Abstract

We investigate the effect of Eurosystem asset purchase programmes (APP) on the monthly yields of 10-year sovereign bonds for 11 euro area sovereigns during January–December 2020. The analysis is based on time-varying coefficient methods applied to monthly panel data covering the period 2004m09–2020m12. During 2020, APP contributed to an average decline in yields estimated in the range of 58–76 bps. In December 2020, the effect per EUR trillion ranged between 34 bps in Germany and 159 bps in Greece. Stronger effects generally display diminishing returns. Our findings suggest that a sharp decline in the size of the APP in the aftermath of the COVID-19 crisis could lead to very sharp increases in bond yields, particularly in peripheral countries. The analysis additionally reveals a differential response to global risks between core and peripheral countries, with the former enjoying safe-haven benefits. Markets’ perceptions of risk are found to be significantly affected by credit ratings, which is in line with recent evidence based on constant parameter methods.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The ESCB’s asset purchase programme (APP) is part of a package of non-standard monetary policy measures initiated in mid-2014 in the context of the historically low rates following the global financial crisis. Outright purchases, often referred to as quantitative easing (QE), have been employed also by other major central banks, namely the Federal Reserve Board, the Bank of England and the Bank of Japan. The Statute of the ESCB (Article 18.1) provides for the purchase of instruments such as government bonds, as long as they are bought on the secondary market from investors and not directly from Member States. The Governing Council expects asset purchases “to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates”.

The Eurosystem’s APP was expanded following the COVID-19 outbreak, with the launch of the pandemic emergency purchase programme (PEPP) in March 2020. The PEPP is a temporary asset purchase programme of private and public sector securities, with an initial envelope of €750 billion, which was subsequently increased by €600 billion in June and by a further €500 billion in December, bringing the total to €1,850 billion. The Governing Council “will terminate net asset purchases under the PEPP once it judges that the COVID-19 crisis phase is over, but in any case not before the end of March 2022”.

In view of the stated intention to eventually terminate these policies, quantifying the effect of APP is important for assessing the likely implications of its termination, or reversal. A large body of literature has documented sizeable and persistent effects of central bank asset purchase programmes on various financial market variables. Here we study the effect on the 10-year sovereign bond yields of 11 euro area sovereigns.Footnote 1 The analysis is based on time-varying parameter methods, which allow us to zoom in to the period between January and December 2020, covering the outbreak of the COVID-19 pandemic and the launch of the PEPP. Earlier econometric analyses of panel data using time-varying coefficient methods like Bernoth and Erdogan (2012) tend to involve smaller sets of explanatory variables and permit a smaller degree of heterogeneity, while the time-varying parameters tend to follow a-theoretical specifications, such as a random walk process in D’Agostino and Ehrmann (2014). More recently, Paniagua et al. (2017) and Monteiro and Vasicek (2019) allow for greater heterogeneity and provide for greater economic interpretation of the variation exhibited by the time-varying parameters. While the former authors focus on spreads against Germany, the latter look directly at sovereign bond yields and expand the set of explanatory variables with, inter alia, the inclusion of APP. Our approach follows closely Paniagua et al. (2017) and Monteiro and Vasicek (2019).

We differ from Paniagua et al. (2017) in that we don’t look at spreads but like Monteiro and Vasicek (2019) we focus on individual sovereign bond yields, allow for greater heterogeneity in the specification of the time-varying coefficients and use an extended set of explanatory variables that includes APP. We differ from Monteiro and Vasicek (2019) by expanding further the explanatory variables through the inclusion of credit ratings, while allowing perceptions of risk to be driven by differences in credit rating compared to the anchor country, Germany, as well as by macroeconomic misalignment. Also, we employ a one-step estimation procedure, instead of the two-step procedure employed by Monteiro and Vasicek (2019).

The empirical analysis is based on monthly panel data covering the period 2004 m09 to 2020 m12 for a non-trivial set of macroeconomic, fiscal and financial explanatory variables and distinguishes between influences related to fundamentals and markets’ perceptions of risk. During 2020, APP is estimated to have contributed to an average decline in euro area 10-yr sovereign bond yields in the range of 58–76 bps, depending on the model. In December 2020, the effect per EUR trillion ranged between 34 bps in Germany and 159 bps in Greece. In line with evidence obtained by event studies, such as Fendel and Neugebauer (2020), stronger marginal effects are concentrated in peripheral countries and generally display diminishing returns.Footnote 2 These estimates indicate that a sharp decline in the size of the ECBs asset purchase programmes in the aftermath of the COVID-19 crisis could lead to very sharp increases in bond yields, particularly in peripheral countries.

The analysis provides also a number of additional insights. In line with evidence reported by Paniagua et al. (2017), coefficients are found to exhibit very persistent deviations from their long-term mean, which highlights the limitations of constant parameter methods. We also find evidence of a differential response to global risks between core and peripheral countries, with the former enjoying safe-haven benefits. Markets’ perceptions of risk are found to be significantly affected by credit ratings, which is in line with recent evidence based on constant parameter methods by Georgoutsos and Migiakis (2018) and Malliaropoulos and Migiakis (2018).

Section 2 presents the econometric framework and data, Sect. 3 discusses the empirical findings and forecast performance, Sect. 4 includes robustness tests, and Sect. 5 concludes.

2 Analytical framework and data

2.1 TVP model

The literature on the determinants of sovereign bond yields in the euro area assigns significant roles to both fundamentals and market perceptions of risk.Footnote 3 Fundamentals include variables capturing (expectations of) country-specific fiscal and macroeconomic performance, asset characteristics like liquidity, as well as horizontal influences, such as global risk appetite, or the common monetary policy. As such, they represent a set of generally quantifiable information that markets price-in when determining the yield of sovereign bonds. Market perceptions, on the other hand, refer to the weight that markets place at each point in time on the different fundamental sources of risk. As such, they may vary through time and across countries. TVP models provide the means to disentangle the role between fundamentals and market perceptions, by explicitly modelling the variation of perceived risk.

