Abstract

Wheat, the most important food crop, can be stored for a much longer time than potato. It is ground and made into flour or pasta that can be turned into bread or a dish at any time. Potato is only storable for a limited period, so it floods the market at harvest. Major benefits of processing for growers include regulating the availability of markets and price through contracts, and the decrease in the number of consumers buying fresh tubers is compensated by processors buying raw material. Processors add value and employment and consumers are offered a wide array of affordable and convenient products. Large potato processing companies produce annual sustainability reports advocating measures for growers to spare the habitat, more efficient processes in factories, newer and healthier products and supporting communities. These are recorded and viewed in a theoretical triangulation from the angles of processors, and those trying to bend the rules. The industry, especially when expanding to new (develo**) markets, faces political, economic, social, technological, environmental and legal (PESTEL) issues that fluctuate according to the presence of a raw material base, competition and buying power and culture of the consumers.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Inception and research questions

Justification of a potato-specific approach

Besides the local eating culture that determines the choice of products, societal aspects of processing potato are its benefits, its sustainability and its setting in societies as perceived by the stakeholders, the participants in the supply chain of whom there are more than growers, processors and users. The reason to study potato instead of food processing in general are the following. Cereals, the main staples processed, are relatively low-tillage, low-input, low-risk, usually rainfed crops, with few specifications, which upon harvest are collected by buyers in silos where they store the produce for up to some years without refrigeration. Before processing, the produce is hauled to mills by boat, train or lorry. Upon milling, the flour is distributed as raw material to an extensive network of outlets: bakeries that sell directly to their customers, retail and food service. The market is mature and evolves mainly along the lines of population development. Bread making is over 10,000 years old (Arranz-Otaegui et al. 2018) whereas potato processing at an industrial scale only took off in the mid last century (Survey 1, Haverkort et al. 2022a). Contrary to potato that is bought by users in kitchens as an untreated harvested “raw material”, cooks only sparsely buy grains of wheat for salads, popcorn or brown rice.

The potato crop, however, requires the best, light, preferably stoneless soils with a deep rooting zone. Crops are planted with a few tons per hectare of costly seed potatoes; crops destined for processing are irrigated in most instances (from a low percentage in Belgium, about half of the crops in the Netherlands, the UK and Eastern Canada, to all crops in the rest of the Americas and Africa and the winter crops in subtropical climates) and they are intensely protected against pests and diseases. Soil is moved several times as deep tilling is required to create a seed bed, planting is in shallow furrows and hilling is done in a few operations. At harvest, many hundreds of tons of soil are lifted to retrieve the tubers that need to be stored under ventilated and refrigerated conditions for a maximum period of eleven months while sprouting is controlled chemically. Adverse weather conditions (heat, drought) reduce yield and processing quality. For growers, it is an expensive, risky crop producing a produce with many specifications for which they remain responsible until the tubers are collected by the processing plant of which there are only one or two near enough to deliver to. Potato is ground for starch production and peeled and cut for other products comparable to milling of grains but the potato processors are, contrary to cereal millers, also responsible for making the final product that, with the exception of starch, is only storable for a limited period and the bulk of it is frozen or stored chilled for a limited period. Processing potato is a rapidly expanding industry venturing into new countries and regions constantly, meeting new societal demands. The link between raw material, the tubers to be harvested and the processors is a strong one as was outlined in Surveys 2 and 3 (Haverkort et al. 2022b, 2022c). All these factors make potato processing of more relevance for communities involved than for cereals. Once this is observed, a potato-specific approach is defensible.

Research questions

In the light of the special agricultural and industrial situation of potato and its setting (its place in society, embedment in its social surroundings) the following research questions arise.

Potato processing is a well-established industry in the major producing well-developed markets. It has not yet been exhaustively investigated and determined what the advantages are for growers, processors and users of potato products over users having access to fresh tubers. The impression exists that the trade is thriving and that the interest of people is increasing but can driving forces, including sourcing further afield, be elucidated and analysed?

To sustain processing in the future, sustainability measures such as increasing efficiencies (Haverkort et al. 2022c) are being taken. Is it possible to systematically itemize which measures growers, processors and consumers are taking or need to take to assure the future for the market and to learn who else takes part in the steering, carrying out and monitoring of sustainability-related issues? How can stakeholders when they are targets of the measures, or advocates or opponents, influence the type, size and relevance of interventions?

Besides sustainability, the industry in each societal setting (background) is co** with governmental policies, with the national or regional economic situation, with how society is organized and with how opinions of the people come about, which are the technological opportunities and aspirations and which laws and regulations are in place and how compliance is monitored and enforced. How can the setting of a processing industry in its social surroundings be systematically and scientifically researched?; and what are the wishes of the three central parties (growers, processors and diverse users) and the role of breeders, and makers of policies and laws?

The subjects mentioned previously are likely to differ in the various stages of availability and use of products and of the industry itself, it being a cottage industry, upcoming or operating in a well-developed almost satisfied market. What settings exist where processing at a cottage or corporate level takes place with and without available local raw material and with or without an affluent society able to afford to buy products. When establishing potato processing and to continue current operations, which hurdles are needed to be taken regarding national government policies, local economies, societal conditions, levels and need of technology and environmental and legal concerns? By what means can it be described how these markets look like and which societal issues the industry faces if needing to expand there?

Research approach

The potato processing ontology covers a large super-domain with domains of each of the actors: growers of tubers specifically for a product, processors manufacturing products and cooks using them to make dishes and consumers eating dishes. There are also domains of things: products, processes and operations and of community matters treated in this survey: benefits, sustainability and social surroundings. In a Four-Tier Analysis, (1) the domains are briefly described and delimited and (2) condensed in tables describing classes with their attributes. Not all attributes apply to the same extent to all classes so (3) they are awarded a quantitative score from 1 (hardly applies) to 5 (fully applies) yielding a heatmap that finally, (4) through a dendrogram, produces a hierarchical clustering of classes and attributes. Of the latter, just one example is presented here.

Domain of Benefits of Processing

Formulation of the Benefits Domain

Cooks buying products rather than fresh tubers has several consequences. In the kitchen, it affects the time needed for cooking, efforts and water and energy needed in kitchen operations. Saving time is only one aspect of convenience. Not having to think about the composition and ingredients and having to buy them are other aspects and so are reduced costs and losses. For manufacturers, it is an opportunity to add value, and for growers, it offers additional growing and outlet opportunities. For all parties: processed products in general have a longer storage time span than fresh tubers so they even out the prices by reducing the peak at harvest.

