Abstract

This chapter explores the future trends in the battery market and analyzes the mutual interdependence of market demands and technological advances. First, most recent market volume projections are summarized, and the related uncertainties are described. Next, the interaction of foreseeable developments in battery technologies and demand scenarios is discussed along most relevant battery use cases. It turns out that current KPI expectations on the demand side and projected KPI on the supply side do not fully coincide yet. However, the market introduction of novel cell chemistries as well as improvements in cell design, manufacturing processes, and advanced material recycling concepts bears large potential for improving the efficiency of the overall battery supply chain and reducing costs. This chapter concludes that technological research and development, collaboration within the battery industry, public funding, and a stringent strategic research agenda are essential to secure the accelerating market growth for batteries.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

The global battery market has been growing very dynamically since the beginning of the 2010s, with annual growth rates of more than 30%. According to data from Avicenne Pillot (2022), the market volume of the entire battery market in 2020 was USD 93 billion. Lead-acid batteries accounted for USD 37 billion of this, of which 414 GWh were produced in 2020. The production volume of Li-ion batteries was just over half that at 250 GWh. However, the market volume of Li-ion batteries was already USD 39 billion in 2020.

2 Market Outlook

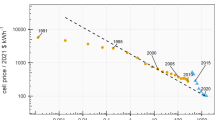

The market outlook is characterized by strong growth in the production of Li-ion batteries. Figure 7.1 shows the battery market development based on an assessment of market reports listed in Table 7.1. This growth is predominantly caused by the transition from internal combustion engine vehicles to battery-electric vehicles. The most likely growth path reaches a global production capacity of 3200 GWh/a in 2030, 7100 GWh/a in 2040, and 8900 GWh/a in 2050 [14].

Evaluation of the global battery market outlook [14]

In terms of regional breakdown of the global market, Asia, and China in particular, remains in the leading position. Based on the announced production capacities, a substantial change in regional market shares is not to be expected. The studies evaluated conclude that Europe will be able to cover a large part of its battery cell demand itself by 2030. Europe’s share of the global market will be 16% to 27% in 2030, depending on the assumptions applied. Due to the multitude of influencing factors, there is a great degree of uncertainty in this result.

In the decade from 2020 to 2030, the compound annual growth rate (CAGR) of the global market is projected to be 26% [14]. This rapid growth provides a good market entry opportunity for many new companies. As market diffusion of battery technology continues, the CAGR will drop to single digits in the following decade from 2030 to 2040. This will start a market consolidation phase which many of the new companies will not survive. The unsuccessful companies will be bought up by the better performing ones. Therefore, an aggressive growth strategy is necessary to survive in the mass market. In the second half of the 2020s, companies will need to secure significant market share and strategic alliances with automakers to survive in the long term. This conflicts with the limited experience of European and North American start-ups in particular. It will be a matter of not only scaling quickly but also learning more efficiently and faster than established companies that have been active in the market for years. Another possible strategy is specialization. By building up know-how and serving the needs of a smaller market segment, a technological advantage over competing companies can be achieved. This approach can enable survival with lower revenues compared to the mass market, but possibly more attractive margins.

The Li-ion battery market projection in Fig. 7.1 shows an assessment of 25 market development scenarios from 18 market reports. The market projections are classified into maximum, minimum, and realistic development paths depending on the assumptions on which they are based. The maximum scenarios are mostly based on the expansion targets announced by battery manufacturers. However, it can be assumed that not all of the announced battery production capacities will actually be created. Some of the players on the market today will not be able to survive and will withdraw their announcements. The minimum scenarios are mostly based on regulatory requirements. Particularly in the vehicle sector, many countries have already passed resolutions to phase out the internal combustion engine. One example of this is the CO2 fleet limits for passenger cars and light commercial vehicles that apply in the European Union [6, 7]. The minimum scenarios use these regulatory requirements as a basic assumption for estimating the expected market diffusion. The realistic scenarios are based on the historically observable market diffusion of battery technology.

