Abstract

This paper analyzes firms’ episodes (spells) of high growth (HG) using a sample of Spanish manufacturing firms observed over two decades. The use of duration models allows us to investigate the following: (i) the probability of experiencing HG episodes, (ii) persistence in HG, and (iii) the determinants of the transitions in and out of the HG state and whether their impact varies over the business cycle. We find that about half of the firms experience at least one HG episode, but they seldom experience more than one. Moreover, high-growth status is rarely repeated due to high first-year selection. Yet, in subsequent years beyond the first one, the hazard rate from HG status falls substantially. These results suggest an “episodic” nature of HG and further allow us to identify two groups of firms characterized by the following: (i) (relatively) long HG spells and short no high-growth (NHG) spells and (ii) short HG spells and long NHG spells. In addition, some firm and market (demand) characteristics increase the probability of becoming an HG firm and enhancing HG persistence. Finally, during the downturn, the role of younger age and smaller size in explaining HG decreases.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Recently, increasing attention has been paid to the study of high-growth firms (HGFs).Footnote 1 These businesses have attracted the interest of policymakers (Vértesy et al. 2017), academic scholars (Henrekson and Johansson 2010), and the popular press (The Economist 2012) because they are responsible for the creation of most new jobs across countries and industries (Schreyer 2000; Nesta 2009; Audretsch 2012; Haltiwanger et al. 2017).

Despite their relevance, some features of HGFs remain blurred (Coad et al. 2014). First, although they tend to be small and young, it is hard to define a set of consistent determinants of HGFs that hold across industries and over time (Coad et al. 2014; World Bank 2019). In particular, the evidence of the behavior of HGFs over the different phases of the business cycle is scant. Second, and closely related to the previous issue, it is difficult to identify patterns of high-growth (HG; Hölzl 2014; Daunfeldt and Halvarsson 2015), in terms of both HG persistence (i.e., repetition of HG status in consecutive periods) and repetition of HG episodes (i.e., more than one transition into HG). The two previous issues have relevant policy implications. Indeed, one may wonder whether it is desirable to outline policies aimed at (ex ante) picking up potential HGFs rather than fostering a competitive environment in which all firms may experience episodes of HG (Coad et al. 2014; World Bank 2019).

This paper investigates HG episodes (HGEs) using a sample of Spanish manufacturing firms with more than 10 employees observed from 1991 to 2015. We proceed by classifying firms at any period into two exhaustive and mutually exclusive statuses—HG and non-HG (NHG, which includes both low and negative yearly growth episodes). We then construct episodes (spells)Footnote 2 of HG and NHG. Using multi-spell discrete-time duration models, we examine the transitions from NHG to HG and from HG to NHG. Duration analysis depicts some desirable features in the present context. First, it focuses on the occurrence (i.e., whether) and timing (i.e., when) of the two transitions. Hence, the timing of the transition matters, as well as the time between transitions, that is, time spent in a particular state (e.g., length of HG spells). Second, these methods allow for capturing the existence of duration dependence, that is, to check whether persistence in a state is related to previous experience in that state. Third, they allow considering time-varying explanatory variables to account for firm characteristics that may change over time. To inquire into the determinants of the two types of transition, we include a large vector of spell, firm, and market characteristics in the empirical model, and we explicitly interact them with the different phases of the business cycle. Fourth, it is uncommon to observe all HG and NHG episodes over a firm’s lifetime because the follow-up period ends or is dropped from a survey. However, the knowledge that the firm has been through HG and NHG until it leaves the sample contains valuable information. Duration models are well suited to take these issues into account. In addition, the application of duration models, which is rather new in the extant literature on HGFs (see Section 2.2), is enhanced by the use of a panel of firms observed over more than two decades. This time span allows us to observe many HGEs over the expansionary and contractionary phases of the recent business cycle in Spain.

We briefly sketch out our main results. First, HG episodes are relatively frequent, but HG is rarely repeated (little HG persistence). About 50% of the firms experience one episode of HG, but 75% of HG spells do not continue in that status in the following period. Indeed, on average, HG spells are much shorter than NHG spells are. Conversely, a few spells of HG last for multiple (2 or more) years, with the probability of continuing in HG rises with the length of the spell (negative duration dependence). Second, HG is “episodic.” Firms that experience one episode of HG do not show a higher probability of experiencing it again in subsequent years. In our view, these results are coherent with the idea that it is hard for multiple and long spells of HG to occur within the same firm, and that the “episodic” nature of HG should be better considered by both scholars and policymakers (World Bank 2019). Third, we identify two groups of firms in our sample—firms that tend to have (relatively) long HG spells and short NHG spells and firms with short HG spells and long NHG spells. Fourth, firm characteristics still matter. Indeed, smaller, younger, and more productive firms that introduce new production processes are more likely both to experience an HGE (i.e., to have a transition from NHG to HG) and to persist in its HG status (i.e., a longer HG spell). Fifth, market characteristics (demand) also play a relevant role. Firms that are active in expansionary markets and increase their market share endure a higher likelihood of starting an HG spell. Sixth, the phase of the business cycle shapes the impact of some explanatory variables: During a recession and weak recovery (2008 onwards), the role of firms’ age and size in explaining the probability of having an HGF is weakened. Finally, a complementary analysis of the length and repetition of HG spells confirms the relevant role (further than age and size) played by market dynamism and process innovation strategies, while suggesting the difficulties in explaining the (occasional) repetition of HG spells within firms.

This work contributes to the extant literature on HGF in several ways. First, while many studies have examined HGFs (e.g., Schreyer 2000; Delmar et al. 2003; Acs and Mueller 2008; Haltiwanger et al. 2017) and persistence in firm growth (e.g., Coad 2007b; Coad and Hölzl 2009; Capasso et al. 2014; Coad et al. 2018), the literature on HG persistence (Hölzl 2014; Daunfeldt and Halvarsson 2015; Bianchini and Pellegrino 2019) and its determinants (Bianchini et al. 2017) is scarce, with mixed results. We contribute to this literature by employing duration models to track the spells of specific growth states (either HG or NHG) and to identify the transitions between them, without imposing (as is common in the extant literature on HGFs) any particular “structure” (i.e., a certain number of lags in the autocorrelation coefficient of growth rates) to persistence in firm growth. We model the two types of transitions as functions of a vector of spell, firm, and market characteristics. This allows us to examine the probability of experiencing an HG episode, as well as persistence in HG. Second, the few studies inquiring into the persistence of HG have been able to track firm growth over a decade at most (e.g., Daunfeldt and Halvarsson 2015; Bianchini et al. 2017; Moschella et al. 2019) and focus on firm performance a few years after the occurrence of HG. We examine the entire length of HGEs, which allows us to unravel the potential effects of time in HG status on the probability of HG in subsequent years. Third, in contrast to previous studies on HG persistence, we further examine the impact of the different phases of the business cycle as possible enhancers or moderators of the determinants of HG and the persistence in it. We are able to exploit them, and we appreciate some significant differences over the cycle. Finally, we contribute to the literature on the growth of modern economies, which is linked to their ability to generate “dynamic businesses.” This dynamism plays a relevant role not just in terms of job creation (Coad et al. 2014; Criscuolo et al. 2014) but also in terms of resource reallocation across firms, which is key for productivity growth (Bravo-Biosca 2011; Haltiwanger et al. 2017) and innovation (Acemoglu et al. 2018). In this regard, our results show a positive story for the case of Spain: on average, higher levels of productivity and the introduction of new production processes significantly enhance the likelihood of both starting an HG spell and making it longer.

Taking stock of all these results, we put forward that scholars interested in HGFs should complement firm-level analyses with episode (spell)-level investigations. HGEs may be the proper target for economic policies aimed at fostering dynamic economies (Bravo-Biosca et al. 2016).

The paper proceeds as follows: Section 2 reviews the relevant literature on HGFs. Section 3 introduces the dataset and the construction of the main variable employed in the empirical analysis. Section 4 illustrates the econometric analysis. Finally, Section 5 concludes the paper.