Condensation of the Benefits Domain

The most important reasons to make use of manufactured potato products are the satisfaction of them and the time saved in preparing a meal, no need to wash, peel, cut and par-fry purchased tubers when employing frozen or chilled French fries and not having to do tedious tasks according to some such as peeling and waiting for a process (cooking) to finish. In restaurants where all time dedicated to processes has to be accounted for, buying factory-processed food there in large quantities and partly automated is at a fraction of costs compared to making it there from fresh tubers. Cooks, however, may have other culinary considerations to start with fresh tubers rather than products. Opening a bag of chips of 100 g takes one second, preparing them in the kitchen takes about 30 min. Especially the frying procedures in several batches and monitoring the process is time consuming. Then, there is time involved in buying the tubers and in doing the dishes. Some dishes are hardly made in kitchens but only purchased such as most formed ones, croquettes for instance. Health reasons are other considerations for some consumers wary of substances such as gluten, glycoalkaloids and acrylamide. A main advantage of using manufactured processed food is also the wide choice; especially in areas where the crop is not grown and tubers not sold, access to products is indispensable. Besides convenience, other aspects play a societal role that are adventageous for processed potato products. In a factory, there is little waste. Peels are made into feed, peeling there is done by steam with minimal losses whereas when peeling and trimming by a knife in a kitchen a considerable proportion of the tuber (20%; De Thouars 2018) is wasted. For abrasive peeling in factories, this is about 12% and weight loss with steam peeling is about 7% (Pelletier et al. 1964; Singh and Shukla 1995; Somsen 2004; De Thouars 2018). Using processed tubers reduces peel losses by 13%. When dosing needed amounts for a meal from a purchased wrap**, these are easily targetable compared with starting from fresh tubers, so this reduces the quantity of leftovers, hence waste and losses. Preparing a potato meal component in the kitchen is not a continuous process but comparable to processing a small batch. For such a small batch, specifically a pan and an amount of water or oil need to be heated and cooled without saving the energy for the next batch or using the energy for another process such as drying as happens in potato processing units. So, from the environmental point of view, using processed food in the kitchen is an advantage. For this very reason and because processors through contracts procure their fresh matter at a fraction of the prices that consumers pay, about 25–30% of the price, the costs of buying processed products is often lower than preparing at home when including the costs of energy and ingredients.

For consumers and the potato industry at large being able to process tubers has multiple advantages. Tubers under refrigerated conditions can be stored for not more than some 11 months (maximally some 10 months on average), and to avoid sprouting, chemical inhibitors (Paul et al. 2016) are applied. Chilled products under a controlled atmosphere can be stored for a few weeks, when pasteurized for a few months and when sterilized for a few years, frozen for 2 years and as a powder (starch, flour) for several years. Being able to store potato-derived products enables the industry to build up stocks when there is excess and to release to the market when there is a short supply. So, for growers who produce the tubers who have contracts with manufacturers, the benefit is in evening out fluctuations among years which also holds for the same reasons, besides increased prospects to make a range of food ingredients. For users, there is a benefit in being able to take a dose and leave the remainder in the freezer or box for an undetermined period, whereas before, they had to make sure the perishable tubers were used up in time. These are economic and efficiency benefits, but socioeconomic considerations also play a role such as assurance that production takes place in environmentally friendly conditions, that food is safe, produced organically if so desired devoid of synthetic agents and of genetic modification as examples.

The economic and environmental considerations of processing have several aspects. Tubers destined to be processed need to meet specifications to manufacture the final product. This avoids the transport of undesired tubers with aberrant sizes and with defects. Many finished products only contain a fraction of the amount of water in fresh tubers which also reduces the need for transport. Consumers replace fresh potato by its products which boosts the industry and also gives all cooks in a household more time to spend on income generation. Uneconomic peeling, washing, heating in small portions and not reusing the water and energy lead to sub-optimal use of resources and losses as in factories steam peeling is more economic and the peels are used as feed, while water and energy are reused. Manufacturing products from potato that usually are not made in the kitchen widens the range of dish and meal ingredients, snacks and the use as non-food (feed and industry). Modified starches are applied as additives in bakeries and extruded potato pellets provide an assortment of expanded snacks. Peels and rejected tubers, rejected tuber parts and intermediate or finished products are used as feed, raw for ruminants but cooked also for non-ruminant animals. So there is hardly any waste in the industry, whereas in kitchens, peels and unconsumed tubers are squandered since the collector of food waste as a feed with his horse and wain disappeared from the streets. Such considerations and more, especially economic reflections, are summarized in Table 1.

Quantification of the Benefits Domain

The advantages of processing in Table 1 are the attributes of the classes of potato products illustrated in Table 2. Most attributes are obvious but some need clarification. The market size of a product is not a benefit per se but a larger market share has a greater economic impact. Transport of raw material to the processing unit and finished product to the consumer is more beneficial for the environment and cost reduction when the distance is more favourable (shorter). Losses in handling and storage are considerable in chips production (stringent grading) so minimizing their losses is insubstantial but is substantial in starch production where handling and storage hardly play a role.

Minimizing losses in starch production on the other hand is quite substantial with skin and protein ending up as low-cost products (feed). The heatmap of Table 2 shows the lowest score for tubers and parts (cubes usually) that are cooked and dried in hot air. They need to be reconstituted and heated, have a small market share, need more energy for cooking and, in total, deliver the lowest advantage. They share such properties with the other dried products of which chuño has the advantage of short distance to processor and consumer as often these are the same individual. Chips have the highest score (3.9) with high values for employment, innovation (especially the expanded variants), variety of products (shape and flavourings) and water, energy and time saved. Starch production has a high total score with only low values for distance to client, usually non-food and food industry and the amount of water involved in washing the starch. Only a few products have such large market shares, in increasing order flakes, starch and chips with frozen French fries at the top that they have a regulating effect on prices and total potato production in a region. For the same reason that many products represent a small market, also maintaining tuber production in a country ends with a relatively low score.

The energy saved in preparation in kitchens is none (Table 2 red colour) for products that need to be reconstituted and boiled, similar to raw tubers. When the product contains gelatinized starch and only needs to be heated the amount of energy saved in the kitchen is moderate (yellow) and ready to eat or drink products need no energy at all (green). Saving water in the kitchen takes place when the tubers of the product have already been washed prior to processing, so chuño is the only exception. When no water is needed for cooking as this took place at the factory, then more water is saved, consequently saving water has the highest (4.0). Producing and processing tubers is a relatively labour-intensive economic activity. It takes more time to manage the crop from ploughing to harvest and handle the tubers post-harvest than is needed for cereals (Haverkort 2018). Also, the factory operations are more labour intensive than grinding wheat and baking bread. Consequently, creating employment has the second highest average.

Clustering of the benefits domain

The dendrogram in Table 3 does show a few clear clusters of the products. The top four products are related dry powders and pellets. Just below there is a group of formed frozen products with blanched chilled at some distance. At the bottom are the snacks grouped together. Extruded baked and fried products have been given identical weight to each attribute so are twins without any distance with distant chips in the same group. Frozen French fries do not belong to a particular cluster but there are a few more closely related twins such as gratin and rissole, raw and cooked freeze dried, formed from mash and shreds (croquettes and hash browns/rösti) and flakes and granulates.

Clustering the attributes reveals that a shorter distance from the processor to the user is not related to any other descriptor of benefit. Innovation and a variety of products are obviously linked and grouped with the other market-related attributes market size and price stability. The cluster in the middle consists of two twins energy need and convenience (rapid cooking costs less energy) and employment and water need: the less water is needed in the kitchen the more labour is needed in the processing plant. The five remaining attributes mainly concern the raw material: its bulkiness and transport and losses in handling and operations and storage of the tubers and products (Table 4).

Sustainability Domain

Formulation of the Sustainability Domain

This section discusses sustainability concerns of the potato processing industry. The three principle stakeholders are the partners in the supply chain: growers, processors and users but other interested parties have stakes as well. These are breeders of the varieties, the seed producers, retailers, food service, food industry, consumers, regulators of governments and certifying bodies. Some are lumped with adjacent participants, seed producers with growers and cooks with consumers as they are suspected to have the same interests. Making the Tables 5 and 6 was done through theoretical triangulation from the position of stakeholders being (1) targeted by sustainability measures and (2) stakeholders trying to disturb the measures for opportunistic reasons.

