Abstract

This paper aims at constructing potential output and output gap measures for the UK which are pinned down by macroeconomic relationships as well as financial indicators. The exercise is based on a parsimonious unobserved components model which is estimated via Bayesian methods where the time-paths of unobserved variables are extracted with the Kalman filter. The resulting measures track current narratives on macroeconomic cycles and trends in the UK reasonably well. The inclusion of summary indicators of financial conditions leads to a more optimistic view on the path of UK potential output after the crisis and adds value to the model via improving its real-time performance. The models augmented with financial conditions have some real-time wage inflation forecasting ability over the monetary policy-relevant 2- to 3-year horizon during the last 15 years. Finally, we also introduce a new approach to construct financial conditions indices, with emphasis on their real-time performance and ability to track the evolution of macro-financial imbalances. Our results can be relevant from both monetary and macro-prudential policy perspectives.

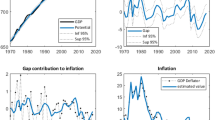

Source: Eurostat—Ameco database

Source: Bank of England, ONS

Similar content being viewed by others

Notes

See e.g. van Norden and Orphanides (2004).

See Havik et al. (2014).

In fact, for the UK, a number of relevant macroeconomic time series have become less volatile since the introduction of inflation targeting in 1992. For example, the standard deviation of a HP-filtered measure of the output gap in 1992 to 2014 is half of its level in 1970 to 1991, while the standard deviation of core inflation is one-fourths of its level in 1970 to 1991.

For a detailed overview on the information content of the long-term unemployment rate with respect to the NAIRU (or trend unemployment rate), see Rusticelli (2014).

For details of data used in the analysis, see Appendix 3.

This is sometimes referred to as a “local linear trend” decomposition, see e.g. Harvey et al. (1998).

See Benes et al. (2010) for a similar approach.

The original formulation of the Phillips curve included wage instead of price inflation (see Phillips 1958). We experimented with different measures of inflation; the main results are relatively robust to the different measures.

Estimation and filtering have been implemented in Matlab with the help of the Iris-toolbox, see: J. Benes, M. K. Johnston, and S. Plotnikov, IRIS Toolbox Release 20150318 (Macroeconomic modelling toolbox). The software is available at http://www.iris-toolbox.com.

We also experimented with larger values for the hyper-parameters of trends and cycles, whilst holding their relative values constant. The results are very similar.

One alternative to this approach is a computationally less-intensive Gibbs sampling, which can be thought of as a Metropolis–Hastings algorithm with a special proposal distribution that is always accepted (see e.g. Robert and Casella 2004). This would have required the usage of (possibly truncated) normal prior densities for the coefficients to be estimated and thus would have limited our choice of priors. Due to the presence of AR(1) terms and our prior views on the sign of the non-AR coefficients in the state equations, we did not find it useful to restrict ourselves to normal priors and the Gibbs sampler.

Median values are close to mean values, so there is no qualitative difference between the results using any of these measures. However, in the case of asymmetry the median is typically considered as the more representative moment of the distribution.

See Jarocinski and Lenza (2016), for a similar approach.

We define pseudo-real-time as filtered real-time estimation of the models, using latest vintage (2014Q4) data. In Sect. 3.2, we use vintage real-time GDP data and quarterly re-estimation of the models to test the fully fledged real-time performance of the models.

However, it is notable how weak net lending and credit dynamics (an important variable in the FCIs) remained at the end of the sample.

For example, OECD, in its June 2015 Economic Outlook, estimated the trend output in the UK at between 2 and 2.5% 2004 to 2006, and at 1.8% in 2014.

Of course, not even this exercise can replicate the true nature of uncertainty as no account is taken of actual vintage price/wage inflation and unemployment rate data (for which revisions are relatively small, however) nor of the uncertainty related to availability of current modelling techniques at each point in time.

The inclusion of the forward-looking element does not have a large effect on the real-time output gap estimates nor the performance of these estimates, although it does have some effect on the level of the gap at the end of the sample. The results for the B1 model are not reported in this section, as they are very close to the B2 model.

This is also true for the estimates of trend unemployment, but we do not report the results here, as this is not the focus of our study.

The models are first estimated with data up to 2004q4, and then, a forecast is produced for each quarter for a three-year period forward. The estimation period is then rolled forward quarter by quarter. Forecasting performance against a simple random walk assumption can then be assessed with standard tools, like root-mean-square errors (RMSE) and Theil U (the relative RMSE of a UCM versus that of a random walk assumption). It is also worth noting that in the FCI models, the dynamic factor model for the FCI is executed in real time to allow only for financial markets data up to the examined point in time to affect the FCI estimate.