2 Related literature

2.1 Nature and determinants of high-growth firms: regularities and open issues

The seminal work by Schreyer (2000) characterizes HGFs along several dimensions. The author definesFootnote 3 them as firms with more than 20 employees across seven Organisation for Economic Co-operation and Development (OECD) countries with the highest growth rates (top 10% of the growth-rate distribution) during the period from the mid-1980s to mid-1990s. Schreyer (2000) also shows that smaller size and younger age are significantly associated with HG. Moreover, HG firms are not particularly relevant in any specific industry or territory. Finally, a positive association emerges between HG and several innovation metrics (i.e., R&D expenditures and R&D personnel shares). These results have been confirmed by subsequent studies, across industries and countries and over time. For example, Henreksson and Johansson (2009) and Anyadike-Danes et al. (2009) confirm that HGFs are generally active in all industries. Across countries, the fastest-growing firms are commonly the youngest ones (see Haltiwanger et al. 2013; Barba Navaretti et al. 2014; Lawless 2014; Manaresi 2015). As for the relationship between firm size and the likelihood of being an HGF, Moreno and Coad (2015) put forward that there is mixed evidence for this. As for innovation, there is a consensus that while product innovation is beneficial for HG (when measured in terms of sales or employment), process innovation may have an adverse effect on employment due to its labor-saving nature, but this may be overcome by multiple “compensation effects” (Vivarelli 2014).

Nonetheless, several issues regarding the determinants of HG may well deserve more attention. First, factors that explain why an HGE starts may not explain persistence in HG. As pointed out by Brenner and Schimke (2015), the determinants of HG paths are not the same as the determinants of firm growth at a point in time. The study of growth paths requires pursuing a long-run perspective. In our empirical model (see Section 3.1), the probability of experiencing a transition from NHG to HG and the probability of persistence in HG (i.e., no transition from HG to NHG leading to longer HG spells) are both explicitly considered and may be associated with different sets of determinants.Footnote 4 Second, although the phase of the business cycle may moderate or enhance the effect of some determinants of HG (Henrekson and Johansson 2010), this has been overlooked in the extant literature on HG. Third, while several studies have inquired into the role of market- (demand)-related factors in firm growth (Foster et al. 2016; Pozzi and Schivardi 2016), their impact on HGFs is still largely unexplored given that the literature has mostly focused on supply-side factors.

To address the outlined issues, we employ a methodology that allows us to identify the transitions from NHG to HG and vice versa and analyze their (possible) different determinants. Among these elements, we inquire into the role of market-related factors. Moreover, we exploit about 25 years in the recent life of Spanish manufacturing to assess the role of the different phases of the business cycle for the transitions between states.

2.2 Persistence of high growth: a cautionary note and scant evidence

Before discussing the results of previous studies of HG and following a recent paper by Erhardt (2019), we should point out that, to some extent, the answer to the question of HG persistence depends on how growth is measured. In particular, it depends on the choices about the formula (absolute, relative, or composite), indicator (e.g., employees, sales), study period (e.g., 1 year, 3 years), and mode of growth (total, organic, or acquired).Footnote 5

Despite the cautionary note above, the empirical work so far provides—at best—extremely weak evidence on the ability of firms that experience HG in a specific year to repeat that HG status in the following year. Parker et al. (2010, p. 209) studied the behavior of a sample of about 100 “non-subsidiary, medium-sized and UK-owned” HGFs observed between the beginning of the 1990s and the beginning of the 2000s. These authors put forward that “gazelle-like growth appears to be fragile,” with a failure by those firms to repeat their tremendous 1-year performance in succeeding years. By employing a sample of Swedish companies in the period 1997–2010, Daunfeldt et al. (2013) have found that HGFs are not persistent in their performance. Moreover, by employing a database covering all active Swedish firms in the period 1997–2008, Daunfeldt and Halvarsson (2015) showed that fast-growing firms in a period were, on average, shrinking firms in the previous period, while showing a low probability of being HGFs again in the following years. Coad (2007b) has studied the autocorrelation of annual growth rates in a dataset of French firms in the period 1996–2002: small firms that experience “extreme” growth performance (either positive or negative) in a given year show a negative autocorrelation coefficient. Conversely, and at odds with previous studies in the field, in a sample of Spanish limited liability companies observed in the period 1996–2003, López-García and Puente (2012) show that past HG positively affects the probability of current HG.

Other studies have taken a different perspective, emphasizing the distinctive characteristics of persistent HGFs and firms that experience tremendous growth performance occasionally. Bianchini et al. (2017) put forward that persistent HGFs are not different (e.g., in terms of productivity and financial structure) from occasional HGFs in a sample of companies active in four European countries. Moschella et al. (2019) found that some relevant characteristics of the firm (e.g., productivity and innovation, profitability, and financial structure) do not allow predicting persistent HGFs using a sample of about 23,000 Chinese manufacturing firms observed over the period 1998–2007 (China’s Miracle). Using the same firm-level data on Spanish firms that we employ in this work, Guarascio and Tamagni (2019) adopt a growth-regression strategy to assess the role of past persistent innovation (7 out of 10 consecutive years of innovation in 1990–1999) in succeeding sales growth over a 12-year period (2000–2012). Their results suggest that persistent innovators do not grow more or more persistently than other firms do. A common characteristic of these works, which also constitutes a limitation, is that the usual time span covers about a decade, which may be a short period if one wants to track the HGEs over time and consider different phases of a business cycle.

Despite the relatively short periods characterizing previous research, some scholars have had access to long-in-time datasets. Coad and Hölzl (2009) employed an extensive database of Austrian firms in a few services sectors over a 30-year period and studied the serial autocorrelation of 1-year growth rates in employment across different size classes. Their results confirmed the negative autocorrelation of annual employment growth for fast-growing micro-firms. However, their dataset only allowed them to control for firm size and year effects in their regression, preventing them from uncovering eventual asymmetries in the determinants of transitions from low or negative growth to HG and vice versa. Using the same data source, Hölzl (2014) explored the performance of the firms in terms of survival and growth, both 3 and 9 years after their HG period. The results, which are robust to a propensity score matched sample technique, confirm low persistence in HG. The author imposed a certain structure to the dependency of future growth on past HG in the following ways: (i) estimating the effect after a specific number of years; and (ii) focusing on just one type of transition, that is, from HG status in one period to either HG (persistence) or an NHG status, while transitions from NHG to HG are not explicitly explored. By employing a sample of US-listed manufacturing firms in an extremely long period (1959–2015), Dosi et al. (2020) showed that, while there are cases of (even high) growth persistence across firms, they are rare and not fully accounted for by a random process.

A paper related to our work is the recent study by Bianchini and Pellegrino (2019), who adopted duration methods to assess the relationship between innovation persistence and persistence in employment growth using a sample of Spanish manufacturing firms covered by the Encuesta Sobre Estrategias Empresariales (ESEE), which is the same source of data we employ here (see Section 3.1). However, with respect to their work, we add four major contributions. First, while Bianchini and Pellegrino (2019) focus on persistence in positive employment growth and the role of innovation in it, we analyze two types of transitions between growth states (i.e., from NHG to HG and vice versa). Indeed, it is important to note the following: (i) the transition from NHG to HG deals with the probability of experiencing an HG episode; (ii) the transition from HG to NHG is relevant per se, as a proper way to study persistence in HG; and (iii) the two transitions may be explained by different sets of determinants. Second, and highly connected to the first point, we assess the role of a broader set of potential determinants of the two types of transition by including characteristics of the spell, the firm, and the market in which the firm is active. Third, we inquire into the role of the business cycle in the determinants of transitions by looking at the recent years of expansion and contraction of the Spanish economy to assess whether and how the impact of these determinants has been shaped by the Great Recession. Fourth, in the last part of the empirical analysis, we further explore the determinants of long HGEs.