Reporting by the Industry and Compartmentalization

Over the recent years in the present century an increasing number of globally operating potato processing companies published sustainability reports, separate from their financial and human resource reports. These reports are more of interest for the potato industry than for most other ones because of the intricate continuity of breeding-seed production-tuber production-processing-chilled and cold distribution-cooking where in many products the original tuber structure (chips, French fries) is still visible. For wheat and corn, both ground and more anonymously disappearing into the food industry the links are much less clear, less interdependent hence less responsibility is felt for performance of the various parts of the chain. Tubers cannot be stored for a prolonged period so fine tuning of supply and demand is more important for this than for any other staple. Processing of tuber parts in the potato industry compared to working with powders (wheat and corn) is another distinct feature meriting its own approach to sustainability.

The processing industry of potato has in common with the other food processing industries the dealing with personnel such as training, fair payment and recruiting issues such as ethnicity, equity and gender. So, this not being potato specific is not treated here nor is charity and contribution to the welfare of communities considered except where explicitly potato production and/or processing features. The sustainability reports often are not annual but biennial or the first and last one dates from more than 10 years. Data were not retrieved triangularly but only through one single method: consulting and condensing the sustainability reports of the companies. These were Avebe (2020), Aviko (2020), Farm Frites (2020), Fritolay (2020), Pepsico (2020), Simplot (2020) and LambWeston (2020).

All companies in their sustainability reporting more or less follow the order of the production of raw material, processing in production plants, food quality and benefits for communities. Predominantly regarding sustainability, the efficient use of resources is considered, next reduction of emissions, then making safe and healthy food available, followed by community and shareholder values. In general most of the information regarding performance of sustainability through key performance indicators comes from the companies’ own sources that could not be verified through independent sources or agents. Data such as “20% less water used over the last 5 years” or a “2% increase of renewable electricity” presented as key performance indicators (KPI) lack coherence and checkability to be represented in a scientific work. The most important sustainability issue of a company is its competitiveness expressed as its profitability, the return on investment. The better it performs the longer it will be in business, and sustain. Such information, however, is not presented in the sustainability reports. The financial reports for owners of the companies, the shareholders, are more explicit but the following tables in this section also address this point.

Production of raw material

Regarding sustainability, there are four major concerns, the efficient use of resources, maintenance of these resources, emissions, and intelligence (information).

The principal resources used in the primary production of tubers are land, water, minerals, crop protection agents and propagation material. When managed more effectively, usually with the assistance of DSS (decision support systems) and breeding of tolerant and resistant varieties, their efficiency increases through a reduction of input and/or an increase in crop yield. This is treated extensively in Survey 3 (Haverkort et al. 2022c). The water use efficiency ameliorates with better soil structure, irrigation scheduling and distribution (drip versus rain gun). Resource conservation measures handle soil matters when its erosion decreases, its structure is improved with machinery less compacting the soil, with measures that increase the organic matter concentration and improve the water holding capacity and rooting depth. The reduction of emissions of chemicals and CO2 also aims at resource conservation by enhancing biodiversity and by mitigating climate change. Intelligence concerns monitoring pests and diseases and DSS-guided dose and timing assist in reducing amounts of biocides, water and fertilizers. The industry guides growers through science, demonstrations, training and monitors through certification schemes such as SAI-FSA and traces and tracks incoming lots of raw through GLOBALGAP certificates. A significant point not mentioned in the reports of the companies but essential for growers is their position in the market and their dependence on fluctuations. Their indicators are satisfaction with procurement expressed in guidance, price and continuation year to year. An unreliable raw material base is a hazard for sustained processing.

Processing

The equivalent of yield in tuber production is recovery in processing, also expressed as potato utilization: the quantity of finished product produced per ton of raw material. The highest value is achieved when less of the material ends up in the lower part of Moerman’s ladder (Aramyan and Valeva 2016 represent an adequate example) where food has the highest value, followed by feed, biobased materials, fuel and dumped in landfills even representing a negative value. Also recapturing of starch and minerals (struvite) contributes to recovery. Concerning processing operations, the foremost resource use efficiency to be improved is that of energy used for heating water and oil from fuel mostly, and from electricity for conveying and cooling. Re-use of heat from cooled steam for drying for instance assists in decarbonization and so does production of biogas from waste water and the use of electricity from renewable sources by placing solar panels over the purification basins. More efficient use of water in washing before and after peeling and blanching has high priority with enhanced cleaning and re-use. Re-use of carton packages and recyclable plastics helps reduce the environmental impact of wrap** and reduction of road kilometres is accomplished by shortening sourcing and distribution distances and transportation by trains and boats. Not mentioned in the sustainability reports of the companies but yet a significant issue when it comes to sustaining the business is the procurement of a steady flow of raw material at an attractive price ensured by long-term relationships with individual growers. Nor are profits mentioned, needed not only to outsmart competition but also to ensure sustained support from the owners.

Food Quality of Products

Food quality is considered a crucial sustainability matter, as safer, healthier and tastier and more convenient products ensure a greater and continuous market. So, a continuous flow of new products of which relatively recent innovations such as fried dough-based emoticons, street fries, higher fibre content and air-fryer ready products are examples. Others are healthier offerings some of which have less indulgence but more health consciousness appeal. Sustainability issues of the products regard the lowering of concentrations of ingredients considered unhealthy or undesired when eaten at relatively great quantities such as fat (striving for light) especially saturated fatty acids, salt and certain additives such as wheat flour in batter which renders the product not gluten free. Skin-on and thicker cuts products absorb less oil as they have less surface for oil to adhere to. Better informing the consumer is done by more extensive, informative and accurate labelling including the recently developed Nutri-Score (Julia et al. 2018). There are also claims that the ingredients are recognizable and respected, seemingly hidden signals that no synthetic chemicals (some E-numbers) nor products from genetically modified plants are deployed.

Serving the community

Some sustainability reports mention contributions to charity with funding, donating to food banks or volunteer’s time (Table 4). These are not potato specific and, like human resource issues, are generic for any industry, so not to be discussed here. Other relevant community-related subjects regard the raw material base, consumers and processing company strategy. Aiming for products for develo** markets that are distributed under ambient conditions (dried, powders, snacks) rather than cooled and chilled rather than frozen assists in making such products available for less well-off consumers not connected to the grid of cold chains or even to the electricity grid. Innovations specifically aimed at such markets with one-sided food like fortified powder as an ingredient for fufu in Africa is another class of sustainability measures. Using indigenous coloured tubers in the Andes serves both growers with an additional outlet and consumers with a new product to choose from. Investing in watershed management to replenish ground water levels is an illustration of serving growers. Societal issues directly regarding companies’ strategies are affairs around sudden changes like a pandemic, widespread climatic events and imposed taxes; slower develo** events are market penetration, saturation and altered preference stemming from population build up and fashions in food. These are only evaluated in Tables 5 and 6 where potato specific.