This choice is also in line with the original formulation of the Phillips curve (see Phillips (1958)).

For brevity, only Figures for the FCI models are reported here. Other results are available from the authors on request.

The smoothing is not crucial for the results of the FCI model presented in this paper, but it slightly improves the real-time performance of the FCI as well as smoothing the short-term volatility.

For details on the construction of the time series, see Speigner (2014).

References

Andrle M (2013) What is in your output gap? Unified framework & decomposition into observables. IMF Working Paper No. 105 (May 2013)

Arseneau DM, Kiley M (2014) The role of financial imbalances in assessing the state of the economy. FEDS Notes, April 18 2014

Benes J, Clinton K, Garcia-Saltos R, Johnson M, Laxton D, Manchev P, Matheson T (2010) Estimating potential output with a multivariate filter. IMF Working Paper No 285 (December 2010)

Bernanke BS, Gertler M, Gilchrist S (1999) The financial accelerator in a quantitative business cycle framework. In: Taylor JB, Woodford M (eds) Handbook of macroeconomics, vol 1, Part C. Elsevier, Amsterdam, pp 1341–1393

Blagrave P, Garcia-Saltos R, Laxton D, Zhang F (2015) A simple multivariate filter for estimating potential output. IMF Working Paper 15/79

Borio C, Disyatat P, Juselius M (2013) Rethinking potential output: embedding information about the financial cycle. BIS Working Papers No 404

Borio C, Disyatat P, Juselius M (2014) A parsimonious approach to incorporating economic information in measures of potential output. BIS Working Papers No 442

Darracq-Paries M, Maurin L, Moccero D (2014) Financial conditions index and credit supply shocks for the euro area. ECB Working Paper No. 1644

Darvas Z, Simon A (2015) Filling the gap: open economy considerations for more reliable potential output estimates. Bruegel Working Paper 2015/11

Durbin J, Koopman SJ (2001) Time series analysis by state space methods. Oxford University Press, Oxford

Fernald J (2012) Productivity and potential output before, during and after the great recession. Federal Reserve Bank of San Francisco Working Paper 2012-18

Fisher I (1933) The debt-deflation theory of great depressions. Econometrica 1(4):337–357

Gali J (2010) The return of the wage Phillips curve. NBER Working Paper No. 15758 (February 2010)

Gertler M, Karadi P (2011) A model of unconventional monetary policy. J Monet Econ 58(1):17–34

Grant A, Chan J (2017) A Bayesian model comparison for trend-cycle decompositions of output. J Money Credit Bank 49:525–552

Guichard S, Haugh D, Turner D (2009) Quantifying the effect of financial conditions in the euro area, Japan, United Kingdom and United States. OECD Economics Department Working Papers No. 677

Harvey A, Koopman SJ, Penzer J (1998) Messy time series: a united approach. Adv Econom 13:103–143

Havik K, McMorrow K, Orlandi F, Planas C, Raciborski R, Roeger W, Rossi A, Thum-Thysen A, Vandermeulenet V (2014) The production function methodology for calculating potential growth rates & output gaps. European Commission Economic Papers No 535

Iacoviello M (2005) House prices, borrowing constraints, and monetary policy in the business cycle. Am Econ Rev 95(3):739–764

Jarocinski M, Lenza M (2016) An inflation-predicting measure of the output gap in the euro area. ECB Working Paper No 1966

Jorda O, Schularick M, Taylor AM (2016) Macrofinancial history and the new business cycle facts. NBER Macroecon Annu 31:213–263

Kalman R (1960) A new approach to linear filtering and prediction problems. J Basic Eng 82(1):35–45

Kiyotaki N, Moore J (1997) Credit cycles. J Polit Econ 105:211–248

Kuttner K (1994) Estimating potential output as a latent variable. J Bus Econ Stat 12(3):361–368

Luo S, Startz R (2014) Is it one break or ongoing permanent shocks that explains US real GDP? J Monet Econ 66:155–163

Matheson T (2012) Financial conditions indexes for the United States and Euro area. Econ Lett 115(3):441–446

OBR (2014) Output gap measurement: judgement and uncertainty. Working paper No 5

Okun A (1962) Potential GDP, its measurement and significance. Cowles Foundation, Yale University, New Heven

Orphanides A (2003) Monetary policy evaluation with noisy information. J Monet Econ 50(3):605–631

Orphanides A, van Norden S (2002) The unreliability of output gap estimates in real time. Rev Econ Stat 84:569–583

