Abstract

This chapter uses an exponential generalized beta distribution of the second kind (EGB2) to model the returns on 30 Dow Jones industrial stocks. The model accounts for stock return characteristics, including fat tails, peakedness (leptokurtosis), skewness, clustered conditional variance, and leverage effect. The evidence suggests that the error assumption based on the EGB2 distribution is capable of taking care of skewness, kurtosis, and peakedness and therefore is also capable of making good predictions on extreme values. The goodness-of-fit statistic provides supporting evidence in favor of EGB2 distribution in modeling stock returns. This chapter also finds evidence that the leverage effect is diminished when higher moments are considered.

The EGB2 distribution used in this chapter is a four-parameter distribution. It has a closed-form density function and its higher-order moments are finite and explicitly expressed by its parameters. The EGB2 distribution nests many widely used distributions such as normal distribution, log-normal distribution, Weibull distribution, and standard logistic distribution.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

Notes

- 1.

- 2.

There are other names for the EGB2 distribution in other nonfinancial fields or in non-American journals; for example, generalized logistic distribution in Wu et al. (2000), z-distribution in Barndorff-Nielsen et al. (1982), the Burr-type distribution in actuarial science in Hogg and Klugman (1983), and four-parameter kappa distribution in geology in Hosking (1994).

- 3.

Dependent on the significance test of the AR(1) coefficient in the AR(1)-GARCH(1,1) model, the AR(1) term is then dropped for some stocks. The following stocks do not have an AR(1) variable: MSFT, HON, DD, GM, IBM, MO, CAT, BA, PFE, AA, DIS, MCD, JPM, and INTC. Stock PG, which is the only one that shows Q(30) any significance, adds an AR(4) variable to ensure that the autocorrelation is removed. The rest of this paper follows this pattern. Recent literature suggests that the sign of the AR(1) coefficient, ϕ 2, can be used to detect feedback trading behavior (Sentana and Wadhwani 1992; Antoniou et al. 2005). Our results show that the coefficient of AR(1) is negative.

- 4.

It is not our intention to exhaust all the non-Gaussian models in our study, which is infeasible. Rather, our strategy is to adopt a distribution that is rich enough to accommodate the features of financial data. To our knowledge, there are different types of flexible parametric distributions parallel to the EGB2 distribution to model both third and fourth moments in the literature. One family of such distributions is a skewed generalized t distribution (SGT) (Theodossiou 1998; Hueng and Brooks 2003). Special cases of SGT include generalized t distribution (McDonald and Newey 1988), skewed t distribution (Hansen 1994), and skewed generalized error distribution (SGED) (Nelson 1991). The skewness and excess kurtosis of SGT are in the range (−∞, ∞) and (1.8, ∞), respectively. Another family is inverse hyperbolic sin distribution (IHS) (Johnson 1949 and Johnson et al. 1994). The skewness and excess kurtosis of IHS is in the range (3, ∞) and (−∞, ∞). EGB2 has less coverage for skewness and excess kurtosis than SGT and IHS. However, it covers many skewness-kurtosis combinations encountered in practice and performs “impressively” in estimating the slope coefficient in a simulation (Theodossiou et al. 2007). Other families of flexible distributions are also available in the literature. But there isn’t any comparison with the EGB2 distribution.

- 5.

It should be noted that beta function here has nothing to do with the stock’s beta.

- 6.

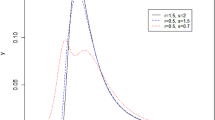

Many distributions are nested in the EGB2 distribution. Wang et al. (2001) show that the EGB2 distribution is very powerful in modeling exchange rates that have fat tails and leptokurtosis features. The EGB2 converges to normal distribution as p = q approaches infinity, to log-normal distribution when only p approaches infinity, to the Weibull distribution when p = 1 and q approaches infinity, and to the standard logistic distribution when p = q = 1. It is symmetric (called a Gumbel distribution) for p = q. The EGB2 is positively (negatively) skewed as p > q (p < q) for σ > 0.

- 7.

This can be obtained in the appendix of Wang et al. (2001).

- 8.

The digamma function is the logarithmic derivative of the gamma function; the trigamma function is the derivative of the digamma function.