Quantification of the Sustainability Domain (1)

The class of sustainability indicators has four sub-classes (production of raw by growers, processing by manufacturers in factories, food quality, and serving the community) and each sub-class is supplied with instances taken from the sustainability reports. These are shown in Tables 5 and 6 and number 34 in total. Two types of attributes are distinguished, expressing two points of view. First, tabled is the degree to which stakeholders are targeted by the indicator, having to abide by them or benefit from them. Next, a second assessment with the degree they are able to bend the rules favouring short-term gain rather than long-term tenability. The attributes also concern several points of view of the stakeholders concerned. In the production of raw, these are potato breeders and growers. In processing and utilization these are the processors, traders (retail), food service, food industry and (cooks and) consumers. Not exclusively potato addressing stakeholders are regulators (policy and law makers) and certifying bodies such as GLOBALGAP and organic schemes for the production of tubers and a HACCP-based Food Safety Management System (FSSC ISO22000) for the industry.

Stakeholders targeted

Table 5 displays the heat map of the degree to which stakeholders are targeted by the sustainability measures of processors and their suppliers of tubers including breeders of varieties they are in close contact with to adjust or improve the processing quality of the tubers and their tolerance of biotic and abiotic factors and resistance to pests and diseases. All these properties favour the environment with higher recovery in factories and better use of resources on farms. The heatmap in Table 5 shows only green colours for growers of tubers for the attributes of the class “raw material production” and only green colours for the attributes of the classes “processing, food quality and community”. The 34 sustainability measures are specifically intended for these two target audiences so also reach the highest scores mean value 4.6 for the degree to which processors are targeted and 3.2 for the growers. The least targeted is the food industry deploying intermediate products as ingredients for whom mainly food safety and health is an issue. Although many measures are directed by regulators, especially around environmental and food safety they are only targeted there where actors comply with such directives. Food quality is the least concern of growers with the exception of food safety where they have to make sure that unwanted substances are absent (glass) or below acceptable levels (MRL). Breeders are more involved as some properties have to do with safety (level of glycoalkaloids), others with processing quality (dry matter concentration) and suitability for new products (roast baby potatoes). Of the 34 classes, food safety reaches the highest score with 4.2 points followed by respected ingredients (4.1) and the desire to be able to trace and track how food is established. All three stem from the concern that food should be safe. The lowest score received the pursuits of increased recovery and making a profit with new products; only the processors are targeted.

Clustering the classes as is done through the dendrogram (not shown) reveals two main clusters. In one, two sub-clusters are visible, one dealing with food safety and one with innovation. The rest illustrates a few twins, an obvious coherence between recovery and profits, between variety tolerance and climate change and resource use and renewable energy. The attributes make clear that regulators and certifying bodies are quiet and so are growers and processors at a larger distance from each other.

Stakeholders Obstructing the Rules

Quantification of the Sustainability Domain (2)

Sustainability efforts, as shown in the previous section, are targeting stakeholders, they can steer them but they can also ignore or even obstruct them when it prefers short-term advantage over long-term survival. It may be bending the rules a bit by exaggerating the performance of a variety by a breeder, by registering a lower dose of a crop protectant than actually applied, by a processor obscuring the presence of certain ingredients, a retailer refusing a new more environmentally friendly product for fear of scaring off clients, food services and industry for the same reasons. Consumers can buy at lower prices when taking home products without green labels. Policymakers can be too lenient to make laws or do not enforce them. The same holds for certifying agencies. The tendency to ignore is stronger for attributes that cannot be detected easily and, where the penalty of an offence does not outweigh the gain.

The heatmap with easiness to ignore sustainability measures by participants in the potato products supply chain is illustrated in Table 6. As in Table 5, the processors operating in all classes involved receive the most points and breeders operating in one class mainly and, with only a small number of classes, receive the fewest points. Processors are followed by retailers when it comes to obstructing ability.

Regarding the classes, no participant ventures to declare a product gluten-free while adding wheat flour on purpose, because detection would be certain; this explains the low score of 1 point for this aspect only. Low scores are measures of the processing company itself without involvement of other participants in the supply chain. Training growers and serving the community clearly illustrate this with about 1.4 points. High scores are given to measures that affect several stakeholders such as packing and supply chain information.

Processing Potato in its Surroundings

Domain of (Policy, Economy, Society, Technology, Environment and Legal) PESTEL Matters per Principal Actor

Formulation of the Domain: the PESTEL Approach

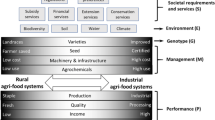

A societal interest-based interdisciplinary study is aimed at gaining insight and develo** a methodology from different disciplinary perspectives: on-farm production of potato tubers, the raw material, food processing technology, food science, environment and socio-economics. The analytical frame used here (PESTEL) allows the gathering of the various disciplines. The PESTEL approach among others is explained in B2U (2020) and the website of Pestelanalysis.com where it is combined with a SWOT (Strengths, Weaknesses, Opportunities and Threats) analysis per PESTEL element. Examples of its use are given by Nurmi and Niemelä (2018) and Roman (2015). The PESTEL approach analyses the external influences on processes and decisions to be taken whereas the SWOT analysis addresses both the internal (SW) and external (OT) influences. Potato products are brought about in Political, Economic, Social, Technological, Environmental and Legal surroundings. Politics among others deals with the protection of trade and promotion of production, Economics with value chains and consumer expenditure on food, Social aspects are for instance green production labels for farmers and convenience food for consumers, Technology concerns scale and innovation, Environment considers resource use and climate change and Legal aspects take into account human and environmental health. Table 7 exemplifies, with keywords, the kinds of issues that arise per group of actors that in subsequent tables are explored at greater length and for an array of actors that exist for the various markets.

Farmers are the first in the flow of material in the supply chain of potato products. The setting of the industry in its social surroundings is strongly determined by the farmers who cultivate and store raw material. Tuber production involves the resources labour, equipment, land, water, minerals and energy and is associated with the emission of nitrogen compounds and greenhouse gases. These are all expressed as unit per ton raw and vary with the system such as high and low input, corporate or family farming, organic or conventional, rainfed or irrigated. Processes also vary in resource use efficiency and losses (peel, defects) as depending on scale (cottage and industry) and method (dehydration, heating) all expressed in units per ton product. Performance of cultivation and processing further depends on the PESTEL elements Policies (trade, taxes, labour) and Legislation (food safety and Environmental requirements). Production ecology, value chain and use of resources among others are extensively described by (Haverkort 1990, 2018; Haverkort and Hillier 2011) as well as the influence of climate change on the potato supply chain (Haverkort and Verhagen 2008) and on production (Haverkort et al. 2013).

Processors in factories dehydrate tubers to mainly produce flour and starch, ingredients used by consumers, but to a greater extent used by manufacturers, to transform it into flour and starch-based derivates such as mash-based croquettes and pellet-based extruded products. Tubers peeled, cut, blanched and cooled provide convenient chilled food for households. Frying tuber cuts partially dehydrated yields French fries delivered frozen as meal component and sliced and fully dehydrated produce snacks as chips. History and development were described among others by (Woolfe 1987; Rana et al. 2017; Willard 1993). Of the PESTEL elements Technology (innovation, research and development) is most prominent, coupled with Economy (competition, pricing) and Environment (efficiency of use of resources).