Battery-electric passenger cars will be by far the most important market segment. Other, much smaller, market segments are commercial vehicles, stationary power storage, consumer electronics, power tools, and similar. Projections for the marine, aviation, and stationary power storage market segments are subject to the greatest uncertainties. Stationary power storage in particular has less limiting requirements for KPIs such as energy or power density neither gravimetric nor volumetric. This allows significantly more freedom in the choice of cell chemistry. One example of new battery chemistries with disruptive potential is sodium ion batteries. It is likely that this battery technology will capture a significant portion of the market volume outlined in Fig. 7.1. The properties of sodium ion batteries make them suitable for use cases that do not necessarily require high energy densities. However, manufacturers are also considering putting sodium ion batteries in vehicles with a range of up to 400 km in the future [3]. Breakthroughs in the industrialization of such cheaper batteries for stationary electricity storage can lead to significantly accelerated market diffusion. Nevertheless, even in this case, passenger cars would be expected to form the largest market segment.

The actual development of the battery market is difficult to estimate because it depends on a variety of influencing factors. The most probable path indicated in Fig. 7.1 reflects the mean value of the realistic scenarios. Realistic scenarios are considered to be those that make probable assumptions for the future impact of key influencing factors while weighing up various options. The consistent scenario descriptions resulting from this approach allow a projection for the future development of the battery market based on the state of knowledge in 2022. The real development of the battery market can deviate considerably from the most probable path. The following developments can lead to a positive deviation [14]:

-

Realization of all announced projects: The construction, commissioning, and ramp-up of battery factories are a complex task that poses considerable challenges, especially for start-up companies. The supply of raw materials, active materials, and components must also be ensured. It is therefore to be expected that not all announced production capacities will actually be built, commissioned, and fully utilized. Time delays also have a negative impact on the availability of production capacities. If these assumptions are not correct and the production capacities are actually realized as announced, the market development will shift into the area of maximum scenarios.

-

Accelerated demand growth: The realistic scenarios are based on the established regulatory framework. In the past, it was observed that the speed of market diffusion of new technologies has been increasing. Accordingly, it is possible that the market for batteries, especially in the automotive segment, could grow much faster than previously assumed.

-

Faster battery cost degression: With every battery produced, the knowledge about possible cost savings increases. Accordingly, the realistic scenarios extrapolate the future development of battery costs in line with the observed learning curve. New technical developments, for example, in production technology or through the introduction of cheaper battery cell chemistries, can accelerate the cost degression. Accordingly, a new market equilibrium would be expected to emerge resulting in a larger battery market volume.

-

Political support measures: Political measures can have a significant impact on the development of the battery market. The realistic scenarios are based on a business as usual assumption derived from the current and expected political framework conditions. More ambitious policies and actual compliance with the 1.5 °C target of the Paris climate agreement would shift the market development into the range of the maximum scenarios.

However, there are also a number of factors that can have a negative impact on the development of the battery market:

-

Upstream supply bottlenecks: The rapid growth of battery production capacities requires an equally rapid growth of upstream supply chains. Capacities along the entire supply chain must be ramped up in parallel. However, especially in the commodity sector, scaling up capacities is much more time-consuming (5–10 years) than building battery factories (2–4 years). Therefore, realistic scenarios assume that not all announced battery production capacities will actually be built. If significantly greater challenges arise in the development of upstream supply chains than expected today, this will have a negative impact on the development of the battery market. Influencing factors that are difficult to assess are the actions of governments in local protests against mining projects and the discovery of new raw material deposits.

-

(Trade) conflicts: International trade went into crisis as early as the 2010s, triggered by trade disputes between the USA and China. Russia’s invasion of Ukraine and the subsequent sanctions also have an impact on the battery industry, since Russia is a major nickel supplier with a global market share of slightly less than 10%. Such conflicts can therefore have a significant impact on the development of the battery industry. However, they are difficult to predict. Even more difficult to assess are their consequences. New conflicts and a further acceleration of the economic decoupling between the USA, Europe, and China can lead to problems along the supply chains with negative effects on the development of the battery market.