- 9.

Stock C (CitiGroup) in Table 80.1 began its trading data on Oct 29, 1986. Within this period, only one stock has one missing value. Stock MO (Philips Morris Co.) was not traded on May 25, 1994, because of “pending news which could affect the stock price.” Philip Morris’ board was meeting to announce whether the company would split its food and tobacco units on May 25, 1994. In this sample period, the most striking event is the market crash on October 19, 1987. This paper considers the 1987 market crash as an outlier in the later part. The week of the 9–11 terrorist attacks has only 1 day of trading information and is incorporated into the next week.

- 10.

http://www.federalreserve.gov/releases/H15/data.htm#top, Treasury bill secondary market rates (serial: tbsm3m) are the averages of the bid rates quoted on a bank discount basis by a sample of primary dealers who report to the Federal Reserve Bank of New York. The rates reported are based on quotes at the official close of the US government securities market for each business day.

- 11.

The sign of the skewness coefficient is related to data frequency. The skewness of the weekly return has nothing to do with the skewness of the daily return. For example, the stock HON (index = 2) shows significant positive skewness in its daily return but significant negative skewness in its weekly return.

- 12.

The skewness coefficient is the relation between the second order moment and the third order moment. It is calculated by \( \frac{T}{\left(T-1\right)\left(T-2\right){\sigma}^3}{\displaystyle \sum {\left({x}_i-\mu \right)}^3} \) where μ is the mean of the sample. The literature about the positive and negative values of the distribution skewness is confusing. The skewness in our study is based on the distribution’s moments (Kenney and Kee** 1962).

- 13.

All the non-normality features are more remarkable in daily data but less so in monthly data. This is consistent with Brown and Warner’s (1985) report that the non-normal features tend to vanish in low-frequency data, such as monthly observations. Even so, subject to individual monthly stock returns, the Jarque-Bera test rejects the normality for 23 of the 30 stocks at the 1 % level.

- 14.

The standardized residuals are obtained by dividing the estimated regression residuals by its conditional standard deviation. Standardizing the error term makes the distribution comparison feasible. Mean and variance are not reported in the table due to the use of normalization.

- 15.

To deal with the skewness, a number of skewed t distributions have been proposed (Theodossiou 1998; Hueng and Brooks 2003). One obvious drawback of a skewed t distribution in our study is the outcome of its peakedness measurement, which displays platykurtosis (flat topped in density). This appears to be the opposite of the leptokurtic stock returns. For this reason, we do not report results from the GARCH model based on a skewed t distribution in order to focus on the EGB2 distribution. However, the results are available upon request.

- 16.

Some refinement of the model is contained in the following section.

- 17.

Engle et al. (1987) suggest putting a conditional volatility variable in the mean equation, which is called the GARCH-M model. However, the expected sign of the conditional variance variable is uncertain, according to literature surveys. Since we do not find its statistical significance in our empirical experiment (not reported), the conditional mean term is excluded from our test equation.

- 18.

Longin (1996) proposes the use of a Frechet distribution, which is able to highlight those extreme price movements. However, his model does not cover whole return distributions but only extreme values.

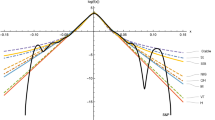

- 19.

Normal distribution is a special case of the EGB2 distribution. A likelihood ratio rest suggests that there is significant improvement in the fit of the EGB2 distribution over that of the normal distribution.

- 20.

The chi-square test is an alternative to the Anderson-Darling and Kolmogorov-Smirnov goodness-of-fit tests. The chi-square test and Anderson-Darling test make use of the specific distribution in calculating critical values. This has the advantage of allowing a more sensitive test and the disadvantage that critical values must be calculated for each distribution.

- 21.

Our sample contains 999 observations; 40 intervals are used. Each group (data class) has theoretically 25 observations. The degrees of freedom are 37, 38, and 39 for the EGB2 distribution, the t distribution and the normal distribution, respectively. (The chi-squared critical values are given in the note in Table 80.6.)

References

Akgiray, V. (1989). Conditional heteroskedasticity in time series of stock returns: Evidence and forecasts. Journal of Business, 62, 55–80.