Drawing on Paniagua et al. (2017) and Monteiro and Vasicek (2019), we formulate the following TVP model:

where the dependent variable \({y}_{i,t}\) is the monthly 10-year government bond yield for country i during month t. The explanatory variables are as follows: \({rf}_{t}\) is the short-term risk-free rate measured by the EONIA overnight rate; \({slope}_{t}\) denotes the spread between the 10-year and the 1-year bonds of AAA-rated euro area sovereigns; \({debt}_{i,t}\) is the debt-to-GDP ratioFootnote 4; \({ur}_{i,t}\) is the unemployment rate; \({risk}_{t}\) denotes a global risk factor measured by the logged VIX indexFootnote 5; \({liq}_{i,t-1}\) captures the role of liquidity of the assets considered and is measured as country i’s volume of gross debt in euros relative to the euro area total; \({APP}_{t}\) denotes the value (in EUR trillions) of securities held by the Eurosystem for monetary policy purposes; \({rating}_{i,t-1}\) denotes the average credit rating by Moody’s, Fitch and S&P.Footnote 6 The error term \({\varepsilon }_{i,t}\sim N(0,{\sigma }_{\varepsilon }^{2})\) is a country-specific residual with homogeneous variance across countries. A positive effect on the 10-year bond yield may generally be anticipated from increases in the risk-free rate, the yield slope, debt and the unemployment rate, while a negative effect can be expected from higher liquidity, increased APP and improved rating. The effect of global risk is more ambiguous, as the literature reports evidence of both positive and negative feedbacks, the latter denoting benefits from “flight to safety”.Footnote 7

The time-varying parameters \({\beta }_{i,t}^{j}\) quantify the sensitivity of yields to variable j, denoting markets’ pricing of risk j. They are modelled as potentially persistent country-specific deviations from a common steady state:

where \(\rho\) is a constant autoregressive coefficient, common across countries, determining the speed of convergence to the common steady state \(\overline{{\beta }^{j}}\). The term \({w}_{i,t}^{j}\) introduces country-specific influences modelled as follows:

where \({\mu }^{j}\) is a homogeneous constant parameter and \({u}_{i,t}^{j}\sim N(0,{\sigma }_{u}^{2})\) is a country-specific disturbance with common variance across countries and \({E(\varepsilon }_{i,t},{u}_{i,t}^{j})=0\). The variable \({cyas}_{i,t}\) permits a permanent departure from the common steady state and provides an economically meaningful driver of markets’ perceptions of risk. In Paniagua et al. (2017) and Monteiro and Vasicek (2019), \({cyas}_{i,t}\) captures macroeconomic misalignment, measured by differences in GDP growth compared to the anchor country, Germany. The underlying reasoning is that in a monetary union macroeconomic misalignment undermines the effectiveness of the common monetary policy, which increases the exposure to risk. Here we use two different versions.

In the first version (model 1), \({cyas}_{i,t}\) measures differences in unemployment rates compared to Germany. The difference in unemployment rates has been preferred over the difference in growth rates because it captures a broader kind of macroeconomic misalignment beyond cyclical effects, such as structural differences in the functioning of product and labour markets. In the second version (model 2), \({cyas}_{i,t}\) measures differences in credit ratings compared to Germany. This definition permits markets’ perceptions of risk to be affected by credit ratings, which is in line with recent evidence based on constant parameter methods by Georgoutsos and Migiakis (2018) and Malliaropoulos and Migiakis (2018).

In line with Monteiro and Vasicek (2019), country-specific influences are not included in the estimation of \({\beta }_{t}^{rf}\) and \({\beta }_{t}^{slope}\), which are common across countries by setting \({\mu }^{j}=0\) and \({u}_{i,t}^{j}={u}_{t}^{j}\). The same treatment applies here also to \({\beta }_{t}^{rating}\). The chosen specification of the time-varying parameters is quite general and encompasses other popular alternatives, such as the driftless random walk, which arises as a special case for \(\rho =1\) and \({\mu }^{j}=0\). Furthermore, unlike a-theoretical alternatives, the chosen specification allows for an economic interpretation of the factors driving markets’ perceptions of risk through \({cyas}_{i,t}\).

2.2 Data and caveats

All series are collected for the following 11 members of the euro area: BE, DE, IE, GR, ES, FR, IT, NL, AT, PT, FI. We use monthly observations, which are commonly available during 2004m09–2020m12. Exceptions are debt, the unemployment rate and liquidity, which are available at quarterly frequency and only until 2020Q3. The last quarter of 2020 has been completed based on the winter forecast of the European Commission and the December 2020 BMPE forecast of the Eurosystem. The quarterly series have been transformed into monthly frequency using a Litterman interpolation.Footnote 8 Figure 1a and b provides plots of all variables over the common sample period (left column) and during 2020 (right column). Descriptive statistics and unit root tests are reported in Tables 1 and 2, respectively.

Data plots for the full sample (left panel) and in 2020 (right panel)

There are potentially important caveats, most of which are discussed by Monteiro and Vasicek (2019). First, 10-year bond yields are likely to reflect expectations on the future value of macroeconomic aggregates, rather than historical realizations. However, the use of historical data is a common compromise, as high-frequency data on long-term expectations are typically not available.Footnote 9 Second, there are endogeneity concerns, particularly regarding liquidity and rating. This is because sovereign risk can cause liquidity to dry up, just as liquidity shortages can cause yields to rise. Similarly, credit ratings can be expected to affect market perceptions of risk, just as market developments can have an effect on credit worthiness. We follow Monteiro and Vasicek (2019) in using the first lag in order to insulate liquidity and ratings from contemporaneous feedbacks from sovereign yields.

Endogeneity can be expected to be less of a concern in the case of the risk-free rate and slope, which are forward-looking and can be expected to mainly reflect inflation and monetary policy, rather than contemporaneous sovereign yields. Debt may equally be argued to be effectively exogenous to contemporaneous yields, the effect of which can take time before being reflected in the debt stock. Likewise, labour market rigidities largely rule out a contemporaneous response of unemployment to bond yields. The use of VIX, a US-based measure of market volatility, has been preferred over an EU-based risk factor in order to mitigate the contemporaneous feedback of euro area yields. Finally, APP is not designed to respond contemporaneously to specific developments in sovereign bond yields and evolves according to pre-defined rules.

One additional caveat concerns the possible bias from collinearity under the specific set-up of model 2. We discuss this explicitly and provide a dedicated robustness check in Sect. 4.

3 Empirical results

The benchmark TVP model in Eqs. (1)-(3) has been estimated by Kalman filter over the set of commonly available data points covering the period 2004 m09–2020 m12 using the state-space object in EViews versions 10 & 12.Footnote 10 We report full estimates and charts for the second version (model 2) of the benchmark TVP model outlined in Sect. 2. Estimates are also reported and discussed for model 1, but the charts have been omitted to economize on space.Footnote 11

3.1 Estimated parameters of the TVP model

The first two columns of Table 3 report the estimated parameters for models 1 and 2. Recall that the difference between the two models concerns the idiosyncratic terms \({\mu }^{j}{cyas}_{i,t}\) in Eq. (3). In model 1, \({cyas}_{i,t}\) measures differences in unemployment rates compared to Germany. In model 2, \({cyas}_{i,t}\) measures differences in credit ratings compared to Germany.