Consumers are the last in the flow of material in the supply chain of potato products as food. With 400 million tons of Global production for 8 billion inhabitants, global availability of potato is about 50 kg per person per year. Actual consumption is less because about 10% is used as propagation material (seed tubers) to be planted and part goes to the starch industry for non-food applications. There is an increase in consumption in Asia and Africa and there was a decrease of freshly prepared tubers in the rest of the world, where processing took an important place. So, in monetary terms, consumer expenses on potato have increased relatedly. The contribution of potato and its products to the energy and protein balance in diets and health (Chandrasekara and Thamilini 2016) accordingly differs in the environments where the role of crop is that of food, cash or industrial crop, convenient or snack food. Besides the beneficial aspects of contribution to food availability and intake, it is consumed as a fried product and leads to obesity, especially by low-income consumers in high-income societies (Borch et al. 2016; Blakely 2019). Of the PESTEL elements, Economy (food affordability), Society (food quality, health) and Legal (compliance and food safety) are dominant matters for users in kitchens in houses, restaurants and institutions.

Disclaimer: the domains of PESTEL matter per principle actor and in diverse environments as approached here are delimited by the personal experience and vision of the first author through methodological triangulation with reference to other research and literature de-emphasized and systematic empirical research lacking.

PESTEL matters per principle actor

Farmer

Important policy decisions that influence growers of tubers destined for the processing industry are imports of tubers for seed production or raw material and the import licences and tariffs that apply to finished products. Some countries prohibit the imports of seed potatoes for plant health and competition reasons although more suitable varieties are required by the industry. Farmers and processors have fear for imports at low tariffs. Governments decide on the type of crop protectant agents that are allowed by farmers and occasionally crucial agents to control late blight or sprouting are forbidden with substantial consequences for the industry. Subsidies on inputs such as free water and electricity, low taxes and a financial allowance per unit farm area strongly influence profitability and financial sustainability. The costs of inputs such as nitrogen fertilizers, following energy prices (Economy matter) and partly determined by taxes and subsidies (Policy matter) fluctuate. Yields and prices of the raw material also fluctuate due to variation in supply because of weather events (Environment) or overproduction (Economy). Access to credit from banks varies among countries, types of farmers and of banks and changes with time as a function of global crises. Socio-economic factors influencing decisions to grow the crop are farm scale, too small does not attract attention of a processor and does not allow mechanization. The sourcing range of a factory roughly speaking is 100 km for starch, 250 to 300 km for tubers destined for making French fries and even up to 1000 km for chips tubers. Urbanization has two repercussions: it takes up arable land and it removes population (workers) from the rural area. Technological developments are mechanization with ever larger machinery, the use of decision support systems based on information from crop, weather and soil to plant, irrigate, fertilize and protect the crops. Besides automation regulating time and dose, precision farming also allocates inputs to parts of the according to sensed requirements. Environmental concerns of growers concern daily weather and the effects of climate change with rising temperatures, and increasing erratic temperature and water events. Legal obligations are restrictions on the use of certain inputs, information supply on the use of inputs to institutions of governments and certifiers and compliances with tax, food safety and environmental laws.

Processor

Policymakers make it of interest for potato processors to establish a factory, as they provide a sales market for growers, employment for workers and taxes for themselves. Through tax tariffs they make it attractive or not, to import raw material which is valuable for processors when local raw is more expensive. Also, export of finished products (export taxes or subsidies) and import (trade barriers or high tariffs) determine the business climate to a great extent. The more corruption exists by officials turning a blind eye, the more processors hesitate to enter a country at all. A major determinant of profit is the presence of competition both for procuring raw material that hinders processors of chips and French fries to the same degree, but not for sales as they supply different markets. The price of raw is of major influence as well. The bulk of factories of frozen products are in the regions with the cheapest raw: North West Europe and East and West North of the USA and the South of Canada. Here the resource use efficiencies are highest. Plants of chips are in the vicinity of large cities and the price of raw is less important because the on-farm potato part in the product is marginal because costs of transport, oil and packaging (bags, cartons) are considerable. Labour costs also determine profitability but there is a level playing field because they are in general in regions with fairly well-remunerated employees as processing food is not easily put at distance in low-income countries. Another social aspect is the outlet of the products, in bulk to the food or non-food industry, in large package to the food service or via retail to the consumers. The aspiration to recycle and optimize the use of resources also has repercussions on processors’ behaviour. Technical challenges are innovations in operations and equipment and their automation aimed at the possibility to increase recovery, make new products and allow automation and reduce the need for labour. Environmental concerns were addressed in the section on sustainability in this survey. Legal matters regard food safety (abide by HACCP: Hazard Analysis at Critical Control Points) and safety of workers, two pre-competitive issues, but checking and enforcement are not the same in each environment.

User

Users of potato products expect policymakers to make sure the national food laws comply with those of the Codex Alimentarius and that proper information flows (tracing and tracking) and labelling are in place. Where appropriate consumers want policies that enhance low prices by allowing competition and not fluctuating prices by maintaining stocks of inputs such as energy. Economic considerations are buying power, so the affordability of the products, which depends on income and price. Household cooks with jobs need products to save time in the kitchen. The degree of economic development of a country is of influence on households and shops having fridges and freezers needed to supply frozen products. Spending on products that are more expensive than fresh tubers is also determined by the economic sentiment such as (financial) crises and pandemics where one category of users, the food service, all of a sudden falls away. Food ethics of societies deliver bans such as “this is devoid of cow, pork, GMOs” which put restrictions on raw, batter and flavourings. Where to find a potato product is a focal point as street markets, small shops and supermarkets have an increasing array of products but distance from the user varies among economies and districts. Regarding technology, the availability of basic (stove and pans) or more advanced (oven, air fryer) equipment and storage (ambient pantry, fridge, freezer) for a great deal determines the absorption capacity of products. The internet is a driver for many consumers to make choices (dish, needed ingredients, prices) and so is circularity of production; besides an environmental issue, it is also a technological consideration for consumers who are aware of the possibilities. Using and consuming all of the product, so avoiding waste, is a most relevant social and environmental matter, so is re-use, avoidance of delivery to a landfill of packages and minimizing the use of energy and water in kitchens. Legal affairs affecting users of products are food safety regulations, waste management (organic, plastic, paper and residual waste) and age restrictions such as potato-based beers and vodka not to be sold to minors.

The heatmap of the classes of stakeholders and PESTEL elements as their attributes is shown in Table 8. There are two versions of the heatmap. On top, a version where it is assumed that the stakeholders are subjected to an existing situation with current PESTEL matters. At the bottom, the same stakeholders are listed but now scores are allocated assuming the stakeholders are able to exert an influence in a direction that favours them. The average of all scores is 3.0 at the top and 2.4 at the bottom, so in general stakeholders feel more a subject than a master of their surroundings. Especially growers seem most affected by policies regarding subsidies, imports regulations of chemicals and water to name a few. On the other hand, together with consumers, an even more numerous group, they also can exert an influence on policymakers through actions and democratic processes. The various stakeholders, although allotted very different scores (regulators are not affected by the economy, processors very much, monitors not by the environment, growers are) the average of scores hardly fluctuates with values around 3.

When it comes to influencing the surroundings through PESTEL matters there is more variation. Stakeholders are not very able to change technology and legal matters with an average score of 1.9 but are capable to influence society and to a slightly lesser degree also the environment. Breeders and monitors are more serving the surroundings than mastering them (average 1.3) and regulators, obviously, are superior with a sum of 3.8.

The classes of stakeholders subjected to PESTEL matters, regulators and controllers, are clustered as rather distant twins. Processors, retailers, food services and food industry have much in common. Consumers are not clustered with any other stakeholder. The PESTEL elements show two clusters, policy economy and environment being one of them. Where stakeholders exert an influence, the four that are most in control (growers, processors, consumers and regulators) are one cluster, the other five with the close twin processors and growers in the other.