3 Data and descriptive analysis

3.1 Growth states, spells, and transitions across states

This paper uses firm-level data extracted from the ESEE, a (non-mandatory) survey sponsored by the Spanish Ministry of Industry and carried out by the Fundación SEPI. The sample is representative, at the industry-level, of the population of Spanish manufacturing firms with more than 10 employees.Footnote 6 The dataset presents at least four desirable features for the purpose of this study. First, the time span covered by the ESEE is rather long. Indeed, we start with an unbalanced panel of about 2000 manufacturing firms per year over the period 1991–2015. This allows us to monitor many firms experiencing both HG and NHG episodes. In addition, the period embraces different phases of the business cycle, that is, the (pre-recession) expansionary phase and the years of the Great Recession, which hit the Spanish economy hard. Second, and highly connected with the first point, most firms show multiple spells of HG and NHG. We exploit this within-firm variability in the empirical model to disentangle unobserved heterogeneity from genuine duration dependence (Heckman 1981). Third, the ESEE is subject to annual consistency tests that mitigate the risk of reporting mistakes, particularly in employment, which may affect the ability to classify firms into HG and NHG status. Fourth, the database has a multi-scope nature, which allows us to consider a rich set of factors as determinants of both HG and NHG episodes. Nevertheless, this data source also depicts two main limitations. On the one hand, the size threshold of more than 10 employees excludes micro-firms, and new-born firms are under-represented, which probably have a high likelihood of experiencing HGEs. On the other, the ESEE is restricted to manufacturing firms. Therefore, our results are conditional on manufacturing firms with 10 or more employees.

To spot the episodes of HG and NHG, track their length, and identify the transitions across the two states over time, we proceed as follows: first, we need to choose a proxy for firm size. Then, we calculate the firms’ annual growth rate. Finally, we establish the criteria to define the states of HG and NHG and place the firms accordingly. As for firm size, we primarily use the information provided by the ESEE on firms’ employment. Thus, SIZEit is equal to the sum of full-time permanent workers of firm i and 50% of part-time permanent workers (both as of December 31st) and the average number of non-permanent workers throughout the year t, that is, considering the quarterly number of non-permanent employees.Footnote 7 As a robustness check, we further re-estimate our baseline specification using (real) sales as a proxy for firm size.Footnote 8 Growth is defined as the 1-year log difference in firm i’s size, as follows:

In line with the previous literature, we focus on episodes of organic growth. Indeed, the preponderance of actual growth episodes is due to an internal expansion of the firm in terms of its capacity and output. Moreover, the decision of undertaking mergers and acquisitions (M&As) is intrinsically different from a growth strategy based on the own resources (Rumelt 1987; Lockett et al. 2011). In this line, Capasso et al. (2014) argued that acquisitions and spin-offs are one-off extreme growth events based on external sources that are unlikely to be repeated over time, whereas the events that are based solely on internal growth may be more likely to be persistent over time. Hence, the former and latter events deserve a different analysis.Footnote 9

We employ a relative definition of HG. A firm i is allocated to the HG state in year t (HGit = 1) if grit lies in the top decile of the sample distribution of employment growth rates.Footnote 10 We employ a 3-year moving average (from t − 1 to t + 1) to build up the employment growth-rate distribution of the sample. By doing so, we try to smooth out the sample growth-rate distribution (e.g., reducing the distortionary impact of recessionary years with extraordinary employment reduction).Footnote 11 Figure 1 displays the 90th percentile of the annual growth-rate distribution and that obtained using the 3-year window. We build the two growth states as mutually exclusive and complementary; thus, a firm that is not classified in the HG state in year t is necessarily classified in the NHG state in the same year (NHGit = 1).Footnote 12

Ninetieth percentile of employment growth rate distribution. Notes: this figure plots the 90th percentile of the employment growth rate distribution, using 1-year (i.e., year t) and 3-year moving average (from t-1 to t + 1) growth rates

The duration of an HG (NHG) spell is equal to the number of consecutive years in which a firm remains in that state from its beginning. An HG (NHG) spell ends in year t if the firm is in that state in year t and not in year t + 1. Hence, the information in 2015 is only used to determine whether ongoing spells in 2015 end in that year or are right-censored (i.e., they continue beyond 2015). The HG (NHG) spells that end without a transition to the other state are included in the analysis and treated as right-censored. This category comprises ongoing episodes at the end of the observation window and dropouts from the ESEE due to failures, M&As, no further collaboration with the survey, or other restructuring processes. The empirical analysis is restricted to “fresh” spells. Left-censored spells (i.e., spells that started before 1993) are excluded from the sample as we do not know exactly when they started. The whole procedure detailed above reduces the usable time span to the period of 1994–2014, which covers 2832 HG spells and 4934 NHG spells corresponding to 3562 firms.Footnote 13

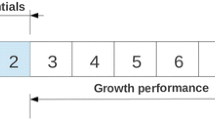

For illustrative purposes, Fig. 2 (panel a) provides an example of HG and NHG episodes that occur in a hypothetical firm i. If 1999 (2005) is the first (last) year in which the information on employment is available for this firm, 2000 (2005) is the first (last) year in which the growth rate can be computed. Firm i has two spells of NHG and one spell of HG. The first spell of NHG starts in 2000 and ends in 2002, while in 2003, an HG spell starts that lasts for just 1 year. In 2004, a second spell of NHG starts, which is ongoing in 2005. Hence, the second NHG spell is right-censored in 2005.

Spells of HG and NHG within a hypothetical firm i; the characteristics of the spells

An analysis of the spells (yearly series) of HG and NHG is reported in Table 1, where the numbers and shares of NHG and HG spells are shown, in cols. 1 and 2 in terms of their length; in addition, the NHG and HG spells of maximum length within each firm are shown in cols. 3 and 4. While most firms in the sample (3446 / 3562 = 96%) show a positive number of spells of NHG, a lower share (though still high) experience HG spells (1897/3562 = 53%). Moreover, the restricted average length of an NHG spell is about 4.37 (= 21,585/4934) years, but this drops to 1.18 (= 3362/2832) years for the spells of HG.Footnote 14 While it is not so rare to experience an episode (spell) of HG over more than two decades, they are typically short.

Another way of looking at the same phenomenon is to estimate the hazard rate of a certain spell, which is equivalent to the probability of transition to the other growth state after having been in the departure state for 1 year. While the first-year hazard rate is equal to 0.10 for the NHG spells, for the HG spells, it is much higher, at 0.76. When a firm starts an episode (spell) of HG, this will end in the subsequent year in almost 8 out of 10 cases. Furthermore, while the maximum length for an HG spell is equal to 6 years, that of an NHG spell is equal to 21 years (i.e., the maximum length of the observed period). Another interesting piece of evidence is that, for both NHG and HG, the total number of spells is higher than the total number of firms, especially for short spells, suggesting that a large share of firms experience more than one spell.

3.2 Determinants of transitions across growth states

The explanatory variables associated the two types of transitions have been grouped into six categories for ease of interpretation. These are as follows: (i) variables capturing the characteristics of the spell, (ii) variables that proxy the structural characteristics of the firm, (iii) productivity and innovation variables, (iv) proxies for alternative growth strategies, (v) variables related to the firm financial structure, and (vi) variables capturing the market (demand) that a firm faces. In addition, year and industry effects (at the two-digit level, NACE-rev.2) are also included. Table 2 describes how all variables have been built and provides some descriptive statistics.

Two sets of variables account for the characteristics of the (HG or NHG) spells. First, three binary variables control for the age of the spells (SP_LENGTHg), where g = {1, 2, 3} if the age of the current spell is equal to 1 year, 2 years, or 3 years or more.Footnote 15 Second, another set of three binary variables (SP_REPg) is employed, where g = {1, 2, 3} gathers the spells representing the first-, second-, third-, or higher order repeated spells of the same type for a firm. Figure 2 (panel b) exemplifies how these two variables take their values for a hypothetical firm i. In the empirical model, the coefficient associated with the variable SP_LENGTHg captures the relationship between the likelihood of ending the spell (i.e., the transition to the other growth state) and the length of the current spell. The coefficient of SP_REPg captures the relationship between the likelihood of ending the spell and the fact that the firm has already experienced a spell of the same type in the past. These two variables are central to pointing out the “episodic” and/or dependent-on-past-firm-experience nature of the HG phenomenon.