The estimates of models 1 and 2 are very similar, except for the opposite signs of parameters \({\mu }^{j}\), which reflect the two different definitions of \({cyas}_{i,t}\). The autoregressive coefficient \(\rho\) in the specification of the time-varying coefficients in Eq. (2) is estimated very close to unity (0.93), which indicates that the time-varying coefficients are subject to very persistent deviations from their long-term mean. This highlights the limitations of constant parameter methods, which rely on the assumption that coefficients are on average at their time-invariant mean value.Footnote 12 The residuals \({\varepsilon }_{i,t}\) in Eq. (1) are plotted in Fig. 15 and appear to be reassuringly mean-reverting, as is more formally confirmed by the panel unit root tests reported in the lower section of Table 2. The flexible structure of TVP models typically allows for a very good fit, resulting in a very small absolute size of residuals. Nevertheless, there appear to be comparatively large outliers during the sovereign debt crisis, particularly for peripheral countries that received EU/IMF financial assistance, which speak against the homogeneity of the variance \({\sigma }_{\varepsilon }^{2}\).

Time-varying intercepts \({\beta }_{i,t}^{intercept}\). Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany. The estimated time-varying coefficients \({\beta }_{i,t}^{j}\) are depicted by solid lines. Dotted lines denote two standard error bands

Models 1 and 2 both generate statistically significant values of \({\mu }^{j}\) for public debt, global risk and APP, the latter more clearly in the case of model 2. A statistically significant value of \({\mu }^{j}\) indicates that the evolution of the time-varying coefficient \({\beta }_{i,t}^{j}\) is affected by the country-specific influences captured by \({cyas}_{i,t}\). In the case of model 1, the positive values of \({\mu }^{debt}\) and \({\mu }^{risk}\) indicate that for given levels of public debt and global risk, markets demand a premium when the unemployment rate exceeds that of Germany, thereby penalizing macroeconomic misalignment. The negative value estimated for \({\mu }^{APP}\) similarly indicates that markets’ perceive a given level of APP to reduce more strongly the risk of sovereigns with higher unemployment than Germany. In the case of model 2, the negative values of \({\mu }^{debt}\) and \({\mu }^{risk}\) indicate that for given levels of public debt and global risk, markets will charge a premium for credit ratings below that of Germany. The positive value estimated for \({\mu }^{APP}\) similarly indicates that markets’ perceive a given level of APP to reduce more strongly the risk of sovereigns with credit rating below that of Germany.Footnote 13

Parameters \(\overline{{\beta }^{rf}}\), \(\overline{{\beta }^{slope}}\) and \(\overline{{\beta }^{rating}}\) report the steady-state values of the time-varying coefficients on the risk-free rate, the yield curve slope and credit rating, respectively, which are common across countries. The remaining \(\overline{{\beta }^{j}}\)’s can only be interpreted as steady-state values, provided \({cyas}_{i,t}=0\), i.e. under perfect alignment with Germany’s unemployment rate (model 1) or credit rating (model 2). In effect, \(\overline{{\beta }^{j}}\)’s other than \(\overline{{\beta }^{rf}}\), \(\overline{{\beta }^{slope}}\) and \(\overline{{\beta }^{rating}}\) report the steady states for Germany. One needs to be aware that, while the \(\overline{{\beta }^{j}}\)’s are informative regarding the properties of the \({\beta }_{i,t}^{j}\)’s, they can be quite different from the estimated realizations of the time-varying coefficients. This is immediately apparent for \({cyas}_{i,t}\ne 0\). However, even for \({cyas}_{i,t}=0\), the very high persistence of shocks reported by the estimated value of ρ (0.93) can cause the \({\beta }_{i,t}^{j}\)’s to exhibit prolonged deviations from the estimated steady states.

Plots of the estimated time-varying coefficients \({\beta }_{i,t}^{j}\) are reported in Figs. 2, 3, 4, 5, 2, 6, 7 and 8, along with two standard error bands. There is considerable heterogeneity across countries and variation through time, particularly in coefficients with significant idiosyncratic influences through \({cyas}_{i,t}\). We generally find statistically significant positive values for the coefficients on the risk-free rate, the yield slope, the unemployment rate and in peripheral countries also debt. However, the effect of debt tends to be less statistically significant, or even negative, for core countries with high credit rating, particularly in model 2 (Fig. 3). This is caused by the small and insignificant estimate of \(\overline{{\beta }^{debt}}\), which denotes the steady state under perfect alignment with Germany. The effect of debt increases and becomes more strongly significant for countries that are less well aligned with Germany and exhibit sustained divergences from \(\overline{{\beta }^{debt}}\) through a sizeable \({cyas}_{i,t}\).

Time-varying coefficients on debt \({\beta }_{i,t}^{debt}\). Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany. The estimated time-varying coefficients \({\beta }_{i,t}^{j}\) are depicted by solid lines. Dotted lines denote two standard error bands

Time-varying coefficients on the unemployment rate \({\beta }_{i,t}^{ur}\). Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany. The estimated time-varying coefficients \({\beta }_{i,t}^{j}\) are depicted by solid lines. Dotted lines denote two standard error bands

Time-varying coefficients on global risk \({\beta }_{i,t}^{risk}\). Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany. The estimated time-varying coefficients \({\beta }_{i,t}^{j}\) are depicted by solid lines. Dotted lines denote two standard error bands. Positive values of \({\beta }_{i,t}^{risk}\) indicate exposure to global risks, while negative values indicate safe-haven benefits

Time-varying coefficients on liquidity \({\beta }_{i,t}^{liq}\). Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany. The estimated time-varying coefficients \({\beta }_{i,t}^{j}\) are depicted by solid lines. Dotted lines denote two standard error bands

Time-varying coefficients on APP \({\beta }_{i,t}^{APP}\). Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany. The estimated time-varying coefficients \({\beta }_{i,t}^{j}\) are depicted by solid lines. Dotted lines denote two standard error bands

Time-varying coefficients on the risk-free rate \({\beta }_{i,t}^{rf}\), the yield slope \({\beta }_{i,t}^{slope}\) and credit rating \({\beta }_{i,t}^{rating}\). Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany. The estimated time-varying coefficients \({\beta }_{i,t}^{j}\) are depicted by solid lines. Dotted lines denote two standard error bands

Global risk is consistently found to have a differentiated effect between euro area members, as depicted in Fig. 5. Positive values indicate exposure to global risk, as increases in global uncertainty lead to increases in yields. Negative values denote declining yields in the face of increased global uncertainty, i.e. benefits from flight to safety. Peripheral economies are exposed to global risks paying a positive premium, while highly rated core countries enjoy safe-haven benefits. The exposure of peripheral countries to global risk increased substantially since the early 2010s, when some of them still enjoyed a safe-haven status. Also, in core countries with the exception of Germany, safe-haven benefits have been declining, as the estimated coefficients have tended to become less negative.