Phillips AW (1958) The relationship between unemployment and the rate of change of money wages in the United Kingdom 1861–1957. Economica 25(November):283–299

Reinhart CM, Rogoff KS (2009) The aftermath of financial crises. Am Econ Rev 99(2):466–472

Robert CP, Casella G (2004) Monte Carlo statistical methods, 2nd edn. Springer, Berlin

Rusticelli E (2014) Rescuing the Phillips curve: making use of long-term unemployment in the measurement of the NAIRU. OECD J Econ Stud 2014(1):109–127

Speigner B (2014) Long-term unemployment and convexity in the Phillips curve. Bank of England Working Paper No. 519

Stock JH, Watson MW (1991) A probability model of the coincident economic indicators. In: Lahiri K, Moore G (eds) Leading economic indicators: new approaches and forecasting records, Chap. 4. Cambridge University Press, Cambridge

Stock JH, Watson MW (1998) Median unbiased estimation of coefficient variance in a time-varying parameter model. J Am Stat Assoc 93(441):349–358

Tóth M (2015) Measuring the cyclical position of the Hungarian economy: a multivariate unobserved components model. Mimeo, New York

van Norden S, Orphanides A (2004) The reliability of inflation forecasts based on output gap estimates in real time. FEDS Working Paper No. 2004-68

Author information

Authors and Affiliations

Corresponding author

Additional information

The views expressed in this paper are those of the authors, and not necessarily those of the Bank of England, the European Central Bank or Magyar Nemzeti Bank. We are grateful to Mikael Juselius and two anonymous referees for comments on the paper. We thank Stefania Spiga for excellent research assistance.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Appendices

Appendix 1: Technical details of the unobserved components model

1.1 State-space form of the UCM

The state-space form gathers the structure of the model into a form consisting of a measurement equation and a state equation. The state-space form can be easily handled by the Kalman filter:

Based on the structure introduced above, the measurement equation consists of the following matrices (for B2, the last row and column are excluded):

The state equation is the following (for B2, the last row and column are excluded):

1.2 Conditional forecast information

The actual real-time versions of the FCI models are also augmented with Bank of England CPI and GDP forecasts to examine whether this improves the real-time performance. The forecasts are added to the models in a similar fashion as in Blagrave et al. (2015):

for \( j = 1, \ldots ,12, \) for the level of GDP and rate of (quarterly) inflation, respectively. Hence, the forecasts are seen as imprecise estimates of future GDP and inflation, with error terms \( \varepsilon_{t + j}^{Yf} \) and \( \varepsilon_{t + j}^{\pi f} \) accounting for the noise and forecast errors. The forecast variables are added to the models in three formats: pure GDP, pure and CPI and both forecasts. As detailed in the main text, the pure GDP format adds the most information.

Appendix 2: Details of the financial conditions indices

It is not obvious which variables should be included in a financial conditions index (FCI) nor is there agreement on which estimation method should be used to derive the index. There is a wide existing literature on the estimation of FCIs.Footnote 28 In these studies, FCI’s are typically derived by using simple averages, principal components analysis or vector autoregressions. The main focus of many of these studies is to examine the ability of FCI’s to predict near-term GDP dynamics. However, there is surprisingly little (if any) analysis in the literature on the real-time performance of FCI models, which is a crucial metric for our purposes. Consequently, we refrain from using any of the existing FCI’s for the UK due to our different emphases on the construction of the FCI, as well as to avoid having to re-estimate and update FCI’s introduced in earlier studies. We are also primarily interested in building a financial conditions index with relevant information on the business cycle rather than just financial markets, which is a slightly different aim compared to more traditional FCI studies.

For the current study, 22 financial indicators for the UK were collected. Different combinations of these indicators were tested, and given the uncertainty related to the estimation of FCIs, we use two different FCIs (denoted FCI1 and FCI2), derived by different methods from different variable sets.

2.1 FCI1

For FCI1, four key UK financial indicators are combined using a simple factor model structure, where the FCI is the only state variable (i.e. a common factor driving the fluctuation in the observable indicators), and the four indicators are the observable variables with four idiosyncratic single shock terms. The four indicators were chosen with the relevant theoretical literature in mind (see the Introduction section). The factor model is estimated using a sample from 1988 to 2014, and the resulting FCI1 index relevant for the sample of the current study (i.e. from 1995 to 2014) is presented in Fig. 12. FCI1 performs well in real time and the contributions of the different indicators to it are intuitive (see Fig. 12c, e). The choice of the relevant indicators depends on the real-time performance of the model. The financial indicators (all demeaned and divided by their respective standard deviations) in the model are:

FCI indices and variables. Demeaned series. Series are normalised so that a tightening of conditions is a negative movement

-

Mortgage spread (2-year fixed mortgage rate (75% LTV) minus Bank Rate) (y/y growth rate). (Source: Bank of England) (mgage_spread)

-

Composite UK house price index (average of the Halifax and Nationwide House Price Indices) (y/y growth rate) (Bank of England/Halifax/Nationwide) (houseprice)

-

Credit to households in real terms (monetary financial institutions’ sterling net lending to the household sector deflated by CPI) (y/y growth rate). (Bank of England/ONS) (rcred_hhold)

-

Credit to firms in real terms (monetary financial institutions’ sterling net lending to the non-financial corporate sector deflated by CPI) (y/y growth rate). (Bank of England/ONS) (rcred_firms)

2.2 FCI2

For the second factor model (FCI2), a more mechanical approach was taken. First, the performance of different combinations of the most relevant financial indicators was examined to extract the best-performing common factor series in real time. In practice, the following procedure was followed:

-

1.

The general suitability and lengths of available samples was examined for all the series. Based on this analysis, nine of the 22 series were dropped either because the time series were too short or bore no relation to macroeconomic cycles.

-

2.

Real-time performance of all possible combinations of the remaining 13 variables was examined by running a real-time experiment from 2001 to 2014, recording the sum of standard deviations of the different vintages of the resulting FCI series at every quarter, and then, the combinations were ranked based on this sum. This experiment was carried out for an FCI consisting of four, five and six variables. Based on this analysis, it was decided that concentrating on 5-variable FCI’s would strike an optimal balance between the best real-time performance and maintaining as parsimonious a model as possible.

-

3.

The 13 variables entering into the 5-variable FCI’s were further ranked by their average position in terms of the standard deviations of the models that a particular variable entered in. The prevailing selection (above) was then made based on the best-performing variables, but also at the same time ensuring that the index would include interest rate spread variables, volatility variables and lending variables.

For the calculation of the index, the variables were first detrended and demeaned and then smoothed with a 4-quarter moving average measure of them.Footnote 29 The resulting index is again shown in Fig. 12a. Similarly to the FCI1 model, the FCI2 model also performs well in real time (Fig. 12d). A dynamic-factor model for FCI2 was derived using the following variables:

-

Net credit flow to households (monetary financial institutions’ sterling net lending to the household sector) (y/y growth rate). (Bank of England)

-

Net credit flow to non-financial corporations (monetary financial institutions’ sterling net lending to private non-financial corporations) (y/y growth rate). (Bank of England)

-

Money market spread (3-month GBP LIBOR minus Bank Rate) (Bloomberg/Bank of England)

-

Short gilt spread (2-year UK Gilt yield minus 3-month GBP LIBOR) (Bloomberg/Bank of England)

-

Bond market volatility (3-month rolling volatility of 10-year UK Gilt yield) (Bloomberg/Bank of England)

2.3 Summary

While the selection of any FCI is always contentious and is not the main focus of the current study, we believe that our FCI indices strike a balance between a good real-time performance, parsimoniousness and the inclusion of relevant variables. The FCIs are also not only relatively close to each other, but also relatively close over the relevant time horizon to the UK FCI introduced by OECD (see Guichard et al. 2009).

Appendix 3: Data

The following data is used in the models:

-

GDP: ESA2010 chain linked volumes, seasonally and working day adjusted (Source: ONS), in log level

-

Unemployment rate: LFS unemployment rate of 16–64-year-olds, in proportion of the labour force. (ONS)

-

Inflation: CPI excluding food and energy. Seasonally adjusted annualised q-o-q log changes (Bank of England/ONS)

-

Wage inflation: average weekly earnings, regular pay, seasonally adjusted annualised q-o-q changes (ONS)

-

Long-term unemployment rate: proportion of the labour force that has been unemployed for more than 12 months, based on claimant count statistics for the UKFootnote 30 (Bank of England/ONS)

-

Financial conditions indices (see details in Appendix 2).

Appendix 4: Additional Figures

FCI model—trend unemployment rate and trend price/wage variables. a Unemployment rate as %, bq/q change in %, cq/q change in %

Prior and posterior distributions of the FCI2w model

Rights and permissions

About this article

Cite this article

Melolinna, M., Tóth, M. Output gaps, inflation and financial cycles in the UK. Empir Econ 56, 1039–1070 (2019). https://doi.org/10.1007/s00181-018-1498-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-018-1498-4

Keywords

- Bayesian estimation

- Business cycle

- Forecasting

- Financial conditions

- Real-time data

- Unobserved components model