-

Shortage of skilled labor: Many thousands of skilled workers are needed to build up the battery industry and its supplier industries. These workers must be trained and educated. This is a major task that requires the cooperation of the governments, industry, and educational institutions. However, the battery industry competes with other emerging industries for talents. This is further exacerbated by the demographic trends in major battery producing countries. However, there is an opportunity for the battery industry to tap into skilled labor that is being laid off in the production of internal combustion engines. Advances in automation can also further reduce labor intensity. If the demand for skilled labor cannot be met, delays are to be expected, which will shift market development into the realm of the minimum scenarios.

-

Economic slowdown: A general economic slowdown is likely to result in restrained consumer spending and thus reduced demand for batteries. Recessions are expected and occur at regular intervals. The realistic scenarios continue the patterns observed in the past. If instead a prolonged stagnation phase or even a depression occurs, this will lead to a slower development of the battery market.

The market reports evaluated in Fig. 7.1 are listed in Table 7.1 together with additional information on the level of detail of those reports. Most of the reports consider the world market in aggregated form. Some break down the market into individual regions or countries. The table also shows the period covered by the reports. Few reports make statements beyond 2030; as such, long-term projections are subject to great uncertainty. The year in which the publication appeared is also indicated.

3 Market Entry of New Battery Technologies

The fundamental challenge of the future battery market lies in the mutual interdependence of market demands and technological advances. The advancement of battery application in various sectors (especially in aviation and medical devices) requires a market maturity of high-performance battery solutions, while in turn technological development progress is—at least partially—determined by market potential. This section hence provides an outlook on foreseeable developments in battery technologies (not limited to cell chemistry but including management systems and further components) and how their market introduction might interact with demand scenarios in various segments.

KPIs play a crucial role in bridging the gap between market assessments and technological outlooks by defining the most important characteristics of a battery system with respect to their applicability. They serve as a measure of “how a battery can be used” (for market scenarios) as well as a guideline for “what a battery can provide” (in technology roadmaps). Our analysis will hence focus on current definitions of and trends in KPIs.

This section is structured as follows: we will first give a short overview of KPI target values for batteries on an international level. We will then discuss KPI trends in relation to both battery market segments and technologies. Finally, we derive conclusions for future market developments on the background of current research trends.

4 Overview of Target KPIs for Batteries

The set of KPIs for a particular battery application defines the main properties of battery performance in the respective application. It typically encompasses a wide range of technical parameters as well as cost parameters. For the sake of our analysis, we will mainly focus on the KPIs used in the most recent battery Strategic Research and Innovation Agenda (SRIA) [2]:

-

Gravimetric and volumetric energy density at cell level (Wh per kg and Wh/l, resp.)

-

Power density at cell level (W per kg and W/l, resp.)

-

Cycle life (for high-capacity and high voltage applications, resp.)

-

Cost at pack level (€ per kWh).

Besides of upcoming improvements of lithium-ion-based cell chemistry, SRIA provides KPI estimates for so-called “beyond lithium” approaches based on natrium ion and metal-air concepts. Another stream of innovation is the concept of solid-state batteries (SSBs) with polymer electrolytes. KPI estimates are taken from a recent report by the Fraunhofer ISI [12].

With the advancement and market introduction of new cell technologies, significant improvements in all KPIs can be expected (see Table 7.2), although the respective year of market availability bears uncertainty. For example, assuming the availability of systems with a lifetime of more than 6000 cycles in the year 2030 and over 15,000 cycles in the years after is well reasonable. The reader should keep in mind though that these numbers represent goals related to ongoing or foreseeable developments until the year 2030 rather than safe forecasts. However, a recent overview [15] of manufacturers announcements indicates an earlier market upscaling of sodium ion batteries than expected by SRIA.

5 KPI Trends in Relation to Both Battery Market Segments and Technologies

The next step in the analysis is to summarize current expectations for particular KPI levels from the demand/application perspective and compare them to the above results. For the purpose of our analysis, we aggregate market subsegments up to a reasonable degree and omit niche applications with relatively small market sizes. The results of the comparison are summarized in Table 7.3.

A differentiated picture emerges in the comparison of KPI requirements in different market sectors with current KPI projections of various battery technologies. For large market segments, esp. light- to heavy-duty vehicles, the needs on the demand side and the projections for generation 4–5 lithium-ion batteries on the supply side are in fair agreement. However, further research is needed to satisfy the needs of smaller segments such as airborne transport.