Negative effects are generally estimated for rating, liquidity and APP. As illustrated in Fig. 7, the effect of APP in both models is strongly significant and displays large heterogeneity across countries. More sizeable values are estimated for peripheral countries, which, however, tend to diminish over time. Detailed estimates for 2020 are reported in Table 4. In December 2020, the estimated effect per EUR trillion ranged between 34 bps in Germany and 159 bps in Greece. These estimates suggest that a sharp decline in the size of the APP in the aftermath of the COVID-19 crisis could lead to very sharp increases in bond yields, particularly in peripheral countries.

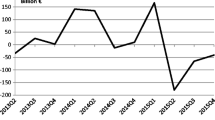

3.2 Decomposition of changes in yields in 2020

Figure 9 depicts the estimated contribution of each determinant to the change in the yields between January and December 2020. The change in yields, denoted by the blue dots, indicates that during 2020 there has been a decline for all countries, which was more pronounced for Italy and Greece, where yields declined by around 80 basis points. The increasing effects mainly from fiscal and macroeconomic influences were more than compensated primarily by the decreasing effect of the asset purchase programmes (yellow bars), with the more sizeable benefits estimated for peripheral countries (GR, IT, ES and PT). While the overall annual effect is revealing, it is particularly interesting to examine more closely the monthly changes over the course of the year.

Decomposition of changes in 10-yr bond yields between January and December 2020. Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany

Figure 10 depicts changes on a monthly basis. Apart from the sizeable influences from debt (red bars) and the APP (yellow bars), one notes that there are also significant influences from global volatility (orange), mainly in March, which are more or less netted out in subsequent months, and are therefore not picked up by the yearly decomposition. It should be pointed out that each bar denotes the estimated contribution of the product \({\beta }_{i,t}^{j}{x}_{i,t}^{j}\) of each explanatory variable \({x}_{i,t}^{j}\) with its corresponding time-varying coefficient \({\beta }_{i,t}^{j}\). In constant parameter models, this is by definition equal to the change in variable \({x}_{i,t}^{j}\). In the context of time-varying coefficients, however, a change in the product \({\beta }_{i,t}^{j}{x}_{i,t}^{j}\) may reflect changes in both \({\beta }_{i,t}^{j}\) and \({x}_{i,t}^{j}\). In order to reveal the full narrative estimated by the model, we decompose further the estimated effects in line with Bernoth and Erdogan (2012), focusing on debt, global volatility and APP.

Decomposition of monthly changes in 10-yr bond yields during 2020. Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany

Figure 11 isolates the monthly effects of debt and decomposes them into the part due to changes in the level of debt (bars without markers) and the part due to changes in the time-varying coefficient (bars with markers). One notices that the effects are dominated by changes in the time-varying coefficient, which denotes changes in market sensitivity to debt, or equivalently in markets’ pricing of debt risk. During the first months of restrictions in response to the pandemic (March, April, May), the sizeable increasing effects on the yields do not so much reflect increases in the level of debt, but instead indicate an increased market perception of debt risk, which was partly corrected in June and in subsequent months.

Decomposition of debt effects. Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany. Monthly changes in the product \({\beta }_{i,t}^{j}{\mathrm{x}}_{i,t}^{j}\) are decomposed into the part due to changes in the level of variable \({\mathrm{x}}_{i,t}^{j}\) (bars without markers) and the part due to changes in the time-varying coefficient \({\beta }_{i,t}^{j}\) (bars with markers)

The opposite picture emerges in the case of global risks, depicted in Fig. 12. In this case, the effects are dominated by changes in the level of global uncertainty (bars without markers), while the pricing of global risks remained unchanged, as indicated by the absence of bars with markers. What is particularly interesting in this case is the difference in the sign of the effect across countries. The large increases in global uncertainty in February and mainly in March, as measured by the VIX index, had a considerable increasing effect on the yields of peripheral countries (GR, IT, ES, PT), while a decreasing effect is estimated for core countries (DE, NL, FI, AT and to a smaller extent FR, BE). This illustrates the safe-haven status enjoyed by core countries and reflects the opposite signs in the estimated time-varying coefficients on global risk compared to peripheral countries reported in Fig. 5.

Decomposition of global risk effects. Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany. Monthly changes in the product \({\beta }_{i,t}^{j}{\mathrm{x}}_{i,t}^{j}\) are decomposed into the part due to changes in the level of variable \({\mathrm{x}}_{i,t}^{j}\) (bars without markers) and the part due to changes in the time-varying coefficient \({\beta }_{i,t}^{j}\) (bars with markers)

Turning to the effects of the APP in Fig. 13, one observes clear negative influences over the whole year, which are driven by the increasing level of APP (bars without markers). There are however, small but positive contributions over the whole year coming from the time-varying coefficient (bars with markers) for some of the countries that record the largest benefits from APP (GR, ES, PT), which points to the existence of decreasing returns. This is illustrated more clearly in Fig. 7 depicting the estimated evolution of the time-varying coefficient on APP, which has become gradually less negative in the cases of large beneficiaries over a number of years.