As for firm characteristics, the literature has consistently emphasized the effects of firm size and age as crucial variables in explaining firm growth (e.g., Hall 1987; Lotti et al. 2009; Haltiwanger et al. 2013; Barba Navaretti et al. 2014). For these reasons, firms have been classified into five size and five age groups (SIZEg, AGEg, where g = {1, 2, 3, 4, 5}) at the onset of each spell they experience; thus, a within-firm variability of these variables is ensured from one spell to another. Productivity has been put forward as one of the key drivers of firm performance (Esteve et al. 2018), both by dynamic competitive equilibrium models (Jovanovic 1982; Ericson and Pakes 1995) and evolutionary theory (Nelson and Winter 1982; Dosi et al. 1995). In our empirical setting, PRODUCTIVITYg, where g = {L, M, H}, is proxied by the ratio of sales to employees, and firms are grouped into “low-,” “medium-,” and “high-productivity” firms by comparing each firm’s productivity in year t with the 25th and 75th percentiles of the sample productivity distribution. Innovation shapes fast size dynamics (Coad and Rao 2008), and it is proxied by two binary variables that measure whether the firm introduced any product (PROD_INN) or process innovation (PROC_INN) in year t.

Firms may grow as a consequence of an international expansion of their activities (Grazzi and Moschella 2018), while being part of an industrial group or corporation may affect their growth pattern. Accordingly, two binary variables (EXPORTER and GROUP) are included, taking value 1 in year t if the firm, respectively, exports or belongs to an industrial group, and 0 otherwise. It is also well-known that the lack of availability of external financial resources may constrain firm growth (Carpenter and Petersen 2002; Hutchinson and Xavier 2006; Clarke et al. 2012). We employ a widely used variable to measure the financial structure of the firm in terms of its balance of external and internal resources, that is, the leverage ratio (LEVERAGEg, where g = {L, M, H}), calculated as the ratio of debts over debts plus shareholders’ equity. Similar to productivity, we include a vector of dummies that gather “low-”, “medium-,” and “high-leverage” firms by comparing each firm’s leverage ratio with the 25th and 75th percentiles of the sample leverage distribution.

Two variables have been included to account for some relevant conditions of the principal market in which the firm is active and for the role of demand. First, a vector of three dummies is included, MARKETDYNg, where g = {R, S, E}, which have been built starting from a categorical variable capturing if the market is going through a “recessionary,” “stable,” or “expansive” phase. Second, based on a categorical variable that measures the firm’s market share evolution, three dummies have been included, MARKETSHg, where g = {D, S, E}, which groups those firms whose market share is “decreasing,” “stable,” or “expanding.” It is relevant to underline that, both for MARKETDYNg and MARKETSHg, the firm self-defines the boundaries of its main market, which do not overlap with the 2-digit level industry definition as they are defined at a much finer level of disaggregation. This is key to better capturing some main characteristics of the demand faced by the firm. As for firm and market characteristics, while SIZEg and AGEg are measured at the onset of the current spell, all other variables have been introduced in the empirical model as 1-year lagged to mitigate simultaneity problems.Footnote 16

Although the set of explanatory variables is rather rich, a potential shortcoming of our analysis is the reduced number of variables with high within-firm variation over time, which may affect our ability to predict HGEs, as pointed out by Coad and Srhoj (2019).Footnote 17 In the robustness section, we re-estimate the main specification using continuous and time-varying explanatory variables. The variables that depict more intra-firm variability over time in our dataset are firm size, productivity, market dynamics, and market share dynamics.

4 Econometric analysis

4.1 The empirical model

This paper analyzes the dependence of the exit from NHG and HG on the length of time in an NHG or HG spell and on other explanatory variables by the estimation of duration models. At any time t, a firm i may be in one of the two exhaustive and mutually exclusive states indexed by s (s = HG, NHG), and Stji denotes the state occupied by firm i during interval t of episode j (i.e., firms may show more than one HG and/or NHG spell). We estimate the probability that a firm leaves NHG or HG during period t, given that it has been in NHG or HG for t − 1 periods. Since we have yearly information, we treat duration as a discrete variable and estimate discrete-time duration models. Let us define ytji as a binary variable indicating whether any transition (i.e., an exit from the spell of NHG or HG) has occurred during interval t. The discrete-time hazard function for state s, that is, the probability of a transition from state s during interval t, given that no transition has occurred before the start of t, is defined as follows:

We estimate the following multilevel two-state logit model:

where Dstji is a vector of dummy variables that capture the age effects of a specific spell in state s by firm i. In particular, in the reported tables, we have estimated models in which Dstji includes three dummy variables to control for age-of-spell effects (SP_LENGTHg). Xstji is a vector of explanatory variables that affects the transition from state s, which includes characteristics of the spell (SP_REPg), as well as firm and market characteristics. We cluster the standard errors at the firm level.

Finally, usi allows for unobserved heterogeneity between firms in their probability of exiting from state s. There may exist unobserved firm-specific factors (constant across both episodes and states) that affect the hazard of an event for all episodes and states (e.g., managerial capabilities of firms not captured by the included explanatory variables). We assume that usi = (uHGi, uNHGi) follow a bivariate normal distribution, which allows for correlation between time-invariant factors that influence each transition.

In Section 4.2 (our baseline results), we assume that cov(uHGi, uNHGi) = 0; that is, we treat the two transitions as independent and model them with two separate equations (one for transitions from NHG to HG and another one for transitions from HG to NHG/persistence in HG). That is, we start by examining duration in one state and/or the probability of transition to a complementary state. In this way, we model duration to an event from the moment at which a firm becomes at risk (onset of episode). We estimate firm-level frailty models because we cannot assume that the durations of repeated episodes by the same firm are independent. There may be unobserved firm-specific factors that affect the hazard of an event for all episodes of the firm. Hence, we estimate multilevel random effects discrete-time logit models.

In Section 4.3.1, we allow for cov(uHGj, uNHGj) ≠ 0, and we estimate the equations for the two transitions jointly. Usually, firms move in and out of different states over time. We model a firm’s entry to HG jointly with exit from HG using a two-state duration model. The state-specific unobserved heterogeneity components of these transition processes are allowed to be correlated across the two states. There may be time-invariant individual-specific unobservable factors that affect each type of transition. For instance, firms with a strong likelihood of experiencing an HG episode may have a low hazard of moving from HG to NHG and a high hazard of moving from NHG to HG, that is, a tendency toward long HG episodes and short periods in the NHG state. This would lead to a negative random effect correlation. Hence, we would have the two following groups of firms: (i) firms with short NHG spells and long HG spells and (ii) firms with long NHG spells and short HG spells. We jointly estimate two equations as follows: (i) transitions NHG to HG and (ii) transitions HG to NHG. Both equations include a firm-level random effect. We estimate it as a bivariate model.

4.2 Main results

We start with the estimation of the hazard of the NHG and HG spells separately. The two hazard rates are functions of the duration in the current state, order (repetition) of the current spell, year and industry effects, and firm unobserved heterogeneity. The results of the random effects logit models for the two types of transitions are shown in Table 3. The dependent variable in col. 1 (col. 2) is the hazard rate for NHG (HG) spells. The first column in each group reports the estimates for the entire sample, and the other columns display the estimates when we split the sample by firm size and technological intensity of the sectors and period for each of the two transitions. We report exponentiated coefficients in all specifications throughout the paper, and these are interpreted as odds ratios with respect to the baseline (omitted) category.

