Abstract

This paper tests for the effects of financial constraints on open-bid English land auction prices and bids. It is argued that bidders’ ability to pay, taken as capital resources and/or capital budget constraints, influence bids and final auction prices. While high capital resource developers may elect to bid more than optimal to win auctions, or bidders may elect to pool resources in joint bidding, budget constraints imposed by firm-specific financial variables on the other hand are expected to restrict bids. Land auction data in Hong Kong are used to test systematically these predictions. It is found that a firm’s age, the number of winners in a joint bid, and firm status in the market are positively related to prices, all factors which may be attributed to a firm’s ability to finance the auction price. Firm size, internal funds, financing cost, debt capacity and existing capital expenditure are also shown to affect bids submitted in land auctions: firm size and internal funds are positively related to bid prices; while constrained debt capacity, financing cost and existing capital expenditure lower bids. The results are consistent with predictions that a firm’s financial constraints, and thus its effect on capital budgets, are relevant factors in predicting land auction outcomes. More generally, these findings confirm that similar financial factors that constrain corporate capital investment also influence directly acquisition of assets at auctions.

Similar content being viewed by others

Notes

Ooi, et al. argue that “differences in market information, access to capital, legal status as well as non-pecuniary preferences all affect the profitability of the parcel of land to that particular type of buyer, hence the bid rent and selling price” (2006:70), but their empirical results do not unambiguously support this effect.

Webb-site is a Hong Kong corporate governance source and database (http://www.webb-site.com/).

In unreported further tests we also use the average of reserve and winner price as dependent variable for the companies that do not win the auctions.The empirical results do not differ materially.

Firm size is measured by total book asset or total market value in corporate finance literature. See Appendix 2.

In unreported results, we entered only one variable in each model. The signs and significance do not change.

Among the 247 sites, only 11 were for office use and 30 for industrial use. The balances of 206 sites are residential land. Our results hold if we only use residential sites.

We also conduct several robustness tests using the winner dataset. We include: (1) the variables of property index; (2) the variables of construction cost index; (3) the dummy variables of year-quarter; (4) the dummy variables of sub-districts in Hong Kong. All these tests do not change the results significantly.

This number is the median value of the reserve prices of all sites in our sample.

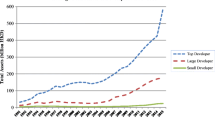

One potential explanation is that these biggest firms may choose to join most of land auctions, for large land or small land. In the auctions for small land, they may face more competitions and lose the bidding because many small/median firms, only being able to afford for small land, can bid aggressively in the small-land auctions.

Prior to a site auctioned on September 6, 2011 , Cheung Kong and Sun Hung Kai Properties were estimated to lead the auction as the two developers held the second and third largest cash balances (HK$9.1 billion and HK$5 billion) among all Hong Kong developers. The final result was that Sun Hung Kai Properties won the auction with a HK$3.12 billion bid.

References

Audit Commission (2001) The Administration of Sale of land by public auction. The Government of the Hong Kong Special Administrative Region, No. 37, Chapter 7. http://www.aud.gov.hk/eng/pubpr_arpt/subj_builp.htm.

Becker, B., & Ivashina, V. (2014). Cyclicality of credit supply: Firm level evidence. Journal of Monetary Economics, 62, 76–93.

Benoît, J., & Krishna, V. (2001). Multiple-object auctions with budget constrained bidders. Review of Economic Studies, 68(1), 155–179.

Boyle, G., & Guthrie, G. (2003). Investment, uncertainty, and liquidity. The Journal of Finance, 58(5), 2143–2166.

Bulow, J., Levin, J., & Milgrom, P. (2009). Winning play in spectrum auctions. NBER working paper no. 14765.

Campello, M., & Hackbarth, D. (2008). Corporate financing and investment: The firm-level credit multiplier. EFA 2008 Athens Meetings Paper.

Campello, M., Graham, J. R., & Harvey, C. R. (2010). The real effects of financial constraints: Evidence from a financial crisis. Journal of Financial Economics, 97(3), 470–487.

Chau, K., Wong, S., Yiu, C., Tse, M., & Pretorius, F. (2010). Do unexpected land auction outcomes bring new information to the real estate market? The Journal of Real Estate Finance and Economics, 40(4), 480–496.