Amihud, Y., & Mendelson, H. (1987). Trading mechanism and stock returns: An empirical investigation. Journal of Finance, 42, 533–553.

Andersen, J. V., & Sornette, D. (2001). Have your cake and eat it too: Increasing returns while lowering large risks! Journal of Risk Finance, 2, 70–82.

Antoniou, A., Koutmos, G., & Pericli, A. (2005). Index futures and positive feedback trading: Evidence from major stock exchanges. Journal of Empirical Finance, 12, 219–238.

Avramov, D. (2002). Stock return predictability and model uncertainty. Journal of Financial Economics, 64, 423–458.

Baillie, R. T., & DeGennaro, R. P. (1990). Stock returns and volatility. Journal of Financial and Quantitative Analysis, 25, 203–215.

Bali, T. G., Mo, H., & Tang, Y. (2008). The role of autoregressive conditional skewness and kurtosis in the estimation of conditional VaR. Journal of Banking & Finance, 32, 269–282.

Barndorff-Nielsen, O., Kent, J., & Sorensen, M. (1982). Normal variance-mean mixtures and z distributions. International Statistical Review, 50, 145–159.

Bollerslev, T. (1987). A conditionally heteroskedastic time series model for speculative prices and rates of return. Review of Economics and Statistics, 69, 542–547.

Bollerslev, T., Chou, R. Y., & Kroner, K. F. (1992). ARCH modeling in finance: A review of the theory and empirical evidence. Journal of Econometrics, 52, 5–59.

Bollerslev, T. R., Engle, F., & Nelson, D. B. (1994). ARCH model. In Engle & McFadden (Eds.), Handbook of econometrics (Vol. IV). Amsterdam: North Holland.

Boothe, P., & Glassman, D. (1987). The statistical distribution of exchange rates. Journal of International Economics, 22, 297–319.

Box, G. E. P., & Tiao, G. C. (1975). Intervention analysis with applications to economic and environmental problem. Journal of the American Statistical Association, 70, 70–79.

Boyer, B., Mitton, T., & Vorkink, K. (2010). Expected idiosyncratic skewness. Review of Financial Studies, 23, 169–202.

Brooks, C., Burke, S., Heravi, S., & Persand, G. (2005). Autoregressive conditional kurtosis. Journal of Financial Econometrics, 3, 399–421.

Brown, S., & Warner, J. (1985). Using daily stock returns: The case of event studies. Journal of Financial Economics, 14, 3–31.

Clark, P. K. (1973). A subordinated stochastic process model with finite variance for speculative prices. Econometrica, 41, 135–155.

Conrad, J. S., Dittmar, R. F., & Ghysels, E. (2009). Ex ante skewness and expected stock returns. Available at SSRN: http://ssrn.com/abstract=1522218 or http://dx.doi.org/10.2139/ssrn.1522218 (Dec 11).

Cvitanic, J., Polimenis, V., & Zapatero, F. (2008). Optimal portfolio allocation with higher moments. Annals Finance, 4, 1–28.

Engle, R., Lilien, D., & Robins, R. (1987). Estimating time-varying risk premia in the term structure: The ARCH-M model. Econometrica, 55, 391–408.

Fama, E. (1965). The behavior of stock-market prices. The Journal of Business, 38, 34–105.

Fama, E., & French, K. (1996). Multifactor explanations of asset pricing anomalies. Journal of Finance, 51, 55–84.

French, K., Schwert, G. W., & Stambaugh, R. (1987). Expected stock returns and volatility. Journal of Financial Economics, 19, 3–29.

Glosten, L. R., Jagannathan, R., & Runkle, D. E. (1993). On the relation between the expected value and the volatility of the normal excess return on stocks. Journal of Finance, 48, 1779–1801.

Hansen, B. (1994). Autoregressive conditional density estimation. International Economic Review, 35, 705–730.

Hansen, C. B., McDonald, J. B., & Theodossiou, P. (2006). Some flexible parametric models for partially adaptive estimators of econometric models (Working Paper). Brigham Young University.

Harvey, C. R., & Siddique, A. (1999). Autoregressive conditional skewness. Journal of Financial and Quantitative Analysis, 34, 465–487.