Light-duty battery-electric vehicles for passengers are the largest market segment within the mobility sector. However, the KPI requirements of this segment cannot fully be met by generation 3 Li-ion batteries (1000 W/kg/2.200 W/l of power density in 2030). The same holds for plug-in hybrid electric vehicles. While their future market share is significantly smaller than for BEVs, they still constitute a demand of over 100 GWh [2] of battery capacity in the year 2030. Market maturity of generation 4 and 5 solutions improves the situation, while the power density remains a challenge.

Sodium (Na) ion-based systems are an option to satisfy the cycle life needs of medium to heavy-duty BEV applications (up to 6000 cycles) in the near future. The market introduction of these systems, expected to allow for a lifetime of over 15,000 cycles, is highly desirable to support a large-scale electrification of road freight transport. Likewise, expectations for cycle lifetime in stationary applications can—according to current projections—only be met by Na-ion systems. The power density projections for Na-ion systems (500 Wh/l) do not satisfy the requirements of stationary applications yet.

Off-road mobile machinery (up to 30 GWh per year in the year 2030), often characterized by continuous operation and robustness, requires large battery systems of up to 1000 kWh in size, optimized for a high energy (rather than power) density and outstanding lifetime requirements of up to 6000 cycles. Similarly, most waterborne transport applications (approx. 4 GWh/a in 2030) require even larger scales (up to several hundreds of MWh) and lifetimes (over 10,000 cycles). The latter requirement can neither be met with generation 3–5 battery concepts for mobility applications nor with metal-air systems. Li-ion batteries for stationary storage applications but also Na-ion systems would meet the cycle lifetime requirements but not the energy density demands. Improved solid-state batteries with polymer electrolytes might provide the power density required in these market segments by 2030 [12].

To conclude, while the technological development of batteries achieved remarkable results, solutions beyond current Li-ion batteries are needed to enable large-scale mobility and stationary applications. Particularly, power density levels beyond those of the coming Li-ion battery generations for road vehicle applications and improved cycle lifetimes for marine/aviation mobility and stationary applications are desirable. While sodium ion battery technologies are a promising option to allow for the high cycle lifetimes needed in most airborne and waterborne transport applications, energy density needs to improve to fully match the requirements of current aircrafts and long-distance vessels for a full electric operation. A mature market battery solution for the electrification of maritime and particularly airborne transportation might have a high symbolic value, beyond its limited market size and relatively modest contribution to current greenhouse gas emissions.

6 Current Research Trends and Conclusions for Future Market Developments

Current challenges in battery research and development span over the whole range of the battery ecosystem. The European Battery Partnership defines in its recent Strategic Research and Innovation Report six focus areas to support the development and market introduction of future battery technologies along the value chain: Raw Materials and Recycling, Advanced Materials and Manufacturing, Battery End Uses and Operations, Crosscutting Topic Safety, Crosscutting Topic Sustainability, and Coordination [2]. The report outlines strategic actions and a timeline of Technology Readiness Level (TRL) estimates in each area. The main trends and TRL projections in the areas of materials and manufacturing are summarized in Fig. 7.2.

7 Lithium-Ion Batteries

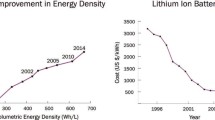

Innovative cell chemistries are catching up, but the current Li-ion battery will most probably remain the dominating battery type until 2030 due to successful market uptake and an established industrial value chain. The Li-ion battery concept is subject to continuous improvement and still bears potential for optimization. Current research focuses on improving the energy density while delivering on the other application relevant KPIs [1].

-

Intensive research is being carried out into nickel-rich NMC materials on the cathode side. Increasing the nickel content increases the specific capacity while reducing the cobalt content. Suitable composites are required to assure a high cycle stability. Nickel-rich 811-NMC cathodes are close to market launch.

-

On the anode side, research aims at increasing the silicon content of graphite electrodes (up to 10% Si/SiOx in generation 3) and thus the specific capacity without large loss of cycle stability.

