Abstract

The relationship between uncertainty and managerial flexibility is particularly crucial in addressing capital projects. We consider a firm that can invest in a project in either a single (lumpy investment) or multiple stages (stepwise investment) under price uncertainty and has discretion over not only the time of investment but also the size of the project. We confirm that if the capacity of a project is fixed and the investment premium associated with stepwise investment is positive, then lumpy investment becomes more valuable than a stepwise investment strategy under high price uncertainty. By contrast, if a firm has discretion over capacity, then we show that the stepwise investment strategy always dominates that of lumpy investment. In addition, we show that the total amount of installed capacity under a stepwise investment strategy is always greater than that under lumpy investment.

Similar content being viewed by others

References

Abel AB, Eberly JC (1996) Optimal investment with costly reversibility. Rev Econ Stud 63(4):581–593

Adkins R, Paxson D (2015) Stepwise Investment Value under Stage Specific Parameters, working paper. Bradford University School of Management, Bradford

Alvarez L, Stenbacka R (2004) Optimal risk adoption: a real options approach. Econ Theory 23:123–147

Anand KS, Girotra K (2007) The strategic perils of delayed differentiation. Manag Sci 53(5):697–712

Arrow K, Fisher AC (1974) Environmental preservation, uncertainty, and irreversibility quarterly. J Econ 88:312–319

Baldursson F, Karatzas I (1997) Irreversible investment and industry equilibrium. Financ Stoch 1:69–89

Baldwin CY, Clark KB (2000) Design rules: the power of modularity. MIT Press, Cambridge

Bøckman T, Fleten SE, Juliussen E, Langhammer HJ, Revdal I (2008) Investment timing and optimal capacity choice for small hydropower projects. Eur J Oper Res 109(1):255–267

Boomsma TK, Meade N, Fleten SE (2012) Renewable energy investments under different support schemes: a real options approach. Eur J Oper Res 220(1):225–237

Chod J, Rudi N (2005) Resource flexibility with responsive pricing. Oper Res 53(3):532–548

Chronopoulos M, De Reyck B, Siddiqui AS (2012) The value of capacity sizing under risk aversion and operational flexibility. IEEE Trans Eng Manag 60(2):272–288

Dangl T (1999) Investment and capacity choice under uncertain demand. Eur J Oper Res 117:415–428

Dixit AK, Pindyck RS (1994) Investment under uncertainty. Princeton University Press, Princeton

Doege J, Schiltknecht P, Lüthi HJ (2006) Risk management of power portfolios and valuation of flexibility. OR Spectrum 28(2):267–287

Gahungu J, Smeers Y (2012) A real options model for electricity capacity expansion. Université Catholique de Louvain, CORE, B-1348, Louvain-la-Neuve

Gamba A, Fusari N (2009) Valuing modularity as a real option. Manag Sci 55(11):1877–1896

Gollier C, Proult D, Thais F, Walgenwitz G (2005) Choice of nuclear power investments under price uncertainty: valuing modularity. Energy Econ 27:667–685

Goyal M, Netessine S (2007) Strategic technology choice and capacity investment under demand uncertainty. Manag Sci 53(2):192–207

Hagspiel V, Huisman KJM, Kort PM (2016) Volume Flexibility and Capacity Investment under Demand Uncertainty. Int J Prod Econ 178:95–108

Henry C (1974) Investment decisions under uncertainty: the irreversibility effect. Am Econ Rev 64:89–104

He H, Pindyck RS (1992) Investments in flexible production capacity. J Econ Dyn Control 16:575–599

Huisman KJM, Kort PM (2015) Strategic capacity investment under uncertainty. RAND J Econ 46(2):376–408

Jørgensen S, Kort PM (1993) Optimal dynamic investment policies under concave–convex adjustment costs. J Econ Dyn Control 17:153–180

Kort PM, Murto P, Pawlina G (2010) Uncertainty and stepwise investment. Eur J Oper Res 202(1):196–203

Leahy JV (1993) Investment in competitive equilibrium: the optimality of myopic behavior. Q J Econ 108(4):1105–1133

Löffler C, Pfeiffer T, Schneider G (2013) The irreversibility effect and agency conflicts. Theory Decis 74:219–239

Longstaff FA, Schwartz ES (2001) Valuing American options by simulation: a simple least-squares approach. Rev Financ Stud 14(1):113–147

Lund D (2005) How to analyse the investment–uncertainty relationship in real option models. Rev Financ Econ 14:311–322

Mackintosh J (2003) Ford learns to bend with the wind. Financial Times, 14 February

Majd S, Pindyck RS (1987) Time to build, option value, and investment decisions. J Financ Econ 18:7–27

Malchow-Møller N, Thorsen BJ (2005) Repeated real options: optimal investment behavior and a good rule of thumb. J Econ Dyna Control 29:1025–1041

Pawlina G, Kort PM (2003) Strategic capital budgeting: asset replacement under market uncertainty. OR Spectrum 25(4):443–479

Pindyck RS (1988) Irreversible investment, capacity choice, and the value of the firm. Am Econ Rev 79:969–985