Harvey, C. R., & Siddique, A. (2000). Conditional skewness in asset pricing tests. Journal of Finance, 55, 1263–1295.

Harvey, C. R., Liechty, J. C., Liechty, M. W., & Muller, P. (2003). Portfolio selection with higher moments. Quantitative Finance, 10(5), 469–485.

Hogg, R. V., & Klugman, S. A. (1983). On the estimation of long tailed skewed distributions with actuarial applications. Journal of Econometrics, 23, 91–102.

Hosking, J. R. M. (1994). The four-parameter kappa distribution. IBM Journal of Research and Development, 38, 251–258.

Hueng, C. J., & Brooks, R. (2003). Forecasting asymmetries in aggregate stock market returns: Evidence from higher moments and conditional densities (Working Paper, WP02-08-01). The University of Alabama. http://scholar.google.com.hk/citations?view_op=view_citation&hl=en&user=Rw22qOoAAAAJ&citation_for_view=Rw22qOoAAAAJ:IjCSPb-OGe4C

Hueng, C. J., & McDonald, J. (2005). Forecasting asymmetries in aggregate stock market returns: Evidence from conditional skewness. Journal of Empirical Finance, 12, 666–685.

Johnson, N. L. (1949). Systems of frequency curves generated by methods of translation. Biometrica, 36, 149–176.

Johnson, H., & Schill, M. J. (2006). Asset pricing when returns are nonnormal: Fama-French factors versus higher order systematic comoments. Journal of Business, 79, 923–940.

Johnson, N. L., Kotz, S., & Balakrishnan, N. (1994). Continuous univariate distributions (2nd ed., Vol. 1). New York: Wiley.

Jurczenko, E., & Maillet, B. (2002). The four moment capital asset pricing model: Some basic results (Working Paper). Paris: Ecole supérieure de commerce de Paris.

Kenney, J. F., & Kee**, E. S. (1962). Skewness. §7.10 In Mathematics of statistics (pp. 100–101). Princeton: Van Nostrand.

Liu, S. M., & Brorsen, B. (1995). Maximum likelihood estimation of a GARCH – STABLE model. Journal of Applied Econometrics, 10, 273–285.

Lo, A., & MacKinlay, A. C. (1990). Data-snoo** biases in tests of financial asset pricing models. Review of Financial Studies, 3, 431–467.

Longin, F. (1996). The asymptotic distribution of extreme stock market returns. Journal of Business, 63, 383–408.

Malevergne, Y., & Sornette, D. (2005). Higher moment portfolio theory. The Journal of Portfolio Management, 31(4), 49–55.

Mandelbrot, B. B. (1963). The variation of certain speculative prices. Journal of Business, 36, 394–419.

McCulloch, J. H. (1985). Interest-risk sensitive deposit insurance premia: Stable ACH estimates. Journal of Banking and Finance, 9, 137–156.

McDonald, J. B. (1984). Some generalized functions for the size distribution of income. Econometrica, 52, 647–663.

McDonald, J. B. (1991). Parametric models for partially adaptive estimation with skewed and leptokurtic residuals. Economics Letters, 37, 273–278.

McDonald, J. B., & Newey, W. K. (1988). Partially adaptive estimation of regression models via the generalized t distribution. Econometric Theory, 4, 428–457.

McDonald, J. B., & Xu, Y. J. (1995). A generalization of the beta distribution with applications. Journal of Econometrics, 66, 133–152.

Mittnik, S., Rachev, S., Doganoglu, T., & Chenyao, D. (1999). Maximum likelihood estimation of stable paretian models. Mathematical and Computer Modelling, 29, 275–293.

Nelson, D. B. (1991). Conditional heteroskedasticity in asset return: A new approach. Econometrica, 59, 347–370.

Officer, R. (1972). The distribution of stock returns. Journal of the American Statistical Association, 67, 807–812.

Patton, A. J. (2004). On the out-of-sample importance of skewness and asymmetric dependence for ass et al location. Journal of Financial Econometrics, 2, 130–168.

Pena, D., Tiao, G. C., & Tsay, R. S. (2001). A course in time series analysis. New York: Wiley.