Decomposition of APP effects. Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany. Monthly changes in the product \({\beta }_{i,t}^{j}{\mathrm{x}}_{i,t}^{j}\) are decomposed into the part due to changes in the level of variable \({\mathrm{x}}_{i,t}^{j}\) (bars without markers) and the part due to changes in the time-varying coefficient \({\beta }_{i,t}^{j}\) (bars with markers)

3.3 Forecast performance

We have looked into the predictive performance of the estimated models. In all cases, estimation ends in December 2018 and static, one-period-ahead forecasts have been performed out-of-sample until December 2020, a total of 24 periods. Table 5 ranks the various models according to RMSE. TVP model 1 και TVP model 2 are the models discussed above, estimated until the end of 2018. AR(1) is a panel autoregression with fixed effects estimated by OLS. VAR is a panel VAR treating as endogenous all the variables of the TVP models in first differences, using 12 lags, fixed effects and seasonal dummies. A direct comparison of the TVP models with the AR(1) and the VAR is not on equal terms. AR(1) and VAR predictions for period t + 1 are based on information available in period t. Due to the presence of contemporaneous terms, however, the TVP models’ prediction for period t + 1 requires information on t + 1. In order to level the playing field, the TVP models have been re-estimated replacing the contemporaneous terms with lagged terms. These reformulated models are labelled “lagged”. Note that the lagged versions of the TVP models use the third lag of debt, unemployment and liquidity. The reason for doing so is that monthly observations for these variables were interpolated from quarterly data points. Hence, the first two months in each quarter were constructed using information about the third. Taking the third lag of these variables ensures that predictions are based strictly on past information. This is more restrictive compared to the VAR, which uses all lags 1 through 12 for all variables. In all cases, the TVP models clearly perform better than the AR(1), while the VAR is found to perform substantially worse.

Figure 14 reports actual yields (black), the forecasts obtained from TVP model 2 lagged (blue) with 68% confidence bands (blue dashed), forecasts from the AR(1) (red) and the VAR (green). One notices that the big errors of the VAR are concentrated mainly in 2020. This coincides with the sharp increases in global risk measured by the VIX index in the first months of 2020, which according to the TVP models had opposite effects in core and peripheral countries, which cannot be captured under the assumption of parameter homogeneity.

Out-of-sample 1-period ahead static forecasts during 19m01-20m12. Notes: All estimation ends in 2018m12. In model 2 the variable \({cyas}_{i,t}\) measures differences in credit ratings compared to Germany. A lagged version of models 2 is estimated using the third lag of debt, ur and liq and the first lag of all remaining regressors. AR(1) is an OLS panel autoregression of order 1 with cross-section fixed effects. VAR denotes a symmetric 9-variable VAR model with 12 lags involving the first differences of y, rf, slope, debt, ur, risk, liq, APP and rating. It is estimated via OLS using cross-section fixed effects and monthly seasonal dummies

Residuals \({\varepsilon }_{i,t}\). Notes: Based on model 2, which allows for idiosyncratic influences on the time-varying coefficients based on differences in credit ratings compared to Germany

4 Robustness checks

4.1 Collinearity of \({rating}_{i,t}\) and \({cyas}_{i,t}\) in model 2

In model 2, \({cyas}_{i,t}\) is defined as the difference in rating compared to DE, which in principle is a different variable from \({rating}_{i,t}\). However, as illustrated in Fig. 1, the rating for DE has been constant over the whole sample and hence, the two variables (the spread of ratings and \({rating}_{i,t}\)) are perfectly collinear as they only differ by a constant. Note that this does not pose a problem for model 1 where \({cyas}_{i,t}\) is defined as the difference in \({ur}_{i,t}\). This is because the \({ur}_{i,t}\) for DE, as for every country, has not been constant. While the difference in \({ur}_{i,t}\) compared to DE is likely to be correlated with \({ur}_{i,t}\), they will not be perfectly collinear.

The fact that \({cyas}_{i,t}\) and \({rating}_{i,t}\) are perfectly collinear is not problematic for any beta other than \({\beta }_{i,t}^{intercept}\). The reason being, that for all betas other than \({\beta }_{i,t}^{intercept}\), \({cyas}_{i,t}\) does not enter linearly the equation for \({y}_{i,t}\) as an independent variable, but as an interaction term with variable j (debt, risk, etc.). Through \({\beta }_{i,t}^{intercept}\), however, \({cyas}_{i,t}\) enters the equation as an independent linear regressor of \({y}_{i,t}\), just as \({rating}_{i,t}\). To check the sensitivity of the estimates of model 2 to this, the model is reformulated to exclude ratings from \({\beta }_{i,t}^{intercept}\) by setting \({\mu }^{intercept}=0\) and is denoted as model 2a. As reported in Table 3, the estimates of model 2a are both qualitatively and in most part also quantitatively unchanged compared to model 2. Similarly, all charts remain virtually unaffected.

4.2 Lagged dependent variable

The empirical framework employed here does not involve lagged endogenous variables in Eq. (1), as persistence is captured by the time variation of risk perception in Eq. (2), in line with Paniagua et al. (2017). However, in constant parameter applications, persistence is frequently captured by lagged endogenous variables.Footnote 14 Model 2b in Table 3 provides a robustness check for the inclusion of a lagged dependent variable. The inclusion of \({y}_{i,t-1}\) as an additional explanatory variable in Eq. 1 does not appear to affect the baseline estimates in any major way. However, the model becomes severely misspecified, as indicated by the non-stationary residuals \({\varepsilon }_{t}\) detected by the ADF tests in Table 2.

4.3 Country-specific purchases of state bonds

As discussed in the previous section, \({APP}_{t}\) was found to have a statistically significant negative effect \({\beta }_{i,t}^{APP}\) on sovereign bond yields, which is more pronounced in low-rated peripheral countries and most notably in GR. One should recall that the variable \({APP}_{t}\) included in Eq. (1) is common across countries and denotes the value (in EUR trillions) of securities held by the Eurosystem for monetary policy purposes. While Greek government bonds are included in the Pandemic Emergency Purchase Programme (PEPP) that was launched in 2020, they were not eligible for the earlier Public Sector Purchase Programme (PSPP). The statistical significance of the negative \({\beta }_{i,t}^{APP}\) for GR, however, applies also in the years before 2020, as depicted in Fig. 7.

One possible interpretation could be that \({\beta }_{i,t}^{APP}\) captures not only the effect of actual purchases, but also markets’ perception of systemic risk. A larger envelope of asset purchases represents a stronger commitment to the integrity of the common currency and thus lower systemic risk. One would expect the most vulnerable countries, such as GR to benefit the most from lower systemic risk, which would explain the statistical significance of \({\beta }_{i,t}^{APP}\) for GR in the years prior to PEPP, when Greek bonds were not eligible for inclusion in PSPP. Such an interpretation would be in line with the evidence reported by event studies, such as Fendel and Neugebauer (2020), who find that announcements of asset purchase programmes prior to PEPP had sizeable negative effects on the yields of Greek 10-year sovereign bonds.