Each class of PESTEL elements in Table 7 is supplied with details (producing subclasses) pertaining to the three principal participants in the supply chain. Theoretically, this leads to 6 PESTEL elements × 3 subjects × 3 participants = 54 subjects. These and a few more added are tabled and heatmapped according to their relative relevance, dependency, for the nine stakeholders alphabetically in Table 9.

There are five average scores lower than 2.2. This in general because they are only of interest to one or two interested parties such as the availability of and recovery from raw material (only growers and processors), only households are interested in appliances and only growers in credit (and in some cases processors too). Mean values between 2.2 and 3.3 dominate and are valid for about half of the classes, typically values of 2.8 are business environment, circularity, distance of outlets, mechanization and vicinity to clients found of interest for a few parties. Typical representatives of the range of averages of classes between 3.3 and 4.4 with a value of about 4 are related to policy and legal matters (allowed additives, certification corruption and compliance that touch most stakeholders. There is only one class with a sum of 4.4 which is information upstream: all stakeholders find this relevant because they have to (comply) or they like to (cooks informing the eaters). Policymakers are an exception, they have no entity above them to answer to. Also, other information-related classes have high scores.

The average scores of the interested parties in Table 9 are low for breeders and controllers as seen in Table 8, but now, the highest score is for the processors who find much relevance of many classes of subjects within the PESTEL elements. Where growers have no interest in the fabric of the clients of processors, product innovation and food waste, these are major concerns of processors. Yet, growers and processors have most in common as is apparent from the two high sums of scores, so there must be much agreement among them, as is also evident from the dendrogram (not shown).

The dendrogram (not presented) illustrates a few clusters and twins that are expected and easily explained, other ones seem more coincidental. Obvious ones are automation, mechanization, information and precision in one cluster and certification, emissions and chemicals allowed and so are labour costs, labour availability and equipment grouped, close by workers’ rights, salaries and business climate. Obvious twins are price and availability of raw (identical), decarbonization and circularity, buying power and new products, food safety and wanting to receive information, diets and health, information up- and downstream, safety at the workplace and scale of operations. Less obvious at first sight are the fabric of outlets users have to look for and package disposal; apparently, they are mainly a consumer concern, hence the logic. The stakeholders form three groups: the twins growers and processors are in one cluster, so are breeders, certifiers and regulators and the four users of products are clustered in the centre.

The Domain of PESTEL Matters in Diverse Environments

Formulation of the domain of PESTEL matters in diverse environments

There are countries, notably those close to the equator devoid of mountains, where it is too hot year round to grow potatoes. Yet, potato products, dried and frozen, are available such as mash powder in Paramaribo and frozen fries in Accra. There are no issues with respect to potato production and processing but high import duties, when applied, act as a taxation and may protect local alternatives. With low buying power and small markets these are not focal points of the multinational processors. The same is the case in low income tropical countries where farmers grow potatoes in the hills, and where often no processing takes place because of lacking demand, unfamiliarity with the products, and absence of a cold chain in shops. Some import of chips and frozen French fries takes place for a supermarket chain and for hotels.

There are countries where potatoes grow but where the raw material cannot compete with imported tubers. Japan imports part of its raw material from Canada both for making chips and French fries. Potato chips producers in Manilla use German potatoes among others because the local tubers with low dry matter are not suitable. In Indonesia, suitable tubers for chips production are not available year round and Indonesia procures them from Australia and Argentina where some harvests are six months later than in Europe. Usually, only cris** tubers are imported as raw material for national production, French fries are imported processed and frozen. Issues for local farmers who supply part of the need are quarantine measures to avoid the introduction of plant diseases, improvement of local raw material through variety introduction and crop management. Globally operating processors processing imported tubers in a new market have no other concerns than in their home country.

In several countries, there is a local cottage industry of chips to cater low-income buyers at markets whereas well-off customers purchase imported products in supermarkets (Kempenaar et al. 2017). The cottage industry procures from the local market where administrations often subsidize inputs such as chemicals, to stimulate the farming community. Farmers are at a disadvantage because of the low quality of the raw material that does not meet international standards coupled with a low efficient use of resources land, water, fertilizers and labour. Policies for processors and users in such markets usually are non-existent. Cottage-level processors’ concerns are increasing their scale of operations, consumers buy more when increasingly they have acquired a taste for the new snack.

Co-existence of large-scale production of frozen fries and chips of domestic and multinational origin is found in large new markets of China and India. Policies affecting global processors are the need to establish joint ventures with national companies and high import tariffs for their imported produce. Their socio-economic concerns are copying and adapting technology and the increasing demand to reduce emissions of pollutants. They have to establish a grower base with adequate technology to deliver raw material of the right quality as instructed by their agronomists: right variety and directed land, water and soil fertility management. Users, consumers in these situations, welcome the new food items, reason why the factories are scaling up. In saturated and export markets such as North America and Northern Europe farmers are subjected to trade wars, complying with agricultural policies including black listing of biocides, meeting contract obligations (quantity and specifications) at competitive prices, continuous adaptations to new techniques, varieties and chemicals. Restricted use of irrigation water, salinity, erosion and climate change are increasingly a concern of growers. Processors keep a close eye on a level playing field with environmental and state aid interventions applying to all actors in the field, anticipating and complying more and more with legislation regarding renewable energy and water use whence also innovations in technology. Users demand adequate policies and laws regarding food and environmental safety and are keen on competitive pricing with a wealth of choice and price-quality combinations. Innovations in the kitchen consist of introduction of appliances such as microwaves and air fryers.

Condensation of the domain of PESTEL matters in diverse environments

Six production-consumption situations exist regarding processing potatoes. These are shown in Table 10 together with a few of their most pressing PESTEL matters. Of each of the situations two cases are shown as examples representative of a number of such countries.

The introduction of potato processing at an industrial scale into new markets takes place following a few different trajectories. Cottage industry-level entrepreneurs start making chips in their kitchen, packed in plastic bags labelled with their mobile phone number and sold at nearby shops and markets. This then is scaled up to a small and gradually expanding factory with a local brand name and competes with the higher market segment of imported chips. When the foreign brand is large enough the global processor either buys the local brand or starts its own supply and demand chain. For a global player venturing into a new market without a take-over an about 10-year trajectory is needed to identify suitable varieties, organize growers for the production of seed and processing tubers before starting a production line. For frozen products it is also needed to establish a cold chain which takes time to develop so in the mean time they supply the chips processors or start making flakes awaiting market development. Meanwhile the PESTEL matters in Table 10 apply.

Quantification of the domain of PESTEL matters in diverse environments

The heatmap (Table 11) resulting from the inventory of Table 10 gives the general impression that the more advanced the processing environment is, the more substantial elements of PESTEL matter to the three principle partners in the product supply chain. The optimal is at the large-scale industry starting in upcoming markets. Here policymakers promulgate trade, tax and import measures that challenge processors, consumers lack knowledge and buying power, the raw material base needs to be built up and bureaucracy often is substantial. Some of these issues also play a role where processors use imported tubers only, but then, raw material is less of a complication as procurement is through a trader. Legal issues score lowest for all classes of actors with an average of 1.2 for users of products and 1.7 for growers of tubers. The producers in develo** markets are most affected by legal (administrative) procedures. The country’s policies, economy and society produce the highest average score indicative of the great interest the actors attach to these PESTEL elements.