Rodrigues A, Armada MJ (2007) The valuation of modular projects: a real options approach to the value of splitting. Global Financ J 18:205–227

Siddiqui AS, Maribu KM (2009) Investment and upgrade in distributed generation under uncertainty. Energy Econ 31(1):25–37

Siddiqui AS, Takashima R (2012) Capacity switching options under rivalry and uncertainty. Eur J Oper Res 222(3):583–595

Takashima R, Siddiqui AS, Nakada S (2012) Investment timing, capacity sizing, and technology choice of power plants. Handbook of networks in power systems I energy systems, pp 303–321

Acknowledgments

The authors would like to express their gratitude to Peter Kort for his valuable comments that helped improve the paper.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Proposition 1

The optimal investment threshold and the corresponding optimal capacity under lumpy and stepwise investment are:

Proof

By maximising the value of the now-or-never investment opportunity, we obtain the expression for the optimal capacity, \(\overline{K}^*_{j}\), corresponding to the current output price P, as indicated in (A.2) for \(j = \ell , s_{i}\).

Next, the value of the option to invest is described in (A.3).

By expanding the first branch on the right-hand side of (A.3) using Itô’s lemma, we obtain the differential equation (A.4)

which, for \(P<P^*_{j}\), has the general solution that is indicated in (A.5).

Notice that \(\delta \) is the negative root of the quadratic \(\frac{1}{2}\sigma ^2x(x - 1) + \mu x - \rho = 0\), and therefore, \(P \rightarrow 0\Rightarrow B_{j}P^{\delta } \rightarrow \infty \). Consequently, we must have \(B_{j} = 0\), and thus, we finally obtain (A.6).

By applying value-matching and smooth-pasting conditions between the two branches of (A.6), we obtain the expression for the endogenous constant and the optimal investment threshold that are indicated in (A.7) and (A.8), respectively.

By inserting (A.8) into (A.2), we obtain the expression for the optimal capacity

while the final expression for the optimal investment threshold is obtained by inserting (A.9) into (A.8) and is indicated in (A.10).

\(\square \)

Proposition 2

\(P^*_{s_{1}}\) is independent of \(P^*_{s_{2}}\).

Proof

If we assume that \(\tau _{s_{2}}\ge \tau _{s_{1}}\), then \(P^*_{s_{1}}\le P^*_{s_{2}}\) and the maximised option value in the case of staged investment is indicated in (A.11).

Hence, \(p_{s_{1}}\) satisfies the first-order necessary condition (A.12)

from which we have:

Consequently, \(P^*_{s_{1}}\) is independent of \(P^*_{s_{2}}\), i.e. the presence of the second stage does not affect the decision to invest in the first one. Note that the assumption \(P^*_{s_{1}}< P^*_{s_{2}}\) can be expressed as in (A.14).

\(\square \)

Proposition 3

\(\frac{\partial K^*_{j}}{\partial \sigma }>0\) and \(\frac{\partial P^*_{j}}{\partial \sigma }>0\).

Proof

By differentiating the expression of the optimal capacity in (A.9), we have:

Since \(\frac{\partial }{\partial \sigma }\beta <0\), we have \(\frac{\partial K^*_{j}}{\partial \sigma }>0\). Additionally, the expression of the optimal investment threshold is:

Since \(\frac{\partial }{\partial \sigma } \frac{\beta }{\beta - 1}>0\) and \(\frac{\partial }{\partial \sigma }K^*_{j}>0\) we have \(\frac{\partial }{\partial \sigma }P^*_{j}>0\). \(\square \)

Proposition 4

If a firm has discretion over capacity, then \(F_{s}(P)> F_{\ell }(P)\).

Proof

The relative value of the two strategies is indicated in (A.17).

to show that \(F_{s}(P)> F_{\ell }(P)\), we will show that each term on the right-hand side of (A.17) is greater than one, i.e.

By manipulating the expression of the relative value in (A.18) we obtain (A.19)

where the expression for \(\frac{K^*_{s_{i}}}{K^*_{\ell }}\) is indicated in (A.20).

By substituting the expression for \(\frac{K^*_{s_{i}}}{K^*_{\ell }}\) into (A.19) and by inserting the expression for the optimal capacity from (A.9) into (A.19), we finally obtain (A.21).

Notice that \((\beta -1)(\gamma - 1)>1\Leftrightarrow \beta >\frac{\gamma }{\gamma - 1}\), which is the required condition so that \(K^*_{j}\in \mathbb {R}^{^{+}}\). Additionally, by differentiating (A.18) with respect to \(\sigma \) as in (A.22), we can determine the relationship between uncertainty and the relative value of the two strategies.

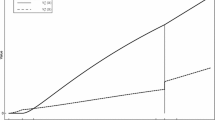

Notice that if \(a_{s_{i}}<a_{\ell }\), then greater uncertainty decreases the relative value of the stepwise investment strategy. Consequently, if \(a_{s_{i}}<a_{\ell }\) \(\forall i\in \mathbb {N}\), then \(\sigma \nearrow \ \Rightarrow \ \frac{F_{s}(P)}{F_{\ell }(P)}\searrow \). In addition, from (A.21) we conclude that the stepwise investment strategy is always more valuable than lumpy investment.

