Abstract

This study examines a European sample of 222 private firms that opted for going public through a reverse takeover transaction during the period 1992–2011. In particular, our study investigates whether reverse takeovers announcements are value-increasing transactions, especially in countries that follow strong governance structures. Moreover, the post-reverse takeover stock price and operating performance is also at the epicenter of the current study. Employing the classical event study methodology, we document significant wealth gains for the shareholders of public firms involved in reverse takeovers. The market reaction is stronger when stricter corporate governance structures prevail in the countries where public firms trade. However, the short-term gains seem to revert to substantial losses over the long-term lending support to the overreaction phenomenon. We further detect negligible improvement in the post-reverse takeover financial performance of the new entity raising further concerns over the efficacy of such transactions.

Similar content being viewed by others

Notes

Brenner and Schroff (2004) estimated the time needed to carry out a reverse takeover at 45 days compared to a year or more for an IPO.

The term is commonly used in the context of reverse takeovers meaning firms that may have had operations once which have narrowed down significantly today, thus appearing to only serve the role of offering a listing status to a private company.

According to Faelten et al. (2013) during the recent financial crisis (2007–2009), the number of IPOs dropped by 96% while that of reverse takeovers remained almost stable in the UK market.

A recent strand of studies by Chen et al. (2013), Darrough et al. (2013), Siegel and Wang (2013), and Lee et al. (2015) have explored various characteristics (i.e. financial reporting quality, corporate governance structures, performance, survivability, etc) of the Chinese reverse mergers seeking a listing status in the USA. Lee et al. (2015) reports that 85% of all foreign reverse takeovers in the US market today involve Chinese acquirers.

Lee et al. (2015) estimated the underwriting cost for an IPO between 7 and 12% of the total offer.

A reverse takeover takes between 2 and 9 months to be consummated (Brenner and Schroff 2004).

The rules were tightened as a result of a reverse transaction between Vallar Plc, a listed shell company, and Bumi Resources, an Indonesian venture, that launched an inquiry into $500 m of alleged irregularities in subsidiaries (Oakley 2012).

Public firms were not exclusively shell firms, but large firms with existing business operations.

Α firm goes public without the use of underwriters.

Givoly et al. (2014) reported that the number of reverse takeovers that took place in the US has quadrupled and that of foreign reverse takeovers has grown tenfold over the last decade.

We required both private and public firms to be located in Europe.

In the UK, under the new proposals which prevent UK companies from buying listed firms merely as a back door to change their listing category, an acquisition of a listed issuer by another listed issuer falling into the same listing category is not considered a reverse takeover (Appadu et al. 2014). Instead this is considered an ordinary acquisition.

In order to assess the long-term stock price and operating performance two years after reverse takeovers, we extend our dataset up to 2013.

Gleason et al. (2005) find negative ROA, ROE and NPM, an average cash to total assets ratio of 22% and a mean debt to total assets ratio of 20%.

FTSE all shares index for UK stocks, CAC 40 index for French stocks, etc.

Similar approach was adopted by Gleason et al. (2005). Based on Scholes and Williams (1977) returns are calculated as follows:

\(\begin{aligned} R_{it} & = \alpha_{1t} + \beta_{1t} (R_{mt - 1} ) + \varepsilon_{it} ,R_{it} = \alpha_{2t} + \beta_{2t} (R_{mt} ) + \varepsilon_{it} ,R_{it} = \alpha_{3t} + \beta_{3t} (R_{mt + 1} ) + \varepsilon_{it} \\ \hat{\beta }_{SW} & = \frac{{\hat{\beta }_{1t} + \hat{\beta }_{2t} + \hat{\beta }_{3t} }}{{1 + 2\hat{\rho }_{m} }} \\ \end{aligned}\) where ρm is the first-order autocorrelation of Rm.