We investigate more formally the robustness of the estimated \({\beta }_{i,t}^{APP}\) by including as an additional explanatory variable the value (in EUR billion) of the own state bonds held by each national central bank through PSPP and PEPP. The ECB provides a monthly breakdown for the PSPP and a bi-monthly breakdown for the PEPP, although aggregates are available at a monthly frequency. We construct monthly values for PEPP by applying the bi-monthly shares to the monthly aggregates. Detailed estimates are reported in Table 3 under model 2c. The extended model produces strongly insignificant parameters for the time-varying coefficient of the own state bonds, reported in the last two rows, while all other parameters remain virtually unchanged. The steady state \(\overline{{\beta }^{APP}}\) is estimated less accurately, but the time-varying coefficient \({\beta }_{i,t}^{APP}\) remains strongly significant for all countries. This validates the estimates reported in the main analysis for the effect of APP and speaks in favour of the interpretation offered above, namely, that markets perceive asset purchases as an overall commitment of monetary authorities to the integrity of the common currency that reduces systemic risk.

4.4 Alternative measure of global risk

Following a suggestion by two anonymous referees, we have additionally checked the robustness of the benchmark model by replacing the (log) VIX with the (log of) the BAA spread as an alternative measure of global risk.Footnote 15 The estimates are reported in the last column of Table 3 (model 2d), and they are qualitatively and in most part also quantitatively unchanged compared to the benchmark (model 2). This is very much in line with the clear positive correlation of the two measures of uncertainty over the whole sample. Differences are very limited and mainly concern the larger absolute size of the estimated steady state \(\overline{{\beta }^{risk}}\), as (log) BAA spread is on average approximately three times smaller than (log) VIX. The use of the BAA spread also increases the statistical significance of the estimated steady state \(\overline{{\beta }^{APP}}\). The replacement of (log) VIX by (log) BAA spread does not affect the presence of differentiated effects of global risk across countries, with highly rated sovereigns enjoying safe-haven benefits and lower rated members paying a premium.

5 Conclusions

We investigated the effect of Eurosystem asset purchase programmes (APPs) on the 10-year sovereign bond yields of 11 euro area sovereigns. The analysis is based on time-varying parameter methods, which allow us to zoom in to the period between January and December 2020, covering the outbreak of the COVID-19 pandemic and the launch of the Pandemic Emergency Purchase Programme. The employed empirical models include a non-trivial set of macroeconomic, fiscal and financial explanatory variables and distinguish between influences related to fundamentals and markets’ perceptions of risk. During 2020, APP is estimated to have contributed to an average decline in euro area 10-yr sovereign bond yields in the range of 58–76 bps, depending on the model. The cross-country average masks considerable heterogeneity, with APP contributing to the annual decline from 36 bps in Germany to 143 bps in Greece. The marginal effect of APP is significantly affected by country-specific conditions and varies through time. In December 2020, the effect per EUR trillion ranged between 34 bps in Germany and 159 bps in Greece. Stronger marginal effects are concentrated in peripheral countries and generally display diminishing returns. These estimates indicate that a sharp decline in the size of the ECBs asset purchase programmes in the aftermath of the COVID-19 crisis could lead to very sharp increases in bond yields, particularly in peripheral countries.

While the main focus is placed on APP, the analysis provides a number of additional insights. Coefficients are found to exhibit very persistent deviations from their long-term mean. This is in line with evidence reported in the literature and highlights the limitations of constant parameter methods, which rely on the assumption that coefficients are on average at their time-invariant mean. A differential response to global risks is identified between core and peripheral countries, with the former enjoying safe-haven benefits. Safe-haven status can vary through time and is found to depend significantly on misalignment compared to the anchor country Germany, with respect to the unemployment rate and credit rating. Markets’ perceptions of risk are found to be significantly affected by credit ratings, which is in line with recent evidence based on constant parameter methods. The sensitivity of bond yields to the debt level can be very volatile and is significantly affected by country-specific conditions. This is not captured by simple threshold effects typically used in risk assessment exercises.

Notes

Belgium, Germany, Ireland, Greece, Spain, France, Italy, Netherlands, Austria, Portugal and Finland.

Focusing on the four largest euro area members (Germany, France, Italy and Spain), Corradin, Grimm and Schwaab (2021) similarly find evidence that unconventional monetary policy announcements had more beneficial effects on the 5-year bond yields of Italy and Spain.

Constructed as a monthly Litterman interpolation based on quarterly observations. The same holds also for \({ur}_{i,t}\).

Corporate Baa spreads relative to the 10-year US Treasury have been used as a robustness check.

Discrete scores are assigned ranging from 1 (default) to 22 (AAA). A simple average is computed across the scores of the three agencies for country i.

D’Agostino, A. and M. Ehrmann (2014) report safe-haven effects for Germany using a stochastic volatility TVP model of 10-year bond spreads with time-varying coefficients modelled as driftless random walks.

Virtually identical series are obtained using a cubic spine, with a correlation in excess of 0.999.

D’Agostino, A. and M. Ehrmann (2014) use monthly expectations by market participants, but report that availability is effectively restricted to the G7 economies.

Annex 1 provides the exact specification used in the state-space object of EViews for model 2.

Full estimates and charts for model 1 are available on request.

Paniagua et al (2017) report even stronger persistence with ρ estimates as high as 0.98.

Using event study analysis, Fengel and Neugebauer (2020) similarly report that countries with lower credit ratings experience more pronounced declines in 10-yr sovereign bond yields following APP announcements.

See, for instance, Georgoutsos and Migiakis (2018).

Moody’s seasoned Baa corporate bond yield relative to the yield of the 10-year US Treasury. Monthly observations are publicly available from the Federal Reserve Bank of St. Louis.