-

Research on electrolytes focuses on compatibility with the electrode by develo** additives for organic liquid electrolytes and on solid electrolytes, to improve battery safety and render the use of metallic lithium anodes possible.

-

Coated separator membranes improve lifetime, temperature tolerance, and safety properties of batteries, e.g., through hydrogen fluoride absorbing ceramic particles. Extra costs for coating need to be compensated for by optimizing the manufacturing process.

8 Innovative Cell Chemistries

Substantial improvements of battery KPIs can be expected from so-called post-lithium-ion batteries. Most technologies have a high theoretical energy density. A variety of challenges still need to be overcome before market maturity can be achieved.

-

Major progress in solid-state batteries (SSBs) with polymer electrolytes is expected in the coming years, bearing large potential to fulfill energy density KPIs in mobility applications [12].

-

The lithium solid-state battery logically connects to the Li-ion battery. The application of solid electrolytes, in the form of ceramics, polymers, or hybrid, allows for the use of metallic lithium in cell chemistry.

-

Na-ion and Ka-ion batteries follow a similar operating principle as Li-ion batteries but bear the advantage of less raw material scarcity compared to lithium. Due to the larger ion radius and lower redox potential, lower energy densities are expected for these two technologies. Na-ion batteries have already entered the market but fill only a small market niche for stationary storage so far due to high costs.

-

The Zn-O2 battery (as an example of metal air batteries) has already reached technological maturity. However, the energy density is still far below the predicted energy density, making this system mostly suitable for stationary applications. Improving reversibility and thus cycle stability remains a challenge.

-

Redox flow batteries, e.g., based on vanadium, potentially allow for high cycle stability (>10,000 cycles) but have only a very low energy density.

9 Cell Design and Manufacturing Processes

Next to advanced material development, innovations in cell design and manufacturing processes provide chances especially for cost reductions. Trends in this area are the following:

Ongoing improvements in particular steps of the manufacturing process contribute to production efficiency. Prominent examples are 3D printing (allowing for individual cell designs), 3D inkjet processes (facilitating the production of anodes and cathodes), selective laser melting (SLM, enabling complex filigree geometries, e.g., in electrode production), and selective laser sintering (SLS, saving additional assembly steps).

Advanced environmentally sustainable processing techniques for Li-ion batteries (denoted as “Step 2 Advanced Cell Manufacturing Processes” in the SRIA report) will become mature in the second half of the decade, with positive effects on the environmental footprint of battery production, in particular energy efficiency (and, hence, costs). First improvements on coating processes are expected already by 2025. The expected impact on KPIs is a 20% cost reduction, and carbon intensity might drop by 25% [2].

Progress in digitalization improves testing and manufacturing processes in the second half of the decade. A major role plays the development of data-driven or physics-driven so-called digital twins—an advanced method for monitoring and managing complex battery systems [10]. A 25% reduction in energy consumption and lower capital costs of manufacturing processes can be expected. The integration of smart functionalities in battery cells allows for improved performance, reliability, and lifetime of 20% and more [2].

10 Battery Systems and End Use

Manufacturing is not the end of the process to ensure a large-scale market uptake of novel battery technologies in mobility and stationary applications. Improvements to the level of battery systems and end use are important to ensure high performance and safety. Current trends focus on improved safety (e.g., Battery4Europe defines the action item to introduce safe-by-design solutions by 2028) [2]; optimized battery management systems allow for accurate and robust determination and active control of cell states (e.g., current of individual cells), improved balancing schemes, and error diagnostics [9].

11 Raw Materials, Recycling, and Sustainability

Recent supply chain disruptions raised concerns on the availability and costs of raw materials in battery production. A recent report by the IEA provides an overview of current trends and challenges in battery supply chains [8]. The stability of the supply chain depends on a reliable supply of scarce materials. Many of them, most prominently lithium, are limited to a few production sites and suppliers. On this background, measures to improve the resilience of the supply chain are highly desirable:

-

Regional diversification of material sources and suppliers.

-

Improving social sustainability standards of material suppliers, not only as an ethical necessity but also as an essential contribution to supply chain resilience.