We start by discussing the results in the columns labeled “Total.” As for the characteristics of the spells, the effect of the length of the current spell on its hazard rate, as captured by the coefficients of the SP_LENGTHg variable (where g is equal to the length of the spell in either the NHG state in col. 1 or the HG state in col. 2), shows an asymmetric effect. While it does not play a role in explaining the likelihood of transition from NHG to HG (col. 1), it shows a negative effect on the hazard from HG to NHG; in other words, it exhibits a higher persistence (of the firm) in the HG state. This effect is mildly significant for the second year of the HG spell (col. 2), but it is higher in magnitude and significance for the group of HG spells that last 3 or more years. HG spells that reach their third year face a 61% lower risk ((1–0.389) * 100) of ending the ongoing spell than a comparable—in terms of industry, year, and order/repetition—HG spell in its first year of existence. These two results are relevant. First, the preliminary evidence suggested that the HG state is not predestined for all firms in the NHG state. Second, the results in Table 3 suggest the existence of true state dependence. That is, after a strong initial selection effect, HG firms that continue beyond their first year in the HG state significantly increase their probability of HG persistence. We find no evidence of a similar effect for NHG episodes.

The effect of the repetition(s) of the current spell on its hazard rate is captured by the coefficients of SP_REPg (where g is equal to the order of the spell in either NHG in col. 1 or HG in col. 2). In col. 1, these coefficients show that, for the average firm with more than one NHG spell, the third- or higher order NHG spell shows a significantly (about (1–0.60) * 100 = 40%) lower probability of ending for the first NHG spell.Footnote 18 This result, which is consistent with the evidence provided by previous studies on the negative autocorrelation of growth rates (Coad 2007b), suggests that, for the average firm that has already experienced two transitions from NHG to HG, it is more difficult to experience a third one in a sort of “erratic” pattern (Coad 2007a; Guarascio and Tamagni 2019). In addition, the results in col. 2 show that the repetition of HG episodes does not increase the expected duration in that state. In our view, these results on the characteristics of the spells are coherent with the difficulty of identifying series of episodes (spells) of HG within the firm even over a long period, while there are (few) episodes that show a relatively long duration and a self-reinforcing effect as their length increases.

As for the year dummies,Footnote 19 no significant differences arise across years in terms of higher/lower probability of ending an NHG spell/starting an HG spell, except for 2008 and 2011, in which the probability for ending an NHG spell is significantly lower (about 64% lower [1–0.36] in 2008 and about 55% lower in 2011) than in the baseline category (1994). Interestingly enough, year dummies are even less effective in explaining persistence in the HG state, as shown in col. 2; indeed, few of them (1998, 2002) are only mildly significant (at 10%). As for the industry dummies, the results generally confirm the previous evidence (e.g., Schreyer 2000; Bianchini et al. 2017; World Bank 2019) on a rather minor role played by industrial specificities in explaining HG episodes (col. 1), and mostly, persistence in HG (col. 2).Footnote 20

The rest of the columns generally support our main findings. First, the negative duration dependence of HG spells holds up for both small and medium-sized enterprises (SMEs) and large firms and is mostly driven by firms active in low- and medium-tech manufacturing sectors.Footnote 21 The same effect is statistically significant before, but not after, 2008. Second, the duration-enhancing effect of repetition of NHG spells is mostly explained by SMEs and firms active in low- and medium-tech manufacturing sectors.

Next, we move to a more refined specification, which contains a larger vector of regressors.Footnote 22 The results are shown in Table 4, and factors that affect the two types of transitions are grouped into six categories, as explained in Section 3.2.

The length and order of the current spell maintain the same relationships with the likelihood of spell ending (i.e., transition to the other growth state) that we found in the more parsimonious specification of Table 3. The longer length of the current spell continues to be significant in explaining a higher persistence in the HG state but only for those spells that last for 3 or more years (captured by the coefficient of SP_LENGTH3, in col. 2) in relation to spells that are 1 year old. Conversely, HGE repetition does not ensure higher persistence in HG compared to firms that are in their first HGE (non-significant hazard ratios of SP_REP2 and SP_REP3 in col. 2). In addition, if a firm has already experienced two previous episodes (spells) of NHG, the current NHG spell shows a lower probability of ending (captured by the coefficient of SP_REP3 in col. 1), ceteris paribus. Again, these results suggest both the “episodic” nature of HG and the “erratic” patterns followed by those firms that experience multiple episodes of HG.

As for firm age and firm size, the results in Table 4 largely confirm the findings of the previous literature on HGFs. In particular, by looking at col. 1, which refers to transitions from NHG to HG, older firms show a significantly lower probability of experiencing an HGE than their younger counterparts do, and the firms with the largest “disadvantage” are precisely the oldest ones. Indeed, firms established more than 30 years ago, as captured by the hazard ratio of AGE5, show a likelihood of passing from NHG to HG, which is about 53% (1–0.469) lower than start-up firms (AGE1, the baseline, omitted category, defined as firms established since at maximum 5 years). By looking at col. 2, we can also appreciate that age plays a negative role in the permanence in the HG state (or, in other words, a positive role in the transitions from HG to NHG). For example, we may quantify the likelihood of persistence in the HG state as about 94% lower for firms established more than 30 years ago (AGE5) compared with start-up firms (AGE1). The role of firm size largely mimics that played by firm age, with firms with a larger size than the baseline (omitted category: SIZE1, from 10 to 20 employees) consistently showing lower probability of experiencing an HGE. However, as for the persistence in HG, larger size is not necessarily a disadvantage: indeed, firms that employ more than 500 employees do not show a lower probability of persistence in the HG state (shown by the non-significant coefficient of SIZE5) with respect to the smallest ones. This result is in line with previous findings; for example, Schreyer (2000) showed that large firms gain in relevance when one considers HGEs instead of considering positive but moderate growth episodes (where large firms are less frequent).

The probability of shifting to the HG state is more than 80% higher (col. 1) for the most productive firms (PRODUCTIVITYH) with respect to the baseline group (the least productive firms, PRODUCTIVITYL). The effect rises as one moves from the category of the least productive to the category of the most productive. At the same time, and especially for the most productive firms, these also show a higher persistence in the HG state (by about 42%, as shown by the hazard ratio associated with PRODUCTIVITYH in col. 2). This is interesting because it suggests that, on average and in the period from 1994 to 2014, the most productive Spanish manufacturing firms have been the ones that more frequently have experienced episodes of fast employment growth. Although Arnold et al. (2011) have provided some negative evidence on the relationship between firm growth and productivity for the case of Spain in the period 1998–2004, our results provide a positive message about the allocation of labor input, at least for the fastest growing firms. The introduction of a process innovation raises the probability of shifting from NHG to HG, as shown by the hazard ratio of PROC_INN in col. 1, which corresponds to a 25% higher probability of experiencing an HGE for those firms that have introduced a new (and likely more efficient) production process compared with their counterparts. This result is consistent with Harrison et al. (2014), who show a growth in demand for old products due to process innovations that lead to higher efficiency and may well compensate for the labor-saving effect of this type of innovation. However, process innovation does not depict a significant impact on HG persistence (col. 2). Unexpectedly, we do not find a significant association (non-significant hazard ratio of PROD_INN) either between product innovation and the likelihood of experiencing an HGE (col. 1) or with persistence in the HG state (col. 2). This result may be explained by the long payback times that characterize the returns associated with the introduction of a new product in the market (Grabowski et al. 2002). Moreover, the relationship between product innovation and firm growth is complex and may change according to firm characteristics, the nature of market selection and the geographical environment (Audretsch et al. 2014).