To get an idea how the market reaction to reverse takeover announcements compares to that of typical IPOs, we refer to some recent studies conducted in the US, Europe and Asia. For example, Chua (2014) examined the first day return of US IPOs for the period 1980–2012 and found an excess return of 19.4% and a median of 6.9%. During the low valuation period, the mean and median first day returns were 11.9 and 5.2%, respectively. During the high valuation period, the mean and median first day returns were 21.7 and 7.6%, respectively. Zhen Li et al. (2016), using a large sample of IPOs in the US, estimated first-day underpricing based on tax rates and found that the mean first-day return was 11.28% for the period 2003–2010 compared to 9.97% in 2002, 17.32% in 2001 and 27.46% during 1993–2000. Ozdemir and Upneja (2016) investigated the market reaction to 1822 service firms that were taken public during the period of 1980–2009 and found an average initial return of 22.74%. On the other hand, examining 740 European IPOs, Jenkinson et al. (2005) found an average initial announcement return of 22.3% (15.2% for 174 French IPOs, 47.5% for 224 German IPOs, 4.8% for 51 Italian IPOs, 9.0% for 124 UK IPOs, and 14.3% for 50 Dutch IPOs). Moreover, Gajewski and Gresse (2006) reported initial average returns of 22.06% for 2104 IPOs from 15 countries (5.36% for 363 French IPOs,6 38.93% for 415 German IPOs, 10.26% for 135 Italian IPOs, 21.27% for 454 UK IPOs, and 22.92% for 47 Dutch IPOs). Dorsman and Gounopoulos (2013) explored the performance of Dutch IPOs during the period 1990 to May 2012 and confirmed the underpricing phenomenon (i.e. initial excess returns of 8.31%). Chong et al. (2010) found that the average IPO underpricing level of H-shares in Hong Kong was about 16.8% for the period 1993–2003.

An increase in industrial focus is defined as when the public firm operates in the same two-digit SIC code with the private firm.

Each index ranges from 1 to 7, with higher values indicating more protected minority shareholders’ interests, or stronger investor protection or management that is highly accountable to investors and boards, or stronger financial auditing and reporting standards.

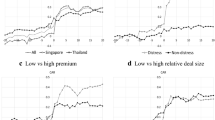

The results from minority shareholder protection mirror the results from the market reaction to reverse takeover announcements according to strength of auditing and reporting standards. Therefore, the sample of high minority shareholder protection coincides with that of high strength of auditing and reporting standards.

Similar findings are observed in the long-run performance of IPOs. In specific, Dorsman and Gounopoulos (2013), using a sample of Dutch IPOs for the period from January 1990 to May 2012, found adjusted BHARs of −7.48% (−26.27%) 1 (2) year(s) after the first trading day. Amor and Kooli (2016) examined the post-IPO performance of 5055 US IPOs taken place between 1980 and 2006 and found a 24-month market-adjusted BHAR of −28.46% for frequent acquirers (firms making multiple acquisitions after the IPO) and −12.40% for infrequent acquirers (firms making a single acquisition after the IPO).

The results from the UK, non-UK, industrial focus and non-focus and corporate governance structures are available upon request.

References

Adjei F, Cyree K, Walker M (2008) The determinants and survival of reverse mergers vs. IPOs. J Econ Finance 32:176–194

Akyol AC, Cooper T, Meoli M, Vismara S (2014) Do regulatory changes affect the underpricing of European IPOs? J Bank Finance 45:43–58

Amor S, Kooli M (2016) Do acquisitions affect IPO long-run performance? evidence from single vs. multiple acquirers. Int Fin Markets Inst Money 40:63–79

Appadu N, Faelten A, Levis M (2014) Reverse takeovers: are they a viable alternative to IPOs? Working paper, Cass Business School

Aydogdu M, Shekhar C, Torbey V (2007) Shell companies as IPO alternatives: an analysis of trading activity around reverse mergers. Appl Fin Econ 17:1335–1347

Ball E, Chiu H, Smith R (2011) Can VCs time the market? an analysis of exit choice for venture-backed firms. Rev Finance Stud 24:3105–3138

Brenner VC, Schroff WK (2004) Reverse merger or IPO. Strateg Finance 85:46–52

Chen KC, Cheng Q, Lin YC, **ao X (2013) Financial reporting quality of Chinese reverse merger firms: the reverse merger effect or the China effect? Working paper, Singapore Management University

Chen C, Gotti G, Herrmann D, Schumann K (2015) Earnings quality of foreign vs. US reverse mergers: geographical location or firm-level incentives? J Int Account Res 15:49–66

Chong T, Yuan S, Yan I (2010) An examination of the underpricing of H-share IPOs in Hong Kong. Rev Pac Basin Finance Markets Polic 13:559–582

Chua A (2014) Market conditions, underwriter reputation and first day return of IPOs. J Fin Markets 19:131–154

Darrough M, Huang R, Zhao S (2013) The spillover effect of fraud allegations against Chinese reverse mergers. Working paper, City University of New York

Dorsman A, Gounopoulos D (2013) European sovereign debt crisis and the performance of Dutch IPOs. Int Rev Fin Anal 30:308–319

Faelten A, Appadu N, Levis M (2013) The poor man’s IPO: reverse takeovers in the UK. Working paper, Cass Business School

Fama E (1998) Market efficiency, long-term returns, and behavioral finance. J Finance Econ 49:283–306