-

Improved recycling processes and additional measures for supply chain efficiency, such as tracing and labeling procedures. For example, the Battery4Europe network defines the action item to develop a tracing and labeling scheme over the full life cycle by 2028 [2]. Also, the concept of a “digital battery passport” receives growing attention [5].

Recycling plays a crucial role in reducing material scarcity and the ecological footprint of batteries. With growing battery production, a massive increase in recycling volume can be foreseen. Recent estimates of the volume of lithium-ion batteries components in Europe amount to 230 kilotons per year in 2030 and about 1500 kilotons per year in 2040 [11].

Current recycling approaches suffer from the fact that production processes do not take end of life treatment into account, so that huge efforts are required for the separation of materials. Besides direct mechanical separation, pyrometallurgical and hydrometallurgical methods are currently applied. Pyrometallurgical methods require substantial energy and material input for chemical calcination and combustion. Hydrometallurgical approaches are more complex and require less energy but use large amounts of toxic substances and require water purification. Both result in high costs and a low material recovery rate. The savings achieved by using recycled material compared to never used material is currently in the range − 5 to +20% [13]. A ready-for-recycling approach in cell design and battery pack assembly is hence the most effective action in this field.

More generally, the environmental sustainability of batteries receives growing awareness. For example, water use of mining is a serious concern in lithium mining regions such as Chile [4]. Due to current uncertainty in energy costs, substantial progress in material recycling and efficient production processes is of vital interest for the battery industry and not only an environmental concern anymore. The development and introduction of sustainability standards and regulations clearly contributes to improved material supply security and the resilience of manufacturing and distribution processes. The widespread implementation of circular designs in industry can be expected in the second half of this decade.

12 Conclusions for Future Market Developments

The overview of current research and development trends leads to the following conclusions for future market developments:

-

1.

Significant improvements in Li-ion batteries can be expected by 2030. According to the above analysis of KPI needs in various applications, post-generation 3 systems can contribute to future market maturity of light- and medium to heavy-duty vehicles in road transportation.

-

2.

Stationary applications and air/marine mobility would benefit from further efforts to improve cycle lifetimes of Li-ion batteries, production ramp-up of Na-ion batteries, and market introduction of improved solid-state batteries.

-

3.

The main application of Na-ion, metal air, and redox flow batteries is currently expected in stationary applications due to their relatively low energy density. As discussed above, their high cycle lifetime might be beneficial in some mobility applications, too. With growing demand for electricity storage, the market share of these innovative concepts will increase substantially, bearing the potential for cost decreases from economies of scale.

-

4.

Improvements in cell design and manufacturing processes as well as advanced material recycling concepts bear a large potential to improve the efficiency of the overall battery supply chain. Substantial cost reductions can be expected, although there is hardly any reliable estimate for the total reduction potential.

-

5.

Growing awareness of risks for supply chain resilience and environmental footprint initiates a trend toward a more circular, diversified, and sustainable approach of the battery supply chain. From a market perspective, this trend translates into improvements of supply and cost stability.

-

6.

Enforced technological research and development are inevitable to secure the accelerating market growth for batteries and the expectations for future cost decreases. Collaboration within the battery industry, public funding, and a stringent strategic research agenda are essential to achieve this goal.

References

European Technology and Innovation Platform on Batteries: Strategic research agenda for batteries (2020) Online: https://www.era-min.eu/sites/default/files/docs/batteries_europe_strategic_resea.pdf

Batteries European Partnership Association (BEPA): Strategic Research & Innovation Agenda (2021) Online: https://bepassociation.eu/wp-content/uploads/2021/09/BATT4EU_reportA4_SRIA_V15_September.pdf

BatteriesNews (2022) Sodium-ion batteries expected in evs with ranges of up to 500 km, CATL Exec Says. 30 November 2022. Online: https://batteriesnews.com/sodium-ion-batteries-expected-evs-ranges-500-km-catl-exec-says/

Baum ZJ, Bird RE, **ang Y, Ma J (2022) Lithium-ion battery recycling─overview of techniques and trends. ACS Energy Lett 7(2):712–719. https://doi.org/10.1021/acsenergylett.1c02602