Che, Y., & Gale, I. (1996). Expected revenue of all-pay auctions and first-price sealed-bid auctions with budget constraints. Economics Letters, 50(3), 373–379.

Che, Y., & Gale, I. (1998). Standard auctions with financially constrained bidders. Review of Economic Studies, 65(1), 1–21.

Che, Y., & Gale, I. (2000). The optimal mechanism for selling to a budget-constrained buyer. Journal of Economic Theory, 92(2), 198–233.

Che, Y., Gale, I., & Kim, J. (2013). Assigning resources to budget-constrained agents. Review of Economic Studies, 80(1), 73–107.

Ching, S., & Fu, Y. (2003). Contestability of the urban land market: An event study of Hong Kong land auctions. Regional Science and Urban Economics, 33(6), 695–720.

Cleary, S. (1999). The relationship between firm investment and financial status. The Journal of Finance, 54(2), 673–692.

Cramton, P. C. (1995). Money out of thin air: The Nationwide narrowband PCS auction. Journal of Economics and Management Strategy, 4(2), 267–343.

Cramton, P. (1997). The FCC Spectrum auctions: An early assessment. Journal of Economics and Management Strategy, 6(3), 431–495.

Deng, Y., Morck, R., Wu, J., & Yeung, B. Y. (2014). China’s pseudo-monetary policy. Review of Finance, 19(1), 55–93.

Dong, Z., & Sing, T. F. (2014). Developer heterogeneity and competitive land bidding. The Journal of Real Estate Finance and Economics, 48(3), 441–466.

Dotzour, M., Moorhead, E., & Winkler, D. (1998). The impact of auctions on residential sales prices in New Zealand. Journal of Real Estate Research, 16(1), 57–72.

Duchin, R., Ozbas, O., & Sensoy, B. A. (2010). Costly external finance, corporate investment, and the subprime mortgage credit crisis. Journal of Financial Economics, 97(3), 418–435.

Erel, I., Julio, B., Kim, W., & Weisbach, M. S. (2012). Macroeconomic conditions and capital raising. Review of Financial Studies, 25(2), 341–376.

Fang, H., & Parreiras, S. O. (2002). Equilibrium of affiliated value second price auctions with financially constrained bidders: The two-bidder case. Games and Economic Behavior, 39(2), 215–236.

Fang, H., & Parreiras, S. O. (2003). On the failure of the linkage principle with financially constrained bidders. Journal of Economic Theory, 110(2), 374–392.

Fazzari, S., Hubbard, G., & Petersen, B. (1988). Financing constraints and corporate investment. Brookings Papers on Economic Activity, 1988(1), 141–195.

Gwin, C. R., Ong, S., & Spieler, A. C. (2005). Auctions and land values: An experimental analysis. Urban Studies, 42(12), 2245–2259.

Hadlock, C. J., & Pierce, J. R. (2010). New evidence on measuring financial constraints: Moving beyond the KZ index. Review of Financial Studies, 23(5), 1909–1940.

Hargreaves, M, Schinasi, G J, and Weisbrod, S R, 1993. Asset price inflation in the 1980s: A funds flow perspective. Working paper WP/93/77, The International Monetary Fund, Washington, DC.

Heckman, J. J. (1979). Sample selection bias as a specification error. Econometrica, 47(1), 153–161.

Kaplan, S. N., & Zingales, L. (1997). Do investment-cash flow sensitivities provide useful measures of financing constraints? The Quarterly Journal of Economics, 112, 169–215.

Kiyotaki, N., & Moore, J. (1997). Credit cycles. Journal of Political Economy, 105(2), 211–248.

Kotowski, M. H. (2013). First-price auctions with budget constraints. Working paper. Kennedy School of Government, Harvard University.

Kotowski, M. H., & Li, F. (2014). On the continuous equilibria of affiliated-value, all-pay auctions with private budget constraints. Games and Economic Behavior, 85, 84–108.

Krishna, V. (2010). Auction theory. Academic press, 2nd edition.

Kwok, V. (2012). Two developers tower over market. South China Morning Post, (30 March).