Financial Services Authority (FSA) (2012a) Amendments to the listing rules, prospectus rules, disclosure rules and transparency rules. http://www.fsa.gov.uk/static/FsaWeb/Shared/Documents/pubs/cp/cp12_02.pdf. Accessed 8 Dec 2016

Financial Services Authority (FSA) (2012b) UKLA publications—technical note—reverse takeovers. http://www.fsa.gov.uk/pubs/ukla/reverse_takeovers.pdf. Accessed 8 Dec 2016

Floros I, Sapp T (2011) Shell games: on the value of shell companies. J Corp Finance 17:850–867

Floros I, Shastri K (2010) A comparison of penny stock initial public offerings and reverse mergers as alternative mechanisms for going public. Working paper, Iowa State University

Gajewski JF, Gresse C (2006) A survey of the European IPO market. ECMI paper no. http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.616.7007&rep=rep1&type=pdf. Accessed 8 Dec 2016

Gao Y, Oler D (2012) Rumors and pre-announcement trading: why sell target stocks before acquisition announcements? Rev Quant Finance Account 39:485–508

Givoly D, Hayn C, Lourie B (2014) Importing accounting quality: the case of foreign reverse merger. Working paper, Pennsylvania State University and University of California

Gleason K, Rosenthal L, Wiggins R (2005) Backing into being public: an exploratory analysis of reverse takeovers. J Corp Finance 12:54–79

Gleason K, Jain R, Rosethal L (2008) Alternatives for going public: evidence from reverse takeovers, self-underwritten IPOs and tranditional IPOs. Finance Decis 20:1–24

Gompers P, Lerner J (1999) Conflict of interest and reputation in the issuance of public securities: evidence from venture capital. J Law Econ 42:53–80

Greene D (2016) The wealth of private firm owners following reverse mergers. J Corp Finance 37:56–75

Grossman S, Hart O (1980) Takeover bids, the free-rider problem and the theory of the corporation. Bell J Econ 11:42–64

Jenkinson T, Morrison A, Wilhelm J (2005) Why are European IPO’s so rarely priced outside the indicative price range? J Fin Econ 80:185–209

La Porta R, Lopez-De-Silanes R, Shleifer A, Vishny R (1998) Law and finance. J Polit Econ 106:1113–1155

Lee C, Li K, Zhang R (2015) Shell games: the long term performance of Chinese reverse merger firms. Account Rev 90:1547–1589

Moerland P (1995) Corporate ownership and control structures: an international comparison. Rev Ind Organ 10:443–464

Oakley D (2012) City watchdog to tighten listing rules. Financial times. http://www.ft.com/intl/cms/s/0/a2709378-0c8c-11e2-a73c-00144feabdc0.html. Accessed 8 Dec 2016

Owen S, Yawson A (2010) Corporate life cycle and M&A activity. J Bank Finance 34:427–440

Ozdemir O, Upneja A (2016) The role of internationalization on the IPO performance of service firms: examination of initial returns, long-run returns, and survivability. Int Bus Rev 25:997–1009

Pastor-Llorca M, Martin-Ugedo J (2004) Long-run performance of Spanish seasoned equity issues with rights. Int Rev Fin Anal 13:191–215

Pollard T (2016) Sneaking in the back door? an evaluation of reverse mergers and IPOs. Rev Quant Finance 47:305–341

Rossi S, Volpin P (2004) Cross-country determinants of mergers and acquisitions. J Finance Econ 74:277–304

Scholes M, Williams J (1977) Estimating betas from nonsychronous data. J Finance Econ 5:309–327

Securities and Exchange Committee (SEC) (2011) Investor bulletin: reverse mergers. Office of investor education and advocacy. http://www.sec.gov/investor/alerts/reversemergers.pdf. Accessed 8 Dec 2016

Semenenko I (2011) Reverse merger waves, market timing and managerial behaviour. Int Res J Appl Finance 2:1453–1481

Siegel J, Wang Y (2013) Cross-border reverse mergers: causes and consequences. Working paper, Harvard University and Boston University

Song K, Kim I, Chang Y (2014) A reverse takeover as an exit strategy of venture capital: Korean evidence. Pac Basin Finance J 29:182–198

Wu C (2013) Underpricing of homecoming A-share IPOs by Chinese firms already listed abroad. Rev Quant Finance Account 43:627–649

Zhen Li O, Lin Y, Robinson J (2016) The effect of capital gains taxes on the initial pricing and underpricing of IPOs. J Account Econ 61:465–485

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Dasilas, A., Grose, C. & Talias, M.A. Investigating the valuation effects of reverse takeovers: evidence from Europe. Rev Quant Finan Acc 49, 973–1004 (2017). https://doi.org/10.1007/s11156-016-0614-9

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11156-016-0614-9