Berger K, Schöggl J-P, Rupert J, Baumgartner (2022) Digital battery passports to enable circular and sustainable value chains: conceptualization and use cases. Journal of Cleaner Production 353:131492, ISSN 0959-6526. https://doi.org/10.1016/j.jclepro.2022.131492

European Union (EU): Regulation (EU) 2019/631 of the European Parliament and of the Council of 17 April 2019 setting CO2 emission performance standards for new passenger cars and for new light commercial vehicles, and repealing Regulations (EC) No 443/2009 and (EU) No 510/2011. 2019. Online: https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX:32019R0631

European Union (EU): ‘Fit for 55’: council adopts regulation on CO2 emissions for new cars and vans. Press release 28 March 2023. Online: https://www.consilium.europa.eu/en/press/press-releases/2023/03/28/fit-for-55-council-adopts-regulation-on-co2-emissions-for-new-cars-and-vans/

International Energy Agency (IEA): Global Supply Chains of EV Batteries. Paris. 2022. Online: https://www.iea.org/reports/global-supply-chains-of-ev-batteries

Komsiyska L, Buchberger T, Diehl S, Ehrensberger M, Hanzl C, Hartmann C, Hölzle M, Kleiner J, Lewerenz M, Liebhart B, Schmid M, Schneider D, Speer S, Stöttner J, Terbrack C, Hinterberger M, Endisch C (2021) Critical review of intelligent battery systems: challenges, implementation, and potential for electric vehicles. Energies 14:5989. https://doi.org/10.3390/en14185989

Lamagna M, Groppi D, Nezhad MM, G. (2021) Piras: a comprehensive review on digital twins for smart energy management systems. Int J of Energy Prod & Mgmt 6(4):323–334. Online: https://elar.urfu.ru/bitstream/10995/106465/4/ijepm_2021_v6_4_01.pdf

Neef C, Schmaltz T, Thielmann A (2021) Recycling von Lithium-Ionen-Batterien: Chancen und Herausforderungen für den Maschinen- und Anlagenbau. C. Neef, T. Schmaltz, A. Thielmann. Online: https://www.isi.fraunhofer.de/content/dam/isi/dokumente/cct/2021/VDMA_Kurzstudie_Batterierecycling.pdf

Schmaltz T, Wicke T, Weymann L, Voß P, Neef C, Thielmann A. Solid-state battery roadmap 2035+. 2022. Online: https://www.isi.fraunhofer.de/content/dam/isi/dokumente/cct/2022/SSB_Roadmap.pdf

Thompson DL, Hartley JM, Lambert SM, Shiref M, Harper GDJ, Kendrick E, Anderson P, Ryder KS, Gaines L, Abbott AP (2020) The importance of design in lithium ion battery recycling – a critical review. Green Chem 22. Online: https://pubs.rsc.org/en/content/articlelanding/2020/gc/d0gc02745f

Vorholt F, Bünting A, Bechberger M. Market analysis Q4 2022 – Turbulent battery cell market. 2023. Online: https://www.ipcei-batteries.eu/fileadmin/Images/accompanying-research/publications/2023-02-BZF_Kurzinfo_Marktanalyse_Q4_22-ENG.pdf

Wunderlich-Pfeiffer F. Die Revolution der Natrium-Akkus wird absehbar. Press article. Golem.de. 12 October 2022. Online: https://www.golem.de/news/akkutechnik-die-revolution-der-natrium-akkus-wird-absehbar-2210-168344.html

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if changes were made.

The images or other third party material in this chapter are included in the chapter's Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter's Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2024 The Author(s)

About this chapter

Cite this chapter

Wolf, S., Lüken, M. (2024). Future Battery Market. In: Passerini, S., Barelli, L., Baumann, M., Peters, J., Weil, M. (eds) Emerging Battery Technologies to Boost the Clean Energy Transition. The Materials Research Society Series. Springer, Cham. https://doi.org/10.1007/978-3-031-48359-2_7

Download citation

DOI: https://doi.org/10.1007/978-3-031-48359-2_7

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-031-48358-5

Online ISBN: 978-3-031-48359-2

eBook Packages: Chemistry and Materials ScienceChemistry and Material Science (R0)