\(\square \)

Proposition 5

\(K^*_{\ell }<\sum ^{n}_{i = 1} K^*_{s_{i}} \ \Leftrightarrow \ a^{^{\frac{1}{\gamma - 1}}}_{\ell }<\sum ^{n}_{i = 1} a^{^{\frac{1}{\gamma - 1}}}_{s_{i}}\).

Proof

The optimal capacity of the project under lumpy and stepwise investment is described in (A.24).

From (A.24) we have \( K^*_{\ell }< K^*_{s_{1}} + K^*_{s_{2}} \Leftrightarrow a^{^{\frac{1}{\gamma - 1}}}_{\ell } < a^{^{\frac{1}{\gamma - 1}}}_{s_{1}} + a^{^{\frac{1}{\gamma - 1}}}_{s_{2}}\). Notice that this inequality cannot be solved analytically for all values of \(\gamma \). However, since \(\gamma>\frac{\beta }{\beta - 1}>1\), it is easy to see that \(\gamma = 2\Rightarrow a_{\ell } < a_{s_{1}} + a_{s_{2}}\), which holds by assumption. Similarly, by substituting the expression for \(K^*_{j}\) into (3), we find that the assumption \(I(K^*_{\ell })<\sum _{i}I (K^*_{s_{i}})\) is equivalent to (A.25).

Consequently, it is not sufficient to assume that \(a_{\ell } < a_{s_{1}} + a_{s_{2}}\) to ensure that at the optimal solution, the modular project is more expensive than the lumpy one. Instead, this assumption depends on a more complex relationship between the cost parameters \(a_{j}\) and the convexity of the cost function. \(\square \)

Corollary 1

The MB is steeper than the MC.

Proof

The result follows from differentiating the MB and MC of delaying investment with respect to the output price. Notice that the MC is positive and independent of the output price, while \(\frac{\partial }{\partial P}\hbox {MB}<0\). \(\square \)

Proposition 6

If \(K_{j}\) is fixed, then \(\frac{\partial }{\partial \sigma }\hbox {MB}<0\), \(\frac{\partial }{\partial \sigma }\hbox {MC}<0\), and \(|\frac{\partial }{\partial \sigma }\hbox {MB}|<|\frac{\partial }{\partial \sigma }\hbox {MC}|\), whereas if \(K_{j}\) is scalable, then \(\frac{\partial }{\partial \sigma }\hbox {MB}>0\), \(\frac{\partial }{\partial \sigma }\hbox {MC}>0\), and \(\frac{\partial }{\partial \sigma }\hbox {MB}>\frac{\partial }{\partial \sigma }\hbox {MC}\).

Proof

The MB and MC of delaying investment is indicated in (A.26).

Notice that if the capacity of the project is fixed, i.e. \(K^*_{j}\equiv K_j\), then an increase in \(\sigma \) lowers both the MB and the MC as indicated in (A.27).

However, from (A.13) we know that \(\frac{I(K_{j})}{P^*_{j}}< \frac{K_{j}}{\rho - \mu }\), and therefore, the MC of delaying investment decreases by more than the MB.

By contrast, if the capacity of the project is scalable, then the MB and MC of delaying investment increase with greater price uncertainty. Indeed, for \(P < P^*_{j}\), we have:

The second term on the right-hand side of (A.29) is positive since \(\frac{\partial }{\partial \sigma }K^*_{j}>0\). Notice also that even though \(\frac{\partial }{\partial \sigma }\beta <0\), \(\beta \) is bounded from below since \(\beta >1\). By contrast, since the capacity of the project is not bounded and \(\frac{\partial }{\partial \sigma }I(K^*_{j})>0\), the decrease in \(\beta \) is mitigated by the increase in the investment cost. The impact of \(\sigma \) on the MC is indicated in (A.30).

Notice that the reduction in \(\beta \) makes the impact of \(\sigma \) on \(K^*_{j}\) less pronounced, and therefore, the second term on the right-hand side of (A.29) is greater than right-hand side of (A.30). Since the first term on the right-hand side of (A.29) is positive, we have:

Finally, notice that the second term on the left-hand side of (A.26) is constant when the capacity is fixed and increasing when the capacity is scalable. Similarly, the reduction of the first term due to the decrease in \(\beta \) with greater uncertainty is offset by the increase in \(K^*_{j}\). Consequently, the impact of \(\sigma \) on the MB of delaying investment is not only reversed when the firm has discretion over capacity but it is also more pronounced. \(\square \)

Rights and permissions

About this article

Cite this article

Chronopoulos, M., Hagspiel, V. & Fleten, SE. Stepwise investment and capacity sizing under uncertainty. OR Spectrum 39, 447–472 (2017). https://doi.org/10.1007/s00291-016-0460-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00291-016-0460-0