Lamont, O., Polk, C., & Saaá-Requejo, J. (2001). Financial constraints and stock returns. The Review of Financial Studies, 14(3), 529–554.

Long, J. S., & Freese, J. (2006). Regression models for categorical and limited dependent variables using stata, 2nd edn. College Station: Stata Press.

Lusht, K. M. (1994). Order and price in a sequential auction. Journal of Real Estate Finance and Economics, 24(4), 517–530.

Lusht, K. M. (1996). A comparison of prices brought by English auctions and private negotiations. Real Estate Economics, 24(4), 517–530.

Marseguerra, G., & Cortelezzi, F. (2009). Debt financing and real estate investment timing decisions. Journal of Property Research, 26(3), 193–212.

Mayer, C. J. (1998). Assessing the performance of real estate auctions. Real Estate Economics, 26(1), 41–66.

McAfee, R. P., & McMillan, J. (1987). Auctions and bidding. Journal of Economic Literature, 25(2), 699–738.

McMillen, D. P. (1997). Multiple regime bid-rent function estimation. Journal of Urban Economics, 41(2), 301–319.

McMillen, D. P., Jarmin, R., & Thorsnes, P. (1992). Selection bias and land development in the monocentric city model. Journal of Urban Economics, 31(3), 273–284.

Milgrom, P. (1989). Auctions and bidding: A primer. Journal of Economic Perspectives, 3(3), 3–22.

Milgrom, P. (2004). Putting auction theory to work. Cambridge: Cambridge University Press.

Ong, S. E. (2006). Price discovery in real estate auctions: The story of unsuccessful attempts. Journal of Real Estate Research, 28(1), 39–60.

Ong, S. E., Lusht, K., & Mak, C. Y. (2005). Factors influencing auction outcomes: Bidder turnout, auction houses and market conditions. Journal of Real Estate Research, 27(2), 177–192.

Ooi, J. T., & Sirmans, C. (2004). The wealth effects of land acquisition. The Journal of Real Estate Finance and Economics, 29(3), 277–294.

Ooi, J. T., Sirmans, C., & Turnbull, G. K. (2006). Price formation under small numbers competition: Evidence from land auctions in Singapore. Real Estate Economics, 34(1), 51–76.

Pitchik, C., & Schotter, A. (1988). Perfect Equilibria in budget-constrained sequential auctions: An experimental study. RAND Journal of Economics, 19(3), 363–388.

Qu, W., & Liu, X. (2012). Assessing the performance of Chinese land lease auctions: Evidence from Bei**g. Journal of Real Estate Research, 34(3), 291–310.

Quan, D. C. (1994). Real estate auctions: A survey of theory and practice. The Journal of Real Estate Finance and Economics, 9(1), 23–49.

Rauh, J. D. (2006). Investment and financing constraints: Evidence from the funding of corporate pension plans. The Journal of Finance, 61(1), 33–71.

Renaud, B., Pretorius, F. & Pasadilla, B. (1997). Markets at Work: Dynamics of the residential real estate market in Hong Kong. Hong Kong: Hong Kong University Press.

Riddiough, T. (1997). Debt and development. Journal of Urban Economics, 42(3), 313–338.

Riley, J. G., & Samuelson, W. F. (1981). Optimal auctions. The American Economic Review, 71(3), 381–392.

Salant, D. J. (1997). Up in the air: GTE’s experience in the MTA auction for personal communication services licenses. Journal of Economics and Management Strategy, 6(3), 549–572.

Shen, J., & Pretorius, F. (2013). Binomial option pricing models for real estate development. Journal of Property Investment & Finance, 31(5), 418–440.

Shleifer, A., & Vishny, R. W. (1992). Liquidation values and debt capacity: A market equilibrium approach. The Journal of Finance, 47(4), 1343–1366.

Tobin, J. (1958). Estimation of relationships for limited dependent variables. Econometrica, 26(1), 24–36.

Tse, R. Y., Hui, E., & Chan, C. (2001). On the competitive land market: Evidence from Hong Kong. Review of Urban & Regional Development Studies, 13(1), 46–61.

Tse, M. K., Pretorius, F. I., & Chau, K. (2011). Market sentiments, winner’s curse and bidding outcome in land auctions. The Journal of Real Estate Finance and Economics, 42(3), 247–274.