As for the alternative ways through which a firm may grow, belonging to an industrial group of firms both reduces the probability to start an HG spell (by about 20% with respect to independent firms, in col. 1) and increases the probability of persistence in the HG state (by about 25% with respect to independent firms, in col. 2). Thus, belonging to a group may “smooth” firm size dynamics in terms of labor input via a reallocation of resources within the group. We find that being an exporter significantly reduces the likelihood of experiencing an HGE (by about 15% with respect to a non-exporter) and does not ensure a higher persistence in the HG state. However, this may be due to the fact that we measure firm size with the number of employees and that exporting abroad does not necessarily entail a significant increase in the staff at home.Footnote 23 The firm’s financial structure does not play a significant role in explaining the higher/lower likelihood of experiencing a transition from NHG to HG, nor of persistence in the HG state.

We next move to analyzing the characteristics of the market (demand) that a firm faces. A “stable” or “expansionary” phase of the market (MARKETDYNS and MARKETDYNE) ensures a higher likelihood of shifting to HG in relation to the firms active in a “recessionary” market (about 38% higher for firms in a market in a stable phase and 74% higher for firms in a market in an expansionary phase, as shown in col. 1). At the same time, the expansionary phase of the market significantly increases the persistence chances in HG state: ceteris paribus, firms active in a market experiencing an expansionary phase are characterized by about a 35% higher probability of continuing in the HG state in year t + 1, conditional on being in that state in t. The information about the evolution of the firm’s market share—that once controlled for productivity may be a proxy for the firm’s specific market power—provides additional insights. Indeed, an “expanding” market share is associated with a higher probability for the firm to start an HG episode, ceteris paribus, in relation to the case in which the market share is “decreasing.” As these results show, both the evolution of the market (demand) and the firm market power, which have seldom been considered by previous studies, are important and complement supply-side factors in explaining the probability of transition to the HG state, and—to a lesser extent—the permanence in it as time passes.

Overall, these results point out three findings. First, the coefficient of the variables capturing the characteristics of the spells (SP_LENGTHg and SP_REPg) shows that HG has an “episodic” and “erratic” nature. On the one hand, while few spells last more than 3 years, those making it beyond this point substantially increase their expected duration. On the other, having experienced past episodes of HG does not ensure a higher probability of repeating this experience. Second, after accounting for these spell characteristics, firm and market characteristics still matter. Indeed, NHG spells in younger, smaller, and more productive firms show higher hazard rates than their counterparts do, which corresponds to a higher probability for these firms experiencing an HGE, starting from the NHG state. Likewise, the expansionary dynamics of both market demand and a firm’s market share are also associated with a higher probability of experiencing a transition from NHG to HG. Third, once we focus on the HG spells and their hazard rate, most of the characteristics that explain a higher probability of starting an HG spell (younger age, smaller, size, higher productivity, being active in a market in its “expansionary” phase) are also associated with a higher likelihood of persisting in the HG state. However, given that it is rare for a firm to experience HGEs that are longer than 1 year (only about 5% of firms show HGEs that last for 3 years or longer), it is harder to “characterize” persistence in HG than the transition from NHG to HG, even with our large set of determinants (Dosi et al. 2020). In Section 4.3.3, we deepen the analysis of the determinants of both length (i.e., persistence) and repetition of HG spells within a firm as time passes.

4.3 Further results

4.3.1 Joint estimation of HG and NHG transitions: a two-level two-state logit model

So far, we have investigated the duration in each state (i.e. HG, NHG) from the period at which a firm becomes “at risk.” The estimation of firm-level frailty models allows us to account for unobserved firm-specific factors (constant across spells) that affect the hazard of the occurrence of an event for all spells of the same firm. However, firms will move in and out of different states over time. In this section, we analyze firm entry to HG jointly with exit from HG using a two-state model that allows for correlation between the time-invariant influences of each type of transition, as previously outlined in Section 4.1. For instance, a firm may simultaneously have a high likelihood of HG ins but a low risk of HG outs, leading to negative correlation. Table 5 depicts the results of the estimation of a two-level, two-state random-intercept and random-coefficient logit model, allowing for correlated (firm-level) random effects across the two equations. We assume that the random effects follow a bivariate normal distribution.

The results suggest the existence of a negative and statistically significant residual correlation between the two transitions analyzed. Thus, firms with a high likelihood of starting an HG spell tend to have a low chance of leaving the HG state. Conversely, firms with a low chance of starting an HG episode tend to have a high probability of leaving the HG state. Hence, the negative correlation arises from two subgroups of firms that have the following characteristics: (i) long HG spells and short NHG spells and (ii) short HG spells and long NHG spells. Interestingly, the results in Table 5 strongly confirm the main results in Table 4, except for a slight impact on the covariates related to the firm’s growth history. Specifically, the negative impact of previous experience (SP_REP3) on the hazard of ending an NHG spell is weakened (0.681 in col. 1, Table 5 vs. 0.621 in col. 1, Table 4), while the positive impact of the variable SP_REP3 on the hazard of leaving the HG state is strengthened (1.298 in col. 2 of Table 5 vs. 1.161 in col. 2 of Table 4), in line with the negative correlation between the residuals.Footnote 24

The impact of the other explanatory variables is highly similar to those obtained in the one-state models of Table 4. The younger and smaller firms both show a higher probability of experiencing an HGE in terms of their older and larger (but not the largest) counterparts and persist more in that state. The most productive firms endure a higher probability of experiencing an HGE compared with their less productive counterparts and persist more in that state. Process innovation does boost the probability for a firm to experience an HGE, but it does not help the firm remain in that state. As for the market characteristics, being active in a market that is going through an “expansionary” phase is relevant for both a higher likelihood of experiencing an HGE and a higher persistence in the HG state, while being active in a stable market does not ensure the firm stays in the HG state. At the same time, a positive evolution of the market share is associated with a higher probability of experiencing an HGE, while it does not explain the persistence in it as time passes.

4.3.2 The Great Recession

The dataset used in this paper provides information on Spanish manufacturing over a long time span that embraces different phases of the business cycle. This allows us to further investigate whether the impact of some factors that explain the transition from NHG to HG and/or the persistence in the HG state are shaped by the phase of the business cycle. To this end, we include a dummy variable, D_DOWNTURN, in the empirical model; this is equal to 1 for the period of 2008–2014 and 0 for the period of 1994–2007. For brevity, Table 6 only shows the variables where the interactions with the dummy capturing the downturn are significant, as well as the respective calculations for the difference in the effect of the variable (on the likelihood of transitions) between the two subperiods.

Overall, few variables show an effect on the hazard rates that significantly vary over the two main phases of the business cycle, but some interesting results emerge. First, during the recession and weak recovery period (i.e., from 2008 onwards), the youngest and smallest firms are no longer the ones with the higher likelihood of experiencing an HGE, as is the case during the upturn, while no changes are observable in relation to these two variables for the persistence in HG. This result is much in line with the evidence provided by Fort et al. (2013) and Criscuolo et al. (2014) on the sensitiveness of growth performance by young and small firms during the Great Recession. Second, the introduction of a new process innovation shows a significant association with a higher probability of persistence in HG during the upturn (before 2008), but this effect reverses from 2008 onwards. This finding is consistent with the interpretation that the introduction of labor-saving technologies during the Great Recession may have led to reduced persistence in HG (i.e., higher risk of ending an HG spell). Third, the higher persistence in HG associated with belonging to an industrial group during the expansionary phase is reduced from 2008 onwards. The outbreak of the economic crisis may have altered the common practices of transferring resources between affiliates and main partners within the same group. Although changes in those practices are difficult to predict, our results are consistent with the view that firms belonging to a group may have found less attractive investment opportunities during the crisis, so resources may well have been redistributed to other affiliates with projects promising higher yields (Belenzon et al. 2013).

4.3.3 Further exploration of HG spells

We complement our previous results with a specific analysis about what factors are associated with a longer/shorter length of the HG spells and their (rare) repetitions within firms and over time. Table 7 (col. 1) shows the breakdown of the HG spells in terms of three categories based on their length (i.e., 1, 2, or 3 years or more). Overall, 2517 HG spells occurred across 1582 firms during the period of 1993–2014. Right-censored spells are dropped to avoid biases due to incomplete information.Footnote 25

Table 7 (col. 2) shows the breakdown of firms in terms of the number of HG spell repetitions. In particular, three groups are defined, where the third category refers to firms with three or more repetitions of HG spells. As expected, the most frequent situation corresponds to firms that experience only one HG episode, although 35.5% of firms have more than one HG spell.

