma F, Li P (2022a) Uncertainty and oil volatility: evidence from shrinkage method. Resour Policy 75:102482

Wang J, Lu X, He F, Ma F (2020) Which popular predictor is more useful to forecast international stock markets during the coronavirus pandemic: VIX vs EPU? Int Rev Financ Anal 72:101596

Wang W, **ao W, Bai C (2022b) Can renewable energy technology innovation alleviate energy poverty? Perspective from the marketization level. Technol Soc 68:101933

Xu Y, Wang J, Chen Z, Liang C (2021) Economic policy uncertainty and stock market returns: new evidence. North Am J Econ Finance 58:101525

Yamada H, Toda HY (1998) Inference in possibly integrated vector autoregressive models: some finite sample evidence. J Econom 86:55–95

Ye L (2022) The effect of climate news risk on uncertainties. Technol Forecast Soc Chang 178:121586

Yi X, Bai C, Lyu S, Dai L (2021) The impacts of the COVID-19 pandemic on China’s green bond market. Financ Res Lett 42:101948

Yuan T, Wu J, Qin N, Xu J (2022) Being nice to stakeholders: the effect of economic policy uncertainty on corporate social responsibility. Econ Model 108:105737

Zhang F, **a Y (2022) Carbon price prediction models based on online news information analytics. Finance Res Lett 46:102809.

Zhang H, Demirer R, Huang J et al (2021) Economic policy uncertainty and gold return dynamics: evidence from high-frequency data. Resour Policy 72:102078

Zhang J, Zhang Y, Sun Y (2022) Restart economy in a resilient way: the value of corporate social responsibility to firms in COVID-19. Finance Res Lett 47:102683

Funding

This paper was funded by National Natural Science Foundation of China (Nos.72131011) and the Natural Science Fund of Hunan Province (2022JJ40647).

Author information

Authors and Affiliations

Contributions

**ong Wang: conceptualization, supervision, funding acquisition.

**gyao Li: data collection, data analysis, software, writing — original draft preparation.

**aohang Ren: conceptualization, methodology, writing — editing and writing — reviewing.

Zudi Lu: writing — reviewing.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Competing interests

The authors declare no competing interests.

Additional information

Responsible Editor: Ilhan Ozturk

Publisher's note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

As mentioned earlier, three algorithms are used to generate Wald statistics. With respect to the FE methodology (Thoma, 1994), the Wald test statistic first computes the minimum window size, \({\tau }_{0}={T}_{r0}\), and successively expands the length of the observations until all samples are used (Fig. 1a). The RO procedure (Arora and Shi 2016; Swanson 1998) moves forward by a fixed window length at a time and calculates the Wald statistics for each subsample separately (Fig. 1b). The RE approach (Phillips et al. 2015) provides common endpoints for each subsample given a specific observation interval; then, the algorithm calculates the Wald statistics for each subsample with the window length of \({\tau }_{0}\) or greater when repeating the process (Fig. 1c). Notably, the three algorithms may generate different conclusions in practical causal tests due to their performance differences in limited samples. In a single switch procedure, the dating rule is giving by the crossing times, specifically, for each algorithm we have:

where cv denotes the critical value of \({W}_{f}\) and scv denotes the critical value of \({SW}_{f}\).

\({\widehat{f}}_{e}\) and \({\widehat{f}}_{f}\) denote the start and end points of the causal relationship, respectively. They are identified as the first observation that exceeds or falls below the causal test threshold. We search the start and end points of episode i in the sample ranges of \({[\widehat{f}}_{i-1f},1]\) and \({[\widehat{f}}_{ie},1]\) respectively.

Rights and permissions

About this article

Cite this article

Wang, X., Li, J., Ren, X. et al. Exploring the bidirectional causality between green markets and economic policy: evidence from the time-varying Granger test. Environ Sci Pollut Res 29, 88131–88146 (2022). https://doi.org/10.1007/s11356-022-21685-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-022-21685-x