Abstract

Community detection for time series without prior knowledge poses an open challenge within complex networks theory. Traditional approaches begin by assessing time series correlations and maximizing modularity under diverse null models. These methods suffer from assuming temporal stationarity and are influenced by the granularity of observation intervals.

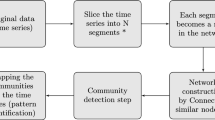

In this study, we propose an approach based on the signature matrix, a concept from path theory for studying stochastic processes. By employing a signature-derived similarity measure, our method overcomes drawbacks of traditional correlation-based techniques.

Through a series of numerical experiments, we demonstrate that our method consistently yields higher modularity compared to baseline models, when tested on the Standard and Poor’s 500 dataset. Moreover, our approach showcases enhanced stability in modularity when the length of the underlying time series is manipulated.

This research contributes to the field of community detection by introducing a signature-based similarity measure, offering an alternative to conventional correlation matrices.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

References

Albert-László, B.: Network science. In: Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences, vol. 371.1987, article no. 20120375 (2013)

Tsay, R.S.: Analysis of Financial Time Series. 2nd edn. John Wiley & Sons (2005)

Prigent, J. L.: Portfolio optimization and performance analysis. CRC Press (2007)

Mantegna, R.N., Stanley, H. E.: Introduction to econophysics: correlations and complexity in finance. Cambridge University Press (1999)

Sinha, S., Chatterjee, A., Chakraborti, A., Chakrabarti, B. K.: Econophysics: An Introduction. John Wiley & Sons (2010)

Onnela, J.P., Kaski, K., Kertész, J.: Clustering and information in correlation based financial networks. In: The European Physical Journal B, vol. 38, pp. 353–362 (2004)

Heimo, T., Kaski, K., Saramäki, J.: Maximal spanning trees, asset graphs and random matrix denoising in the analysis of dynamics of financial networks. In: Physica A: Statistical Mechanics and its Applications, vol. 388(2–3), pp. 145–156 (2009)

Mehta, M. L.: Random matrices. Elsevier (2004)

Bai, Z., Silverstein, J. W.: Spectral analysis of large dimensional random matrices (Vol. 20). New York: Springer (2010). https://doi.org/10.1007/978-1-4419-0661-8

Brockwell, P.J., Davis, R.A.: Introduction to Time Series and Forecasting, 2nd edn. Springer, New York, New York, NY (2002). https://doi.org/10.1007/b97391

Lyons, T. J.: Differential equations driven by rough signals. In: Revista Matemática Iberoamericana, vol. 14(2), pp. 215-310. (1998)

Lyons, T., Ni, H., Oberhauser, H.: A feature set for streams and an application to high-frequency financial tick data. In: In Proceedings of the 2014 International Conference on Big Data Science and Computing, pp. 1–8 (2014)

Chen, K.T.: Integration of paths A faithful representation of paths by noncommutative formal power series. In: Transactions of the American Mathematical Society, vol. 89(2), pp. 395-407 (1958)

Lyons, T.: Rough paths, signatures and the modelling of functions on streams (2014). In: ar**v preprint ar**v:1405.4537

Fisher, R.A.: Frequency distribution of the values of the correlation coefficient in samples from an indefinitely large population. In: Biometrika, vol. 10(4), pp. 507–521 (1915)

Yuan, S., Wang, C., Jiang, Q., Ma, J.: Community detection with graph neural network using Markov stability. In: 2022 International Conference on Artificial Intelligence in Information and Communication (ICAIIC), pp. 437–442. IEEE (2022)

Mantegna, R.N.: Hierarchical structure in financial markets. In: The European Physical Journal B-Condensed Matter and Complex Systems, vol. 11, pp. 193-197 (1999)

Bonanno, G., Caldarelli, G., Lillo, F., Micciche, S., Vandewalle, N., Mantegna, R. N.: Networks of equities in financial markets. In: The European Physical Journal B, vol. 38, pp. 363–371 (2004)

Tumminello, M., Aste, T., Di Matteo, T., Mantegna, R.N.: A tool for filtering information in complex systems. In: Proceedings of the National Academy of Sciences, vol. 102(30), pp. 10421–10426 (2005)

Tumminello, M., Di Matteo, T., Aste, T., Mantegna, R. N.: Correlation based networks of equity returns sampled at different time horizons. In: The European Physical Journal B, vol. 55, pp. 209–217 (2007)

Laloux, L., Cizeau, P., Bouchaud, J.P., Potters, M.: Noise dressing of financial correlation matrices. In: Physical Review Letters, vol. 83(7), pp. 1467 (1999)

Utsugi, A., Ino, K., Oshikawa, M.; Random matrix theory analysis of cross correlations in financial markets. In: Physical Review E, vol. 70(2), pp. 026110 (2004)