References

Bernoth K, Erdogan B (2012) Sovereign bond yield spreads: a time-varying coefficient approach. J Int Money Financ 31:639–656

Corradin, S., Grimm, N. and B. Schwaab (2021). “Euro area sovereign bond risk premia during the Covid-19 pandemic”, ECB Working Paper Series, no 2561

D’Agostino A, Ehrmann M (2014) The pricing of G7 sovereign bond spreads – the times, they are a-changin. J Bank Finance 47:155–176

Fendel R, Neugebauer F (2020) Country-specific euro area government bond yield reactions to ECB’s non-standard monetary policy announcements. German Econ Rev. 21(4):417–474

Georgoutsos, D. A. and P. M. Migiakis (2018). “Risk perceptions and fundamental effects on sovereign spreads”, Bank of Greece Working Paper no. 250

Malliaropulos, D. and P. M. Migiakis (2018), “Quantitative easing and sovereign bond yields: a global perspective”, Bank of Greece Working Paper no. 253

Monteiro, M. and B. Vasicek (2019). “A retrospective look at sovereign bond dynamics in the euro area”, Quarterly Report on the Euro Area, vol. 17, no.4, Institutional Paper no.100, March

Paniagua J, Sapena J, Tamarit C (2017) Sovereign debt spreads in EMU: the time-varying role of fundamentals and market distrust. J Financ Stab 33:187–206

Acknowledgements

We would like to thank Maria Gkioka for excellent research assistance and participants at an internal presentation at the Bank of Greece for very helpful comments. We are most grateful to Hiona Balfoussia, Dimitrios Louzis and two anonymous referees for very helpful comments and suggestions on an earlier draft. All remaining errors are our own. The views expressed are those of the authors and should not be interpreted as those of their respective institutions. An earlier version has beenm published online as Bank of Greece Working Paper no.291.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix

Annex 1: Specification of model 2 in the state-space object of EViews

@signal y_be = b00_be + b01*rf + b02*slope + b03_be*debt_be + b04_be*ur_be + b05_be*risk + b06_be*liq_be(-1) + b07_be*app2 + b08*rating_be(-1) + [var = exp(c(3))].

@state b00_be = c(500)*(1-c(1)) + c(1)*b00_be(-1) + c(200)*(rating_be(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b03_be = c(503)*(1-c(1)) + c(1)*b03_be(-1) + c(203)*(rating_be(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b04_be = c(504)*(1-c(1)) + c(1)*b04_be(-1) + c(204)*(rating_be(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b05_be = c(505)*(1-c(1)) + c(1)*b05_be(-1) + c(205)*(rating_be(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b06_be = c(506)*(1-c(1)) + c(1)*b06_be(-1) + c(206)*(rating_be(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b07_be = c(507)*(1-c(1)) + c(1)*b07_be(-1) + c(207)*(rating_be(-1)-rating_de(-1)) + [var = exp(c(2))].

@signal y_de = b00_de + b01*rf + b02*slope + b03_de*debt_de + b04_de*ur_de + b05_de*risk + b06_de*liq_de(-1) + b07_de*app2 + b08*rating_de(-1) + [var = exp(c(3))].

@state b00_de = c(500)*(1-c(1)) + c(1)*b00_de(-1) + c(200)*(rating_de(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b03_de = c(503)*(1-c(1)) + c(1)*b03_de(-1) + c(203)*(rating_de(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b04_de = c(504)*(1-c(1)) + c(1)*b04_de(-1) + c(204)*(rating_de(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b05_de = c(505)*(1-c(1)) + c(1)*b05_de(-1) + c(205)*(rating_de(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b06_de = c(506)*(1-c(1)) + c(1)*b06_de(-1) + c(206)*(rating_de(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b07_de = c(507)*(1-c(1)) + c(1)*b07_de(-1) + c(207)*(rating_de(-1)-rating_de(-1)) + [var = exp(c(2))].

@signal y_ie = b00_ie + b01*rf + b02*slope + b03_ie*debt_ie + b04_ie*ur_ie + b05_ie*risk + b06_ie*liq_ie(-1) + b07_ie*app2 + b08*rating_ie(-1) + [var = exp(c(3))].

@state b00_ie = c(500)*(1-c(1)) + c(1)*b00_ie(-1) + c(200)*(rating_ie(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b03_ie = c(503)*(1-c(1)) + c(1)*b03_ie(-1) + c(203)*(rating_ie(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b04_ie = c(504)*(1-c(1)) + c(1)*b04_ie(-1) + c(204)*(rating_ie(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b05_ie = c(505)*(1-c(1)) + c(1)*b05_ie(-1) + c(205)*(rating_ie(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b06_ie = c(506)*(1-c(1)) + c(1)*b06_ie(-1) + c(206)*(rating_ie(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b07_ie = c(507)*(1-c(1)) + c(1)*b07_ie(-1) + c(207)*(rating_ie(-1)-rating_de(-1)) + [var = exp(c(2))].

@signal y_gr = b00_gr + b01*rf + b02*slope + b03_gr*debt_gr + b04_gr*ur_gr + b05_gr*risk + b06_gr*liq_gr(-1) + b07_gr*app2 + b08*rating_gr(-1) + [var = exp(c(3))].

@state b00_gr = c(500)*(1-c(1)) + c(1)*b00_gr(-1) + c(200)*(rating_gr(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b03_gr = c(503)*(1-c(1)) + c(1)*b03_gr(-1) + c(203)*(rating_gr(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b04_gr = c(504)*(1-c(1)) + c(1)*b04_gr(-1) + c(204)*(rating_gr(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b05_gr = c(505)*(1-c(1)) + c(1)*b05_gr(-1) + c(205)*(rating_gr(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b06_gr = c(506)*(1-c(1)) + c(1)*b06_gr(-1) + c(206)*(rating_gr(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b07_gr = c(507)*(1-c(1)) + c(1)*b07_gr(-1) + c(207)*(rating_gr(-1)-rating_de(-1)) + [var = exp(c(2))].

@signal y_es = b00_es + b01*rf + b02*slope + b03_es*debt_es + b04_es*ur_es + b05_es*risk + b06_es*liq_es(-1) + b07_es*app2 + b08*rating_es(-1) + [var = exp(c(3))].

@state b00_es = c(500)*(1-c(1)) + c(1)*b00_es(-1) + c(200)*(rating_es(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b03_es = c(503)*(1-c(1)) + c(1)*b03_es(-1) + c(203)*(rating_es(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b04_es = c(504)*(1-c(1)) + c(1)*b04_es(-1) + c(204)*(rating_es(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b05_es = c(505)*(1-c(1)) + c(1)*b05_es(-1) + c(205)*(rating_es(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b06_es = c(506)*(1-c(1)) + c(1)*b06_es(-1) + c(206)*(rating_es(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b07_es = c(507)*(1-c(1)) + c(1)*b07_es(-1) + c(207)*(rating_es(-1)-rating_de(-1)) + [var = exp(c(2))].

@signal y_fr = b00_fr + b01*rf + b02*slope + b03_fr*debt_fr + b04_fr*ur_fr + b05_fr*risk + b06_fr*liq_fr(-1) + b07_fr*app2 + b08*rating_fr(-1) + [var = exp(c(3))].