Ranaldo, A., & Favre, L. (2005). How to price hedge funds: From two- to four-moment CAPM (UBS Research Paper). SSRN: http://ssrn.com/abstract=474561.

Sentana, E., & Wadhwani, S. (1992). Feedback traders and stock return autocorrelations: Evidence from a century of daily data. Economic Journal, 102, 415–425.

Snedecor, G. W., & Cochran, W. G. (1989). Statistical methods. Ames: Iowa State Press.

Tang, G. Y. N. (1998). Monthly pattern and portfolio effect on higher moments of stock returns: Empirical evidence from Hong Kong. Asia-Pacific Financial Markets, 5, 275–307.

Theodossiou, P. (1998). Financial data and the skewed generalized t distribution. Management Science, 44, 1650–1661.

Theodossiou, P., McDonald, J. B., & Hansen, C. B. (2007). Some flexible parametric models for partially adaptive estimators of econometric models. Economics: The Open-Access, Open-Assessment E-Journal, 1(2007-7), 1–20. http://dx.doi.org/10.5018/economics-ejournal.ja.2007-7.

Tsay, R. C., Peña, D., & Pankratz, A. (2000). Outliers in multivariate time series. Biometrica, 87, 789–804.

Vinod, H. D. (2004). Ranking mutual funds using unconventional utility theory and stochastic dominance. Journal of Empirical Finance, 11, 353–377.

Wang, K. L., Fawson, C., Barrett, C. B., & McDonald, J. B. (2001). A flexible parametric GARCH model with an application to exchange rates. Journal of Applied Econometrics, 16, 521–536.

Wu, J. W., Hung, W. L., & Lee, H. M. (2000). Some moments and limit behaviors of the generalized logistic distribution with applications. Proceedings of the National Science Council ROC, 24, 7–14.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Appendix 1

Appendix 1

80.1.1 Delta Method and Standard Errors of the Skewness and Kurtosis Coefficients of the EGB2 Distribution

The delta method, in its essence, expands a function of a random variable about its mean, usually with a one-step Taylor approximation, and then takes the variance. For example, if we want to approximate the variance of G(x) where x is a random variable with mean μ and G(x) is differentiable, we can try

so that

where G′() = dG/dX. This is a good approximation only if x has a high probability of being close enough to its mean so that the Taylor approximation is still good.

The nth central moments of the EGB2 distribution is given by

where ψn is nth order a polygamma function. Correspondingly, the skewness coefficient is given by

The variance of the skewness coefficient by the delta method is given by

where

Similarly, the excess kurtosis coefficient is given by

The variance of the kurtosis coefficient by the delta method is given by

where

In the equations above, high-order polygamma functions are involved. A polygamma function is the nth normal derivative of the logarithmic derivative of Γ(z):

which, for n > 0, can be written as

which is used to calculate polygamma functions in this chapter.

Note: This appendix is based on the paper by Wang et al. (2001). However, there are typos and errors in that paper. The standard deviation formula for skewness used by Wang et al. (2001) is incorrect (see g′q(p,q) equation in the paper at http://www.econ.queensu.ca/jae/2001-v16.4/wang-fawson-barrett-mcdonald/Appendix4_delta_derivations.pdf). We therefore provide this appendix. Accordingly, as we reviewed and replicated that paper by using the data supplied by the Journal of Applied Econometrics, the EGB2 distribution doesn’t remove the skewness problem completely as shown in their Table 3. In addition, there is a computational error in the JPY series, so that its kurtosis has not been resolved either.

Rights and permissions

Copyright information

© 2015 Springer Science+Business Media New York

About this entry

Cite this entry

Chiang, T.C., Li, J. (2015). Modeling Asset Returns with Skewness, Kurtosis, and Outliers. In: Lee, CF., Lee, J. (eds) Handbook of Financial Econometrics and Statistics. Springer, New York, NY. https://doi.org/10.1007/978-1-4614-7750-1_80

Download citation

DOI: https://doi.org/10.1007/978-1-4614-7750-1_80

Published:

Publisher Name: Springer, New York, NY

Print ISBN: 978-1-4614-7749-5

Online ISBN: 978-1-4614-7750-1

eBook Packages: Business and Economics