In accordance with the ordinal nature of the three categories, an ordered logit specification is applied. In this context, Y* is the latent variable that crosses progressively higher thresholds, whereYi ∗ = βXi + εi. For example, in the case of HG spell length, three categories are defined by two thresholds (α1, α2), which are as follows: if Yi* ≤ α1, then the length is 1 year; if α1 < Yi* < α2, then the length is 2 years; and finally, if Yi* ≥ α2, then the period is longer than 2 years. The j-category probability (j = 1,2,3) is defined as \( \Pr \left({Y}_i=j\right)=F\left({\alpha}_{j-1}<{Y}_i^{\ast}\le {\alpha}_j\right)=F\left({\alpha}_j-\beta {X}_i\right)-F\left({\alpha}_{j-1}-\beta {X}_i\right) \), where F is the logistically distributed function. Two threshold parameters are estimated in our setting (intercept is excluded); if they are significantly different from each other, it suggests that they should not be collapsed into fewer categories (two, in this case). As is well-known, ordered logistic regression assumes that the coefficients that describe the relationship between category 1 versus categories 2 and 3 of the response variable are the same as between categories 1 and 2 versus category 3. This is called the proportional odds assumption or the parallel regression assumption. If the assumption is met, then all the coefficients (except the constant) should be equal across different logistic regressions, other than when differences are caused by sampling variability (Williams 2016). If that assumption is not fulfilled, a generalized ordered logistic regression is required to relax that assumption. However, some explanatory variables can meet the proportional odds assumption, while others do not. The partial proportional odds model is an intermediate model between two extremes—the ordered logit and the generalized ordered logit—in which some variables are constrained to be the same across values of j-categories, while others are not. A set of tests is carried out in an iterative process, for each coefficient, to identify whether a less constrained approach is required.Footnote 26

As is common in discrete choice models, estimated parameters indicate the sign but not the magnitude of impacts. Therefore, Table 8 shows average marginal effects for some selected significant variables. Marginal effects are evaluated for each state of the dependent variable, ceteris paribus. As can be appreciated, the largest and oldest firms have larger probabilities of having an HG spell of 1-year in length, and correspondingly, smaller probabilities of longer HG spells. In addition, being active in an expansive market or carrying out process innovation all increase the likelihood of experiencing longer HG spells. For example, while extremely large firms are 6.5 percentage points less likely than smaller firms are to experience a 2-year spell duration, firms in expansive markets or carrying out process innovations are more likely to experience a spell with such a duration, ceteris paribus.

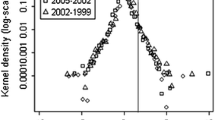

Figure 3 shows the average adjusted predictions for the three categories of the ordinal dependent variable and each state of the explanatory binary variables. As we already know from Table 7, the first category (HG spells that last for 1 year) gathers a large mass of probability, while the third category (HG spells that last for 3 years or more) is relatively small. The corresponding changes (i.e., marginal effects) are not large in absolute terms, but they are so in relative terms. For example, carrying out process innovations increases the predicted probability of having an HG spell of 3 or more by 1.0 percentage points (from 3.0 to 4.1%), which represents a relevant increase in likelihood (37%) compared with firms that do not carry out process innovation.

Spell length: average adjusted predictions for the three states (selected variables). Note: horizontal axis shows the three states in the generalized ordered logit: 1 year (1), 2 years (2), and 3 or more years (3)

The last column in Table A1 in the Online Appendix shows the results of the ordered logit estimation for repetition. The results point out the difficulty in predicting the pattern of HG repetition within firms: Hardly any variable is significant in explaining the number of repetitions of HG spells.

4.4 Robustness checks

This section performs several robustness checks for the main results of Table 4, varying the nature of some explanatory variables (i.e., productivity, age, size, leverage, and innovation), sample, indicator variable (i.e., employment vs. sales growth), and HG threshold (top 10% vs. top 20%). Complete tables are included in the Online Appendix (Tables B1–B6) and are broadly consistent with our main findings (Table 4).

First, we re-estimate our baseline model in Table 4, replacing our measure of firm productivity with firm total factor productivity (Table B1). The results confirm our findings in our baseline specification, except for a non-significant impact of the highest productivity group on the probability of experiencing HG.Footnote 27

Second, the results of Table 4 hold up when we use continuous and time-varying covariates as they are originally found in the ESEE, that is, size, age, productivity, and leverage. This specification takes advantage of the maximum within-firm variation over time of explanatory variables (Table B2). This partly mitigates the criticism pointed out by Coad and Srhoj (2019) related to the use of variables with low variation within firms over time to predict HG firms. Rather interestingly, the impact of size and productivity are consistent with those using categorized variables. Smaller and more productive firms are more likely to experience HG and to persist longer in HG status.

Third, Table B3 further explores the role of innovation activities. The results are broadly consistent with our findings in our baseline specification. In addition, the introduction of an interaction between product and process innovations reinforces our previous findings that process innovation (and not product or both product and process) increases the likelihood of experiencing an HG episode. In addition, the two binary indicators introduced to capture whether firms carry out R&D or patenting show no effect in each of the two hazards examined. This result is consistent with the finding by Brenner and Schimke (2015) that R&D and export activities reduce the risk of fluctuations as firms become less vulnerable to unexpected circumstances.

Fourth, in the baseline specification, we proceed by considering as censored all spells that do not end in a transition to its complementary state (HG, NHG). One may argue that there could be heterogeneity between spells ending in firm exit or M&A and those dropped from the survey. The results of Table 4 remain unaltered after drop** all observations corresponding to spells ending in firm exit or the firm being acquired (Table B4).

Fifth, Table B5 re-estimates our baseline model when we replace employment with (real) sales as the indicator variable for growth (e.g., Erhardt 2019).Footnote 28 Except for few changes in hazard ratios associated with some variables that explain the transitions from NHG to HG (productivity, being an exporter, and belonging to an industrial group), the results regarding most of the firm and market (demand) characteristics for the hazards of both NHG and HG spells are confirmed. Consistent with our main results, a longer current spell is significant in explaining a higher persistence in the HG state, especially for those spells that last for 3 years or more (captured by the coefficient of SP_LENGTH3, in col. 2). Conversely, having experienced past episodes (spells) of NHG or HG does not ensure a higher probability of shifting to the HG state or a higher persistence in it, respectively, compared with firms that are in their first spell (non-significant hazard ratios of SP_REP2 and SP_REP3 in cols. 1 and 2).

Sixth, as a final robustness check, we consider a less restrictive definition of HG by replacing the threshold of the top 10% of the annual growth distribution with the top 20% of the distribution (Table B6). The use of this lower cutoff point implies that we may classify some firms with relatively modest growth rates as HG. Specifically, the minimum and maximum values of this new threshold are 2.67% and 8.39%, respectively (vs. 11.12% and 18.43% if we focus on the top 10%). Overall, the results are consistent with our baseline results in Table 4. Yet, as expected, few differences emerge. The use of a less restrictive definition for the dependent variable may have led to a reduction in the explanatory power of some covariates. Specifically, negative duration dependence is found for NHG spells, while no duration dependence arises for HG spells. The probability of experiencing an HG episode is only lower for very old firms, and being a member of a group does not increase the expected duration. In contrast to our previous findings, process innovation increases the expected duration in HG that could indicate that process innovation is positively associated with persistent positive (moderate) growth, while it is less effective for persistence in very high growth.