@state b00_fr = c(500)*(1-c(1)) + c(1)*b00_fr(-1) + c(200)*(rating_fr(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b03_fr = c(503)*(1-c(1)) + c(1)*b03_fr(-1) + c(203)*(rating_fr(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b04_fr = c(504)*(1-c(1)) + c(1)*b04_fr(-1) + c(204)*(rating_fr(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b05_fr = c(505)*(1-c(1)) + c(1)*b05_fr(-1) + c(205)*(rating_fr(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b06_fr = c(506)*(1-c(1)) + c(1)*b06_fr(-1) + c(206)*(rating_fr(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b07_fr = c(507)*(1-c(1)) + c(1)*b07_fr(-1) + c(207)*(rating_fr(-1)-rating_de(-1)) + [var = exp(c(2))].

@signal y_it = b00_it + b01*rf + b02*slope + b03_it*debt_it + b04_it*ur_it + b05_it*risk + b06_it*liq_it(-1) + b07_it*app2 + b08*rating_it(-1) + [var = exp(c(3))].

@state b00_it = c(500)*(1-c(1)) + c(1)*b00_it(-1) + c(200)*(rating_it(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b03_it = c(503)*(1-c(1)) + c(1)*b03_it(-1) + c(203)*(rating_it(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b04_it = c(504)*(1-c(1)) + c(1)*b04_it(-1) + c(204)*(rating_it(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b05_it = c(505)*(1-c(1)) + c(1)*b05_it(-1) + c(205)*(rating_it(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b06_it = c(506)*(1-c(1)) + c(1)*b06_it(-1) + c(206)*(rating_it(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b07_it = c(507)*(1-c(1)) + c(1)*b07_it(-1) + c(207)*(rating_it(-1)-rating_de(-1)) + [var = exp(c(2))].

@signal y_nl = b00_nl + b01*rf + b02*slope + b03_nl*debt_nl + b04_nl*ur_nl + b05_nl*risk + b06_nl*liq_nl(-1) + b07_nl*app2 + b08*rating_nl(-1) + [var = exp(c(3))].

@state b00_nl = c(500)*(1-c(1)) + c(1)*b00_nl(-1) + c(200)*(rating_nl(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b03_nl = c(503)*(1-c(1)) + c(1)*b03_nl(-1) + c(203)*(rating_nl(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b04_nl = c(504)*(1-c(1)) + c(1)*b04_nl(-1) + c(204)*(rating_nl(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b05_nl = c(505)*(1-c(1)) + c(1)*b05_nl(-1) + c(205)*(rating_nl(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b06_nl = c(506)*(1-c(1)) + c(1)*b06_nl(-1) + c(206)*(rating_nl(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b07_nl = c(507)*(1-c(1)) + c(1)*b07_nl(-1) + c(207)*(rating_nl(-1)-rating_de(-1)) + [var = exp(c(2))].

@signal y_at = b00_at + b01*rf + b02*slope + b03_at*debt_at + b04_at*ur_at + b05_at*risk + b06_at*liq_at(-1) + b07_at*app2 + b08*rating_at(-1) + [var = exp(c(3))].

@state b00_at = c(500)*(1-c(1)) + c(1)*b00_at(-1) + c(200)*(rating_at(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b03_at = c(503)*(1-c(1)) + c(1)*b03_at(-1) + c(203)*(rating_at(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b04_at = c(504)*(1-c(1)) + c(1)*b04_at(-1) + c(204)*(rating_at(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b05_at = c(505)*(1-c(1)) + c(1)*b05_at(-1) + c(205)*(rating_at(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b06_at = c(506)*(1-c(1)) + c(1)*b06_at(-1) + c(206)*(rating_at(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b07_at = c(507)*(1-c(1)) + c(1)*b07_at(-1) + c(207)*(rating_at(-1)-rating_de(-1)) + [var = exp(c(2))].

@signal y_pt = b00_pt + b01*rf + b02*slope + b03_pt*debt_pt + b04_pt*ur_pt + b05_pt*risk + b06_pt*liq_pt(-1) + b07_pt*app2 + b08*rating_pt(-1) + [var = exp(c(3))].

@state b00_pt = c(500)*(1-c(1)) + c(1)*b00_pt(-1) + c(200)*(rating_pt(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b03_pt = c(503)*(1-c(1)) + c(1)*b03_pt(-1) + c(203)*(rating_pt(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b04_pt = c(504)*(1-c(1)) + c(1)*b04_pt(-1) + c(204)*(rating_pt(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b05_pt = c(505)*(1-c(1)) + c(1)*b05_pt(-1) + c(205)*(rating_pt(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b06_pt = c(506)*(1-c(1)) + c(1)*b06_pt(-1) + c(206)*(rating_pt(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b07_pt = c(507)*(1-c(1)) + c(1)*b07_pt(-1) + c(207)*(rating_pt(-1)-rating_de(-1)) + [var = exp(c(2))].

@signal y_fi = b00_fi + b01*rf + b02*slope + b03_fi*debt_fi + b04_fi*ur_fi + b05_fi*risk + b06_fi*liq_fi(-1) + b07_fi*app2 + b08*rating_fi(-1) + [var = exp(c(3))].

@state b00_fi = c(500)*(1-c(1)) + c(1)*b00_fi(-1) + c(200)*(rating_fi(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b03_fi = c(503)*(1-c(1)) + c(1)*b03_fi(-1) + c(203)*(rating_fi(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b04_fi = c(504)*(1-c(1)) + c(1)*b04_fi(-1) + c(204)*(rating_fi(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b05_fi = c(505)*(1-c(1)) + c(1)*b05_fi(-1) + c(205)*(rating_fi(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b06_fi = c(506)*(1-c(1)) + c(1)*b06_fi(-1) + c(206)*(rating_fi(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b07_fi = c(507)*(1-c(1)) + c(1)*b07_fi(-1) + c(207)*(rating_fi(-1)-rating_de(-1)) + [var = exp(c(2))].

@state b01 = c(501)*(1-c(1)) + c(1)*b01(-1) + [var = exp(c(2))].

@state b02 = c(502)*(1-c(1)) + c(1)*b02(-1) + [var = exp(c(2))].

@state b08 = c(508)*(1-c(1)) + c(1)*b08(-1) + [var = exp(c(2))].

Rights and permissions

About this article

Cite this article

Hondroyiannis, G., Papaoikonomou, D. The effect of Eurosystem asset purchase programmes on euro area sovereign bond yields during the COVID-19 pandemic. Empir Econ 63, 2997–3026 (2022). https://doi.org/10.1007/s00181-022-02225-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-022-02225-5