Potters, M., Bouchaud, J.P., Laloux, L.: Financial applications of random matrix theory: Old laces and new pieces (2005). ar**v preprint physics/0507111

Livan, G., Alfarano, S., Scalas, E.: Fine structure of spectral properties for random correlation matrices: an application to financial markets. In: Physical Review E, vol. 84(1), pp. 016113 (2011)

MacMahon, M., Garlaschelli, D.: Community detection for correlation matrices. In: Physical Review X, vol. 5(11), pp. 021006 (2015)

Heimo, T., Kumpula, J.M., Kaski, K., Saramäki, J.: Detecting modules in dense weighted networks with the Potts method. In: Journal of Statistical Mechanics: Theory and Experiment, vol. 2008(08), pp. P08007 (2008)

Fenn, D.J., et al.: Dynamical clustering of exchange rates. In: Quantitative Finance, vol. 12(10), pp. 1493–1520 (2012)

Isogai, T.: Clustering of Japanese stock returns by recursive modularity optimization for efficient portfolio diversification. In: Journal of Complex Networks, vol. 2(4), pp. 557–584 (2014)

Chakraborty, A., Easwaran, S., Sinha, S.: Uncovering the hierarchical structure of the international Forex market by using similarity metric between the fluctuation distributions of currencies (2020). In: ar**v preprint ar**v:2005.02482

Blondel, V.D., Guillaume, J.L., Lambiotte, R., Lefebvre, E.: Fast unfolding of communities in large networks. In: Journal of statistical mechanics: theory and experiment, vol. 2008(10), pp. P10008 (2008)

Clauset, A., Newman, M.E., Moore, C.: Finding community structure in very large networks. In: Physical review E, vol. 70(6), pp. 066111 (2004)

Plerou, V., Gopikrishnan, P., Rosenow, B., Amaral, L.A.N., Stanley, H.E.: Universal and nonuniversal properties of cross correlations in financial time series. In: Physical Review Letters, vol. 83(7), pp. 1471 (1999)

Fortunato, S.: Community detection in graphs. In: Physics reports, vol. 486(3–5), pp. 75–174 (2010)

Plerou, V., Gopikrishnan, P., Rosenow, B., Amaral, L.A.N., Guhr, T., Stanley, H.E.: Random matrix approach to cross correlations in financial data. In: Physical Review E, vol. 65(6), pp. 066126 (2002)

Newman, M. E., Girvan, M.: Finding and evaluating community structure in networks. In: Physical Review E, vol. 9(2), pp. 026113 (2004)

Ni, H., Szpruch, L., Wiese, M., Liao, S., **ao, B.: Conditional sig-wasserstein GANs for time series generation (2020). In: ar**v preprint ar**v:2006.05421

Levin, D., Lyons, T., Ni, H.: Learning from the past, predicting the statistics for the future, learning an evolving system (2013). In: ar**v preprint ar**v:1309.0260

Chen, K.T.: Integration of paths–A faithful representation of paths by noncommutative formal power series. In: Transactions of the American Mathematical Society, vol. 89(2), pp. 395-407 (1958)

Lemercier, M., Salvi, C., Damoulas, T., Bonilla, E., Lyons, T.: Distribution regression for sequential data. In: In International Conference on Artificial Intelligence and Statistics, pp. 3754–3762. PMLR (2021)

Lyons, T., Ni, H.: Expected signature of Brownian motion up to the first exit time from a bounded domain. In: The Annals of Probability, vol. 43(5), pp. 2729–2762 (2015)

Chevyrev, I., Lyons, T.: Characteristic functions of measures on geometric rough paths. In: The Annals of Probability, vol. 44(6), pp. 4049–4082 (2016)

Chevyrev, I., Kormilitzin, A.: A primer on the signature method in machine learning (2016). In: ar**v preprint ar**v:1603.03788

S &P Global Homepage. https://www.spglobal.com

Acknowledgment

The authors were partially supported by the PRIN 2022 project “Multiscale Analysis of Human and Artificial Trajectories: Models and Applications”, funded by the European Union - Next Generation EU program (CUP: D53D23008790006).

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2024 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this paper

Cite this paper

Gregnanin, M., De Smedt, J., Gnecco, G., Parton, M. (2024). Signature-Based Community Detection for Time Series. In: Cherifi, H., Rocha, L.M., Cherifi, C., Donduran, M. (eds) Complex Networks & Their Applications XII. COMPLEX NETWORKS 2023. Studies in Computational Intelligence, vol 1142. Springer, Cham. https://doi.org/10.1007/978-3-031-53499-7_12

Download citation

DOI: https://doi.org/10.1007/978-3-031-53499-7_12

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-031-53498-0

Online ISBN: 978-3-031-53499-7

eBook Packages: EngineeringEngineering (R0)