Hierarchical clustering of the classes revealed that growers form a separate group finding all PESTEL elements essential (especially economic and social matters), with the exception of legal which they have in common with users. Policy for users and Technology for processors (both low scores) appear to be twins; here processing takes place with imported raw material, clusters with high scores are economy for users and processors. The attributes of the interest of markets in PESTEL elements show two groups. Twins represent the two markets where no processing of tubers takes place. Of the other four markets, the two with globally operating companies in upcoming and mature markets share the most interests followed by the remainder at some distance.

Deliberations and Conclusions

In this survey on processing potato and society, the domains of benefits, sustainability measures and PESTEL matters are distinguished. Values awarded to attributes of the classes of sustainability measures are given from the angle of those advocating the measures and by theoretical triangulation of those obstructing the measures. The domain of PESTEL matters consists of three sub-domains with respective classes of stakeholders, surroundings and parties. Stakeholders, through theoretical triangulation, give direction or are subjected to PESTEL matters. Table 12 enumerates the total number of classes (145) and of attributes (42) that appear in this survey. The number of times a score between 1 and 5 is awarded totals 1953.

The research questions, asked about benefits, sustainability measures and PESTEL matters and the degree of market development, are addressed in the three paragraphs below.

Processing potato is a well-established trade in the major potato producing countries so the advantages must be apparent. The inventory and analysis of the rewards of the industry (Tables 4, 5 and 6) show benefits for the three participants in the supply chain. The joint driving forces of growers, processors realize the benefits they all look for. Map** 21 products with 15 attributes showed that the highest sum of scores was about twice that of the lowest, indicative of a generally strong variation in perceived benefits by parties for different products. Users of potato products, notably cooks and consumers especially appreciate the convenience they are used to when preparing other meal components such as those from cereals. Shops, depending on the social setting, offer a wide array of products some of them are too difficult to make at home for many cooks, especially the breaded fried mash-based ones, or take so much time that it only rarely is done such as the preparation of chips. The introduction of new products such as pellet-based expended snacks or vegetable mixes in baby food have benefits for consumers, a widened choice, and for processors, a widened market. Besides, product innovation processors find benefits in adding value by increasing recovery through optimization of operations, use of side-flows and improving the raw material base by guiding growers. Especially for growers, but the other two parties, processors and users, benefit from the scale of production of tubers that is enhanced or maintained by the industry and by the somewhat regulating effect processing tubers into frozen French fries, chips and flakes has on supply of raw and the reduction of fluctuation of supply and prices of raw. This is because tubers can only be stored less than a year but products for years and tubers not meeting specifications for one product (e.g., chips) are then processed into a lower value product such as flakes.

Sustainability is a major social issue, how to optimally use and re-use resources and reduce emissions related to the environment. Processing companies also reckon food quality aspects and benefits for society as part of the sustainability domain which is justified from their business perspective: safe for the environment, consumer and community. In the Four-Tier Analysis the classes of sustainability issues are expressed as measures to be taken by growers on their farms (9 measures) and processors in operations (7), on food quality (8) and for communities (8). Retail, food service, food industry and users/consumers are not dealt with by the industry, nor treated here as they are of too a generic nature to merit scrutiny here. The attributes in the Tables 5 and 6 are successively (1) the degree nine stakeholders are targeted and need to carry out the measures or monitor them, (2) how much they are able to steer the measures in a way they become more effective and (3) how much they are able to ignore them if they feel opportunistic. Of the attributes, consumers are least targeted and processors in their operations most, more than twice; of the classes profits score least and food safety highest also more than twice. Important measures are tracing for growers, distances for processors, food safety and mitigating effects of calamities in the community such as a pandemic. The sum of all scores in this scenario is 777. The dendrogram discloses a class of measures about food safety, one about innovation and a few twins like profits and recovery. The sum of scores in the heatmap where stakeholders steer is 630, so in general, participants are more subjected than in control. Breeders receive lower scores than when subjected but regulators evidently more. Being able to obstruct also has a total sum of 630. Processors score more than three times that of breeders. Most difficult to obstruct is gluten-free batter as it would be disclosed easily and most simply innovation of new products by producers shops and consumer refusing to produce, distribute or use them. Figure 1 makes it clear that growers and processors are not very distinct in the three scenarios except for growers being targeted for information streaming. Food quality is most targeted, best given direction and least sensible to obstruction.

Average value of the scores of sustainability measures pertaining to growers, processors, food health and safety and community services in the two scenarios given by the nine stakeholders (breeders, growers, processors…cooks, policymakers) when they are targeted or obstructing the measures

The same nine stakeholders involved in sustainability issues and measures, show interest in and are subjected to national policies, the economy, the social setting, technological developments, the environment and legal matters embodied in the PESTEL approach (Tables 8 and 9). But they can also exert an influence. Growers are most influenced because of societal demands regarding biodiversity, use of land, water chemicals and subsidies but also have quite some influence through numbers and political actions and by illustrating which rules work and which ones do not. A clear demonstration of interaction. Breeders on the other hand are influenced by 4 out of 6 PESTEL elements but have no say so there. Processors and restaurants are much influenced by surroundings but have less power than growers and consumers, two numerous groups. Focusing on each PESTEL matter was done by switching PESTEL matters and stakeholders of Tables 8 and 9 in Table 11 and dividing the resulting classes of PESTEL elements in 3–4 subclasses totaling 63 subclasses. The stakeholders were made their attributes by giving them scores for the relative relevance of the PESTEL elements for them. The average score for the processors was twice as high as for the monitors. The order of the stakeholders in Table 11 looks most like stakeholders affected by PESTEL elements and less like the order of mastering the elements. In both situations processors and growers take the lead and breeders and monitors are at the tail end. Clusters of PESTEL matter receiving the same degree of attention are (1) those around technology, precision and automation, (2) price, availability and quality of raw and 3) food safety, health and diets.

Involvement of the degree of market development while analysing is a typical example of environmental triangulation. Three parties (growers, processors and users) in six environments (stages of market development) produce eighteen classes with the six PESTEL matters of relevance for them as attributes. The sums of the scores for attributes are 18 for countries where no potato is grown nor processed and moves up to 65 with increasing processing taking place with local tubers by nationally and internationally operating companies to decrease to 60 when produced in mature markets. In these markets, compared to the develo** ones, policy is less relevant for processors since policies are stable, growers are less delivered to the whims of economy, users still have to get more used to new products and growers are still in greater need of mechanization. All six economies have users of potato products where they find legal, policy and environmental matters less pertinent than growers and processors but the economy is of importance to them. The highest score (three times more than users-legal) is for economy and processors. They only export to, enter economies or start operations when the economic situation looks promising.

References

Arici A (2019) Exclusive: North America speeds up investments in processing POTATO BUSINESS. https://www.potatobusiness.com/market/exclusive-north-america-has-sped-up-investments-in-processing/ Accessed April 14, 2022

Arranz-Otaegui A, Gonzalez Carretero L, Ramsey MN, Fuller DQ, Richter T (2018) Archaeobotanical evidence reveals the origins of bread 14,400 years ago in northeastern Jordan. Proc Natl Acad Sci 115:7925–7930

Avebe (2020) https://schuttelaar-partners.com/werk/avebe/geintegreerd-jaarverslag-2018-2019-avebe-16-dec-en_online.pdf Accessed April 14, 2022

Aviko (2020) https://corporate.aviko.com/media/1388/aviko-susainability-report-2102-2103.pdf Accessed April 14, 2022

B2U (2020) https://www.business-to-you.com/industry-analysis/scanning-the-environment-pestel-analysis/. Accessed October 1 2020.