5 Concluding remarks

While HGFs have attracted the attention of scholars, policymakers, and the popular press in recent years, several features of this group of firms are still not clear cut (Audretsch 2012; Coad et al. 2014). Among the open issues, we may outline the following ones: First, there is the controversial nature of the HG phenomenon in terms of whether it is fully “episodic” or—at least for some firms—rather “persistent.” Second, there is the role of market (demand) characteristics on top of that played by firm (supply) characteristics in explaining the probability of experiencing an HGE and the persistence in it. Third, there is the role of the different phases of the business cycle in explaining HG and its determinants. In relation to these issues, this paper contributes to the literature in three ways, as described below.

First, using duration models, we identify the episodes (spells) of HG and NHG in a representative sample of Spanish manufacturing firms with more than 10 employees over about two decades. HGEs are not uncommon, but they are usually short and rather hard to repeat. Nonetheless, there are a few HGEs that last several years. These episodes depict a self-reinforcing effect in the probability of lasting longer the higher their length (duration dependence), and they are mainly explained by (other than age and size) market dynamism and process innovations strategies. The results point to the existence of two groups of firms, which are as follows: (i) firms with long HG spells and short NHG spells and (ii) firms with short HGEs and long NHG spells. At the same time, it is difficult to explain, and thus to predict, the repetition of HG spells over time within the same firm. Second, in the empirical analysis, together with spell characteristics, we have included a vector of firm and market (demand) characteristics. Firm characteristics confirm the previous literature findings. Moreover, an expansionary dynamic both of the market in which a firm is active and its increasing market share positively affects the probability of the firm experiencing an HG episode and making it last longer. Third, we have explored the role of the business cycle in enhancing or hindering the determinants of both experiencing an HG episode and persisting in it. Few variables show a differentiated effect across the phases of the business cycle, but they bring interesting insights. In particular, while the role of younger age and smaller size for explaining the transition from NHG to HG is reduced during the years of the Great Recession, no changes are observable in relation to these two variables for the persistence in HG. At the same time, the positive effect of introducing a process innovation for persistence in HG in the expansionary phase is reversed during the Great Recession. Furthermore, the positive effect of belonging to a group of firms on HG persistence disappears during the downturn, which may suggest the redistribution of resources between affiliates in a context of diminished domestic investment opportunities.

Taking stock of these results, we put forward that the researchers interested in HGFs should complement firm-level analyses with episode (spell)-level investigations. Episodes of HG may be the proper target for economic policies aimed at fostering dynamic economies (Bravo-Biosca et al. 2016). Policymakers may devote effort to designing policies that support the following: (i) firm entry by young firms, and through more effective exit procedures, a more effective resource reallocation across and toward the most productive firms; (ii) more effective flows/transfers of knowledge, managerial practices, and technology flows across firms through denser networks; and (iii) improvements in firm internal processes and productivity, fostering stronger firm capabilities.

Finally, rather tentatively, our paper has a final implication for policy makers in the turmoil of economic shocks. Our findings suggest that, in general, small and young firms (which account for a large share of SMEs) are more likely to be in the group of firms that endure short NHG and long HG spells that significantly contribute to employment growth. It is well documented the higher levels of vulnerability and lower resilience of SMEs during economic shocks (e.g., COVID-19 pandemic, 2008 financial crisis). Traditionally, practitioners and policy makers point out the need to protect them due to their importance as they account for the vast majority of companies and employment. This is particularly important in countries and regions where the prevalence of SMEs is even higher (e.g., Spain, Italy) as well as in certain industries. Our paper unravels an additional argument to protect them during downturns given that they tend to have long HG spells and short NHG, prompting economic growth and job creation.

Notes

Throughout the paper, we use the terms spell and episode interchangeably.

The definition of (what constitutes) an HGF is not a trivial issue (Coad et al. 2014); indeed, the choice of the growth metric may well affect the results of the analyses (Delmar et al. 2003; Daunfeldt et al. 2013). The reader is cross-referred to Section 3, in which we introduce the definition of HG employed in this work.

We also jointly estimate the equations modeling the two types of transitions, allowing for non-zero correlation across the firm-level unobserved variables that affect both transitions.

The sampling procedure of the ESEE is the following: firms with fewer than 10 employees are excluded from the survey. Firms with 10–200 employees are randomly sampled by two-digit NACE industry and size strata, holding around 4% of the population in 1990. All firms with more than 200 employees were requested to participate, resulting in a participation rate of around 60% in 1990. Important efforts have been made to minimize attrition and annually incorporate new firms with the same sampling criteria as in the base year so that the sample of firms is representative of the Spanish manufacturing sector over time. See https://www.fundacionsepi.es/investigacion/esee/en/spresentacion.asp for comprehensive information about the ESEE.

The ESEE does not provide the number of hours worked by part-time employees, but they are merely 3% of permanent workers.

In the words of Sutton (1997, p. 40), “Size can be measured in a number of ways […] annual sales, […] current employment, and […] total assets. Though we might in principle expect systematic differences between the several measures, such differences have not been a focus of interest in the literature.”

Firms in the sample grow either organically or via M&As. For the purpose of this work and to avoid losing the information provided by firms that go through M&As or spin-off procedures, we identify episodes of non-organic growth at the moment in time in which they happen (year t). We consider the pre-episode (up to year t − 1) and post-episode (from year t + 1 onward) units of analysis as two separate spells.

Admittedly, while our definition resembles Birch’s (1981) definition, an absolute definition may also be used, such as the one proposed by the Eurostat–OECD Manual on Business Demography Statistics (2007). The manual defines an HGF as one with the following attributes: (i) it initially possesses 10 or more employees or has at least four times the national per capita income in annual revenues, and (ii) it experiences average annualized employment or revenue growth of greater than 20% over a 3-year period. While the debate about what constitutes an HGF is nontrivial (Coad et al. 2014), it is beyond the scope of this work. Only for comparison purposes with the definition advocated by the Eurostat–OECD manual, we report that about 3% of firms fulfill the criterion of having a cumulative average growth rate larger than 20% for 3 consecutive years.

For example, in 2009 (the worst year for employment in Spain), the 90th percentile was 0.0453, which contrasts sharply with the 1998 value of 0.198.

The NHG state comprises a heterogeneous set of growth episodes (from mildly positive to very negative), gathering a lot of heterogeneity. Some of these episodes may be interesting per se (e.g., the high-decline firms, as suggested by Coad et al. 2014), but exploitation of the heterogeneity within the NHG state is beyond the scope of this work.

Briefly, we start with an unbalanced panel of firms over 1991–2016. The definition of HGF involves comparing a firm’s annual growth rate with the sample annual growth rate obtained using a 3-year moving average. Therefore, we define HG/NHG states from 1993 to 2015. Furthermore, in the survival analysis, (i) the information in 2015 is only used to determine whether ongoing spells in 2014 end or are right-censored (i.e., continue in 2015); (ii) we focus on “fresh” spells, so ongoing spells in 1993 are dropped. Thus, we end up with 24,947 observations.

This corresponds to the simple mean of observed durations both for complete and right-censored spells.

To avoid an odd behavior in the estimated baseline hazard functions due to scarcity of observations spanning longer durations, we right-censor spells of HG longer than 3 years. Likewise, to make the results comparable for the two transitions, we apply the same right-censoring to NHG spells, which is also supported by piecewise estimates of the baseline (not reported, but available from the authors upon request) that suggest no significant differences in hazards across different spell ages.

However, if unmeasured factors that affect the error term were correlated with our lagged covariates over time, then biased estimators would be obtained. We partly deal with this issue both using a relatively large set of explanatory variables and estimating frailty duration models that account for firm-level unobserved heterogeneity.

We are grateful to a reviewer for raising this point.

In the model for the transitions NHG to HG, we cannot reject the existence of unobserved heterogeneity (col. 1 in Tables 3 and 4). Hence, the regression coefficients for this model are defined conditional on the unobserved heterogeneity. Hence, the impact of each covariate holds valid for two spells with an identical frailty term.

Table C1 in an online appendix reports the full estimates of the columns labeled “Total” for NHG and HG hazards.