Turnbull, G. K., & Sirmans, C. (1993). Information, search, and house prices. Regional Science and Urban Economics, 23(4), 545–557.

Turnbull, G. K., Sirmans, C., & Benjamin, J. D. (1990). Do corporations sell houses for less? A test of housing market efficiency. Applied Economics, 22(10), 1389–1398.

Vickrey, W. (1961). Counterspeculation, auctions, and competitive sealed tenders. Journal of Finance, 16(1), 8–37.

Whited, T. M., & Wu, G. (2006). Financial constraints risk. Review of Financial Studies, 19(2), 531–559.

Wooldridge, J. M. (2010). Econometric analysis of cross section and panel data. Cambridge: MIT Press.

Yao, H., & Pretorius, F. (2014). Demand uncertainty, development timing and leasehold land valuation: Empirical testing of real options in residential real estate development. Real Estate Economics, 42(4), 829–868.

Zheng, C. Z. (2001). High bids and broke winners. Journal of Economic Theory, 100, 129–171.

Author information

Authors and Affiliations

Corresponding author

Additional information

Editors: SE Ong, KW Chau, Hongyu Liu

Appendices

Appendix 1

Land Auctions in Hong Kong

Hong Kong manages its land resources through a leasehold system where the state owns all land (with trivial exceptions), and alienates land through long leases. Land prices thus reflect the value of long land leases (see Yao and Pretorius 2014), with vacant or (re)developable land released to the market mostly through auction or tender (for example, following lease maturation and reentry, or occasional release of previously unalienated or newly reclaimed land). Detailed auction information is made public well before auctions (typically at least four weeks before the auction date, and two to three months for some major and complicated land sales). The Government sets a reserve price; only bids larger than the reserve price would typically be considered at auction. The auction process is transparent and the bidder that offers the highest price wins the auction (for insight into the nature and complex dynamics of land auctions in Hong Kong, see Tse et al. 2011).

Land auctions in Hong Kong provide a good experiment to test the impact of financial constraints on auction outcomes, for at least three reasons. First, the auctions are highly transparent and the data from auctions are well documented, with information on the auctioned land, participants and bidding strategies. Second, urban Hong Kong is almost exclusively high-rise and extremely densely developed, with strict constraints on release of additional developable land. Industry participation in a high-rise, high-density environment demands high capital resources for typically large-scale/value projects (typically in excess of US$1bn). This reflects very high barriers to entry and advantages to leading developers,Footnote 12 often presented as causal to the industry’s concentration. Development in Hong Kong is often considered to be oligopolistic but stable, with some 14 big developers in Hong Kong accounting for most of total activity and with genuine contestability restricted only to smaller developments. The top four developers - Sun Hung Kai Properties, Cheung Kong, Kerry Properties and Sino Land - accounted for some 70% of all new flats sold in the first half of 2012 alone (Kwok 2012). Thus the developers’ ability to pay (the capital resources advantage) may be substantially reflected in auction outcomes, but the significant size and value of sites at auction also makes joint bidding an important financial and development risk-sharing strategy. Most developers who obtain land from auctions in our sample are thus large listed companies, and thus insight into their financial constraints and financial strength, also prior to auctions, can be obtained from public sources. Third, typically the Government sets a deadline for successful purchasers to pay the balance of the auction price in one lump sum, within 28 days after auction date, and commence development shortly after winning the auction and complete the project within a set time constraint (Audit Commission 2001), a common constraint in many markets. This indicates a substantial commitment of corporate capital at the time of the auction as the cost structure of development in Hong Kong is heavily weighted towards the cost of land, sufficiently so potentially to influence bidding if there is are both bidders with binding constraints and ones that bid strategically. The Auction rules allow Government to repossess the site if a winning company bids more than its ability to pay and defaults after winning (Zheng 2001).

Appendix 2

Rights and permissions

About this article

Cite this article

Shen, J., Pretorius, F. & Chau, K.W. Land Auctions with Budget Constraints. J Real Estate Finan Econ 56, 443–471 (2018). https://doi.org/10.1007/s11146-017-9618-z

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-017-9618-z