Blakely R (2019) Junk food causing obesity in world’s poorest places. The Times https://www.thetimes.co.uk/article/junk-food-causing-obesity-in-worlds-poorest-places-6f5zkrvcw Accessed April 14, 2022

Borch D, Juul-Hindsgaul N, Veller M, Astrup A, Jaskolowski J, Raben A (2016) Potatoes and risk of obesity, type 2 diabetes, and cardiovascular disease in apparently healthy adults: a systematic review of clinical intervention and observational studies. Am J Clin Nutr 104:489–498

Chandrasekara A, Thamilini JK (2016) Roots and tuber crops as functional foods: a review on phytochemical constituents and their potential. Int J Food Sci 3631647:15. https://doi.org/10.1155/2016/3631647

De Thouars J (2018) https://www.change.inc/industrie/er-gaan-2-kilo-aardappels-in-1-kilo-frites-waar-blijft-de-rest-28393 Accessed April 14, 2022

EUPPA (2021) https://euppa.eu/_library/_files/EUPPA_Sustainability_Report_2021_online.pdf. Accessed 10 May 2022

FAO (2021) http://www.fao.org/prices/en/. Accessed 11 Apr 2022

Farm Frites (2020) https://sustainabilityreport2019.farmfrites.com/summary/ Accessed April 14, 2022

Fona (2021) https://www.fona.com/1219indulgence Accessed April 14, 2022

Fresh Plaza (2022) https://www.freshplaza.com/content/about-us/. Accessed 10 May 2022

FritoLay (2020) https://www.fritolay.com/about-frito-lay/sustainability 2019 Accessed April 14, 2022

Haverkort AJ (1990) Ecology of potato crop** systems in relation to altitude and latitude. Ag Systems 32:251–272

Haverkort AJ (2018) Potato handbook: crop of the future. Potato World Magazine, CITY, Country, 600 pp

Haverkort AJ, Hillier JG (2011) Cool farm tool – potato: model description and performance of four production systems. Potato Res 54:355–369

Haverkort AJ, Verhagen J (2008) Climate change and its repercussions for the potato supply chain. Potato Res 51:223–237

Haverkort AJ, Franke AC, Engelbrecht FA, Steyn JM (2013) Climate change and potato production in contrasting South African agro-ecosystems 1. Effects on land and water use efficiencies. Potato Res 56:31–50

Haverkort AJ, van Koesveld MJ, Schepers HATM, Wijnands JHM, Wustman R, Zhang X (2012) Potato prospects for Ethiopia: on the road to value addition. PPO publication No. 528, Wageningen University and Research, Wageningen, 72 pp

Haverkort AJ, Linnemann AR, Struik PC, Wiskerke JSC (2022a) On processing potato. 1. Survey of the ontology, history and participating actors. Potato Res. https://doi.org/10.1007/s11540-022-09562-z

Haverkort AJ, Linnemann AR, Struik PC, Wiskerke JSC (2022b) On processing potato. 2. Survey of processes and operations in manufacturing products. Potato Res. https://doi.org/10.1007/s11540-022-09563-y

Haverkort AJ, Linnemann AR, Struik PC, Wiskerke JSC (2022c) On processing potato. 3. Survey of performances, productivity and losses in the supply chain. Potato Res. https://doi.org/10.1007/s11540-022-09576-7

Inouye A (2018) China – Potato and Potato Products Annual Report (USDA Foreign Agricultural Service GAIN Report CH18066). United States Department of Agriculture, Washington, DC, 7 pp

Julia C, Etilé F, Hercberg S (2018) Front-of-pack Nutri-Score labelling in France: an evidence-based policy. The Lancet Public Health. https://www.thelancet.com/pdfs/journals/lanpub/PIIS2468-2667(18)30009-4.pdf, Accessed April 14, 2022

Kempenaar C, Blom-Zandstra M, Brouwer TA, De Putter H, De Vries H, Hengsdijk H, Janssens SR, Kessel GJT, Van Koesveld F, Meijer BJM, Pronk AA, Schoutsen M, Ter Beke F, Van den Brink L, Michielsen JM, Schepers HTAM, Wustman R, Zhang X, Qiu IT, Haverkort AJ (2017) Netherlands public private partnerships aimed at co-innovation in the potato value chain in emerging markets. Open Agric 2:544–551

Kurai T (2017) Japan Potato Annual 2017. https://www.usdajapan.org/wpusda/wp-content/uploads/2017/11/Japan-Potato-Annual-2017_Tokyo_Japan_10-27-2017.pdf

LambWeston (2020) https://lambweston.eu/emea/sustainability/report-and-summary Accessed April 14, 2022

Nurmi J, Mikko S. Niemelä (2018) PESTEL Analysis of hacktivism campaign motivations. Nordic Conference on Secure IT Systems. NordSec 2018: Secure IT Systems pp 323–335.

Paul V, Ezekiel R, Pandey R (2016) Sprout suppression on potato: need to look beyond CIPC for more effective and safer alternatives. J Nutr Food Sci 53:1–18

Paul AA, Southgate DAT (1978) McCance and Widdowson’s The composition of foods, 4th edition. MRC Special Reports no. 297. HMSA London. Cited by Woolfe JA, 1987. The potato in the human diet. Cambridge University Press, Cambridge, 231 pp

Pelletier RC, Getchell JS, Highlands ME, Clark DR (1964) A comparison of several peeling methods as applied to Maine potatoes for processing. Maine Agric Exp Station Bull 624:32

Pepsico (2020) https://www.pepsico.com/sustainability-report/climate#introduction Accessed April 14, 2022

Rana RK, Martolia R, Singh V (2017) Trends in global potato processing industry-evidence from patents’ analysis with special reference to Chinese experience. Potato Journal 44:37–44

Roman A (2015) An integrated strategy framework (ISF) for combining Porter’s 5-forces, Diamond, PESTEL, and SWOT analysis. HfWU - University of Economics and Environment, FAME https://mpra.ub.uni-muenchen.de/72507/ Accessed 14 April, 2022

Simplot (2020) https://www.simplot.com/sustainability (2013) Accessed April 14, 2022

Singh KK, Shukla BD (1995) Abrasive peeling of potatoes. J Food Eng 26:431–42

Somsen D (2004) Production yield analysis in food processing; applications in the French fries and poultry processing Industries. PhD Thesis Wageningen University, Wageningen, 116 pp

Willard M (1993) Potato processing: past, present and future. Am Potato J 70:405–418

Woolfe JA (1987) The potato in the human diet. Cambridge University Press, Cambridge, p 231

Zarantonello L, Schmitt B (2010) Using the brand experience scale to profile consumers and predict consumer behaviour. J Brand Manag 17:532–540

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Competing Interests

P.C. Struik is editor-in-chief of Potato Research.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Haverkort, A.J., Linnemann, A.R., Struik, P.C. et al. On Processing Potato. 5. Survey of Societal Benefits, Stewardship and Surroundings. Potato Res. 66, 469–505 (2023). https://doi.org/10.1007/s11540-022-09569-6

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11540-022-09569-6